Nikada/iStock Unreleased via Getty Images

With the Fed set to embark on its long-awaited tightening cycle, bond yields have been steadily marching higher. Not surprisingly, the slow grind higher in yields has caused a bit of a bumpy ride for the Nasdaq 100 (QQQ). Down more than 10% year-to-date, the triple-Qs’ dreadful performance might cause an investor to assume the ETF’s major components were also struggling of late. While that would be true of numbers two through five in the top weightings – Microsoft (MSFT), Amazon (AMZN), Meta (FB), and Tesla (TSLA) are sporting year-to-date declines of 10.66%, 6.12%, 34.29%, and 12.71% respectively – numero uno, Apple (AAPL), has bucked the trend, down a mere 2.69% year-to-date.

Apple’s stock is living its best life, with a fiscal-year 2022 P/E ratio above 28, and future earnings-growth projections of just 8.5% and 6.9% for fiscal years 2023 and 2024. The company has been consistently rewarding investors with dividends and dividends hikes for nearly ten years and can still get away with paying a paltry 0.51%. But can you blame them? When you are king, no valuation is too high, no dividend yield is too low, and slowing earnings growth is irrelevant … until it isn’t.

As an investor with money to put to work, I’ve been scouring the markets far and wide looking for the best combinations of value, growth, and yield. When I got to Apple, the aforementioned valuation, miniscule dividend yield, and slowing future earnings projections sent me quickly climbing the capital structure. And as I climbed, I noticed something enticing.

Apple has a laundry list of CUSIPs (i.e., debt, bonds, notes), and of the 52 I examined, one stood out to me as the perfect combination of yield, duration, coupon, price, and spread-to-Treasury. At the time of this writing, the bond in question offers a fairly attractive 3.45% yield, nearly seven times higher than the stock’s awful 0.51% dividend yield.

Trading roughly 100 basis points over its benchmark Treasury, Apple’s AAA-rated CUSIP 037833BA7, maturing February 9, 2045, sports a 3.45% coupon and a bid-ask spread currently straddling par (i.e., 100 cents-on-the-dollar). I realize 3.45% doesn’t sound like a lot, but we are talking about a triple-A bond, not a triple-B. As an aside, if the mid-to-upper 4%s sounds more enticing, there’s one bond in particular I have in mind for a future commentary.

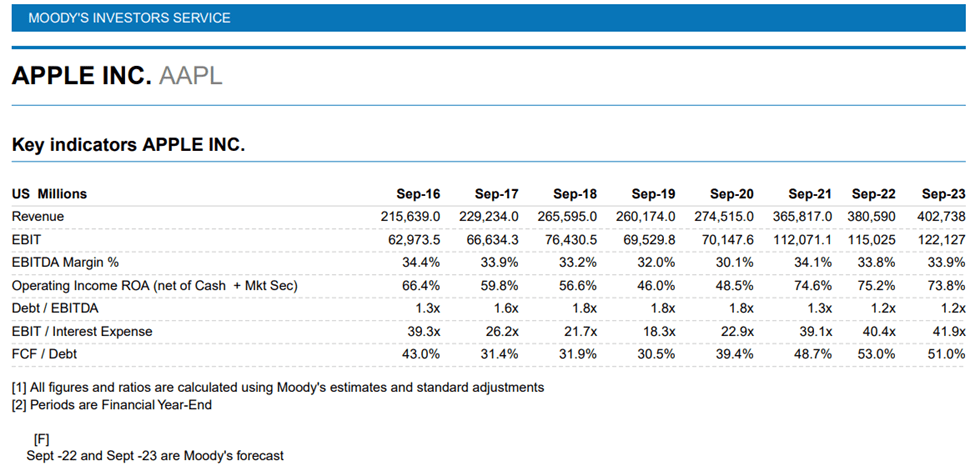

For investors worried about Apple’s financials, here’s a look at some key indicators, as calculated by Moody’s Investors Service:

Moody’s Investors Service

Current year debt-to-EBITDA of 1.2x and EBIT/Interest Expense of 40.4x are a bond investor’s dream. Combine that with massive free-cash flow, Apple’s huge ecosystem, strong brand recognition, and over 1.65 billion active devices, and I can live with Apple’s $161.685 billion of total non-current liabilities. But why not just buy the stock?

Here’s why I think it might actually make sense to go with the bond instead.

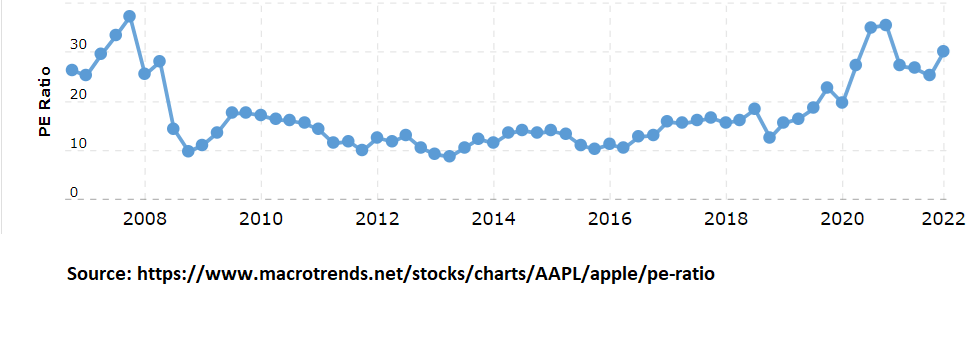

Let’s start by taking a look at the stock’s P/E-ratio trend over time. Notice the ebbs and flows, especially within the 10-to-20 region, a region in which the stock has spent most of its post-iPhone-launch existence. Also, notice the strong P/E-ratio uptrend that began in late 2018 when interest rates peaked. Furthermore, notice the acceleration of the P/E-ratio uptrend in 2020, breaking out above its historical range when the Fed went all-in on easy-money. The most recent easy-money period helped drive Apple’s P/E ratio well above the upper end of its long-held 10-to-20 range. With the Fed now about to embark on a tightening cycle, there’s a good chance the P/E ratio will act as a stock-price inhibitor for the foreseeable future.

Macrotrends.net

Given the aforementioned Apple bond currently yields 294 basis points more than Apple’s stock, the stock will need to rise by 67.55% from current values to break even with the bond over the bond’s remaining life. Yes, a dividend hike will change that equation, as would a bond investor averaging into the bond at ever higher yields or reinvesting the interest into the same bond. As those scenarios are unique to each investor and hard to forecast, for simplicity’s sake and for the purpose of demonstration, let’s start by sticking to the idea that moving forward, the bond has a 294-basis points advantage over the stock.

Apple’s $2.82 trillion market cap, combined with the bond’s initial 67.55% lifetime income advantage over the stock, means the stock’s market cap will need to grow to at least $4.73 trillion before investors begin to realize an equity premium over the bond. While Apple is likely to increase its dividend over time, it would require a 10% compound annual growth rate in Apple’s dividend over the next 20 years just to match the yield of the bond. Given Apple’s dividend-growth history, I would argue a 10% compound-annual-growth rate in the dividend is unachievable. Therefore, for investors putting money to work at current levels, I feel confident the bond will retain an income advantage over the stock over the entire life of the bond. The question is simply how much can Apple’s dividend hikes eat into the bond’s advantage. As dividend hikes eat into the bond’s income advantage, the breakeven market cap for equity investors (from an opportunity-cost perspective) will slowly decline from its $4.73 trillion starting point.

In most cases, equity investors do not simply strive to match a bond’s return. Otherwise, those investors would simply buy the bond in the first place. Over the life of Apple’s 2045-maturing bond, do I think Apple’s stock will outperform the bond by an amount the average equity investor would find acceptable? I think it is unlikely, and I think this for one simple reason. Apple, as the world’s largest company by valuation, would have to grow to such an astounding market value that as it grows closer to breaking even with the bond, let alone outperforming the bond by an amount the average equity investor would find acceptable, the cries from Congress to break the company up will reach fever pitch and eventually result in the company’s split.

Whether or not you agree with my opinion, I hope it demonstrates that the starting income advantage of Apple’s February 9, 2045-maturing bond of nearly 7x over the stock makes the bond worth a serious look for someone with new money to put to work on Apple’s capital structure. If Apple’s market cap eventually needs to cross $4 trillion just to have a chance to break even with the bond, it means the market cap would likely need to approach $8 trillion over the life of the bond in order to offer an acceptable equity risk premium for most investors. Anything is possible, but I’d rather clip coupons in Apple and put my equity-growth dollars elsewhere.

Finally, for those investors who decide it’s worth clipping coupons in the aforementioned bond, keep in mind that just as equity investors buy the dip and average into stocks, so too can bond investors do the same as yields rise and prices fall.