PhillDanze

After staging a strong rebound in July, shares of Apple (NASDAQ:AAPL) are down “only” 14% year to date. However, I believe the recovery rally has no legs to stand on as Apple has a growth problem that is set to get worse, not better, if a recession approaches. While Apple has historically been generous in returning cash to shareholders through large stock buybacks, investors will have no other choice but to face Apple’s deteriorating growth prospects going forward. For this reason, I expect Apple’s shares to revalue to the down-side again!

Slowing hardware revenue growth could diminish Apple’s appeal as a growth stock

Slowing topline growth is a challenge for all companies, not just Apple. But if a business is evaluated chiefly based on its prospects for topline expansion, like Apple and other technology companies are, then slowing growth becomes a much bigger issue.

Apple’s competitive advantage in the past has been to translate product innovation and strong execution to massive cash resources. Blockbuster introductions like the iPhone, which debuted 15 years ago, continue to generate the majority of Apple’s revenues today and with no major new innovations coming to market lately, Apple is at risk of compounding its growth problem.

I say compounding because Apple already sees dangerously slowing topline growth, especially in key product categories like the iPhone. Apple’s iPhone revenues increased only 5.5% in FQ2’22 and totaled $50.6B, which calculates to a revenue share of 52%. Sales of iPhones are also no longer the fastest growing product category for Apple, Services are: they grew 17.3% year over year and include sales from the firm’s advertising, AppleCare®, cloud, digital content, payment and other services.

In FQ2’22, Apple’s hardware revenues (iPhones, Mac, iPad and Wearables) increased only at a rate of 6.6% year over year which marked a serious slowdown compared to the year-earlier period which saw 61.6% growth.

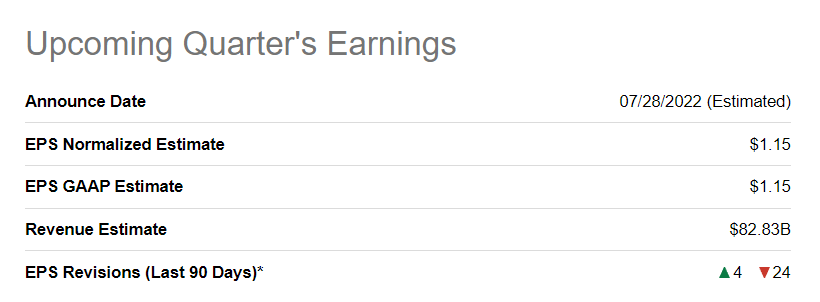

This trend likely continued for Apple in the third quarter, and I expect no more than mid-single digit growth in combined ex-Services sales and approximately 12-15% Services revenue growth year over year. Earnings estimates for Apple’s FQ3’22 have trended downward with only 4 revisions to the upside and 24 to the downside in the last 90 days.

Seeking Alpha

Slowing hardware sales have been reflected in depressingly low revenue growth estimates for Apple in the next four years. Estimates are calling for 5.5% annual topline growth until FY 2026, a rate that is truly disappointing considering Apple’s growth rates of the past.

Seeking Alpha

P-E ratio and estimates imply growing down-side risks

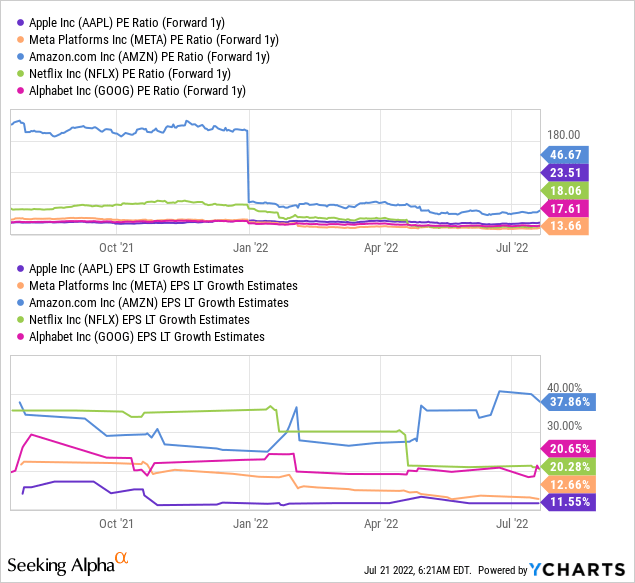

Weak expected revenue growth and a slowdown in core hardware sales justify a material downward revaluation of Apple’s shares, especially since Apple, relative to other FAANG stocks, has a high P-E ratio. Shares of Apple are the second-most expensive in the FAANG category, after Amazon (AMZN), based on P-E while at the same time offering the weakest EPS growth going forward.

At a P-E ratio of 23.5 X, Apple’s shares are expensive. EPS estimates are also trending down hard, and the expectation is for Apple’s annual EPS growth to average only 5.4% until FY 2026. A recession may result in even lower EPS growth estimates and force Apple to explore new ways to ignite stronger revenue growth.

Seeking Alpha

Buybacks have become less valuable for shareholders

Apple has historically returned a lot of money to shareholders with buybacks, and many investors cited Apple’s growing cash pile as a good reason to buy the stock. But buybacks alone may no longer suffice to get investors excited about investing into Apple’s business if growth prospects keep deteriorating.

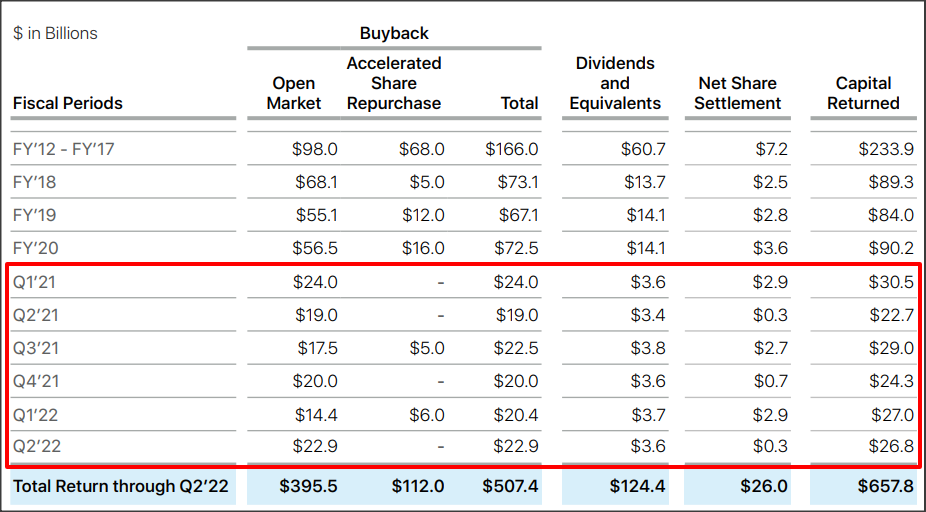

In FY 2019, FY 2020 and FY 2021 Apple repurchased $66.9B, $72.4B and $86.0B of its shares. In the six months ended March 26, 2022, Apple repurchased $43.3B of its shares in the market.

Apple

However, recent buybacks – between FY 2021 and FY 2022 especially – have occurred at a time when Apple’s shares were trading at a high valuation factor, thereby reducing the effectiveness of the buyback.

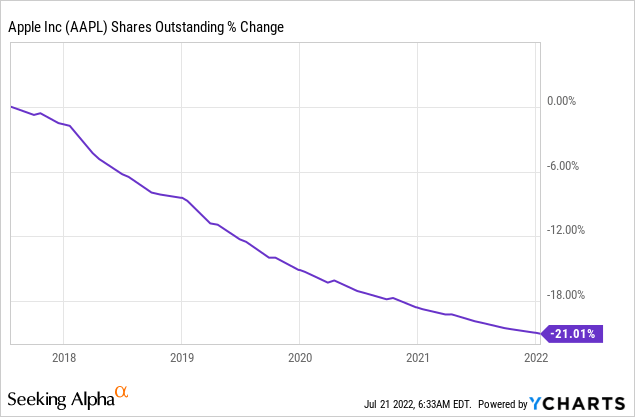

Buybacks have much less value for investors when the stock price is at record highs and core business momentum is dramatically slowing down at the same time. In the last five years, Apple has reduced its outstanding shares by 21%.

While Apple will likely continue to repurchase about $20B a quarter of its own shares, buybacks can’t mask that Apple’s shares are expensive based off of P-E and that they have therefore less value for shareholders. Secondly, they also can’t mask that Apple has a serious growth problem at its hands.

Risks with Apple

The biggest risk for Apple right now is a continual slowdown in hardware-related topline growth that could make Apple no longer a growth play. Another risk is that growth in Services revenues may not be high enough to compensate for weak revenue growth in Apple’s hardware segments. While Services is growing rapidly, the size of the segment is still relatively small and out-performance will only marginally move Apple’s total revenue growth rate moving forward. Thirdly, the valuation is itself a risk: If Apple is no longer seen chiefly as a growth play, then the valuation factor may compress.

Final thoughts

Apple’s consolidation is likely not over, and risks are only growing. Growth concerns could receive new fodder next week when Apple reports for FQ3’22 and the earnings card shows a continual decline in revenue growth.

Because Apple’s topline and EPS growth predictions have seriously decelerated and forecasts now call for only 5.5% annual revenue growth until FY 2026, I believe the risk matrix has completely changed, and it indicates further downside for Apple’s overpriced shares!