Hispanolistic

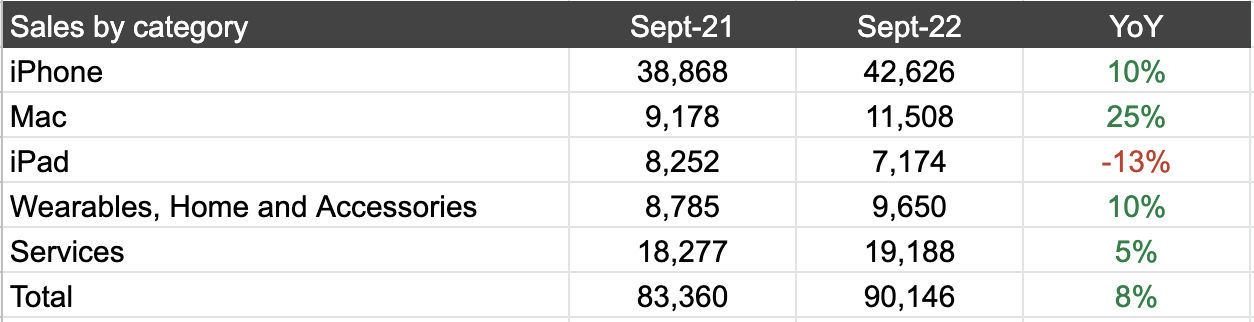

Shares of Apple Inc. (NASDAQ:AAPL) rose as much as 8% on the day after the iPhone maker reported above-consensus revenue and EPS for the September quarter. Total revenue of $90.15 billion (+8% YoY/+14% ex-FX) and diluted EPS of $1.29 (+4% YoY) both beat Street estimates of $88.8 billion and $1.27.

For the December quarter, management did not provide any specific top-line guidance due to macro uncertainty, but noted the following:

- YoY revenue growth to decelerate from +8% YoY in the September quarter, while FX will impact revenue by 10 points.

- Gross margin between 42.5%-43.5%.

- OPEX between $14.7 billion and $14.9 billion.

- OI&E to be around -$300 million.

-

Tax rate to be around 16.5%.

The Street currently expects Apple to grow revenue by 2.7% YoY to $127 billion and to deliver EPS $2.08 (-1% YoY) in the current quarter.

Company data, Albert Lin

iPhone

Revenue of $42.6 billion (+10% YoY) was slightly below $43 billion consensus, but management highlighted strong 14 Pro and 14 Pro Max demand where supply has been constrained since the beginning. As a percentage of revenue, the iPhone remained the largest top-line contributor at 47% in FQ4, despite the product has been around for 15 years.

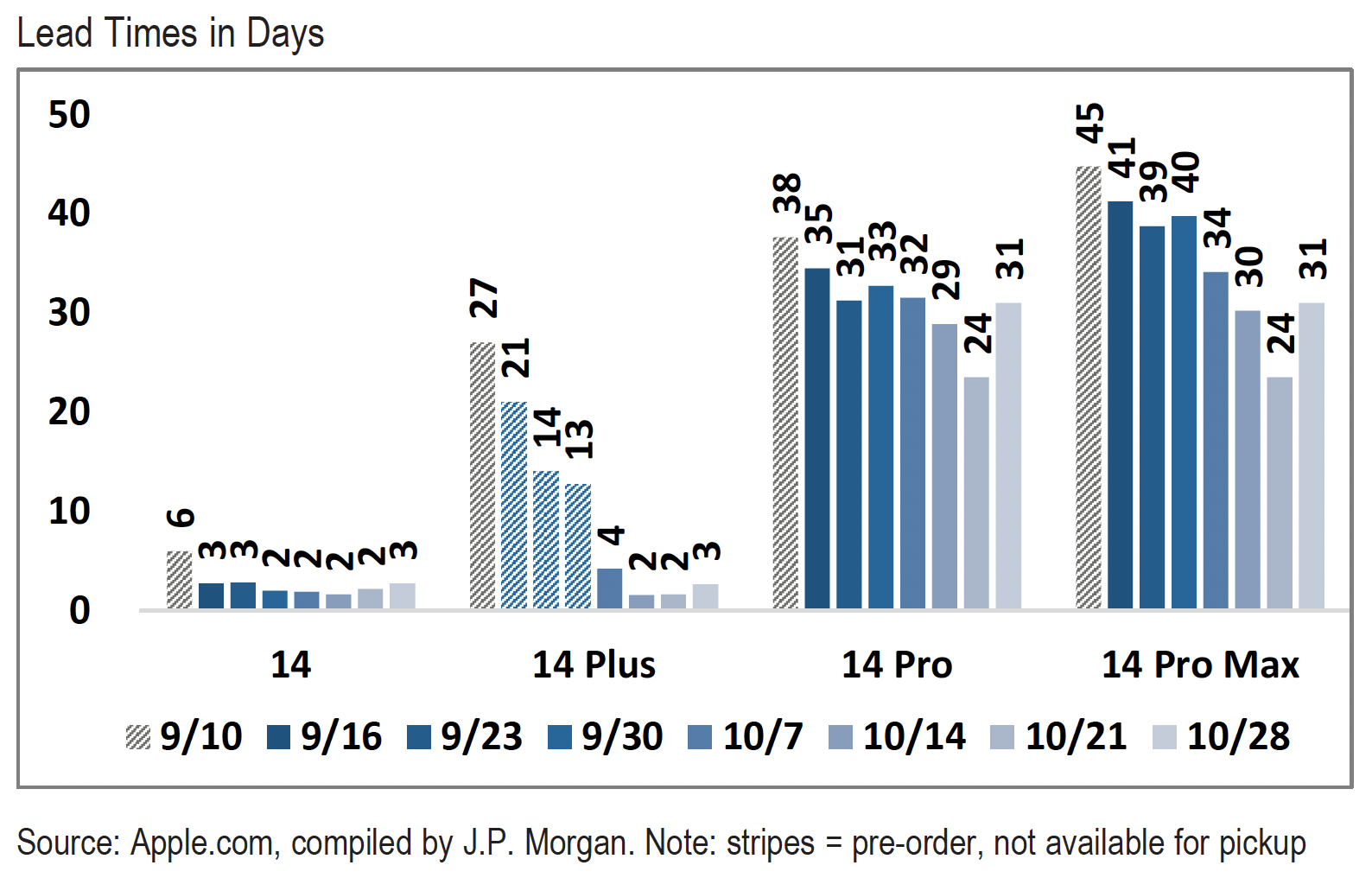

According JPM Availability Tracker, global iPhone lead times for the 14/14 Plus/14 Pro/14 Pro Max increased to 3/3/31/31 days in the 8th week since launch vs. 2/2/24/24 days in week 7. Lead times for the 14 Pro and 14 Pro Max were in line with comparable 13 models, while those for base 14 models were shorter.

JPM

It’s not common to see an increase in lead times after many weeks since launch, so the recently extended timeframes could be attributed to Covid disruptions in Zhengzhou, China, where a major iPhone assembly plant by Foxconn is located. Given China has consistently embraced a zero-Covid policy across major cities, Apple could potentially see a shortfall in iPhone shipment in the December quarter if conditions do not improve in Zhengzhou (responsible for 50% of global iPhone supply).

This again highlights Apple’s production risk in China. For perspective, Chinese contractors currently account for 98% of Apple’s iPhone production. Already, Apple is aiming to move production to other countries such as Vietnam and India. It’s unclear how fast Apple can cut its dependence on China, but according to Bloomberg it could take up to 8 years just to move 10% of production capacity out of the PRC.

Mac

Mac revenue increased 25% YoY to $11.5 billion, driven by the launch of the new MacBook Air and MacBook Pro on the M2 chip, manufactured using Taiwan Semiconductor’s (TSM) 4nm process. The increase in revenue was also due to Apple being able to meet unfulfilled demand in the June quarter because of supply chain disruptions.

Looking to the December quarter, management guided a challenging comp for Mac revenue on top of FX headwinds. In C4Q21, Apple launched the new M1 MacBook Pro, which was a key contributor to the top-line. Nevertheless, Mac has been performing extremely well in a difficult PC market, with a 16% market share in 3Q22, up from 15.3% in Q2 and 14.5% in Q1.

iPad

Revenue saw a 13% YoY decline to $7.2 billion on negative FX and a difficult comp due to the launch of new iPad models last year. However, management noted a record high installed base for the iPad, where 50% of purchases in the September quarter were from first-time buyers. In October, Apple launched the 10th-generation iPad starting at $449.

Wearables, Home and Accessories

Revenue grew 10% YoY to $9.7 billion driven by new products including the Apple Watch and AirPods Pro. Per management, Watch was a key top-line contributor where 2/3 of sales came from first-time customers, again a positive on the worldwide iOS installed base. The new Watch SE, Watch 8 and Watch Ultra remained supply constrained during the September quarter.

Services

Revenue from Apple’s Services division was up 5% YoY to $19.2 billion during the September quarter, while management noted growth would’ve been double-digit excluding the impact of FX. Further, Apple Services reached more than 900 million paid subscriptions vs. 745 million in F4Q21.

Within services, management expects weakness in digital advertising and gaming to extend into the current quarter while negative FX will also pressure the top-line. This is potentially driven by macro factors including a broader pullback in ad spend and less gaming engagement post-Covid. According to data from Sensor Tower, Global app store revenue saw a 4% YoY decline in October (until 10/30), whereas China app store revenue (26% of global revenue QTD) declined 3% YoY in October (10/30). Further, gaming (55% of global app store revenue) dropped by 12% YoY.

BofA

Per BofA estimates, Apple’s App Store and Licensing – Google (GOOG) pays Apple to be the default search engine on all iOS devices – could account for >60% of total Services revenue. While the data from SensorTower cannot predict Apple’s Services revenue with 100% accuracy, the trend remains negative in the current backdrop of slowing consumer demand.

Conclusion

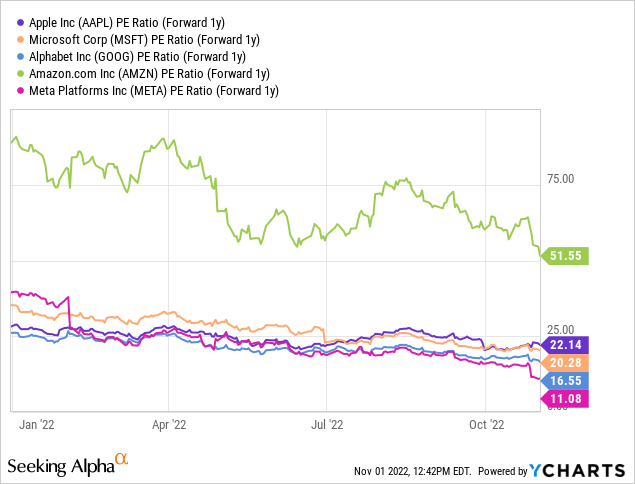

Overall, investors found Apple’s results and outlook better than feared, and felt safe enough to jump into the stock while most other major tech names were crushed after their earnings releases. Year-to-date, Apple’s stock is down only 15% while Microsoft (MSFT), Google, Meta (META), and Amazon (AMZN) are down 32%, 36%, 43%, 72%, respectively.

Investors are clearly treating Apple as a safe haven in this market, but the resiliency of Apple’s business in the current cycle is likely well understood, making any further macro pressure in 2023 seem somewhat underappreciated.

While Services are commonly known as the next major growth driver, the story looks less inspiring today in light of two straight quarters of declining revenue as well as unfavorable trends in the current quarter.

The iPhone should continue to perform thanks to a sticky user base that will create upgrade/replacement opportunities. However, the product has been around since 2007, and new models are getting less revolutionary. Though 5G could be the next driver, smartphones in general are in a much more mature stage of the product lifecycle today vs. 3-5 years ago. For now, it’s unclear what the “next big thing” is for Apple (VR in 2023? Apple Car in 20XX?).

At 22x forward earnings, shares of Apple seem fully valued, as investors have been dealing with a difficult environment where there are just not that many high-quality stocks to park their money in. This has been the dominant investment psychology throughout the year, so I’d question whether markets are buying Apple for the sake of Apple. As much as Apple is a great company, it’s never ideal to overpay for the stock.