brightstars

Thesis

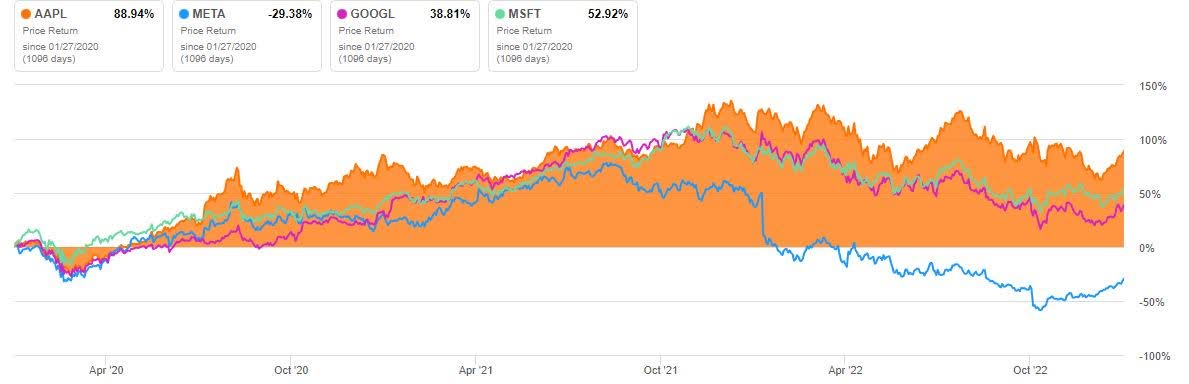

Apple Inc. (NASDAQ:AAPL) is a tech giant in search of future growth, and in my view it’s yet to find a clear avenue to get it. It has performed favourably compared to other big tech companies in the last few years, but this probably has more to do with aggressive share repurchases and impressively resilient earnings. However, in terms of developing cutting edge technology that will dominate the bottom lines of the next decade, I think they are falling behind. Poor positioning on these key developing technologies could have grave implications for the long-term valuation of Apple and is making them more of a consumer staples stock and less of a tech stock. Because of these factors I won’t be opening a position here.

Seeking Alpha

The Reality Pro

Estimates vary, but the AR and VR market could be worth $856 billion by 2031 with a mammoth CAGR of 41.1%. Apple will be making an entry into the AR/VR market with a yet to be unveiled Mixed Reality headset reportedly costing up to $3000, tentatively being termed the ‘Reality Pro’. Immediately, a price tag like that makes me sceptical even without any of the specs being released. Unless this is an experience not only superior to, but completely unchallenged by what competitors are offering, then it’s unclear whether the market for this price point exists in any meaningful capacity. The cost is an even greater concern in the current slowdown where consumers are cutting back on luxuries.

However, a budget model is also apparently in the pipeline due sometime in 2024-2025. The absence of this budget model on launch seems questionable though. Are customers really going to buy a $3000 headset as their first entry into the Apple VR ecosystem? Apple obviously has a strong brand, but I am not sure it is that strong. With VR products, the popularity of the product will determine the success of the entire ecosystem to a large extent, so if the initial model is a dud, it could sink the entire product line.

Interestingly though, Apple is developing a novel software that might well popularise their ecosystem of MR apps. The software enables users to easily design apps themselves, entirely code-free via Siri. This is potentially a big plus for the Reality Pro, as it provides a unique selling point as well as fleshing out a feature that might help justify the substantial price tag. This feature’s success or failure could play a big part in the ultimate fate of the Reality Pro.

This budget MR model comes at the expense of plans for AR glasses, which have now been indefinitely delayed. The AR play is particularly crucial for Apple, because it is possible that AR glasses become the smartphones of tomorrow. If this happened, Apple would have to establish a dominant market share like that of the iPhone to survive, and likely be at the forefront of development.

Out of the two, AR seems like the natural evolution for Apple products. AR glasses have utility in daily life in a similar way to smartphones and seem easier to scale down to the sleek, aesthetically pleasing design associated with Apple hardware. This is why the AR development being pushed back is particularly worrisome for Apple in my view.

The Apple Car

It’s hard to believe, but Apple has had automobile ambitions for over a decade now. Steve Jobs was said to “dream” of creating an iCar before his death in 2011. The project has since become reality, but was plagued with nonstop setbacks including a 2018 partnership with Volkswagen (OTCPK:VWAGY) falling apart. Now, the internal release target has been shifted back to 2026 and the proposed self-driving capabilities have been scaled back. These red flags are not the only reasons the project was doomed to disappoint, however. Self-driving primarily relies on AI technology, and the next section addresses why Apple is likely behind the curve on this.

AI

I strongly believe that within the next decade, AI will become the standout technological innovation and therefore the driver of economic growth. The AI market is predicted to grow to $1.394 trillion by 2029. ChatGPT has generated a lot of hype, but really it is just the AI Model that has garnered the most publicity because it is so accessible to the public. Similarly impressive AI models are rapidly being developed, but usually they are not released publicly. Just last year for example, DeepMind produced a ‘generalist’ AI capable of performing many different tasks and playing games called Gato. With regards to AI development, Apple seems to be lagging competitors in big tech.

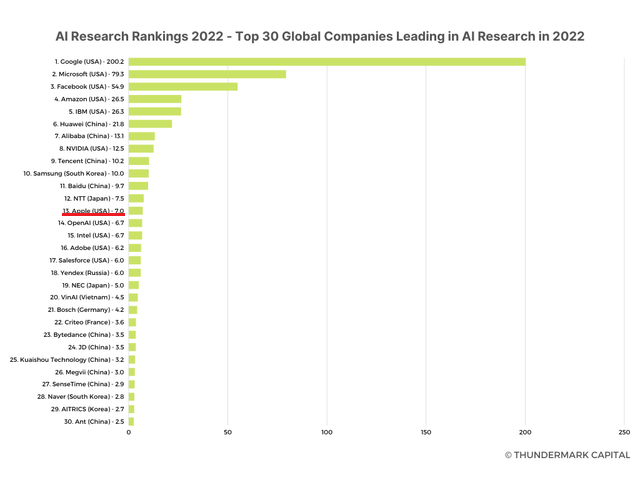

Google (NASDAQ:GOOG) has DeepMind, Microsoft (NASDAQ:MSFT) has OpenAI, Meta (NASDAQ:META) has Meta AI and Apple has…Apple Machine Learning Research. It’s safe to say the name brand recognition for Apple’s AI lab is not at the same levels as others-which would not matter at all if the lab seemed to be of the same quality as competitors. Except, by some metrics that does not seem to be the case. The graph below shows major companies ranked by the number of publications that made it into the two most prestigious AI conferences held annually (NeurIPS and ICML). Apple ranks 13th, well behind many other tech companies but also crucially with a score some orders of magnitudes behind the leaders, Google, Microsoft and Meta. Now, obviously this is not a perfect proxy for success in AI research, let alone AI research that will translate into commercially viable products-but it does indicate roughly which companies are at the forefront of AI research.

Thundermark Capital

Reinforcing this data are the opinions of AI researchers. When asked to rank the top AI labs worldwide, AI researchers don’t tend to select Apple in the top three, instead generally preferring Google, Meta and Microsoft (or labs under their ownership).

Acquisitions Could Be An Answer

Apple could be snapping up potentially undervalued companies in numerous nascent tech sectors right now. Instead, they use their hefty Free Cash Flow to prop up their own share price through share repurchases. This is not inherently a bad thing, it absolutely could be the most prudent strategy, but I do have a concern they are sleepwalking towards stagnant growth rates in the long term.

Valuation

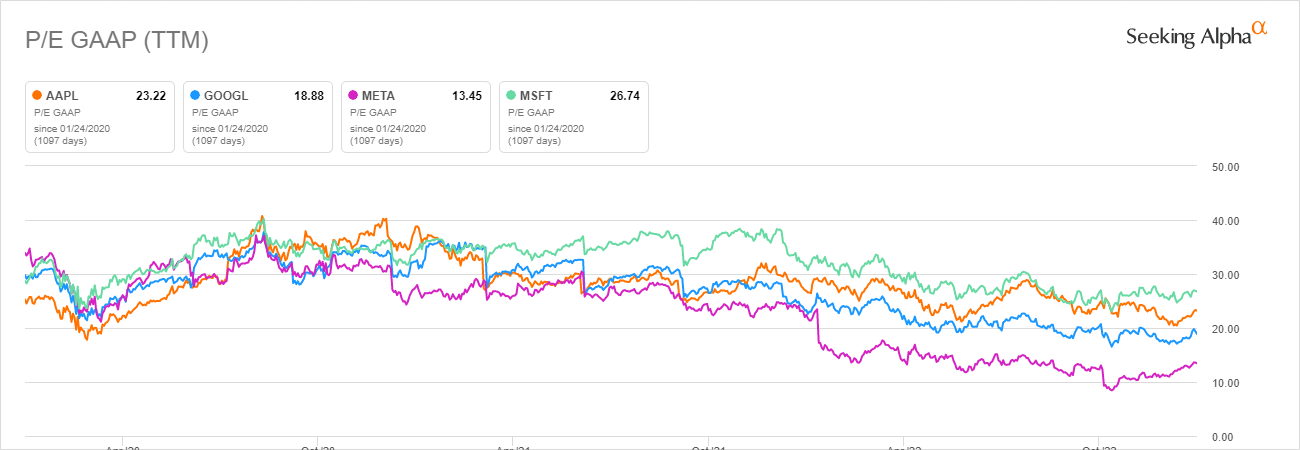

Apple trades at a forward and trailing P/E of about 23, as shown below this puts it in the upper end of the range with regards to other big tech companies. However, this premium is probably somewhat justified owing to resilient earnings in Q4 and a continued regimen of share repurchases. If my expectations for AI are accurate and Apple’s other emerging technology plays are mediocre enough that they do not make up for that, then their relative premium compared to the competition might not be justified.

Seeking Alpha

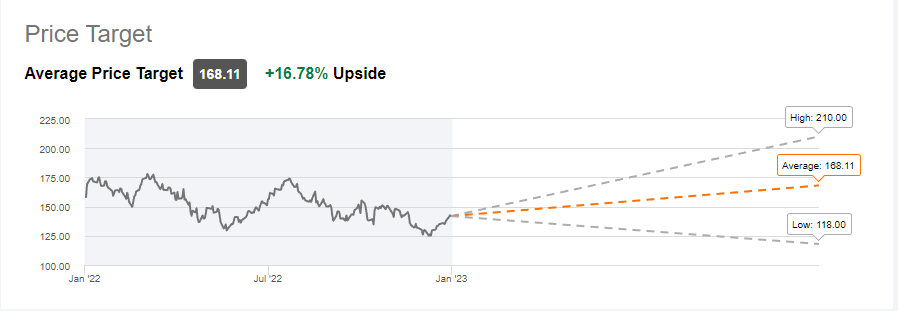

Wall Street has a somewhat optimistic target on Apple in my view of 168.11 implying a 16.78% upside from current prices. I don’t think it fully reflects Apple’s relatively weak positioning in emerging technologies, so the lower price targets seem more convincing to me.

Seeking Alpha

Conclusion

Apple is an amazing company with a great product line and strong brand loyalty, but I am concerned their current positioning on emerging technologies and products are much weaker compared to the competition. As such I will be waiting for a lower entry on the stock, or alternatively better news on key areas like AI, VR/AR and the Apple car project.