Shahid Jamil

I first wrote about Apple (NASDAQ:AAPL) on the Seeking Alpha platform in September 2014. My Buy recommendation then holds as true today as it did then.

In that article I highlighted the golden opportunities for Apple around Asia, especially in China. Many of my critics then poured scorn on the idea. They reckoned that the perceived poor masses of Asia could never afford high-priced Apple products. Now many of the same people say Apple is in fact too dependent on Asia: “plus ca change, plus c’est la meme chose”.

There is a huge and loyal user base in China and around Asia, particularly in Japan. The installed base keeps growing. Sales keep growing. This growth is especially based on a higher proportion of high-end products being sold. This seemingly captive market means that it is almost a certainty that at least one of the company’s new long-term arrows will strike the bulls-eye.

For me that golden arrow will most likely be healthcare. This makes China and healthcare the twin vectors of future growth around an ever-growing iPhone user base.

The returns from Apple

The graphic below from the Economist tells the tale:

The Economist

It’s about a year out of date but the picture would actually be even more positive now. Apple under Tim Cook has been the ultimate source of capital growth for investors. He has out-performed all the other famous titans of Wall Street performance.

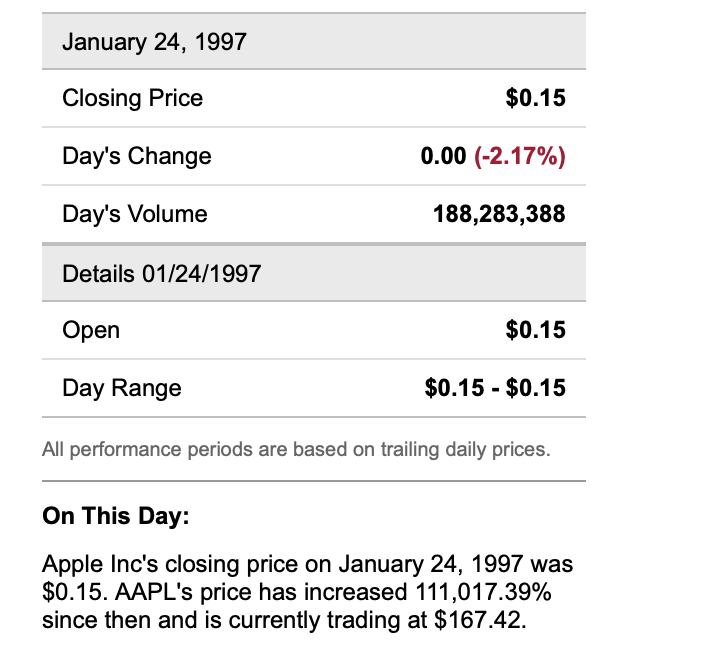

The calculation illustrated below from Charles Schwab shows the benefit of long-term investment in Apple. Tim Cook’s fantastic performance has been only a part of it, and in fact the lesser of it. Personally, I first invested in the company in 1997 upon the return of Steve Jobs. He was the corporate titan I wanted to follow. For me a similar strategy has been followed with Elon Musk at Tesla (NASDAQ:TSLA) and Wang Chuanfu at BYD Auto (OTCPK:BYDDF). In all three cases an understanding of the importance of Asia has been a key component.

charles schwab

Those who bet against Apple (and there are many here on SA) have been holding losing hands literally for decades. As the song goes:

You gotta know when to hold them you gotta know when to fold ’em.

An American perspective of misunderstanding China has been key to this failure of sound advice.

The Importance of China

China is key to Apple as both supplier and revenue generator.

Approximately 75% of its products are manufactured in China. Over 1 million people are directly employed in manufacturing Apple products in China and probably twice as many indirectly. Some outside observers think the Chinese government is likely to pressurise and attack Apple in the country. They under-estimate the Chinese leadership’s own need to maintain growth and incomes. As detailed here, Apple had previously signed an MOU with the Chinese government (through the National Development & Reform Commission) to invest huge long-term funds to developments between Apple and Chinese bodies.

Approximately 19% of Apple’s annual sales revenue now comes from China. This compares to 11.7% of revenue in 2011 when Apple first began itemising this. The proportion of net profitability that comes from China is thought to be substantially higher than that 19% figure.

The Consolidated Statement of Operations for the last 9 months published with the Q3 2022 results shows the following revenue breakdown:

Americas 42%

Europe 24%

China 19%

Japan 7%

Rest of Asia 8%.

This 34% of revenue from Asia will in my opinion continue to increase as a proportion of the whole. This is due to both macroeconomic reasons and to specific Apple products being well-suited for Asian consumers.

This year has seen particularly strong growth in China for the company’s iPhone 13 and MacBook Pro. With the iPhone 14 about to launch, that is likely to maintain strong revenue growth in China in the next couple of quarters. Reports suggest that Apple’s component suppliers in China are building up for an iPhone production ramp-up for the remainder of this year. Apple has seen 147% year-on-year growth up to August in the premium phone market. That is defined as $1000 and above. In general this premium market has increased quite sharply as a percentage of the market as a whole. Apple holds about 46% of it.

It is also being speculated that the new AR/VR headsets from Apple might launch anytime soon. They are expected to be on sale in the first half of next year under the “Reality” brand. Currently the vast majority of the world’s SAR/VR headsets are exported from China. I’ve seen various figures for the proportion of VR headsets which are sold in China. This report here suggests a 5 year CAGR 0f 43.8%. So if Apple really is releasing something special soon, then it is likely to grow both sales figures and production numbers in China for Apple significantly more than in any other market.

Long-term China has higher growth prospects in general going forward than do the more mature North American and European markets. Already China’s GDP has exceeded that of the USA on a PPP (purchasing power parity) basis.

The figures Apple gets from China equate to the revenue the company gets from its entire Services business. Tim Cook is slowly and politically shifting this dependency. This highlights his supply chain management skills and his political savvy. The company has plans to invest $430 billion in just the USA alone in the next 5 years. When you hear company announcements of the amount Intel (NYSE:INTC) is planning to invest in the next few years in their home country, they are small compared to Apple’s numbers. Intel is currently constructing 2 fab plants in Arizona with a cost of approximately $20 billion.

It may turn out that investments in China for Apple in total do not reduce in dollar terms in the next few years. For instance it was recently reported that the company is looking to source semiconductor chips from China for the first time. So the amount being invested by Apple in China is unlikely to reduce in nominal dollar terms anytime soon. The amount invested in China will though probably reduce as a percentage of Apple’s total capex worldwide.

The Importance of Rest of Asia

As my original article back in 2014 emphasised, it is not just China which is a bull factor for Apple. Asia in general is the fastest growing economic region in the world. It is rapidly becoming the most important market in the world for many companies.

On the production side Apple has been diversifying production to other Asian countries, in particular to Vietnam. Completed products from other countries are however quite limited. They are composed mainly of the Mac Mini from Malaysia and the AirPods Pro from Vietnam.

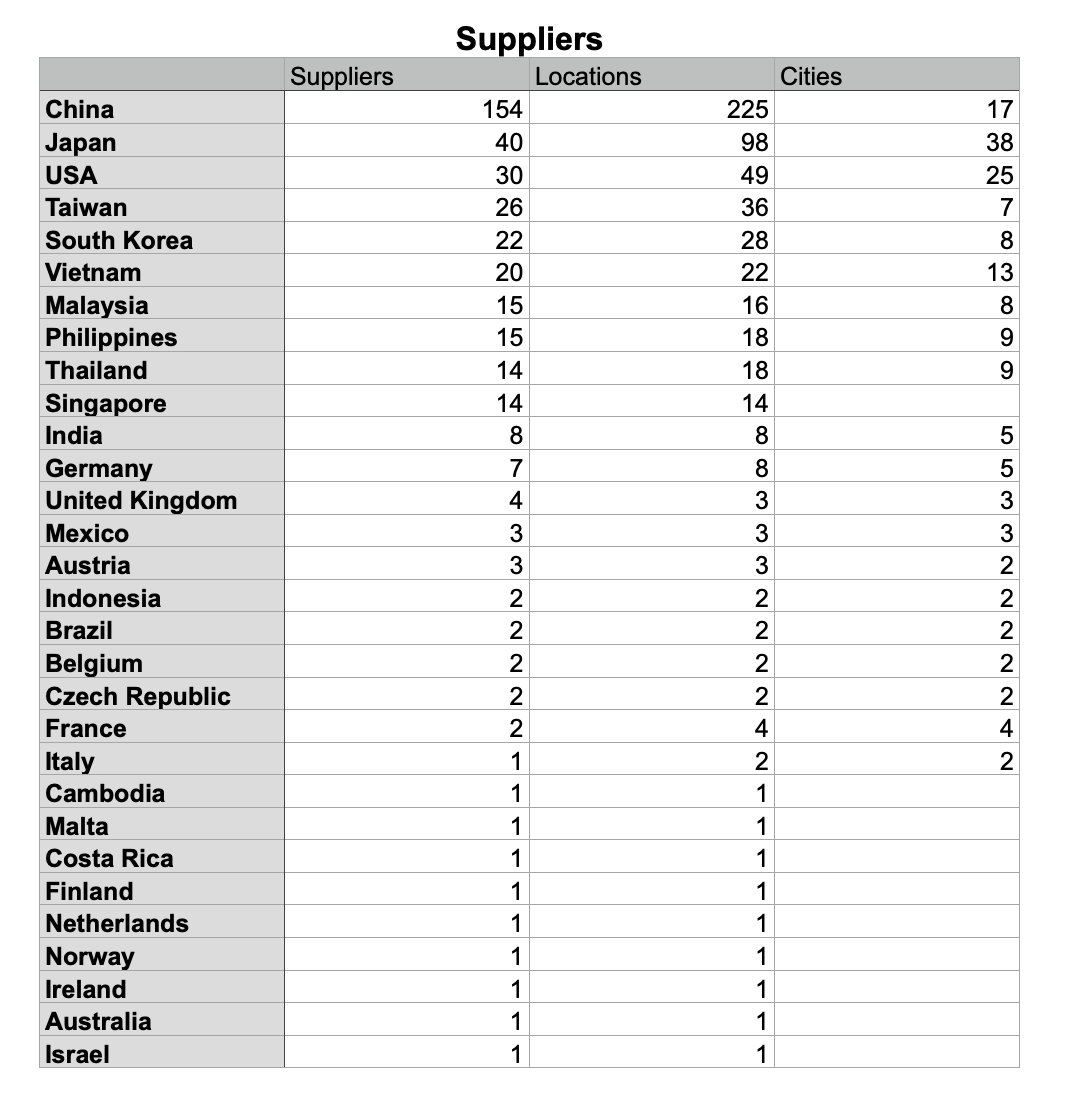

The graphic below from Loup Ventures illustrates this nicely:

loup ventures

Of the company’s 11 main suppliers bases, 9 are from Asia. Interestingly Apple is easily able to straddle both China and Taiwan. It is the largest client of Taiwan Semiconductor (NYSE:TSM),the world’s largest chipmaker. Together they will be producing the new iPad Pro and MacBook Pro later this year. That should be another example of how Apple continues to grow its established product base through continued organic growth.

The picture is similar on the revenue side. It is not often noted by commentators that Japan represents Apple’s best market by market share. Over 60% of phones there operate on the IOS system, as detailed in this article. Yet how often do you hear complaints from U.S. manufacturers that the Japanese market is rigged unfairly against its products? That mantra does not seem to apply to Apple.

As detailed in this article, Apple’s business around Asia is likely to grow more rapidly than elsewhere in the world in coming years. In Apple’s Q3 results, Cook especially emphasised the progress reported across the product area Rest of Asia.

In Asia, the company has a higher proportion of first-time buyers than elsewhere. It has a higher ASP, more often than not because of Asia’s liking and readiness for 5G. Asian countries in general have better growth rates than any other area in the world. India is a huge slumbering market for Apple, though I personally believe Apple’s growth there will continue to be slow due to the endemic corruption and inefficiencies in that country.

Healthcare

Healthcare is in many ways the US economy’s largest addressable market. It is also a very fast growing market as the population ages and as medical costs escalate. It represents 20% of U.S. GDP and over $4 trillion of spending. If Apple could attain just 2% of healthcare spend in the USA alone, that would add $80 billion in increased annual revenue.

So far, the Apple Watch has been the main entry into this market. However access points to iPhone healthcare applications are growing strongly as well. It is no coincidence that Watch sales have skyrocketed since Apple shifted the marketing focus from fashion glamour to healthcare functions. Of course Watch sales are still a small percentage of the company’s revenues, as the illustration below from Apple shows:

apple inc

The healthcare functions are however building up, mainly through acquisitions.

Some of these include:

* Rare Light, for non-invasive glucose monitoring.

* Glimpse, as a health data platform.

* Beddit, as a sleep tracking app to monitor breathing and heart rate.

* Tueo Health, a childhood asthma app.

Watch recently received its and 510(k) clearance with the new AFib History (atrial fibrillation) and Parkinson’s features. This is the second FDA endorsement after the EKG app in 2018. So it is a gradual process. Watch currently monitors things such as pulse rate, oxygen levels and tremors. Blood pressure monitoring is likely to come next. Watch can be seen as an aid to healthcare professionals in the sense it gives consumers information on when to visit a doctor. It is a long path to being able to replace a visit to the doctor.

Recent developments in the UK though have shown, for example, how health services have almost broken down under patient demand. Everywhere there will be huge and growing demand for products that will enable visits to doctors to reduce. Already somewhat controversial medical consultations by video are becoming more common. The over-stretching of personal medical resources is only likely to increase around the world.

Apple’s strength as a health data platform is increasing strongly. Already it has relationships with over 800 health institutions in the USA in which the company provides its “Health App” and “Health Kit” products through the iPhone. There are approximately 1 billion iPhones currently in use around the world today. That is the massive platform on which Apple can offer healthcare products. This will combine with the rapidly growing platform of the Apple Watch. Last year the company sold over 34 million Watches. That is more than the entire Swiss watch industry combined.

One analyst has calculated that currently 13% of iPhone 13 users have a Watch from Apple and that going forward 35% of iPhone buyers will add a Watch as the bio functions build up.

Alternative to Healthcare for Meaningful Growth

If I am mistaken on healthcare that is hardly the end of the thesis that Apple is still a great investment for the future.

The stock price should continue to grow on the back of many factors.

* Continuous organic growth in what are now traditional areas. These comprise iPhone, computers, music, Watch, Air Pods, iPad, and Services. These all flourish on the back of the ever-rising user base.

* The much-heralded Apple car or some sort of car-based products.

* Streaming programming, which has been rising faster than anticipated. In this they have a similar advantage over the competition that Sony (NYSE:SONY) possesses. The vast in-house base to which to launch products easily fits in streaming services.

* Augmented Reality, which is likely to be particularly popular in Asia.

Healthcare has one strong long-term advantage. It ticks the box of securing future strong growth through necessities rather than luxuries. Luxury product demand can always be fickle. There is nothing fickle about healthcare needs. It may however presage a lower margin business for Apple. Healthcare products are somewhat different from Steve Jobs’ “insanely great products” target. In addition the other tech titans such as Microsoft (NYSE:MSFT) and Alphabet (NYSE:GOOGL) are also looking very seriously at healthcare. There is a sense that they have often avoided treading on each other’s toes in the past.

Conclusion

Of course it is not impossible that none of Apple’s new product lines will succeed. That seems most unlikely though. It is also possible that none of its growing existing organic products will continue to grow. That is possible but is highly unlikely. In Q3 2022, in fact, active installed devices hit records in all major product categories. Recent figures show an increasing proportion of consumers want to buy Apple’s more expensive products.

Health, for me, is the best bet in the long run. It should not be forgotten that Tim Cook has often repeated the mantra:

Health will be Apple’s greatest contribution to mankind.

As for the China political risk, that is always there. If that incinerates Apple’s stock price it will do the same to most other U.S. giants. So if you avoid Apple stock because of the China risk, you should probably avoid the U.S. stock market entirely.

China plays a long game and at some stage Taiwan will be an existential crisis. I would estimate that would be at about the end of the decade at the earliest. That is about the same time Tim Cook is likely to retire. That leaves plenty of time to make capital gains on my thesis of Apple increasing its percentage revenue coming from China and healthcare on the back of an ever-expanding iPhone user base.