aapsky

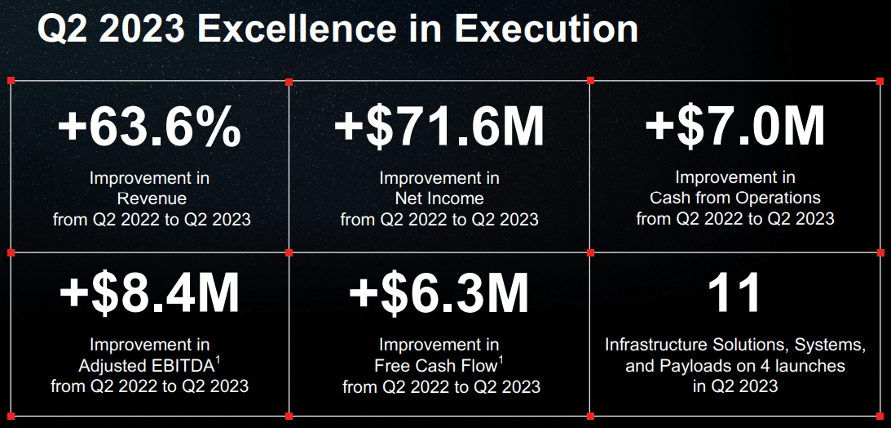

Space infrastructure company, Redwire Corporation (NYSE:RDW) released its second quarter earnings results on Tuesday. Notably, the company’s revenue surged by over 63% in comparison to the same period last year. The company also managed to substantially reduce its net loss, narrowing it down to $5.5 million from the previous year’s significant loss of $77 million. Moreover, a milestone was achieved as the company marked its first-ever quarterly generation of positive cash from operations and positive free cash flow. Redwire stock rose as much as 9% in after-hours trading following the earnings report.

Company’s Presentation

As highlighted in the analysis title, there are indications that the company is making good progress in terms of revenue, profitability, and cash flow. The company is showing potential to grow in the sector, but still with some problems to solve, like liquidity and debt position. Therefore, while it might appear cheap and an attractive bet in the future, investors should keep in view closely on the metrics to be discussed later. Therefore, a hold rating is assigned.

Now, let us delve into the pivotal highlights within the earnings report that hold significant importance for investors’ careful consideration.

Results Overview

Analyst’s Research (Produced by SankeyArt)

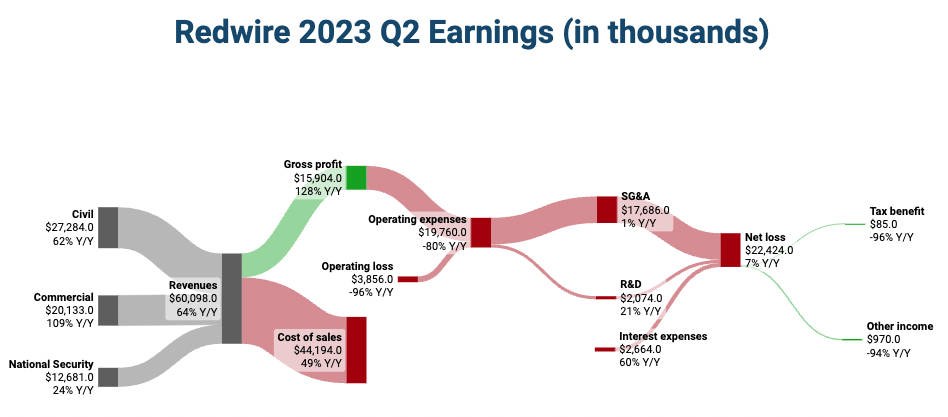

Taking a cue from App Economy Insights, I decided to initiate my earnings review by introducing a Sankey Chart. This visual tool adeptly portrays the financial flow, meticulously displaying the movement of funds across various income and expense components.

Revenue of Redwire increased 63.6% year on year and 4.3% quarter on quarter. The main revenue driver is from commercial clients, which has doubled compared with last Q2. Notably, out of the $60 million total revenues, $14 million, or about 25%, came from the company’s most recent acquisition Space NV. This has shown that the acquisition made last year, which has been an earning-positive business, is contributing to the company’s increasing sales.

Redwire’s revenue has experienced a remarkable surge of 63.6% on a year-over-year basis and 4.3% increase on a quarter-over-quarter scale. This growth surge is predominantly propelled by commercial clients, marking a doubling from the previous Q2 figures.

It is worth highlighting that, out of the total revenue sum of $60 million, a noteworthy $14 million – accounting for approximately 25% – can be attributed to the recent acquisition of Space NV. This has shown that the acquisition, accomplished last year, has emerged as a positive contributor to the overall revenue growth.

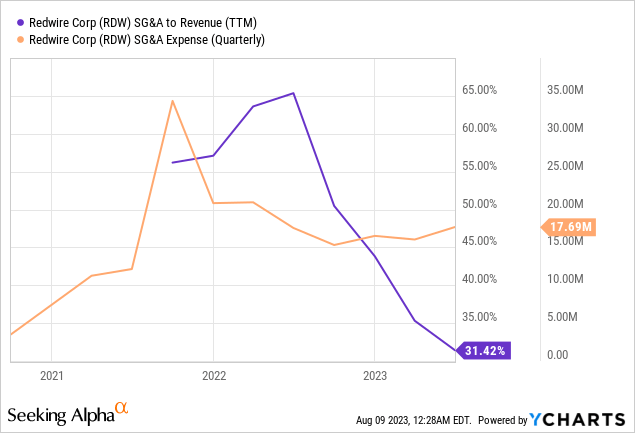

Despite an expanding margin, which we will delve into later, the company has reported a net loss. This is primarily due to selling, general, and administrative costs, including an investment of $1.9 million in systems and infrastructure. A positive aspect here is that the management has mentioned that SG&A expenses have remained and will continue to remain stable going forward on an absolute basis. This sets the stage for achieving net profit as long as the company continues to grow its sales.

Sales Pipeline

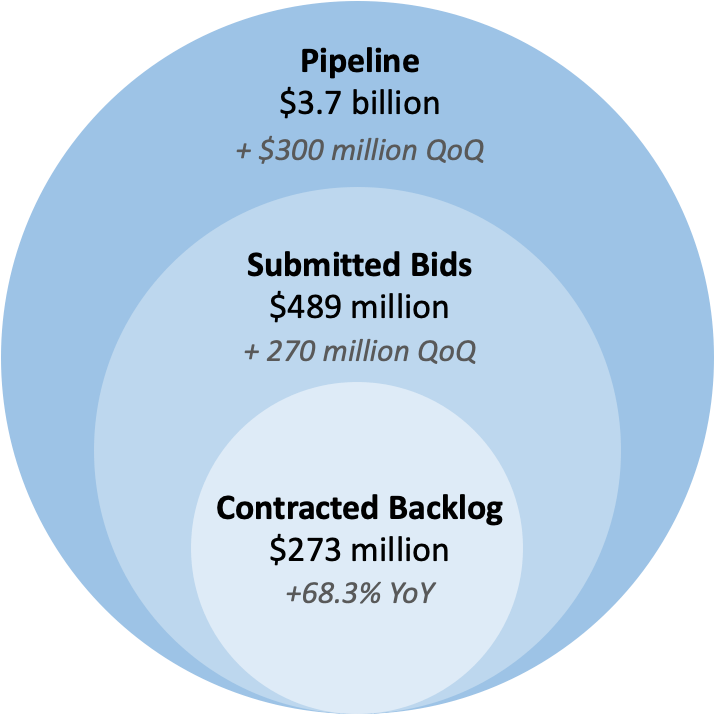

During the earnings call, several terms were discussed concerning the company’s longer-term business prospects. To provide a clearer understanding of the distinctions between these terms and their implications for the company’s business outlook, the following graph proves to be an informative visualization tool.

Analyst’s Research

While the company has stated a pipeline of $3.7 billion and approximately $490 million in submitted bids that are currently under evaluation by potential clients, the management has not disclosed a conversion rate or level of confidence regarding the eventual conversion of these figures into actual sales.

Consequently, the most relevant and meaningful metric in this context is the contracted backlog, which represents sales that have been confirmed and secured. The impressive nearly 70% year-on-year growth in the backlog is a positive indicator, underscoring Redwire’s successful establishment of a substantial pipeline for delivering infrastructure and engineering services.

A key element emphasized by the management is the company’s increasing expertise and completion of projects within the rapidly expanding national security sector. This strategic focus has allowed Redwire to gain the necessary “documentation that allows you to participate in more classified work.” Monitoring how the company continues to execute in this area remains crucial for assessing its trajectory in the foreseeable future.

In view of the management’s targets and the growing contracted backlog, the revenue guidance for FY2023 stands at $220 million to $250 million. While this projection indicates a robust 46% year-on-year expansion, it is consistent with the pace maintained during the initial two quarters, which totaled $117.7 million. With a prudent approach by the management, investors can closely monitor project completion milestones throughout the year for potential surprises in the upcoming quarters.

Profitability

There are two positives from this earnings result in relation to profitability.

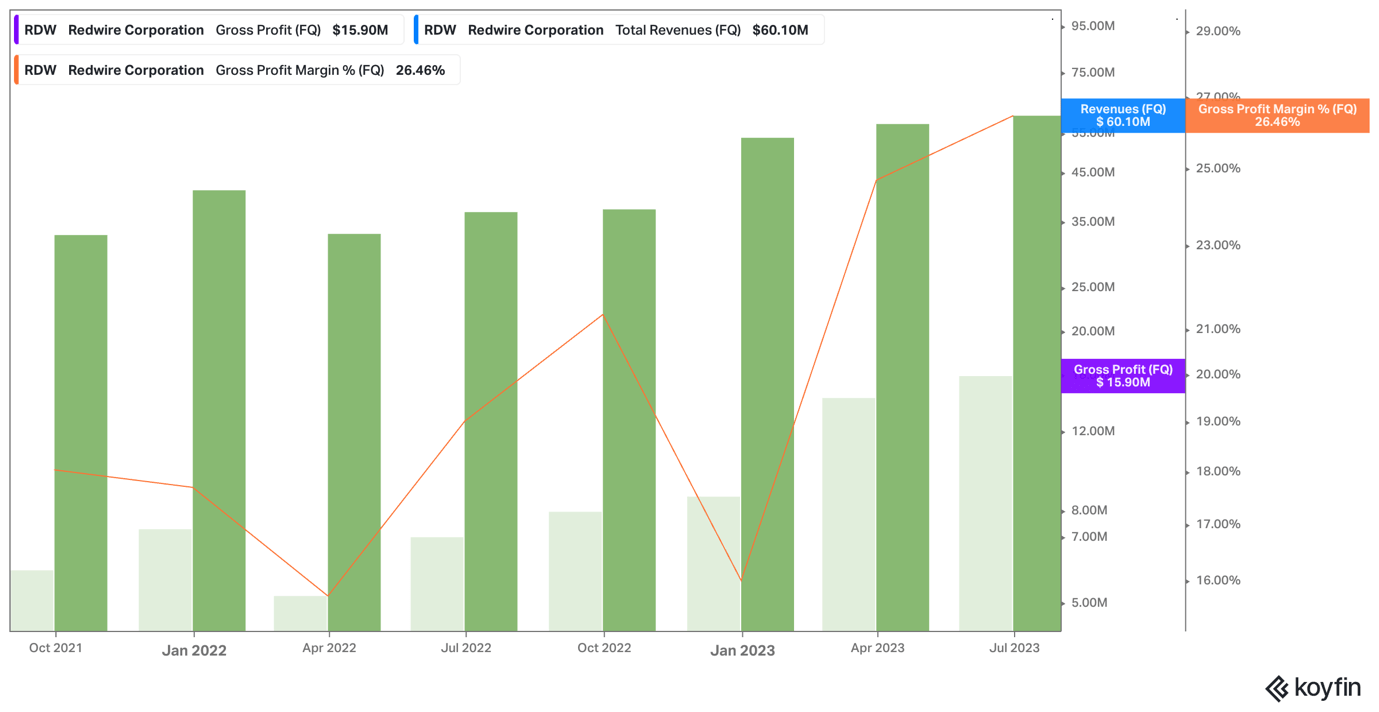

Gross Margin: Continue to expand with better mix and new acquisition

The first one is on gross margin. While investors are worried about the sluggish margin growth in the past year, gross margin ratio has been improved to 26.5%, mainly attributed to the management initiatives such as rolling off low-margin contracts, better program management, etc.

Koyfin

Having closely followed Redwire over a period of time, I have always been attracted by the company’s ability to provide diversified space-based products and services, from drug manufacturing, production of crystal, to the more ordinary space 3D printing and commercial space station. However, this diversification has occasionally led to challenges, resembling “chasing after” various clients that demand significant groundwork and impact profitability.

This year, though, a shift has been observed as the company is securing recurring contracts. From my standpoint, this is critical in enhancing the profit margin, since it brings about a reduction in the need for extensive investments and capital expenditures that typically accompany the development of new products and services.

Of course, the new acquisition of Space NV has also been helpful in improving the margin in the Europe market, since the company has originally been a profitable business that can bring synergies to the core company. Therefore, I deem this acquisition an initial success.

Earnings: Perfect expenditure control leads to positive cash flow, but pay attention to some details

SG&A, a significant cost component in the income statement, accounting for nearly 30% of sales, has remained flat over the past year. This stability indicates effective management of the company’s overall expenditure, resulting in a decline in spending in proportion to sales. Consequently, coupled with the growth in gross profit, this trend provides an encouraging indication that a positive earnings outcome is on the horizon.

However, while most analyses predominantly center on the company’s consecutive attainment of positive adjusted EBITDA and its achievement of positive free cash flow on Redwire’s Q2 earnings, certain aspects require investors’ attention:

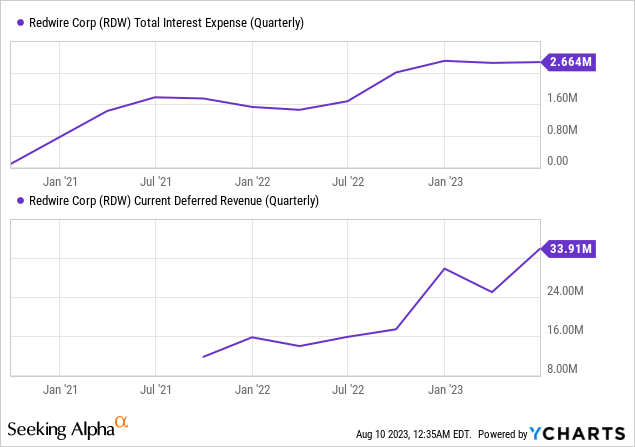

- Interest expense: It is noteworthy that interest payments have escalated on a year-on-year basis, which is added to the GAAP EBITDA to calculate the adjusted earnings, encompassing a substantial 61% share of the adjusted EBITDA. Given the company’s expanding debt position and the anticipated utilization of new borrowing capacity, interest expense will potentially increase further.

- Deferred revenue: $8.9 million of increase in deferred revenue is added to the cash flow that contributes to the positive total operating cash flow of $2.8 million and positive free cash flow of $1.1 million. Deferred revenue, also known as unearned revenue, is an advance payment for the company. For investors, understanding this one-off cash flow surge is pivotal for assessing the company’s progression toward positive cash flow.

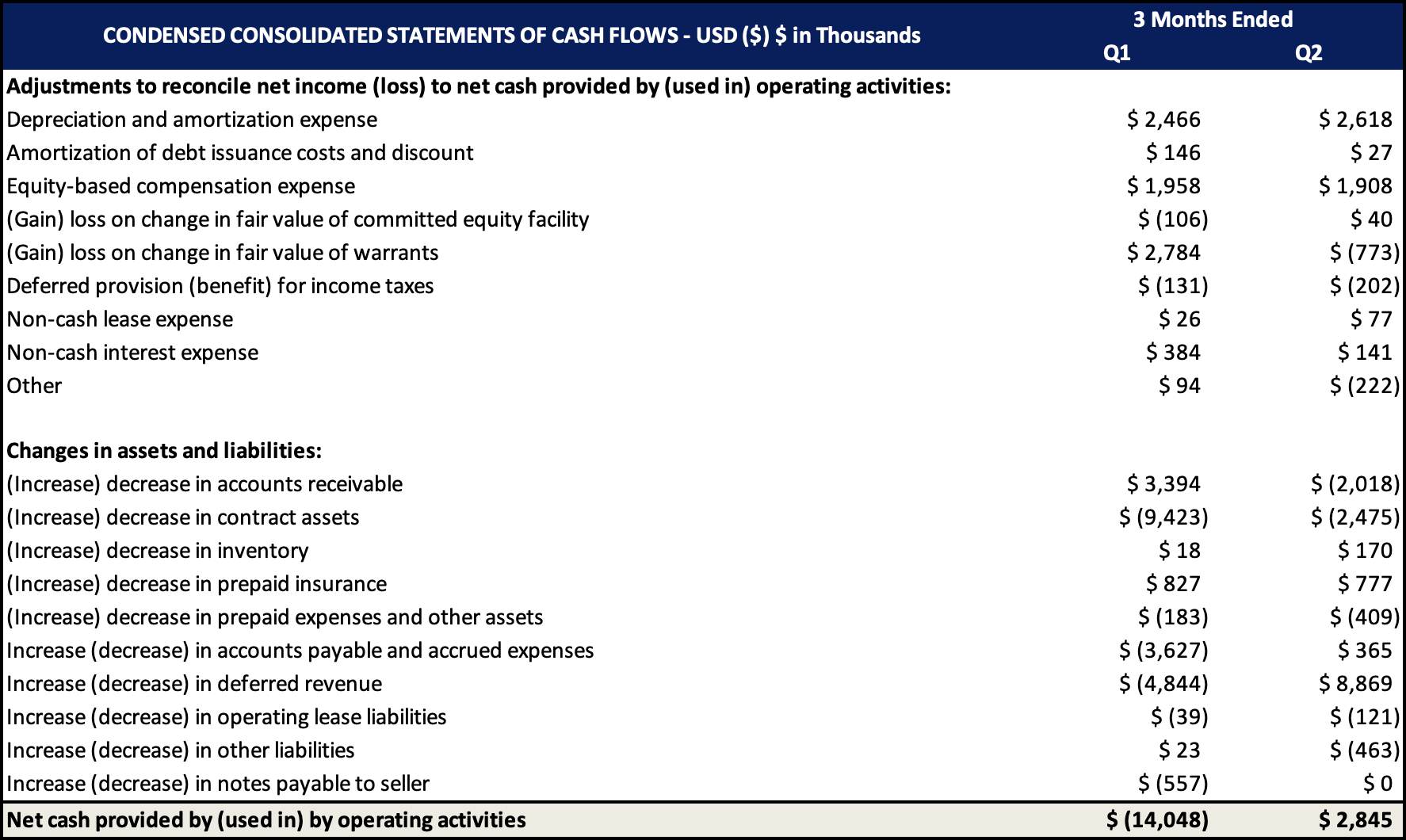

In the company’s 10-Q, a cash flow statement spanning six months has been furnished. As a result, I have delineated the individual cash flow statements for both Q1 and Q2 below.

Company 10-Q; Analyst’s Research

Valuation

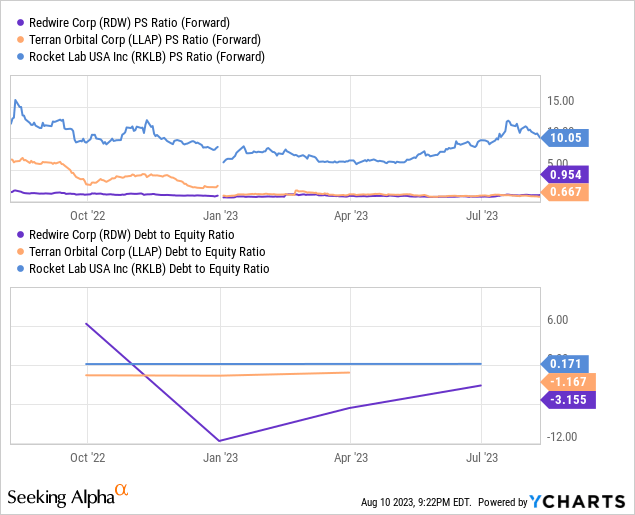

The current market capitalization of the company stands at approximately $220 million, with an EV-to-Revenue ratio of 1.4. This might appear as cheap, especially considering the company’s expanding pipeline. However, investors should keep in mind the company’s high debt-to-equity ratio, exceeding 140%, in addition to other liquidity ratios that are underperforming.

Hence, in evaluating Redwire, the question is not “if the company is cheap compared to its peer”, but rather, “if the company is sustainable in terms of liquidity and profitability”. Before getting to a valuation similar to that of its top-performing peer, Rocket Lab (RKLB), it is crucial for the company to prioritize its debt-to-equity ratio. This involves improving both parts of the equation.

Conclusion

Although Redwire stands as one of my preferred stocks among various space technology stocks, and the company is showing promising indicators toward profitability and positive cash flow, investors should remain cautious and for at least another quarter. Certain uncertainties still exist concerning aspects such as profit margins, earnings, and cash flow.

The only thing that is more certain is the company’s need to leverage additional debt for business financing, which presents an additional risk for investors. Consequently, a “hold” rating is recommended for the company at this juncture.