2018 Launch of Starbucks Visa Credit Card

Mario Tama/Getty Images News

I recently wrote a bullish thesis on BM Technologies (NYSE:BMTX) which I believe is a mispriced fintech and it’s about to acquire a bank charter. The bulk of that research and information was compiled just before the Q2 earnings report which occurred on August 16th. As part of coverage here I wanted to write a bit of an update regarding information that came through.

I rely pretty heavily for context on the previous article though so you may want to review that first.

Headline data was mixed with a top line GAAP EPS of $0.35 which beat estimates by $0.25 yet a slight decline in revenue overall. I’d say there’s a lot more signal underneath this than the headlines though. Here are my notes.

Filings

The company has not been current with filings since Q1 due to auditor changes which has created a delisting headwind. On August 16th they finally filed their 10-Q for Q1 and their Q2 filing came out recently on August 22nd.

This will help investors get an up-to-date view of the company and removes the risk of delisting. It also should reveal if there is any warranted fear regarding further auditing issues.

Profitability

Free cash flow was $7.052m in Q1 and $8.983m for the first half. Expenses have jumped up due to development of software likely related to their new BaaS partner. In Q1 they booked $2.02m expense for software development and $1.165m in Q2. Costs are expected to continue throughout the rest of the year as they prepare for commercial launch

First half EBITDA is $15.1m compared to BMTX’s enterprise value of $47.748m. This implies an EV/EBITDA of 3.16x based on the first half numbers alone.

An overall note is that comps to last year are a bit challenged due to tailwinds from government stimulus checks generating deposit growth and spending fees.

Deposits

Average serviced deposits totaled $2b in Q2 which suggest some slowing in their growth. CEO Luvleen addressed this directly in prepared commentary:

Additionally, given the changes in the current macro environment, we are considering slowing the growth of deposits on our balance sheet, which will require us to raise significantly less capital and will also have valuation benefits from an EPS standpoint. We are considering brokering off deposits or partnering with additional sponsor banks to accomplish this.

With the First Sound Bank merger still expected to close by the end of this year, BankMobile will be positioned with a bank charter before long. While they are expected to be limited in how many of their $2b of deposits they can start to hold on the balance sheet, it seems management is intending to approach this through a hybrid model of building their capital case while bringing deposits over in a thoughtful way. This tracks with my original commentary that the company does not need to do an immediate capital raise through the markets which some are fixated on as a risk.

Instead, I think the takeaway for investors here is related to CFO Bob Ramsey’s comments in the Q&A:

Additionally, given some of the shifts in market dynamics, most notably that the value of off balance sheet deposits is higher in a higher rate environment, and that our cost of capital is also higher given where our stock trades today. We are really looking at what can we do to maximize our earnings per share and minimize any potential dilutions. So as we think about the capital needs of the business today, as compared to a year ago, we are looking at it through a different lens. We certainly are very mindful of investor concerns around dilution, and we’re all shareholders here and don’t want to do anything that would be dilutive either.

This is a good thing for current shareholders as it suggests that management understands that further dilution, especially at current stock price levels, is not beneficial and also perhaps not needed given higher interest rate environment.

By the year’s end we should have more clarity about First Sound Bank merger completion and with that management will be able to make some decisions regarding their deposit base. But from the looks of things, they seem like they have partner bank options lined up.

Building Scale

They’ve had 215,000 new accounts in the first half. Higher Education Organic Deposits (deposits that are not part of a school disbursement and are indicative of primary banking behavior) came in at $925 million for the first half showing the continued strength of their student disbursement business anchor.

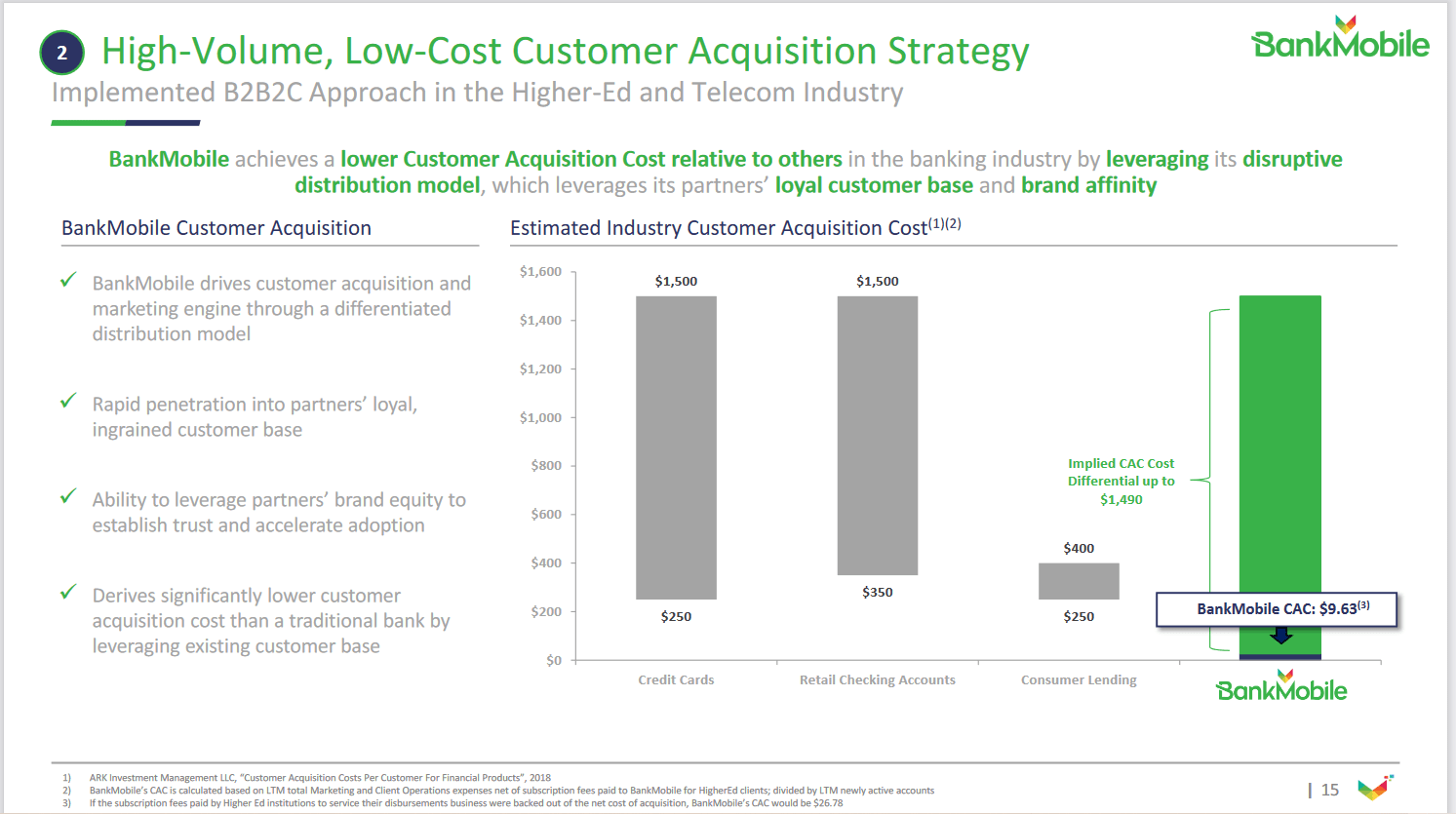

Ten new colleges and universities have signed agreements with BankMobile this year increasing exposure to their Vibe checking account by 55,000 people through the course of their higher-ed disbursement business. It’s likely that the disbursement business is profitable on a standalone basis which means that if any of these 55,000 students convert to banking customers the customer acquisition cost (CAC) is negative.

I’d like to reemphasize that for a second given it’s a huge reflection. BankMobile already boasts industry low CAC around $9.63. You can see that the low-end CAC for credit cards and checking accounts is between $250-350 — miles away from BMTX.

BankMobile IR Materials

This a reflection of the operating benefit created by their higher-ed disbursement anchor. If that business itself is profitable in selling their disbursement services, then any student that chooses to disburse their money to a BankMobile’s Vibe checking account costs the company nothing, it just happens as a normal course of the disbursement services business. In fact, if the company is profitable then the cost to acquire those customers is actually negative as they are making money while acquiring those customers.

There’s a bit of speculation here though given we don’t know exactly the profitability of the disbursement business on a standalone basis. Even if the segment is breakeven, it still creates a huge operating benefit for BankMobile in the form of a recurring crop of new depositors every year. What we do know though is that regardless, reported CAC is remarkably low already.

A New Best BaaS Partner: But Who?

One component of how the company makes money is through Banking as a Service (BaaS) where they offer a white-label digital platform enabling brands to offer banking-like services while not operating as a bank. To date BMTX only has one BaaS partner, T-Mobile, who they’ve partnered with since 2017 to support their T-Mobile MONEY offering.

Management has targeted bringing on one new significant partner each 12-18 months. Previously the company had a partnership with Google that fell through simply because Google decided not to enter the space. So investors have been waiting for a bit to see if there’s any further traction in this business line.

BankMobile benefits by managing the deposits generated through the partner. T-Mobile benefits by expanding its offerings as a brand and company with the intention to create further stickiness and customer loyalty as a result. While it’s not exactly clear how many deposits are generated in this way it likely at the least represents a very low cost exposure to T-Mobile’s estimated 109.5m customers.

Recently BankMobile announced a new BaaS partner expected to launch in 2023. Management was very tight-lipped about the details of this new partner in their earnings call with only two sentences in their prepared remarks regarding it:

This new best partner has global operations and 10s of millions of U.S. customers. BMTX was awarded this relationship through a competitive RFP process, underscoring the competitiveness of its vast offerings in the marketplace.

Three subsequent questions were asked regarding the new partner all of which were rebuffed by management. The given reason shared by BMTX CEO Luvleen Sidhu is, “But out of respect for the privacy and the excitement over the commercial launch, we will not be able to share more.“

While details seem unlikely to be forthcoming from BMTX for a while, what we know at present suggests that their new partner will expose them to tens of millions of new potential customers. That’s a net benefit for BankMobile no matter who the partner is.

But here’s where I’m gonna go out on a limb and make a prediction. Simply put, I believe it’s possible the new BaaS partner is Starbucks (NASDAQ:SBUX).

Starbucks the Bank: A Speculation

What started me down this line of thinking was that one sentence that Luvleen shared on the call regarding the new partner. It revealed two details: (1) the company is global and (2) the company has 10s of millions of US customers. A quick check garnered an estimate of 37.8m US customers for Starbucks. This means that Starbucks at least passes the test of what we know so far about this BaaS partner.

Admittedly, that’s not much to go on so far though. Nike, McDonalds, and Apple all fit that profile as well. But stay with me a second. Consider that Starbucks has been pursuing a digital strategy for a while which has accelerated since COVID. They’ve done a lot here including launching a web store, their loyalty program, and now offering subscription options to their drinks and food. Management talks about unmet demand in their brand, how they build emotional attachments and connections with younger people – a target demographic of BankMobile. Starbucks is also a crucial partner with colleges and universities around the US and they recently profiled twelve higher ed locations to visit.

Starbucks’ is estimated to have the industry’s most popular mobile rewards app already. The results of this are rather impressive and reveal a perhaps surprising element to Starbucks’ business. Take for instance this snippet from an article entitled “How Starbucks Is Also A Bank”.

Because of Starbucks’ size and customer loyalty, customers are not afraid to keep some of their money in their Starbucks account, as they know they’ll use it someday or other. 41% of U.S. and Canadian users pay with their Starbucks card. At the end of 2019, users held a collective $1.5 billion in balances. 1.5 billion dollars might not sound like a huge amount, but it’s significant when you consider that more than 3,900 banks across the U.S. have less than $1 billion in total assets, according to the FDIC.

The article further highlights that officials from Korean banks have raised concerns that Starbucks is in fact an unregulated bank that threatens the Korean banks very survival. The concerns are not without merit given the critique that while Starbucks can build “deposits” on their prepaid cards, customers can essentially only buy coffee or other Starbucks products with them. Some have even begun to frame Starbucks simply as a fintech company.

Starbucks announced a partnership with Chase in 2018 launching a branded Visa rewards credit card. The card was integrated with Starbucks’ loyalty and rewards system enabling customers to earn Starbucks related rewards on all of their credit card purchases.

So Starbucks is clearly already playing around in an area that is related to BaaS with expected moves further into that space. It seems plausible that Starbucks may have initiated an RFP process to explore BaaS options.

Rather than simply offering prepaid gift cards or branded credit cards, what if Starbucks could offer full-service debit cards with similarly uniquely designed rewards and savings programs for their business? That’s essentially what a partnership with BankMobile could provide to both their customers and even their employee base.

Consider also that Starbucks engages in massive data analytics mining consumer spend behavior with their cards. According to this article in 2018, an estimated 90 million transactions a week occurred across their stores. Using big data and artificial intelligence the company leverages their data mine to determine future store locations, expand into grocery items, update their menu, and do targeted marketing. Adding in a BaaS option could massively expand their data pile on customers that chose to bank with them.

Founder Howard Schultz rejoined Starbucks as interim CEO in March of this year to navigate a company in transition and in their latest quarterly call they announced: “Lastly, we have been working on a very exciting new digital initiative that builds on our existing industry-leading digital platform in innovative new ways, all centered around coffee and most importantly, loyalty that we will reveal at Investor Day.”

Investor Day is scheduled for September 13th and is expected to be a big day for the company. A recent Seeking Alpha news update on the company noted a 50% likelihood that the new CEO is announced and also highlighted “ Starbucks (SBUX) could also issue more details about on-trend initiatives like iced & plant-based beverages, broadening payment options beyond a Starbucks gift card for customers to join the My Starbucks Rewards loyalty program, and making digital ordering more frictionless.”

Potential and Risks for BMTX

What I’ve shared above can only be considered speculative at best. There’s nothing more than circumstantial data points which may suggest Starbucks as the new partner. With that said, let’s reflect on the potential impact for BankMobile overall.

A partnership with Starbucks would expose BMTX to a new loyal customer base that are already digitally engaged through a robust loyalty and rewards program. The customer base of Starbucks aligns with BMTX’s young adult targeting as well. So the partnership would at a high level seem beneficial to BMTX and strategic. Starbucks will likely be incentivized to grow deposits with the new offering and BMTX will benefit from that and association with such a strong brand.

What if I’m wrong though? Fortunately, if I’m wrong the company still has a new partner of which I simply would remain ignorant. I’m not making any fundamental changes to my thesis based on the Starbucks speculation and remain convicted that Starbucks or not, BMTX is undervalued. The new partner will still bring an asset of tens of millions of customers to BMTX the value of which will likely depend on the strength of the brand. It seems management will continue to be quiet until commercial launch, estimated for early next year, so we wouldn’t have further details until then.

Some Final Reflections

BankMobile stands to benefit from whoever the new BaaS partner is and with a contract signed it’s just a question of who it is and when details are coming. I think there are some reasons that point to Starbucks being the new partner but in all it doesn’t change the thesis regarding BMTX whether it is them or not.

With a review of Q2 earnings it seems the company has made significant steps both in terms of continued profitability and the delisting risk. With quarterly filings now current the financials there for investors to evaluate things are happening as I expected so far.

Additionally, the merger of First Sound Bank continues to be on track and management has indicated a capital raise which includes stock dilution is not something they are looking at with current prices. Instead, they are looking to leverage a hybrid model to monetize their deposits while they build their capital base organically. And crucially they actually have the relationships and flexibility to seemingly do this, especially given a higher interest rate environment.

All in all, Q2 earnings track with my thesis and BMTX remains undervalued. I maintain a 1-2 year price target of $12.22 which I believe to be conservative.