Michael M. Santiago/Getty Images News

Apple (NASDAQ:AAPL) is one of the businesses on public markets that has built up a cult-like investor following. This stems from the premium products and ecosystem, the brand image, and the eye-popping returns over the last decade. Investors should use the rearview mirror to help make informed decisions, but the real test is trying to figure out what the future holds in the coming years. Apple is a great company, but I don’t think that it will lead to great forward returns for investors who hold the stock.

Investment Thesis

Apple is one of the best businesses available to investors on the public markets. The company has a fortress balance sheet and has an impressive track record of returning capital to shareholders over the last decade. Apple recently announced a 4.5% increase in the dividend along with a boost in the buyback program. While these factors all support the bullish thesis for Apple, it has been priced into the stock for some time now.

Unfortunately, the valuation leads me to believe that forward returns over the next 5 years will not be as impressive as they have been over the last 5 years. With a market cap over $2.5T, slowing growth, and an earnings multiple of 26.7x, shares currently trade at a premium valuation even after a double-digit drop from recent highs. I would love to own Apple because it is a fantastic high-margin business and a cash cow, but the current valuation doesn’t leave a margin of safety for new investors.

Slowing Growth & Supply Chain Issues

One of the main things that will likely be a drag on returns for Apple shareholders is the law of large numbers. Apple has grown into a mature business with several different segments, but the business revolves around the iPhone and the whole Apple ecosystem. The company is projected to have single-digit earnings growth over the next couple of years. The company certainly has an impressive moat and a rock-solid balance sheet, but I don’t think the current valuation makes sense when you look at the growth rates.

One of the other things that could have a material impact on Apple is supply chain issues related to the lockdowns in China. While it is hard to distinguish news from noise when it comes to China, I think we can all agree that something strange is happening in China with the newest round of lockdowns.

Big Ol’ Boat Traffic Jam (statista.com)

I won’t pretend to be a macro genius and explain all the different ways this could have an impact on Apple, but I think it would be smart for investors to consider the potential chain reaction, especially for investors buying at the current prices. It is possible that these problems could spell trouble for Apple’s stock, especially with the premium valuation.

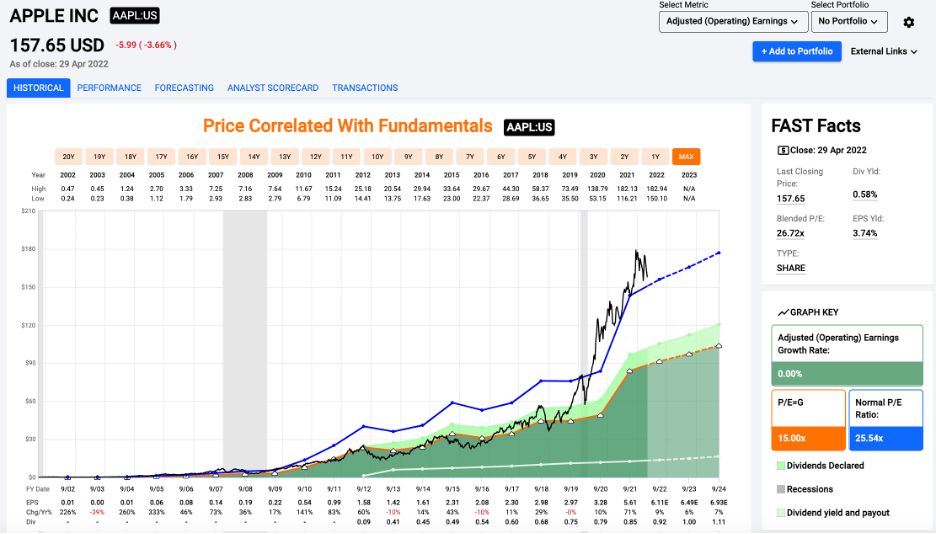

Valuation

While the business has been firing on all cylinders over the last couple of years, Wall Street and other investors know that and have awarded Apple with a premium valuation. Shares trade at 26.7x earnings, which is slightly above the average 25.5x multiple. Unless the projections are too pessimistic, I think a 20x multiple would be closer to fair value today.

Price/Earnings (fastgraphs.com)

Part of the multiple expansion over the last couple of years is likely due to the increase in service revenues. It is a higher margin line of business than the physical products that Apple sells and has been growing faster as well. The gross margin on services is just under 73%, while the product segment had a gross margin of 36% for the most recent quarter. While the returns might be lackluster without further multiple expansion, investors have come to expect regular dividend and buyback increases from Apple.

Dividends & Buybacks

Every investor loves dividends and buybacks. We all invest to get a return on our capital, and Apple has been one of the best for a long time when it comes to shareholder returns. While the buyback program reduces shares outstanding, it is more beneficial to investors when the valuations are lower. The company has repurchased 266M shares in the first six months of the fiscal year for a total of $43.3B. That is a lot of money spent while the stock has been trading near all-time highs.

The 0.6% yield isn’t much to get income investors excited either. While the one penny raise is better than nothing, I would love to see Apple prioritize dividend growth while the stock is trading at a premium. I know some investors complain about the tax inefficiencies of dividends, but I would prefer it to buybacks while the stock is expensive. While I know that investors don’t hold Apple for the dividend, the company is likely to continue their string of raises for the foreseeable future.

Conclusion

Apple is a business that many investors have owned for a long time. While the company has matured into a cash printing machine over the last decade, it has also seen significant multiple expansion. It looks like growth will be slowing down in the next couple of years, and the Chinese lockdowns could create issues for Apple’s manufacturing and supply chain processes. At 26.7x earnings and a 0.6% yield, I don’t think it makes sense to be a buyer at current prices.

As I mentioned in yesterday’s article on Microsoft (MSFT), the other thing that investors should look out for is the potential for selling pressure related to the index funds. Big tech companies have received the lion’s share of buying demand from the index inflows over the last decade, but that also works in reverse. If we see selling across the board, it will hit the largest companies the hardest. Apple will stay on my watchlist because it is a high-quality business, but I will be patient to see if we get a price decline and a wider margin of safety in the coming months.