Adrian Vidal/iStock Editorial via Getty Images

The rise of cryptocurrencies has opened up an entirely new, and now very accessible world of alternative assets. While cryptos like Bitcoin (BTC-USD) have been around for years, only very recently have they become much more mainstream in terms of institutional adoption, and accessibility for the average investor.

This has driven unprecedented interest in the asset class itself, with Bitcoin remaining the OG and largest in the universe of cryptos. Bitcoin has had a tough few months since hitting its all-time high in November of last year, but for those of us that are bullish longer-term on Bitcoin, these selloffs present buying chances.

But if you’re looking to get into Bitcoin investing for the first time, or simply looking for the best spot for your money to take advantage of a rising Bitcoin price over time, we can pose a timely question; is it better to own the coin itself, or those companies that have ties to mining instead? The question is analogous to considering whether to own gold itself, or the gold miners, and the “correct” answer depends on many factors that change and shift over time.

In this article, we’ll first take a glance at my outlook for Bitcoin itself, and then a slew of miners to see if it’s better to stick with the coin, or if perhaps there is more potential upside to owning a miner.

Bitcoin winter? Maybe the spring thaw

Before we get to the discussion on Bitcoin, let me just start by saying I’m by no means a Bitcoin or cryptocurrency perma-bull. There are those that are either always bearish or always bullish on any asset class you can imagine, and these views are generally driven by some sort of emotional attachment to the asset class. My philosophy is not to have emotional attachments to asset classes, and instead, follow the evidence.

In the case of Bitcoin, I’ve been bullish plenty of times in the past couple of years because that’s what the charts told me. And when I’m wrong – which has also happened plenty of times – I take a small loss and move on to the next trade. It really is that simple.

Since the ATH in November, we’ve obviously been in a bearish period, and that’s fine; those things happen. But the important thing to keep in mind is that I’m not a crypto believer that thinks fiat money is dead; I’m just trying to follow the charts to make myself and all of you some (fiat) money.

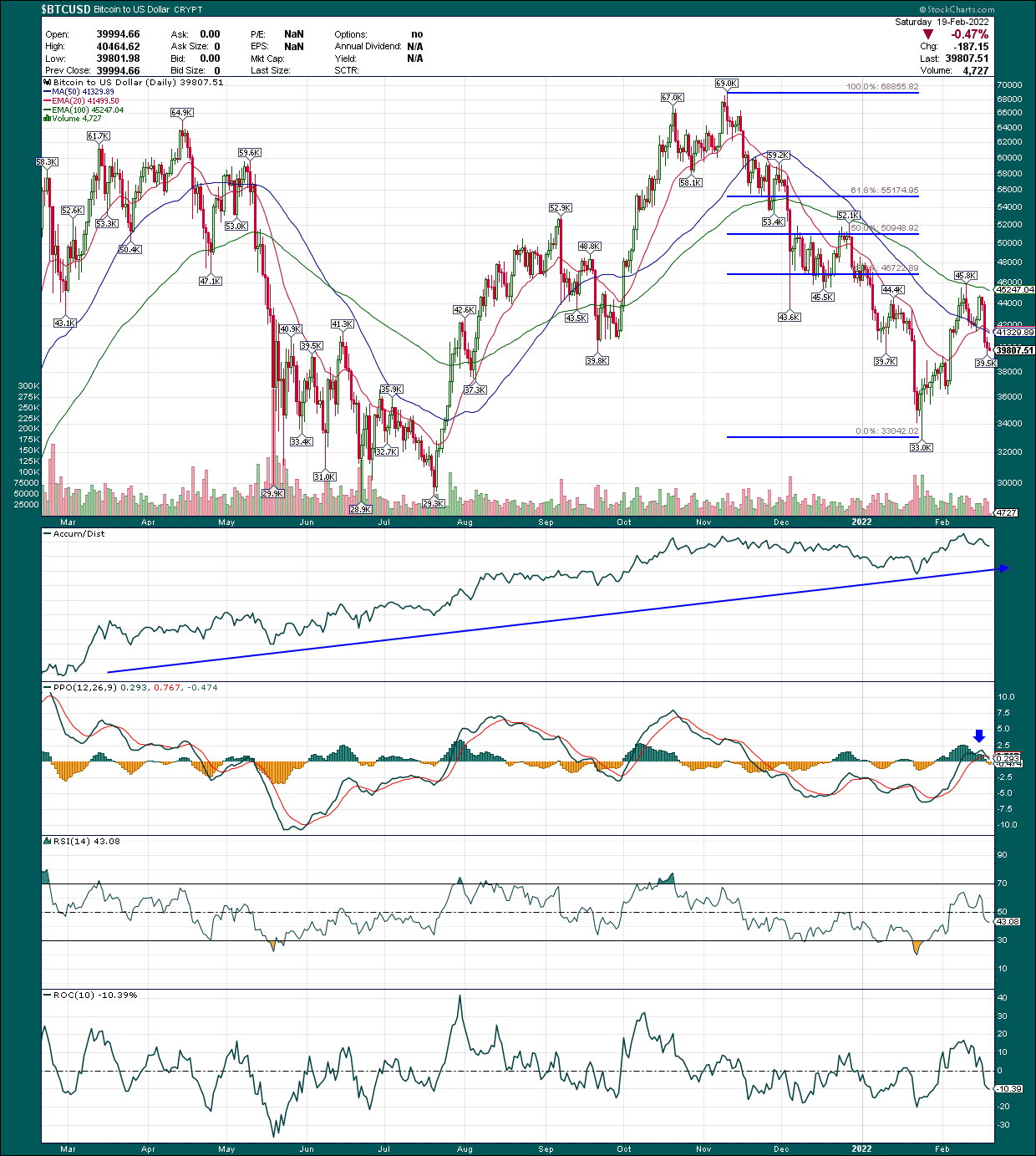

Now that we have that out of the way, let’s get to the meat of the discussion. I’ve seen numerous commentators on Bitcoin state we’re in a “Bitcoin Winter”, implying that the ATH that was made in November has set off a protracted and deep bear market that may take years to recover. I don’t subscribe to that theory, mostly because when I look at the chart of Bitcoin, I just don’t see that many reasons to continue to be bearish. Below we have a one-year daily chart to kick us off.

StockCharts

Starting with the price chart, we can see the digital coin’s pullback from the ATH to the January low was $36k, or just over 50%. That’s ugly, but keep in mind that cryptos have much larger rallies and pullbacks than stock indices, for instance. If volatility is something you aren’t into, that’s totally fine, but crypto investing is not for you.

However, I take the other view; volatility like this creates numerous opportunities on both sides of the trade, and that means there are numerous opportunities to make money. At the moment, I think we’re much closer to a local bottom than we are the top, given we’re still ~$30k off from the ATH, even after a big rebound rally. This isn’t the rally, though; I do think this is a rebound that will see another leg down before we go higher.

I noted the Fibonacci levels from the ATH, and you can see we made it almost exactly to the 38% retracement of the decline, which is certainly not unprecedented. What I expect now is that we’ll make one more low, probably in the area of $35k, before the next bullish phase can begin.

Why am I confident we’re not that far away? Price action is always the biggest indicator you can have, but if we look at the secondary ones, such as momentum, I think there’s a case that sellers are nearing exhaustion.

First, the accumulation/distribution line remains near its highs despite very weak price action for months. That means that buyers continue to step in on weakness, which is what you see with leading stocks/indices/coins/etc. If you don’t see dip-buyers, it means the asset has fallen out of favor with big money investors; there is no such issue with Bitcoin.

The PPO is my favorite momentum indicator, and it is showing positive divergences since the first corrective low was made in December of last year. Essentially, that means that momentum is flat or rising while the asset is making new lows. This is bullish because it means selling pressure is abating, and that’s how you know the bottoming process has begun. We can see the PPO actually made it back into positive territory on this last bounce attempt, and while I do think Bitcoin has some weakness ahead in the near-term, this behavior with momentum is exactly what I want to see to know the coin is likely to bottom, and subsequently start its next bullish phase.

To sum it up, I think we are likely to see a bit of near-term weakness as the last of the sellers are shaken out, and then, we could see a pretty epic bullish phase that takes us back to the ATH, at a minimum.

Now, the question becomes, do you buy Bitcoin, or is there a better alternative with more upside potential? To answer that, let’s take a look at some of the miners that are available to investors today.

Bitcoin mining stocks: Separating the wheat from the chaff

There’s a variety of approaches one could take to find the best crypto miner for your money, but I’m one that favors following the money rather than strictly fundamental analysis. As such, we’ll begin our discussion of the miners by looking at their price charts and seeing which one(s) Wall Street has anointed as leaders. From there, we can tell which may be setup the best for leveraging an eventual Bitcoin rally to a higher share price.

Our first miner is Argo Blockchain (ARBK), a company that is still very much in the early stages of its scaling efforts.

Seeking Alpha

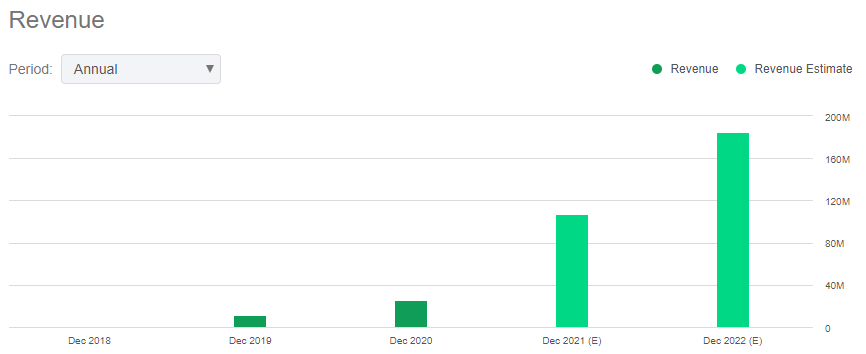

The company had essentially no revenue in 2018, but is on pace to produce about $185 million this year. With its current market cap at $433 million, it’s priced at 2.3X forward sales. That’s actually pretty reasonable among the miners, so that’s one point in Argo’s corner.

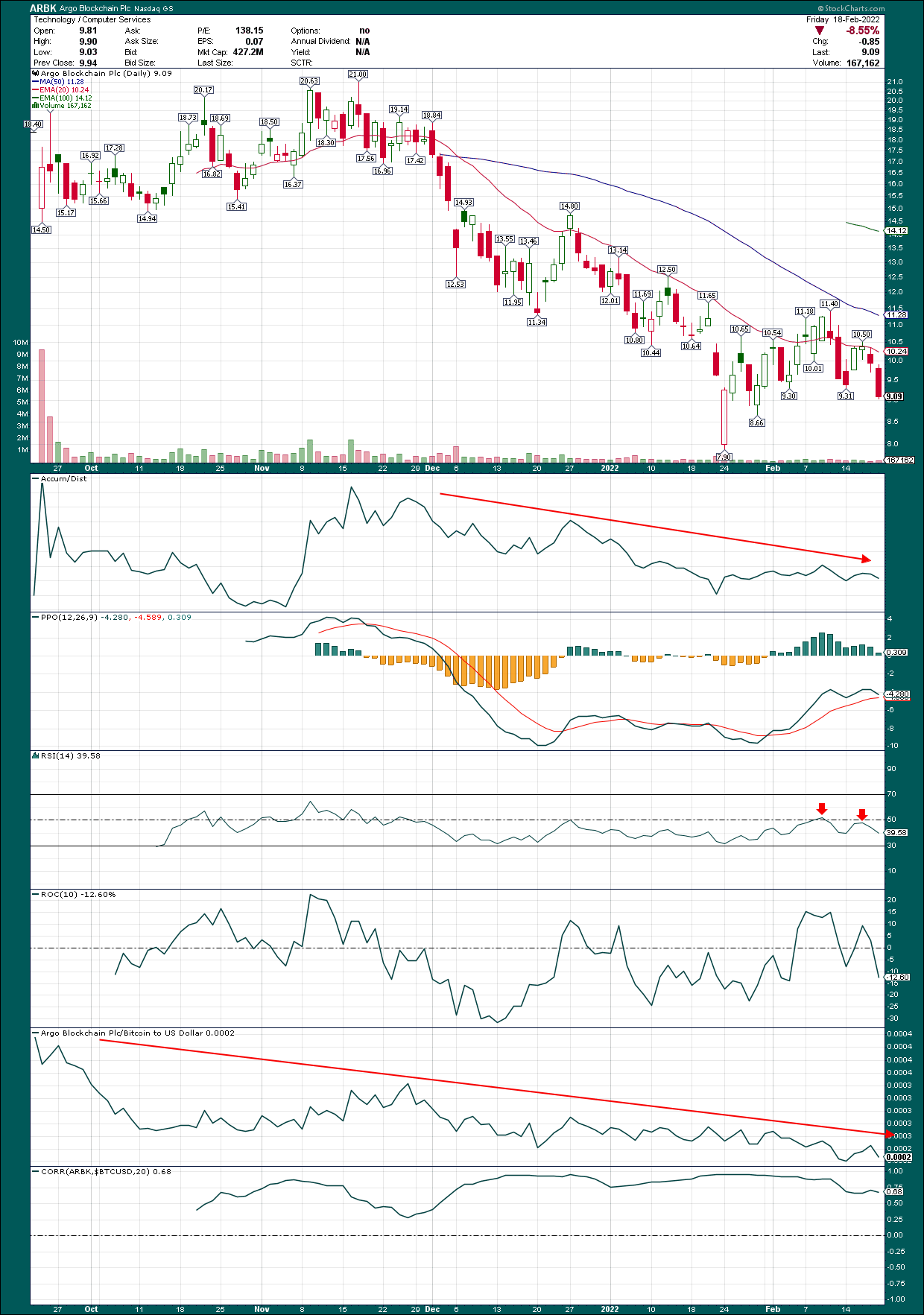

Now, let’s take a look at its chart, which I find to be fairly unattractive.

StockCharts

Argo is off by more than half in recent months, which is unsurprising given the action we’ve seen in Bitcoin itself. But when I look at the same indicators we looked at for Bitcoin itself – the PPO, the A/D line – they are showing sustained weakness, not strength. Essentially, this means that Argo is in sell first, ask questions later mode. Contrast that with Bitcoin, which I explained above is in the opposite sort of phase.

In the bottom panel, I’ve plotted Argo’s performance against the coin itself, as well as its correlation to Bitcoin. These are important for two reasons. First, they give us a great look into whether the miner tracks Bitcoin’s movements, and to what extent. And second, the point of this analysis is to determine whether buying the coin is better or worse than buying a miner.

For Argo, the correlation is okay, but not great. It’s 0.68 on a 20-day basis, although it is usually higher than that. On the relative performance chart, Argo has continued to lose ground to Bitcoin. That essentially means Argo’s tracking error to Bitcoin is pretty high, and in the wrong direction. That’s a bad combination, and for that reason, Argo is out of the running.

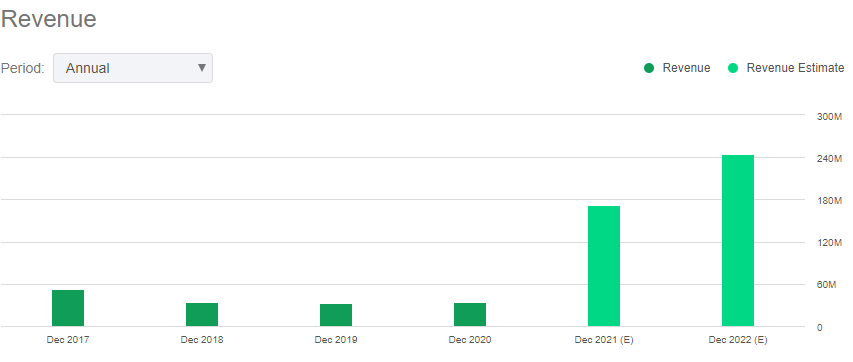

Next up is Bitfarms (BITF), a miner that is further along in its revenue journey in some ways, with 2022 revenue slated to come in at $244 million.

Seeking Alpha

With its $679 million market cap, BITF trades for 2.8X forward sales, which is higher than Argo, but better than most of its competitors; more on that later.

Now, let’s take a look at BITF’s chart and follow the money to assess its relative attractiveness.

StockCharts

BITF is a very long way from its former highs, and all of the indicators are in pretty rough shape. I won’t explain all of them again but I’ve annotated the indicators where you should focus, and none of the annotations are positive.

Relative strength to Bitcoin is pretty awful, although its correlation is very high at 0.88. On this measure, it’s better than Argo at tracking Bitcoin, but that’s where the positives end. Just like Argo, the chart on Bitfarms is far too weak, and it’s underperforming the coin, so this one is out too.

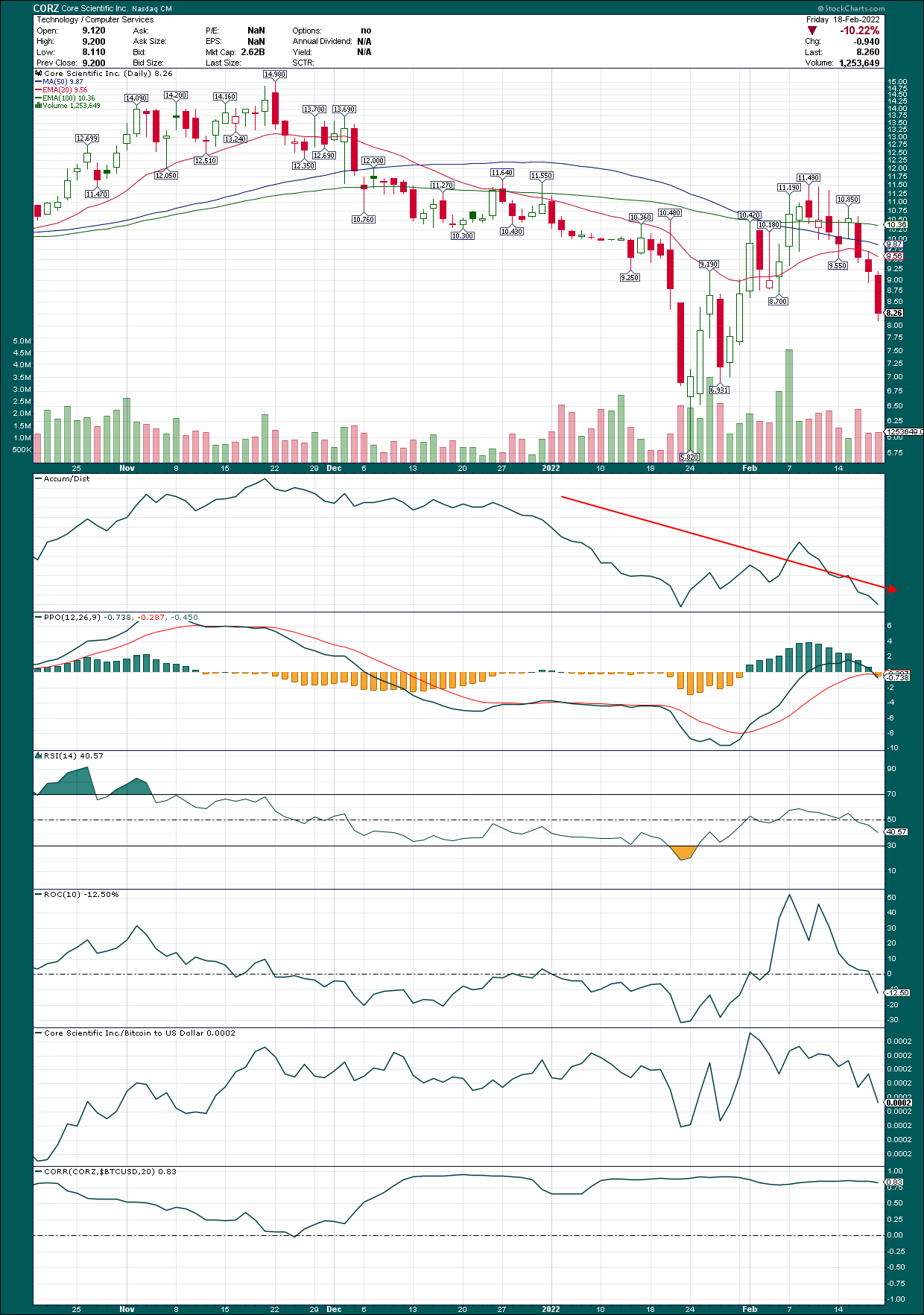

Next up is Core Scientific (CORZ), a newly public entry into the mining fray via a SPAC that has been trading for only a few months. Even so, Core Scientific has some scale in an industry where scale is difficult to come by. The company’s January update showed 1,077 Bitcoins mined in January, bringing its total holdings to 6,373 coins. That’s about $43 million in raw production in January, and ~$250 million of coins on the balance sheet. Core Scientific is one that mines Bitcoin to hold it, mostly, so keep that in mind if you’re buying.

Stock Charts

Like the others we’ve looked at so far, Core Scientific’s chart is pretty ugly. It’s down nearly half since its high, but also appears to be in a bottoming process at the moment. The A/D line is weak, but momentum looks good in the face of weak price action, and the stock’s performance against and correlation to Bitcoin are in pretty good shape. Given these factors, and the scale the company is operating with ($500+ million in annualized production), Core Scientific takes the top spot thus far.

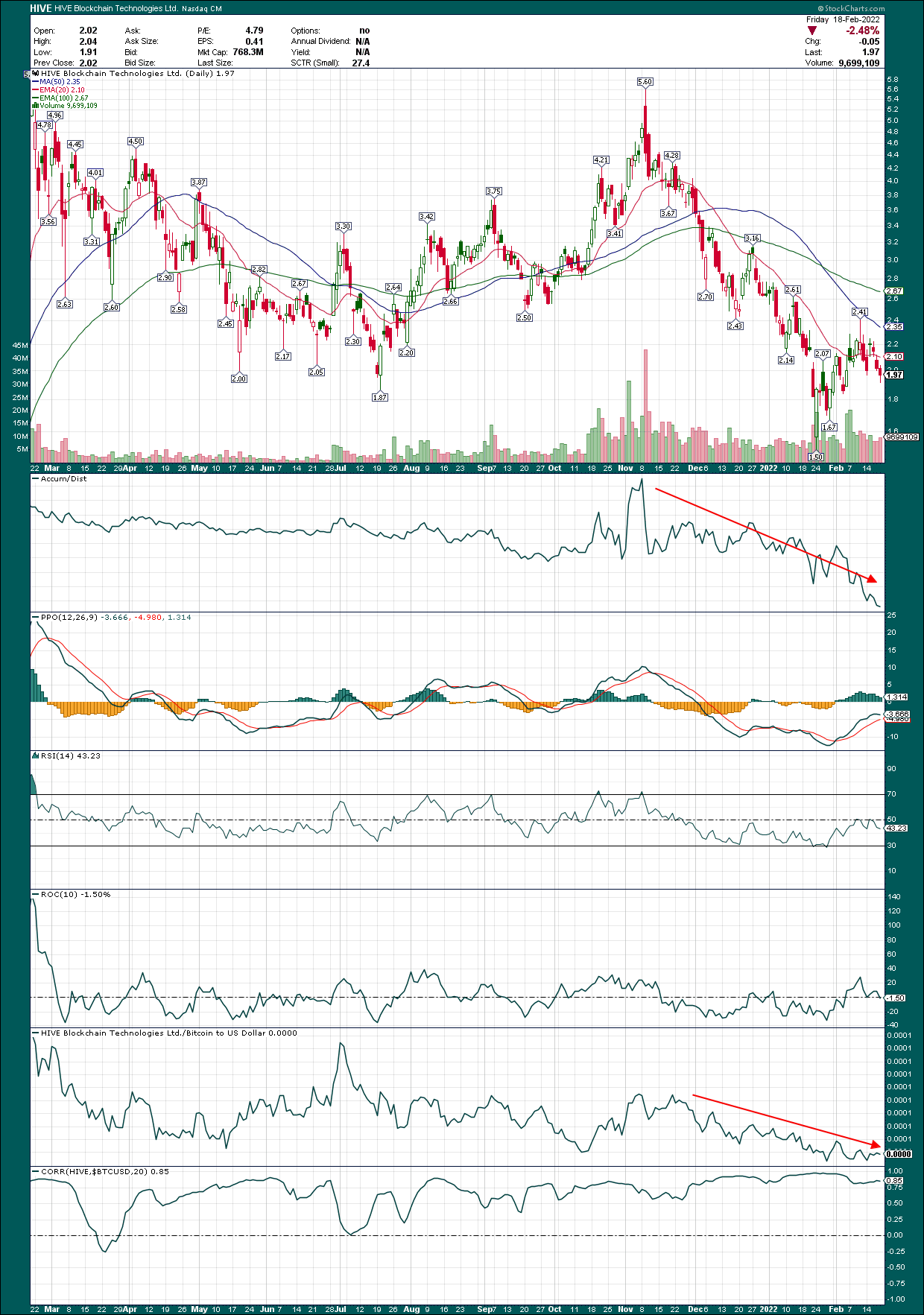

Next up is Hive Blockchain Technologies (HIVE), another new entrant, having been publicly traded since last September. Hive is expected to produce $193 million in revenue this year, which would represent exponential growth from 2021.

Seeking Alpha

With its market cap at $815 million, it has a very steep valuation of 4.2X sales. And keep in mind that’s after a ~65% decline since the November high.

StockCharts

The chart discussion is pretty quick on this one. Correlation to Bitcoin is good, but relative performance, price action, A/D, and momentum are all weak. With an expensive valuation and an ugly chart, Hive is out of the running for a Bitcoin alternative. It literally has nothing to offer in terms of relative attractiveness.

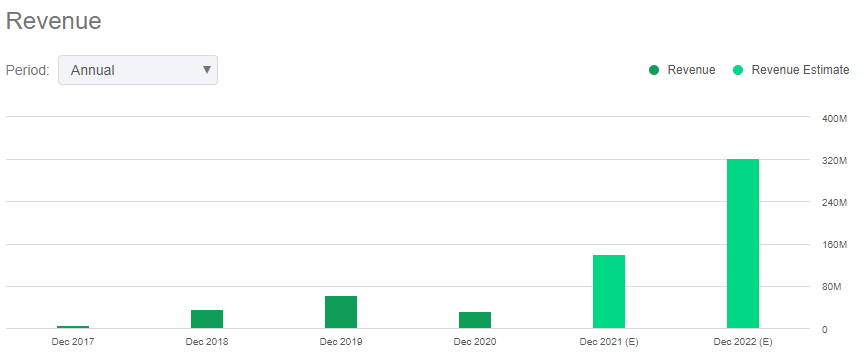

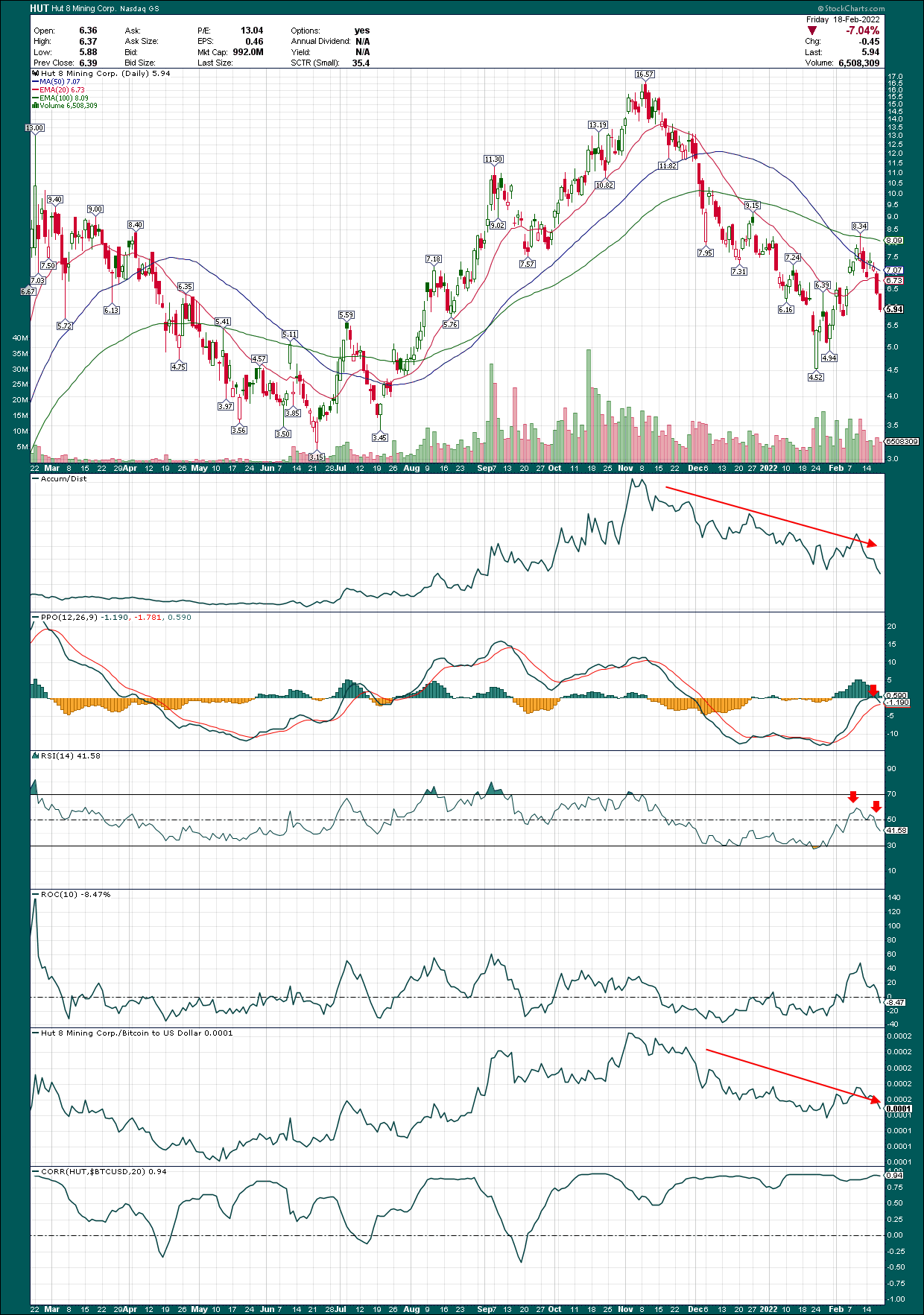

Our next miner is Hut 8 (HUT), certainly one of the larger miners available to investors. It’s expected to produce $320 million in revenue this year, but it also has a $1 billion market cap.

Seeking Alpha

That means it’s going for 3.2X sales, which puts it towards the higher end of the crypto miner valuation spectrum. It’s not egregiously overvalued, but the valuation picture is a mark against it. Let’s see what the price chart looks like.

StockCharts

Correlation to Bitcoin is excellent at 0.94, making it one of the best miners in terms of tracking the price of Bitcoin. But relative strength has been pretty awful, and the A/D line, as well as momentum indicators are all showing lots of weakness. The stock is down ~65% from its high but I’m afraid it may not be cheap enough. Thus far, we’re still sitting with Core Scientific as our top Bitcoin alternative, but let’s press on.

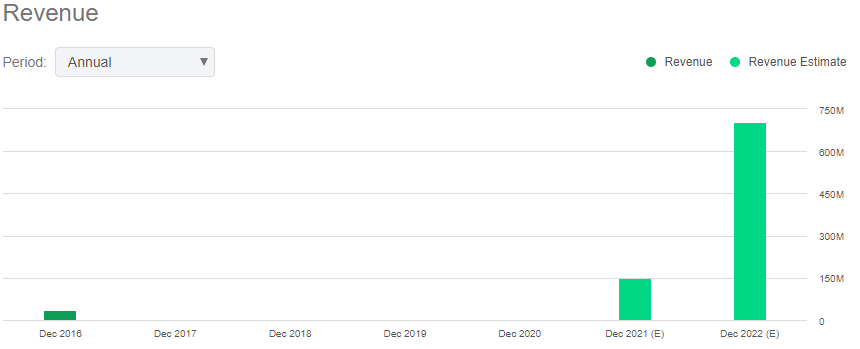

Next up is Marathon Digital Holdings (MARA), a behemoth in the sector that I’ve been bullish on at times in the past. Marathon is in the midst of a massive expansion of capacity, which we can see below with revenue estimates.

Seeking Alpha

Revenue is expected at $705 million this year, so even with its $2.46 billion market cap – which is huge in the world of crypto mining – it is going for 3.5X sales. That puts Marathon at a premium in terms of the smaller miners, but scale is worth something, and Marathon is, as I said, in the midst of a rapid expansion. That explains some of the premium, but whether it explains all of it or not is in the eye of the beholder.

Let’s see if the chart can settle the debate.

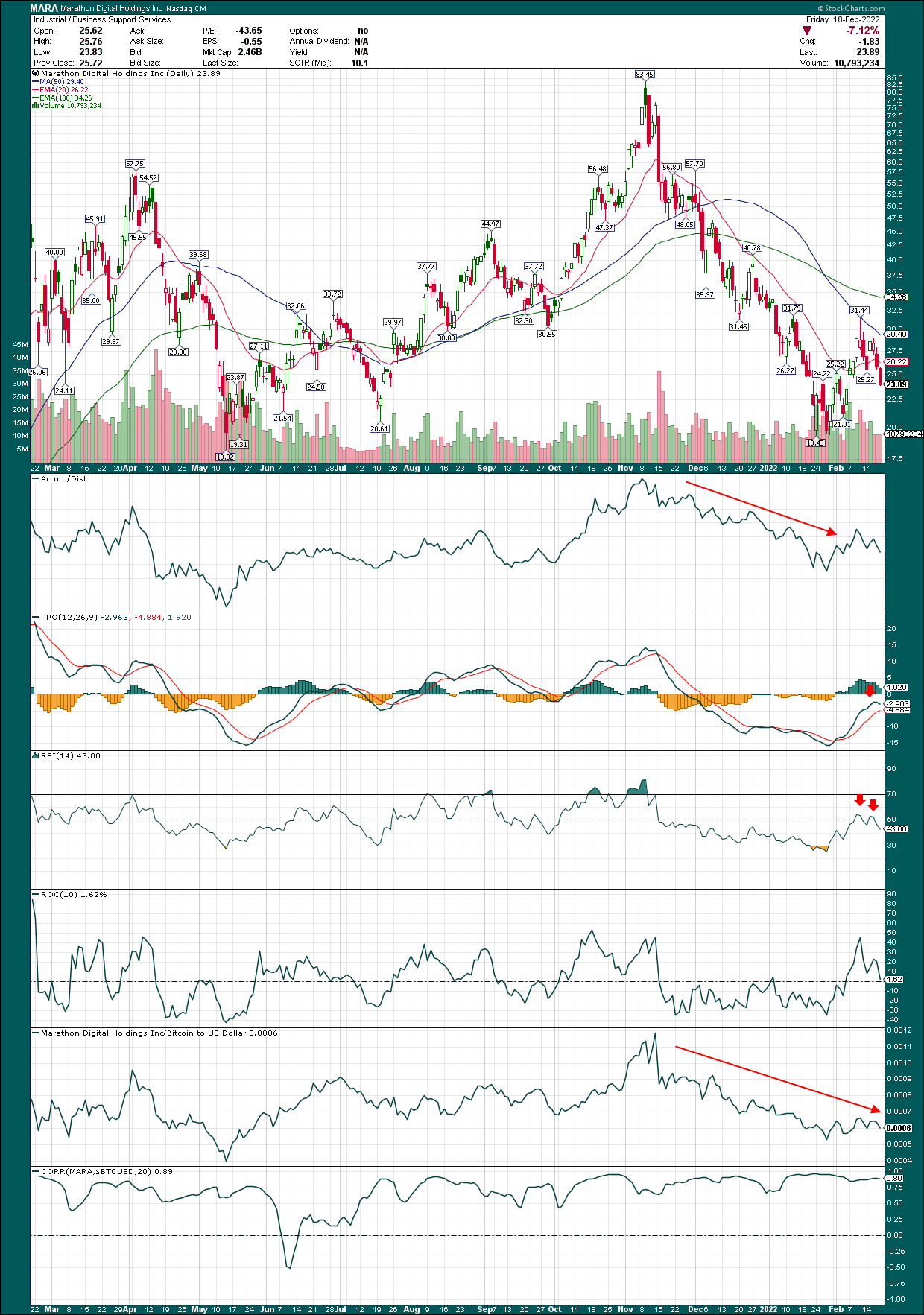

StockCharts

Marathon is off more than 70% since its high, but is showing some signs of life of late. Momentum is trying to rebound but Marathon still looks like it’s in a bottoming process, and not that it already has bottomed. Correlation is pretty good at 0.89, but relative performance is one again pretty weak. So just like the other miners, Marathon is a substitute for Bitcoin itself, but not necessarily a good one.

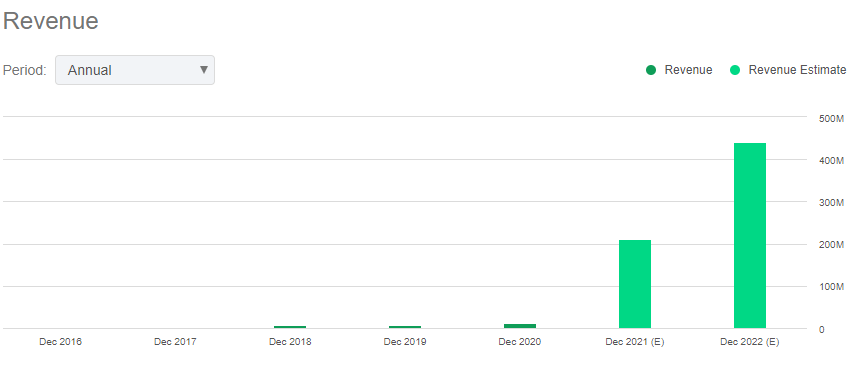

On to the next one, which is Riot Blockchain (RIOT), which is off ~80% from its high. Riot was one of few choices for investors in crypto miners during the early, mania phase of the most recent bull run in Bitcoin, and its stock price showed it. That’s no longer the case, of course, and Riot has come back down to earth and then some.

Seeking Alpha

Riot also has good scale, with projected revenue of $441 million for this year. That puts its price-to-sales ratio at a nosebleed level of 4.5X. That on its own makes Riot egregiously priced against its peers, and therefore, it is unlikely to be the best Bitcoin alternative. But we’re being thorough here, so let’s take a look at the chart.

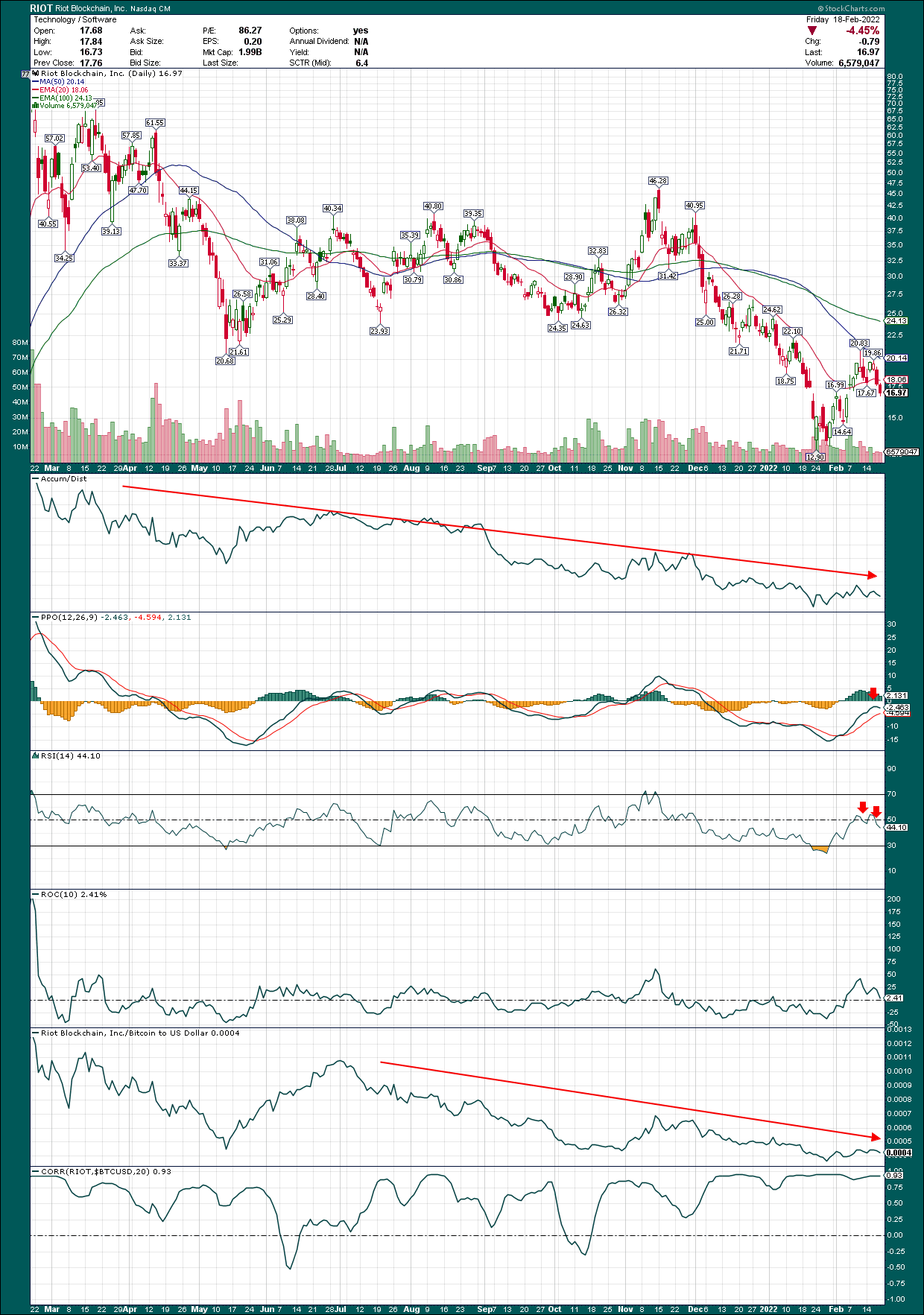

StockCharts

We see all the same characteristics here, but worse. The A/D line, relative performance against Bitcoin, momentum, sheer price action, it’s all terrible. Riot has been anointed as a loser in the sector by Wall Street, so whether you like the company or not, the money is saying Riot is not a good pick.

This is one I’ve been bullish on in the past, but obviously, none of those calls worked out longer-term. Riot is, perhaps, the weakest of the group right now so we certainly don’t want it as a Bitcoin alternative. Out of the group we’ve seen, Core Scientific has the best shot of being a viable Bitcoin alternative. But below, we’ll see the one I like even more.

Sell. Every. Megawatt.

That brings us to our final miner, Soluna Holdings (SLNH). In this case, I think we’ve saved the best for last, as Soluna has a unique way of going about crypto mining. Soluna is not a crypto miner in the way that the others in this list are, but rather, the company builds “scalable data centers that convert wasted renewable energy into computing power.” This is then used for applications such as crypto mining, machine learning, or artificial intelligence computing. Soluna aims to provide low-cost alternatives to battery storage or transmission lines, taking advantage of generated power that would otherwise be wasted. The company’s slogan – Sell. Every. Megawatt. – sums up the business model pretty well. Soluna harvests power that would otherwise go to waste, and utilizes it to generate low-cost revenue in crypto mining.

The January update showed that the company is on pace to hit 1 EH/s by the end of March 2022, and over triple that level by this year’s fourth quarter. In other words, capacity to mine crypto is ramping extremely quickly, and therefore, revenue generation capacity. The 1 EH/s capacity is about two months ahead of schedule, and management remains very bullish.

The company currently has 52 MW energized and its January Bitcoin equivalent mining rate was up 11% month-over-month. On a comparable basis, mined Bitcoin was up 20% month-over-month in January. Targets for the end of this year are 150 MW, and 3 EH/s, both of which are 3X current levels.

Annualized revenue was ~$39 million in January, so on a price-to-sales basis, Soluna is at 3.4X. However, keep in mind that January’s revenue rate is likely to be a small fraction of December 2022 revenue, as we should see capacity ramp throughout the year. So if we triple January’s annualized revenue rate and estimate ~$100 million in revenue, Soluna may be trading for 1X sales or just over it. On this basis, I find Soluna to be an extremely attractive Bitcoin alternative. Keep in mind we’re working off of forecasts from management, so there’s a lot of execution risk between here and there. But it appears to me that if Soluna gets even in the ballpark, the stock is very cheap.

I also like the unique model Soluna employs, because it also has flexibility to apply its computing power to a variety of applications. It has a green element to it because the company is harvesting power the generators would otherwise be wasting, and costs are low because of that. It all comes together in a differentiated package that marks Soluna aside from the others.

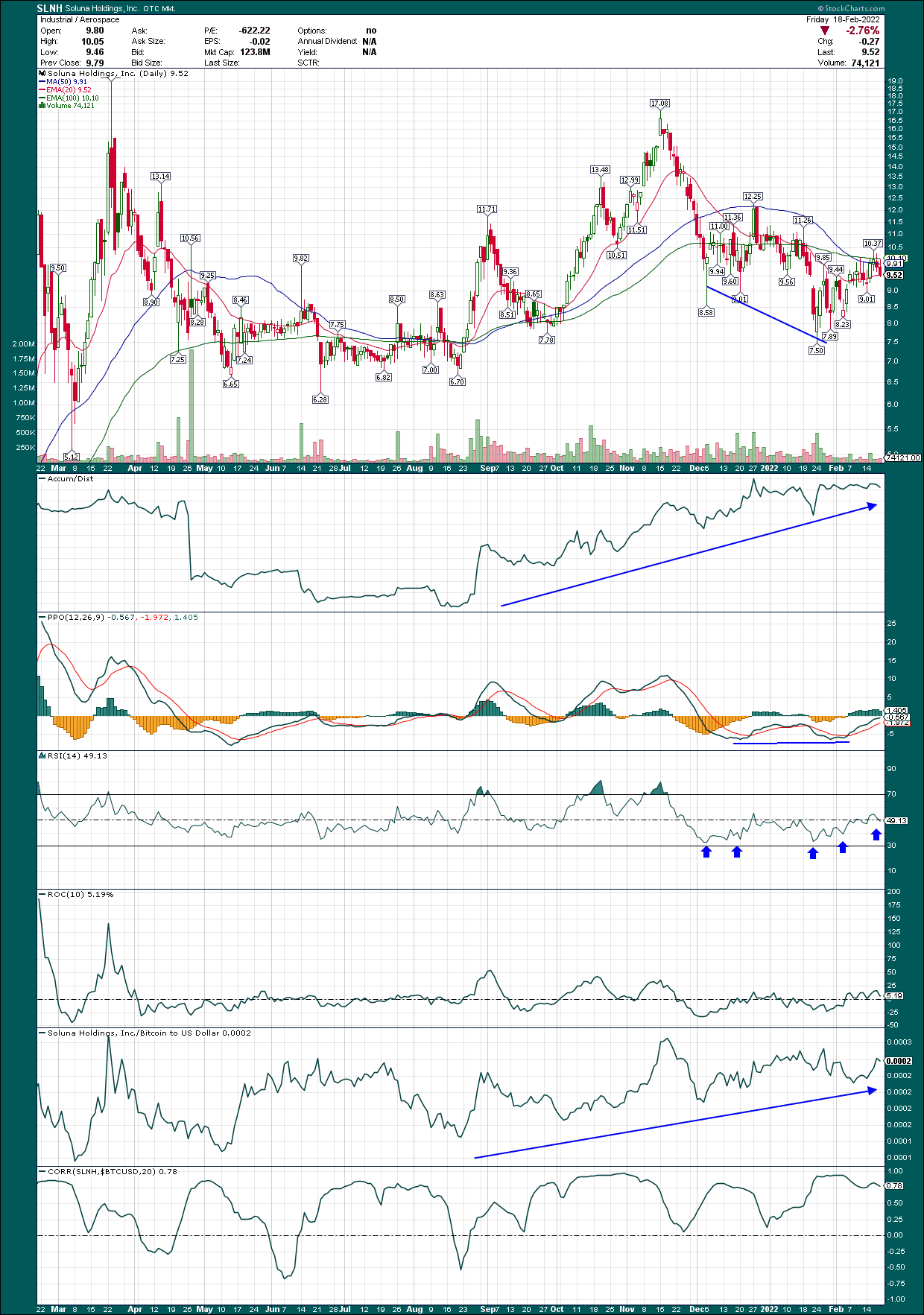

Now, let’s take a look at the chart.

StockCharts

Unlike the others in this list, Soluna has a very strong A/D line that is making new highs, while the stock is down almost half from its high. That speaks volumes (literally) about how investors feel about this stock. People are buying dips, and that’s an extremely bullish trait for any financial asset. In the face of the rest of the miners all posting weak A/D lines, I think Wall Street has picked this stock as the leader of the group. When/if bullish Bitcoin price action returns, the leaders are allocated the most money. That’s where you want to be.

Momentum put in a positive divergence in the past several weeks, another bullish sign. That makes it much more likely that we’ve already seen the low on Soluna, which drastically reduces the risk one needs to take to own it.

Its correlation to Bitcoin is lower than most of the others in this list, but it’s still certainly positive. If we stretch the timeframe from 20 days to 100, Soluna’s correlation to Bitcoin is 0.77. That means they’re reasonably well correlated, which then leaves the last piece of the puzzle being its performance against the coin itself.

Soluna has outperformed Bitcoin, if modestly, for the past few months. I think this has to do with the cheap valuation driving buyers (evidenced by the rising A/D line), and for all of these reasons, I see Soluna as having more upside potential from here than Bitcoin itself.

One final point that I think supports the bulls is that nearly 30% of Soluna’s float is owned by the CEO’s investment firm, Brookstone Partners. Those are going to be very sticky shares that don’t trade hands, so if we do start getting a rally, it can be quick. It also means management is extremely interested in a good outcome for shareholders, and that’s never a bad thing to have the people steering the ship with the same goals as you.

Conclusion: Which Bitcoin mining stock is a buy?

If we see Bitcoin rally later this year – as I believe we will – Soluna is still highly correlated and will almost certainly advance on that prospect. In addition, Soluna has the extra leverage of rapidly increasing capacity, adding another lever that the coin itself won’t have.

The miners in general aren’t necessarily in that good of shape in a lot of cases. There are widely varying valuations, very poor looking charts, and increasing competition. However, Soluna is different; I see it as very cheaply valued, and with huge potential upside.

Be in no doubt that owning any crypto-related stock is a risky proposition. The rewards are significant, and so are the risks. You don’t have to take my word for it; you can look at any of the charts in this article for sufficient evidence of that. However, given that we’re so far down from the highs, the massive excess that was present a few months ago is gone, and we can buy the best of the best at what I see at a very attractive valuation.

Keep your positions sized prudently, and keep stop losses in place if that’s your thing. The point is, manage your risk on these carefully so you don’t end up holding the bag if the sector goes south. I honestly don’t think any of the others look that great at the moment, apart from Soluna, which I like very much.

We began with posing the question of whether it’s better to buy the coin, or to buy miners, and at this point, I would confidently answer that for me, Soluna looks the better value than the coin itself. Don’t get me wrong; I like Bitcoin for later this year. I do think we have some chopping around to do before we rally, but I still believe we’re going to see a big rally later this year when risk-on is back in vogue. However, Soluna, with its soaring capacity, cheap valuation, and (potentially) rising Bitcoin price, could triple or more. Bitcoin is almost certainly not going to triple, or come anywhere close to that this year. So if I had to pick just one, Soluna is top of the crop for me.