Last week, newly installed Xero chief executive Sukhinder Singh Cassidy revealed that the company had spent on average $NZ30 million ($27.76 million) every year for 10 years in the US. “People have had all sorts of wildly inconsistent numbers on what we’ve spent in the US,” she said.

“Relative to the size of that market and opportunity, we believe, on average a net investment of $NZ30 million a year is pretty measured,” she said, adding that the figure was comparable to what US-venture-backed businesses would invest.

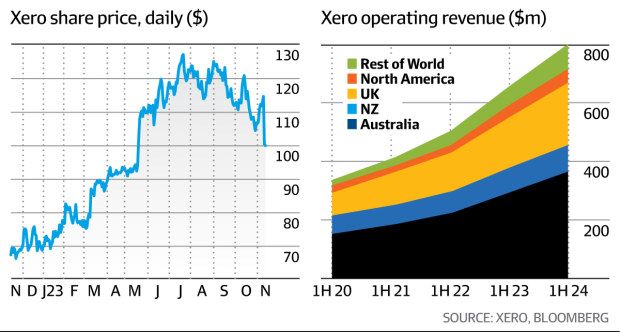

After spending $NZ300 million, Xero has gained 396,000 subscribers in North America (including customers in Canada). It added 12,000 subscribers in the last half and revenue increased 9 per cent to $NZ47.3 million.

Overall, Xero has almost 4 million subscribers. While the bulk are in Australia and New Zealand, it has more than 1 million customers in the United Kingdom. Analysts worry that the company has overinvested in US – or is in danger of doing so – with growth elsewhere a bigger opportunity.

After a trip to Silicon Valley, analysts at Jarden told clients last month that they were also worried about Xero’s ability to take on its US rival, software giant Intuit, which makes QuickBooks. “Meetings with … partner channels, Intuit sales and product teams in the US leave us still unconvinced that [Xero] can efficiently deploy its resources to win in this market,” they wrote.

For years, the US has been the problem child for Xero. Singh Cassidy, who replaced former CEO Steve Vamos in February, ordered a review into the company’s operations in the region over the past 10 years.

It found the US operation had suffered from frequent changes in sales leadership, chopping and changing its go-to market strategies, and inconsistent investment in its product development.

During an earnings call last week, outlining the company’s accounts for the six months to the end of September, Singh Cassidy said Xero would narrow its focus to two key segments in the US. They were small businesses “with multiple jobs to be done” – higher-value subscribers that rely on several parts of the software to run their accounts – and the client advisory services segment of accountants and bookkeepers.

More questions than answers

The result missed the market’s expectations for its revenue and profit, and Xero’s share price dropped 13 per cent, falling back below $100.

Elise Kennedy, Jarden’s head of technology, said the half-year results, “left us asking more questions than those answered around the US strategy, cost base and other revenue opportunities.

“It is unclear to us how Xero is going to get economies of scale to deliver operating leverage if it is scaling to only two segments in the US and not driving other revenue into new markets and/or the ecosystem,” she said.

“Having said that, it is early days and only a few months post the effective outcome of the earlier redundancies and start of the US revised strategy. A strategy shift can take two to three years to see the output.”

Analysts at Morgan Stanley, meanwhile, said there was a risk that Xero’s international markets would fail to gain traction, resulting in larger cash burn. The US business review showed focused growth opportunity with measured cost base, the investment bank’s brokers added.

The company plans to increased its US-based product and engineering support to help localise its product. It has also revised its operating structure so the US and Canadian country heads report directly to Xero’s new chief revenue officer, Ashley Grech, Square’s former head of sales.

Without revealing exactly how much Xero would continue to spend in the US, Singh Cassidy said any investment would be relative to how much revenue the region generates. With the ambition to turn Xero into a high-performing global software business, she will need to show the US can finally deliver the scale it has long promised – without the big price tag.