greenleaf123/iStock via Getty Images

Despite most Covid pull forward tech plays collapsing in the last few months, Apple (AAPL) still trades near all-time highs. The best-case scenario predicts the stock still trading at a similar level in FY25, or four years from now. My investment thesis remains Bearish on a stock not expected to reward shareholders from these prices over the next four years.

Historical Norms

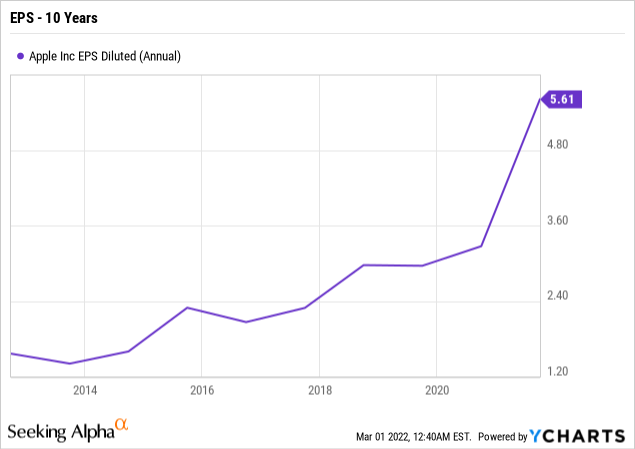

Too many investors are making the mistake of extrapolating current blockbuster earnings into the future. One reader recently suggested Apple was on the pace for 25% earnings growth just because the first quarter of the year had such growth while ignoring growth rates continue to decelerate.

In reality, the tech giant has had a history of declining earnings after the iPhone goes through normal cycles. The one difference this cycle is that Covid pulled forward earnings dramatically, setting up a potential bigger hit this time after EPS surged 71% from $3.28 in FY20 to $5.61 in FY21.

Based on current consensus estimates, Apple is set to earn $7.32 in FY25. The stock currently trades at 22.3x these EPS estimates, with Apple trading around $166 now. Ironically, analysts don’t even forecast the normal cycle hit despite the biggest pull forward in history.

Source: SA earnings estimates

Analysts forecast the tech giant growing earnings by 9.6%, 6.2%, 5.4%, and 6.3%, respectively, over this period. Apple isn’t expected to see one year of 10% growth with the higher earnings growth in FY22, all related to the strong FQ1’22 holiday report.

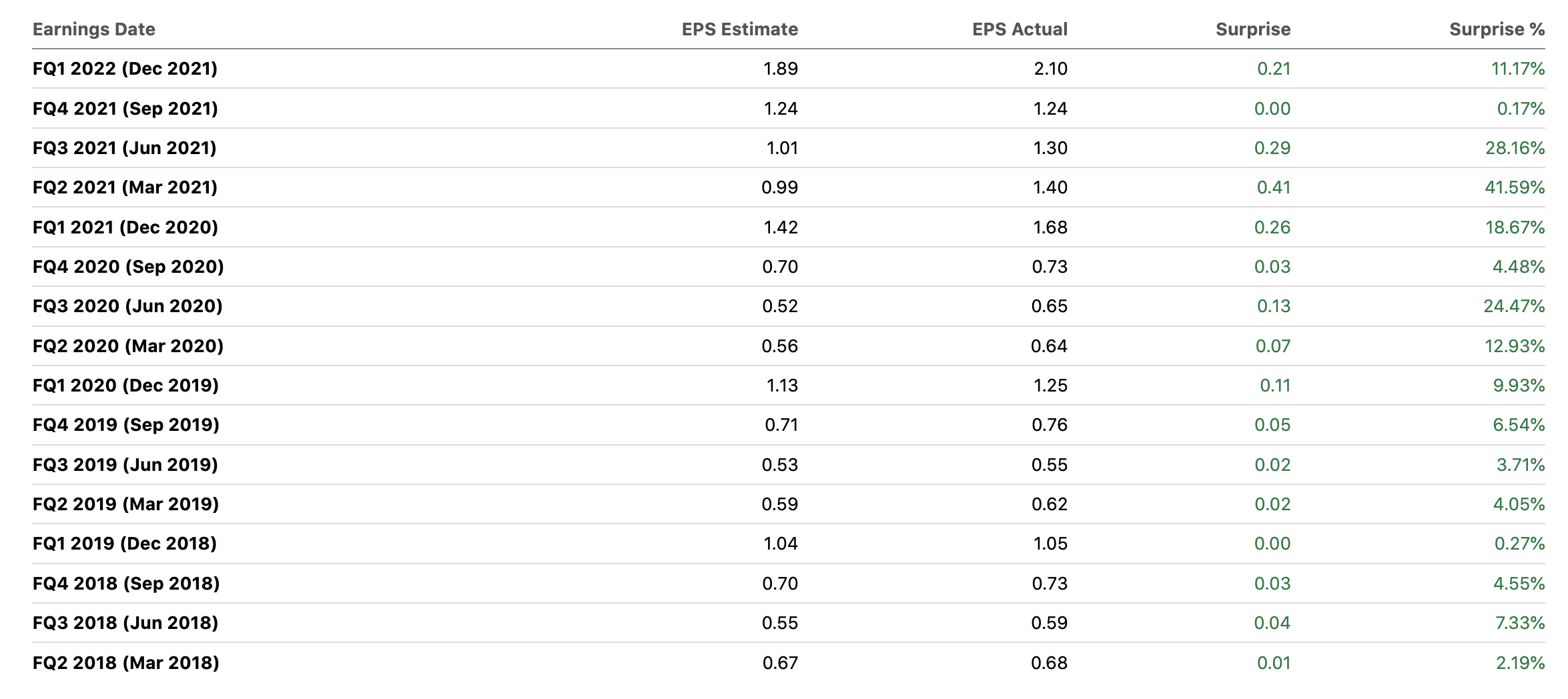

Investors willing to pay up to 30x forward earnings for Apple now have clearly forgotten the years prior to the Covid pull forward period. The tech giant reported quarterly results for years where the company hardly beat analyst estimates.

Source: SA earnings surprise

Prior to the December 2019 quarter, Apple only had a couple of quarters where EPS beat estimates by $0.05. The company is likely to go back to a trend of slightly leaping consensus targets. Remember, the tech giant needs to smash current EPS targets in order to justify the current stock price, much less a higher stock price.

Even if Apple beat current EPS targets 5% annually, the annual EPS targets would end up as follows:

- FY22 – $6.15 x 5% beat = $6.46

- FY23 – +6% growth = $6.85 x 5% beat = $7.19

- FY24 – +5% growth = $7.55 x 5% beat = $7.92

- FY25 – +6% growth = $8.40 x 5% beat = $8.82

Under such a scenario where analysts forecast growth in the 5% to 6% range each year and Apple ends up beating the targets by 5% each and every year, Apple would end up earning nearly $9 per share by FY25.

The stock now trades at 18.6x these FY25 EPS estimates. Remember, these EPS targets are factoring in Apple beats current analyst estimates by $1.50 per share over this 4-year period. In addition, these estimates assume consistent growth in the 10% annual range to achieve these results while Apple has a strong history of iPhone cycle troughs leading to earnings declines.

Investors need to keep in mind that Apple achieving 10%+ growth is phenomenal and phenomenal results don’t usually last.

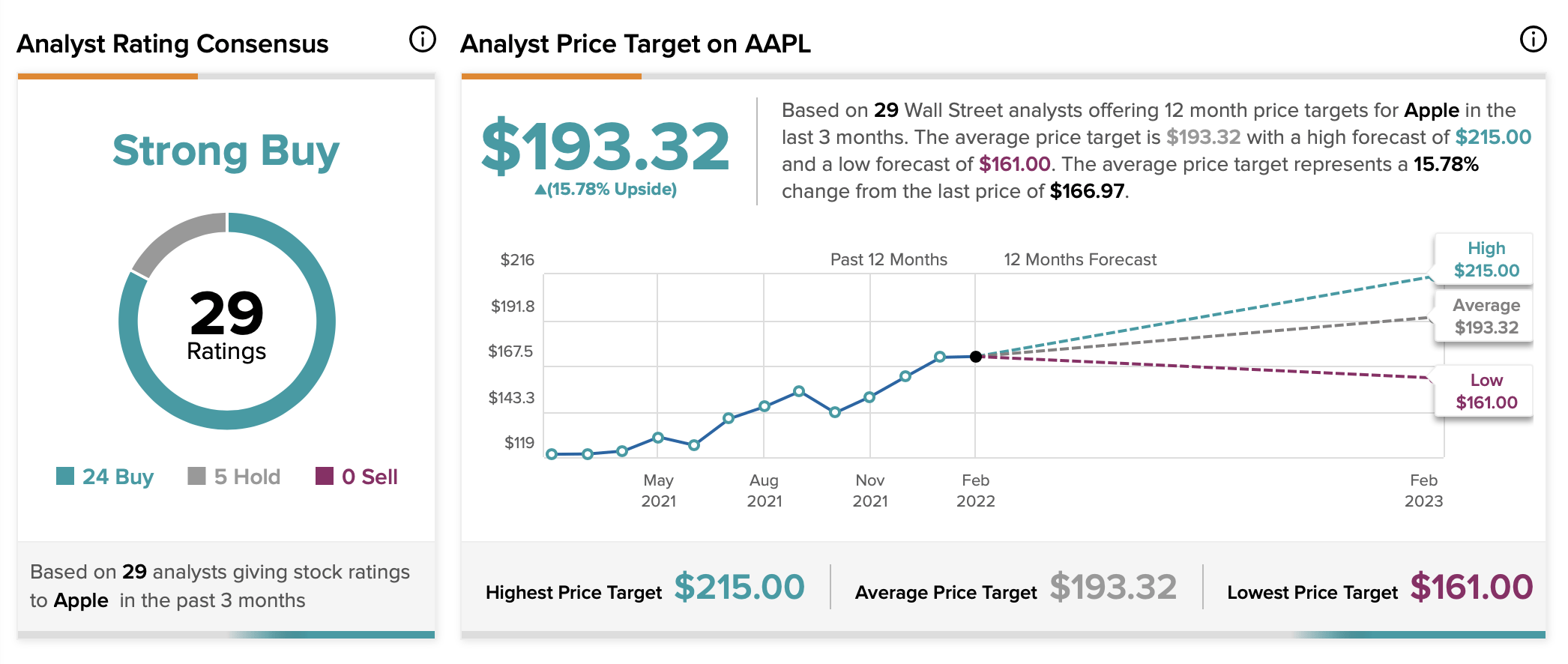

Analyst Disconnect

The odd part is that analysts are generally disconnected from their own EPS targets. The average analyst Apple price target is an insane $193, or equal to 31x their own EPS targets for FY22.

Source: TipRanks

For an analyst to have such a bullish view on the stock, those analysts should hike EPS targets. Yet, the deep-dive research these analysts provide investment clients don’t conclude such EPS growth will occur.

The $193 price target isn’t even inline for a logical price target for FY25 using numbers that smash current analyst estimates by over 20%.

Remember, star analysts like Katy Huberty from Morgan Stanley and Ming-Chi Kou from TF International Securities both have very low estimates for new products like AR/VR devices and autonomous EVs. These hot products might warrant paying over 18x EPS targets for FY25 in a few years, but the numbers don’t add up to Apple being a good investment over this extended time period.

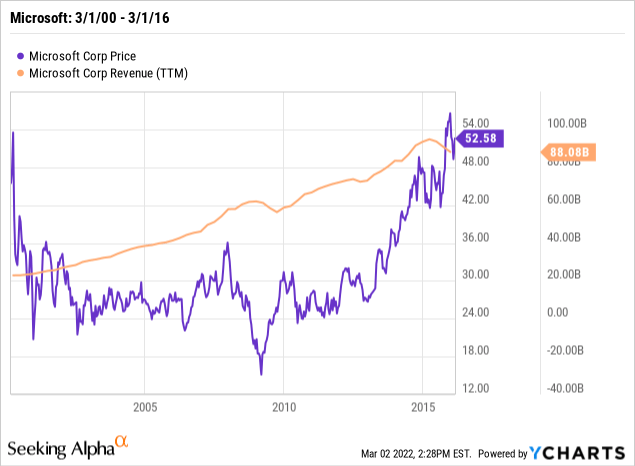

Investors seem to forget that stocks such as Microsoft (MSFT) went through extended periods where the stocks saw no gains. The tech giant went from the peaks in 2000 (a period not so dissimilar from 2021) to 2016 without seeing any gains despite massive revenue growth of over 300% during the 16 years.

My analysis is only suggesting a 3- to 4-year period where an investor probably sees no gains in the stock. Microsoft actually went a decade trading at the post-internet bubble lows before the recent rally. Apple might rise to $200 or even $250 during this period, but the stock is likely headed right back to the current level prior to FY25.

At best, only a trader willing to sell the stock on any big rallies should hold Apple now. Otherwise, a long-term investor with the Jim Cramer mantra of “hold Apple, don’t trade it” won’t be rewarded during this period.

Takeaway

The key investor takeaway is that Apple is far too expensive here. The market has built in wildly bullish expectations of further growth not even logical with the obvious Covid pull forward in FY21.

My negative thesis isn’t even factoring in the potential of the tech giant missing targets and facing a period where targets actually need to be cut. Investors need to look for the best way to exit a position in Apple with years of no gains ahead.

, Solana (SOL) Hit New Cycle Highs Against Ether (ETH) as Trump Edges Closer to Victory in U.S.")