Joe Raedle

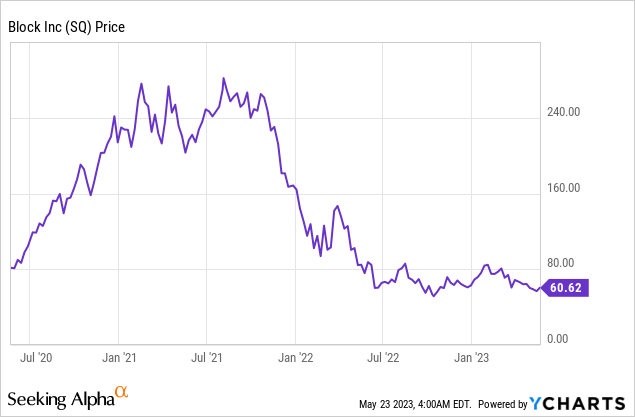

I’ve covered Block (NYSE:SQ) on several occasions, and have generally been constructive on this name. Notably, I covered the company in early April, presenting a $109 share price target.

Block is a thriving fintech company that has developed at least two “growth engines”, its popular Cash App and its Square ecosystem. These two services, create a variety of touchpoints with an underserved user in a huge market (~$75B for the Cash App alone). In the first quarter of 2023, the company reported strong results beating both top and bottom-line forecasts for growth. Given its founder and CEO Jack Dorsey is now back full-time at the business (having left Twitter) I’m not surprised to see outstanding execution even given the tough environment for financial companies. In this post I’m going to break down its financials, before revealing my valuation and forecasts for the stock.

Growing Financials

Block reported strong financial results for the first quarter of 2023. Its revenue was $4.99 billion which beat analyst forecasts by $385 million and rose by 25.99% year over year.

This growth rate was a stark improvement over the negative 22% YoY growth rate reported in Q1,23 and the 14% growth rate reported in Q4,22. This is a positive sign as I have stated in prior posts that the main decline in revenue was driven by lower Bitcoin transactions since 2022, which has now started to be lapped since the prior year. In addition, the price of Bitcoin has actually risen by 55% between November 2022 and May 2023. This drove the total sale amount of Bitcoin to customers to $2.16 billion, up a rapid 25% year over year.

Block’s transaction revenue rose by 15% year over year to $1.42 billion. However, the real surprise was its subscription and services revenue which increased by a rapid 42% year over year to $1.37 billion. Its subscription revenue now makes up 27.9% of its total, which is great for diversification.

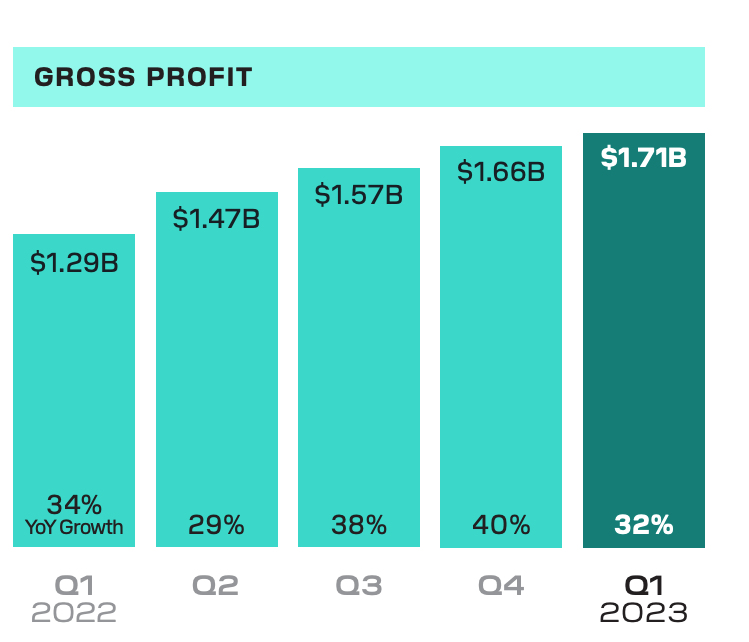

Moving onto Gross profit which is also a primary metric for Block. The business reported a rapid 32% year-over-year growth to $1.71 billion. This is a solid growth rate given it included $19 million related to the amortization of assets related to its acquired Buy Now Pay Later [BNPL] platform.

Gross Profit (Q1,23)

Bitcoin has never been a major profit driver for the business (~2.4% gross margin), so despite the large increase in transactions, bitcoin gross profit only added $50 million, up 16% year over year.

This may not seem great but keep in mind, Crypto is just one touch point in Block’s ecosystem and the idea of it is to encourage interaction with other parts of the app. For example, a user may sign up just to trade crypto and then find themselves using Block’s cash app as their go-to digital wallet/private bank account, which is where the real customer lifetime value [CLV] will be found.

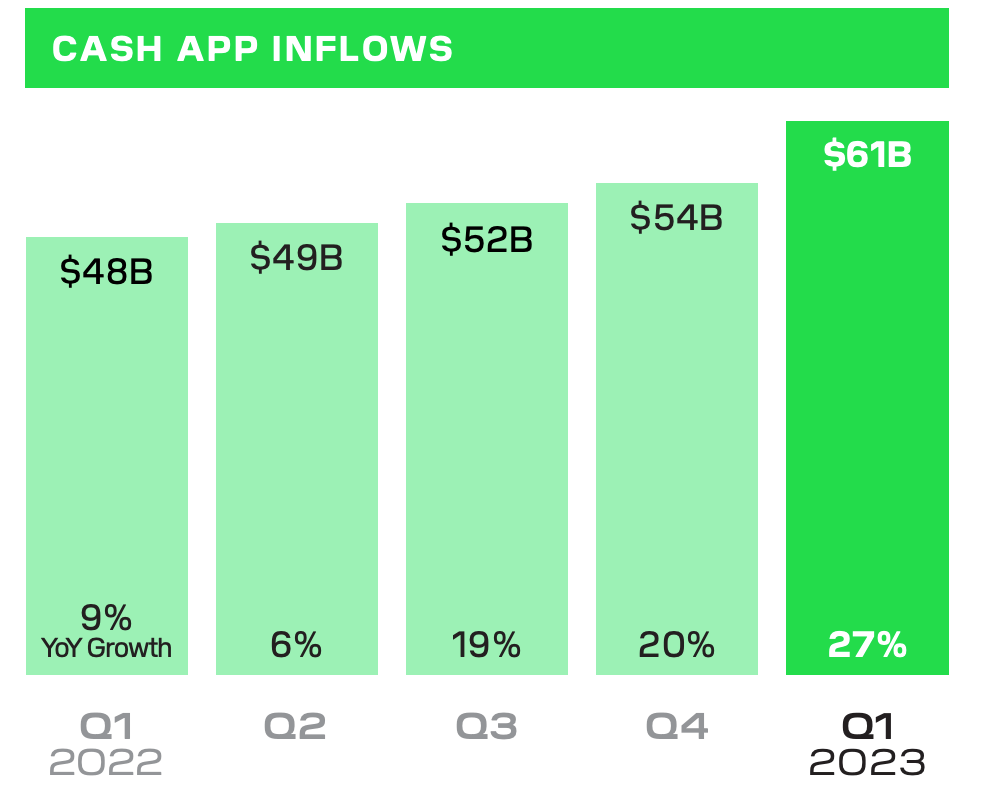

Cash App inflows rose by 27% year over year to $61 billion. This was a much faster growth rate than the 20% YoY level reported in Q4,22. The Cash App looks to be relatively insulated from the lower consumer demand expected due to the macroeconomic environment. I believe this makes sense as even if users are spending less, they may wish to save it or invest it, both of which they can do inside the Cash App ecosystem.

Cash App Inflows (Q1,23)

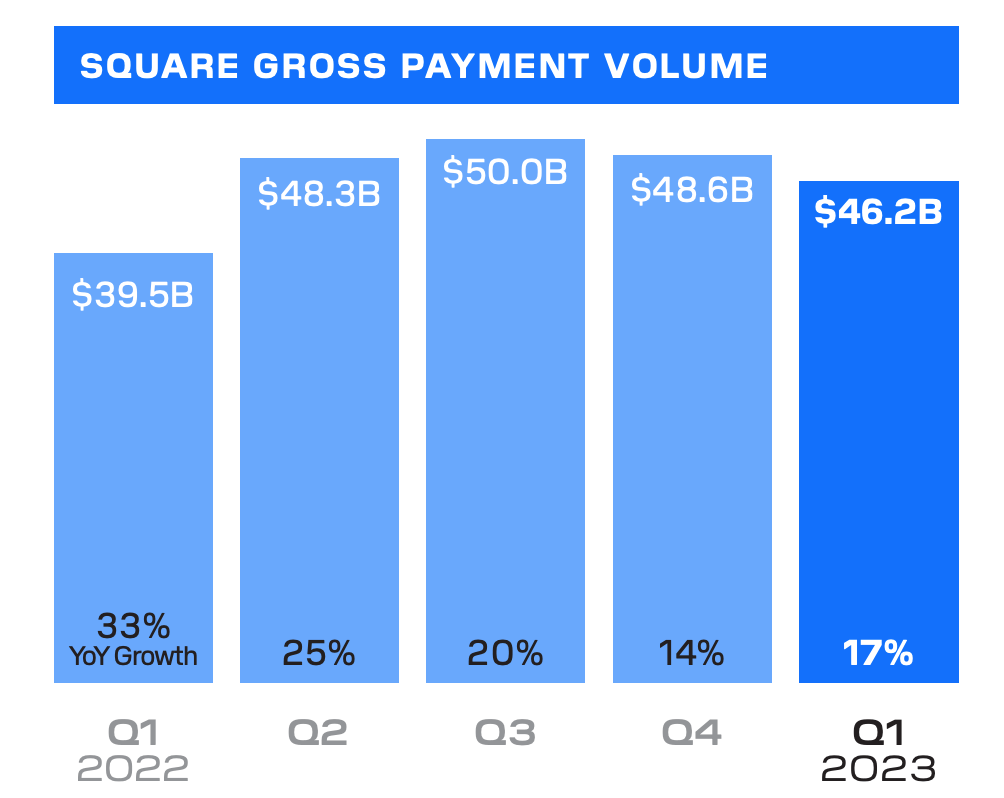

Block’s Square ecosystem, saw an expected drop in Gross Payment Volume [GPV] from $48.6 billion (at the Q4, peak holiday shopping season) to $46.2 billion in Q1,23. A positive was this still increased by 17% year over year. In addition, its international growth was strong at 33% YoY relative to 14% YoY in the U.S for GPV. One of management’s key growth pillars has been to scale internationally into less saturated markets. This strategy looks to be working fantastic so far and is a testament to the execution of the business.

Square Gross Payment Volume (Q1,23)

Square Loans was surprisingly strong in Q1,23, with $1.10 billion in originations (113,000 loans) up 46% year over year. I believe the vast number of these loans is a key competitive advantage for Square as it has data on the Small-Medium sized business market, which has historically been underserved by traditional banks. Given Square’s PoS (Point of Sale) terminals track transactions, cash flow etc, this enables more accurate underwriting. The business also benefited from $1 million from PPP loan forgiveness in Q1,23, which was positive.

Margins and Expenses

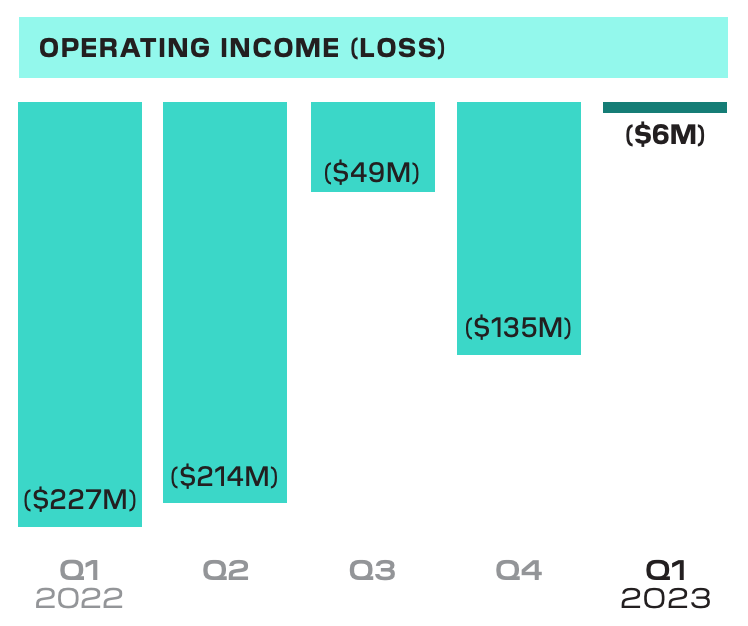

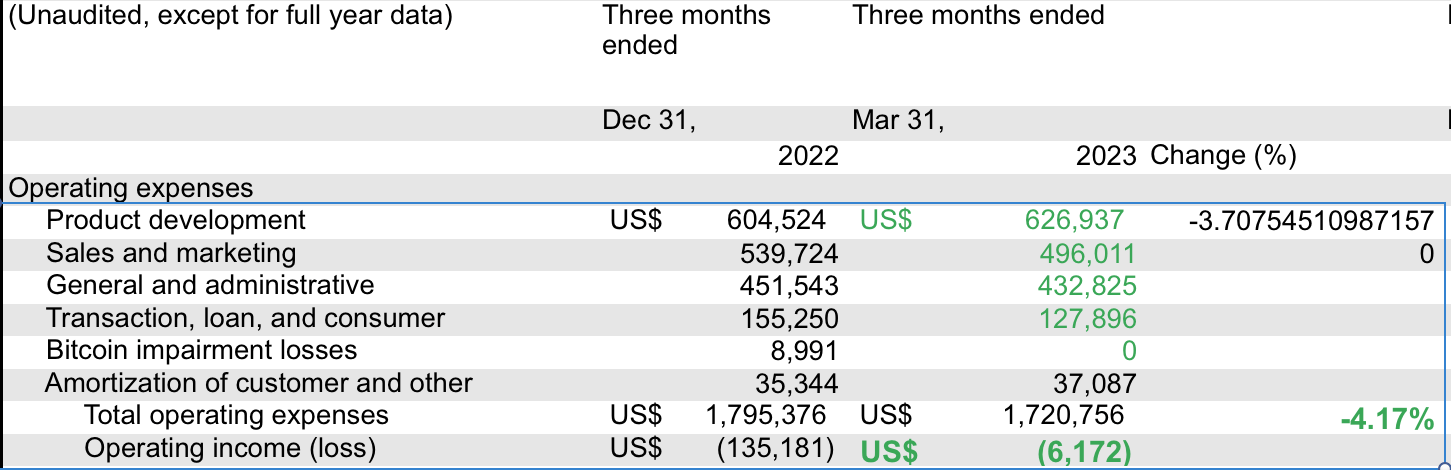

Block reported a $6 million operating loss in Q1,23, which is a vast improvement from the $135 million loss in Q4,22. This was fantastic to see given the high cost of capital and investor sentiment for “profitability” as opposed to growth at all costs, which was the prior rhetoric. On an “adjusted” basis its operating income was actually positive $51 million. However, this doesn’t include bitcoin “impairment losses”, amortization of intangible assets (related to acquisitions), and of course stock-based compensation.

Operating Loss (Q1,23 data)

Either way, the raw operating loss improvement, was driven by solid top-line growth combined with moderately lower expenses. Total operating expenses was $1.72 billion in Q1,23, down 4.17% sequentially. This was driven by 3.7% lower Product development expenses. In addition, to moderate corrections in G&A, S&M and transactions. As mentioned prior, the boost in the price of Bitcoin has reduced its impairment loss to zero, which effectively means Block is at break even on its purchase. These trends are all positive and I expect further operating leverage improvements moving forward, which I will discuss in greater detail in my “valuation and forecasts” section.

Block Expenses (Q1,23 financials with author annotations)

Block also has a solid balance sheet with $6 billion in cash and short-term investments. In addition, the company reported total debt of $5.6 billion of which the majority $4.4 billion is long-term debt. This is more than enough liquidity to weather any economic storm.

Valuation and Forecasts

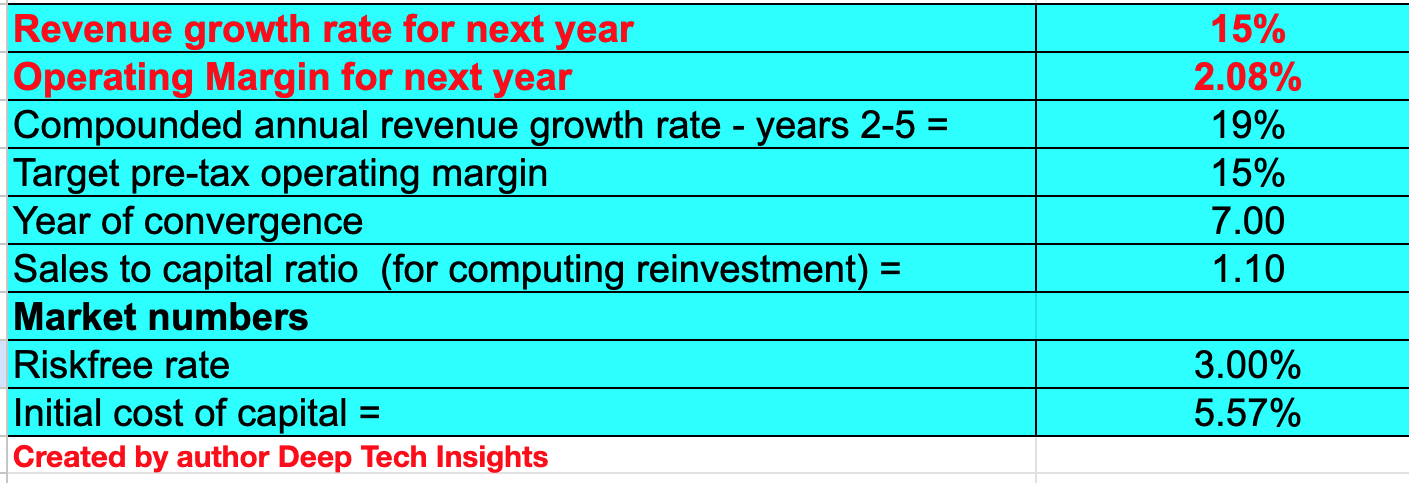

In order to value Block, I have plugged its latest financial data into my discounted cash flow valuation model. Relative to my prior post, I have revised up my forecast of growth for “next year” or the next four quarters by 2% to 15%. This is still fairly conservative given the strong ~26% YoY growth rate reported in Q1,23. However, I believe we will see further declines in GMV for Square, as consumer demand slows during the latter half of the year.

In years 2 to 5, I have also revised up my forecast from 17% to 19%, due to the strong quarter. In addition, I forecast a rebound in consumer demand post any forecasted recession. I also expect continued growth in the cash app and further growth in international markets, as per the current trend.

Block stock valuation 1 (Created by author Deep Tech Insights)

Forecasting Block’s operating margin long term, is a much harder challenge. We have seen improvement in Q1,23 and the business is close to break even, which it has achieved previously. Given a mature fintech company such as PayPal (PYPL) has a 15% operating margin, I believe Block can achieve close to this long term, thus I have forecast this over the next 7 years. I have also capitalized the company’s R&D expenses for increased accuracy.

Block stock valuation 2 (created by author Deep Tech Insights)

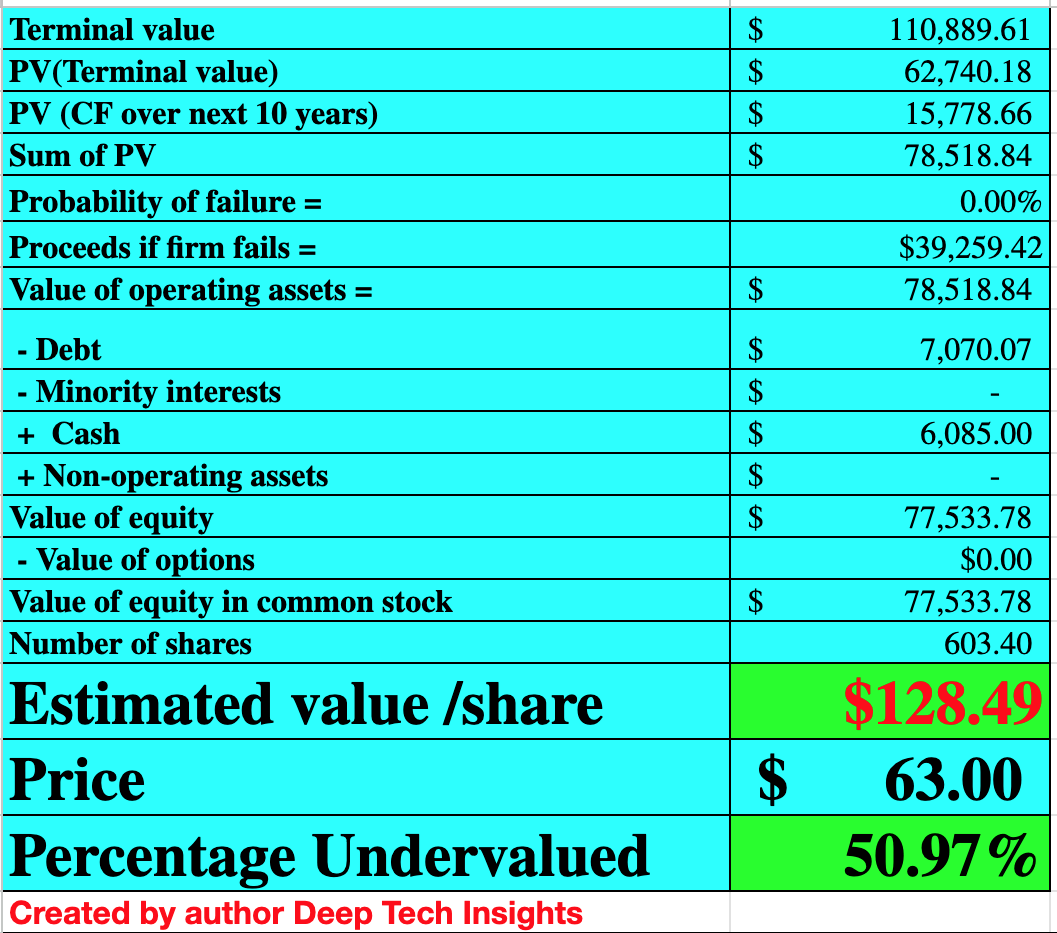

Given these factors I get a fair value of $127.79 per share, the stock is trading at ~$63 per share at the time of writing and thus is 53% undervalued.

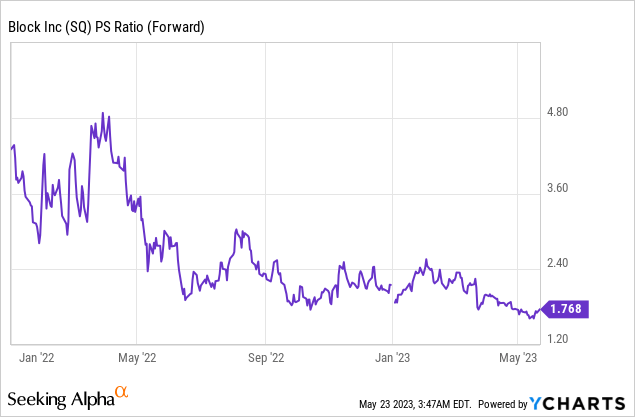

As an extra data point, Block trades at a forward P/S ratio = 1.78, which is over 70% cheaper than its 5 year average.

Risks

Recessionary Environment

As mentioned prior the forecasted recession will likely impact Square’s SMB revenue and possibly even its cash app. Therefore this must be taken into account, as I have done in my valuation model.

Final Thoughts

Block is a tremendous company that has developed two substantial growth engines. This business is more diversified than prior years and Its financial results have been surprisingly good in Q1,23, given the tough economic backdrop. I also haven’t mentioned Block’s other bets such as Spiral and TBD, two Bitcoin-focused development projects, which could offer huge potential. However, I personally believe this would just be the cherry on top and my forecasts just include its two main ecosystems. Given my valuation model indicate the stock is undervalued deeply, I will deem it to be a solid buy for the long-term investor.