gece33/iStock via Getty Images

Based on its performance this week, Bitcoin (BTC-USD) pretty much failed its most recent trial as a flight to safety asset. The unwinding of the yen carry trade this week had spooked markets across the world, and we saw the VIX hit 60, which was one of its highest readings in history. This was clearly a time when some assets did experience a flight to safety. U.S. treasuries, for instance, saw an unusual price appreciation, as reflected by a broad shift down of the yield curve.

BTC crashed from $62000 to $52000 between Saturday (3 August) and Monday (5 August). Spot markets were not open for most assets at this time. The S&P 500 only fell 3.8% between Friday and Monday morning. By Monday at market close, most risk assets, including BTC had started a climb back from this dip.

It’s important to note that the S&P 500 is down just 6% from ATH (set just last month), but BTC is down 17% from the local top of $68000, set at around the same time the S&P 500 had its ATH.

This price performance honestly surprised me, because I am of the opinion that BTC is the most compelling asset today for long-term returns. Much of my thesis is that it is a superior protection against monetary debasement and fiat financial system issues. Despite the recent price action, I still stand by this position, but I have been trying to poke holes in my own thesis as an exercise of intellectual honesty.

Flight To Safety

One of the most memorable moments in my Bitcoin investing journey was the collapse of Silicon Valley Bank back in March 2023. At the time, many banks were in crisis because they owned long-duration assets in the form of treasury bonds. You might recall that March 2023 was preceded by a string of aggressive rate hikes to quell the decades-high inflation in 2021 and 2022, which was caused by the aggressive fiscal and monetary stimulus done in 2020. The rate hikes were terrible for long-duration assets, so many banks had major duration mismatch issues, which turned into liquidity and solvency issues when people suddenly wanted to withdraw. This is an inherent risk of fractional reserve banking.

This forced the Federal Reserve to step in with the Bank Term Funding Program (BTFP) which allowed banks to redeem their heavily underwater long-duration positions at par. This was basically another bailout for the U.S. banking sector, and by the end of the year, banks were using the BTFP to earn some easy arbitrage profits.

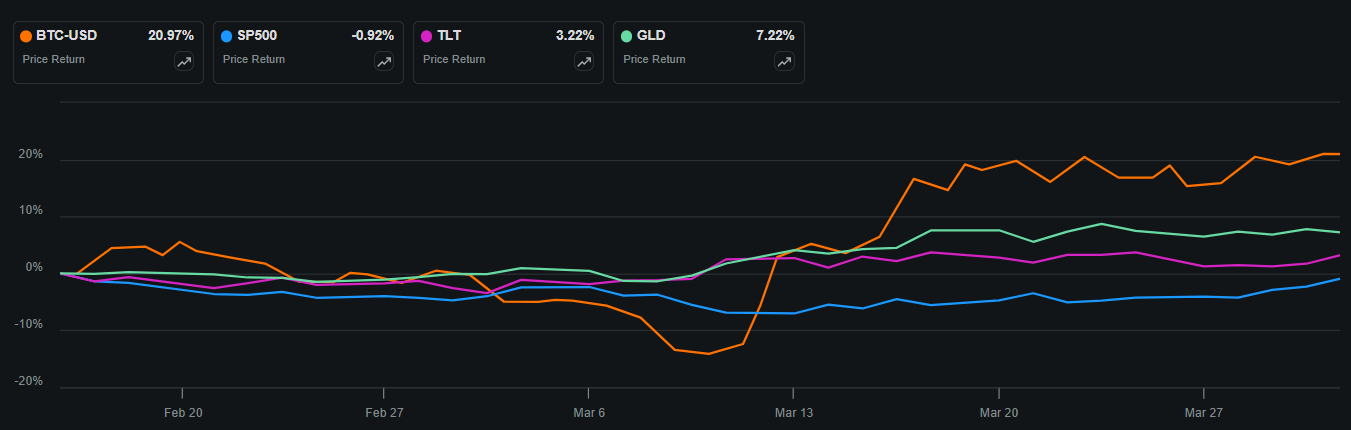

When the banking scare resulted in the infamous failure of Silicon Valley Bank on 10 March 2023, these were the market reactions of four very different asset classes.

BTC and others around SVB failure (Seeking Alpha)

In the next two days, BTC shot through $24000 and never looked back. It was up over 10% while the others were flat or down on the banking crisis news.

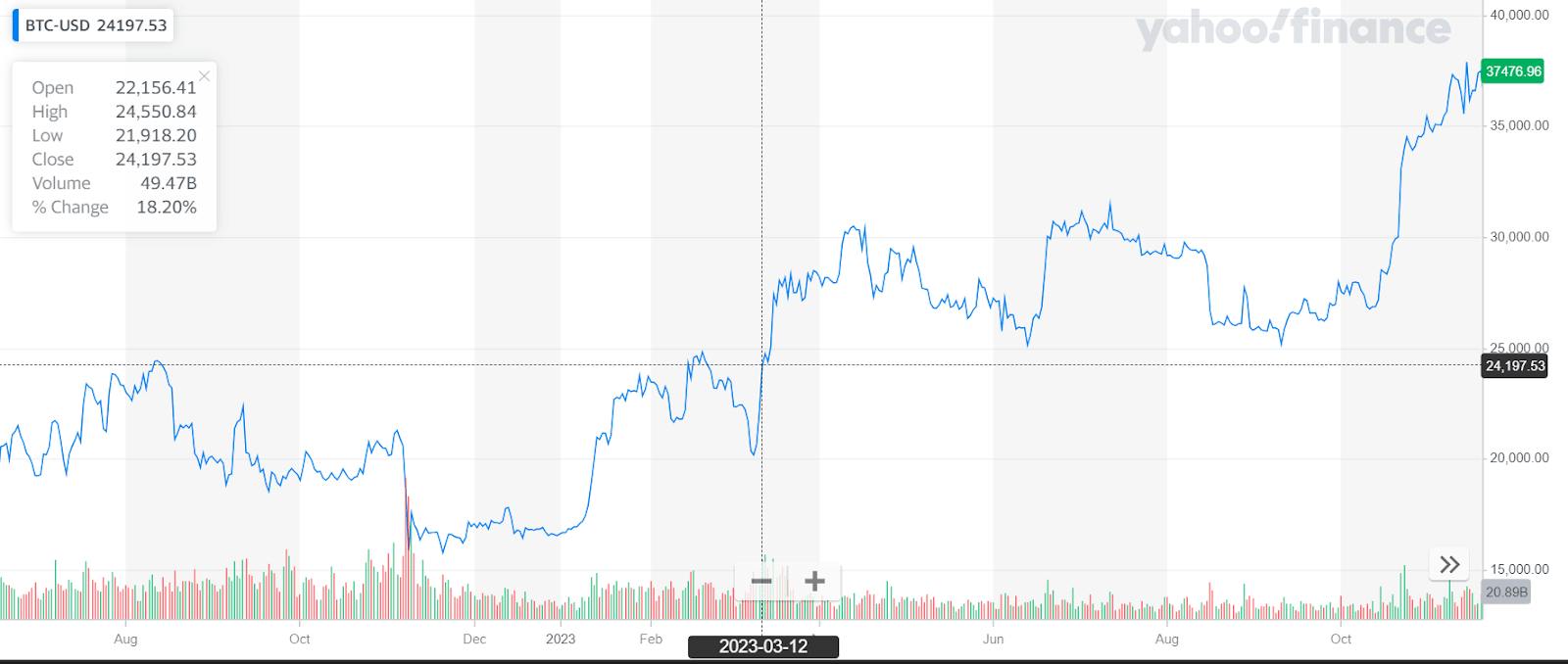

BTC around SVB failure (Yahoo Finance)

The SPX fell a little bit before it started higher. TLT and GLD seemed to go up slightly with BTC on the day of SVB’s collapse.

I took that episode as a sign of BTC’s status as a flight to safety asset. And this was quite unexpected given that crypto was just months coming out from the collapse of FTX. When things got very chaotic as it did with SVB, with some commentators even saying that this was a “Lehman moment,” BTC of all things was the flight to safety.

So this time around, when the financial system was again reeling from the results of central bank actions, now in the form of the Bank of Japan unexpectedly raising rates and unwinding a classic carry trade, I was surprised that BTC did not respond as a flight to safety at all. In fact, it drastically underperformed most assets and utterly failed the test.

I am still thinking through why this happened. There are a few theories which I’ve seen which are interesting.

Theory 1: Only Asset Around to Sell on Weekends

The major moves started happening on Friday, 2 August. The BoJ raised rates on 31 July, on Wednesday. Thursday and Friday both saw adverse price action in most markets. The Nasdaq 100 was hit a bit harder than the S&P 500. Friday was quite bad for U.S. markets, and Japanese equities weren’t doing too good either.

Now, the theory is that over the weekend, crypto was the only spot market which were trading, so traders dumped crypto to raise cash in anticipation for the coming margin calls on Monday as they realized that the yen carry trade was probably going to start unwinding.

This meant that BTC took much of the selling pressure to the chin, and this is reflected in a pretty large 19% drop from Saturday to Monday.

I think this theory makes sense on the surface but is more like a coping mechanism by the diehard Bitcoin supporters (and even though I am certainly a member of this group, I try to be intellectually honest). It is making the rounds on social media, and Bitcoin companies like Swan and River have communicated this theory as a possible explanation for the crash in their email newsletters.

Theory 2: Overleveraged and Cascading Liquidations

Crypto allows for massive leverage. Some perpetual futures products support up to 100x leverage. It is not uncommon to be trading BTC derivatives with over 20x leverage. These derivatives also trade 24/7/365. When there is a little bit of volatility, a lot of liquidations can happen at once, creating a cascading selling pressure.

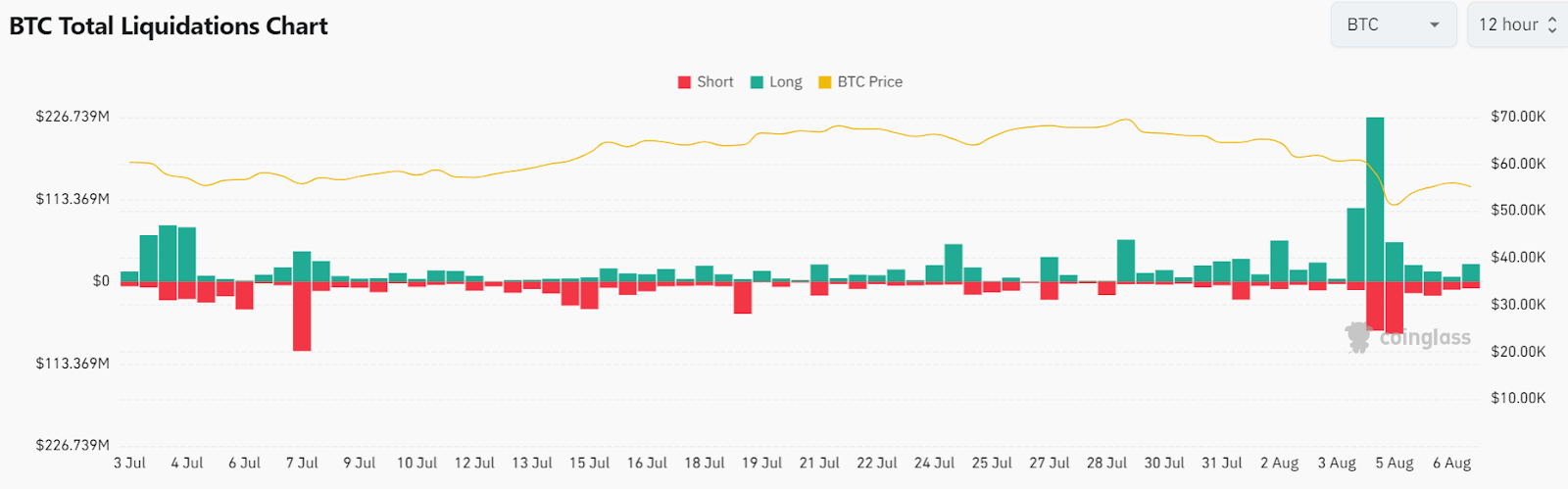

Here is a chart of BTC liquidations aggregated across various crypto exchanges. A lot of longs were liquidated on Sunday, 4 August. This is likely a reflexive factor that contributed to the 19% crash.

Liquidations (Coinglass)

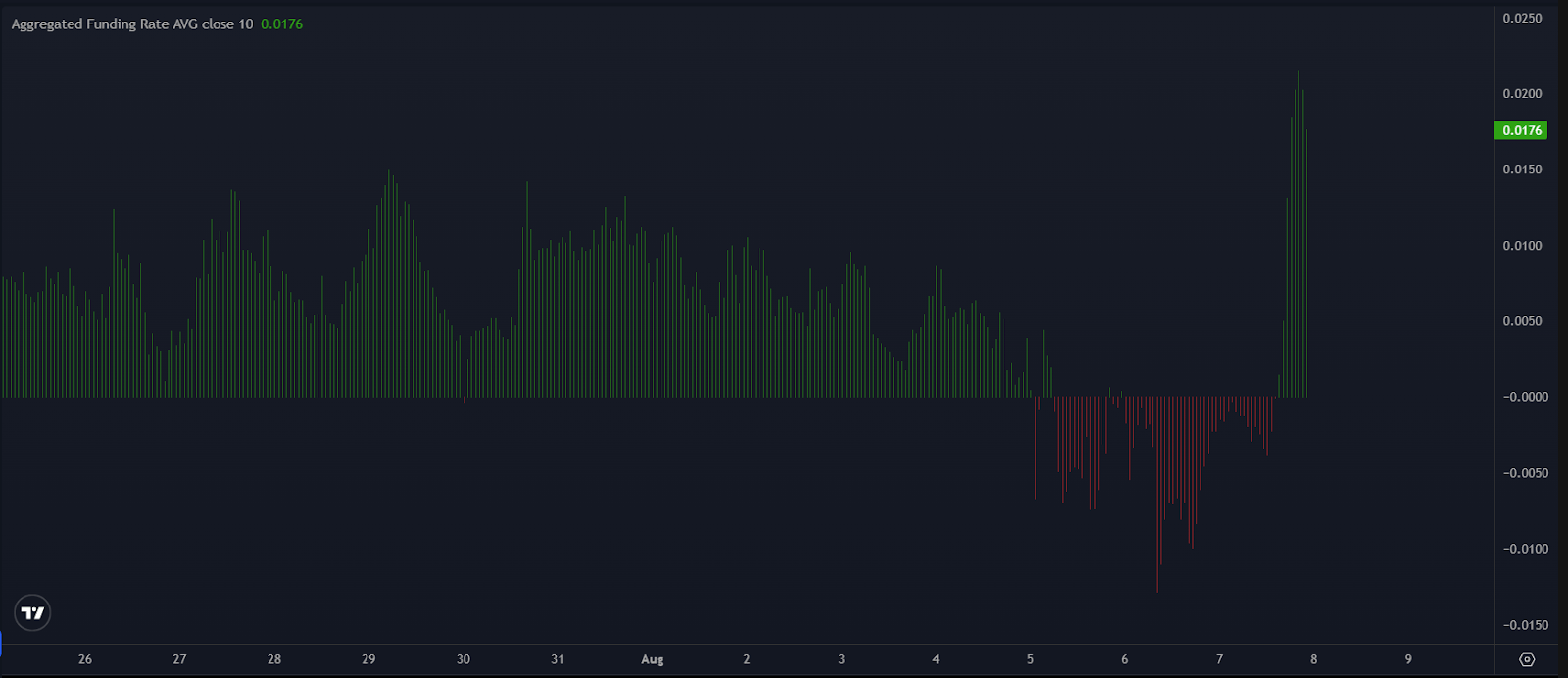

Here are the funding rates of perpetual futures, also aggregated from different crypto exchanges.

Funding rates (Coinalyze)

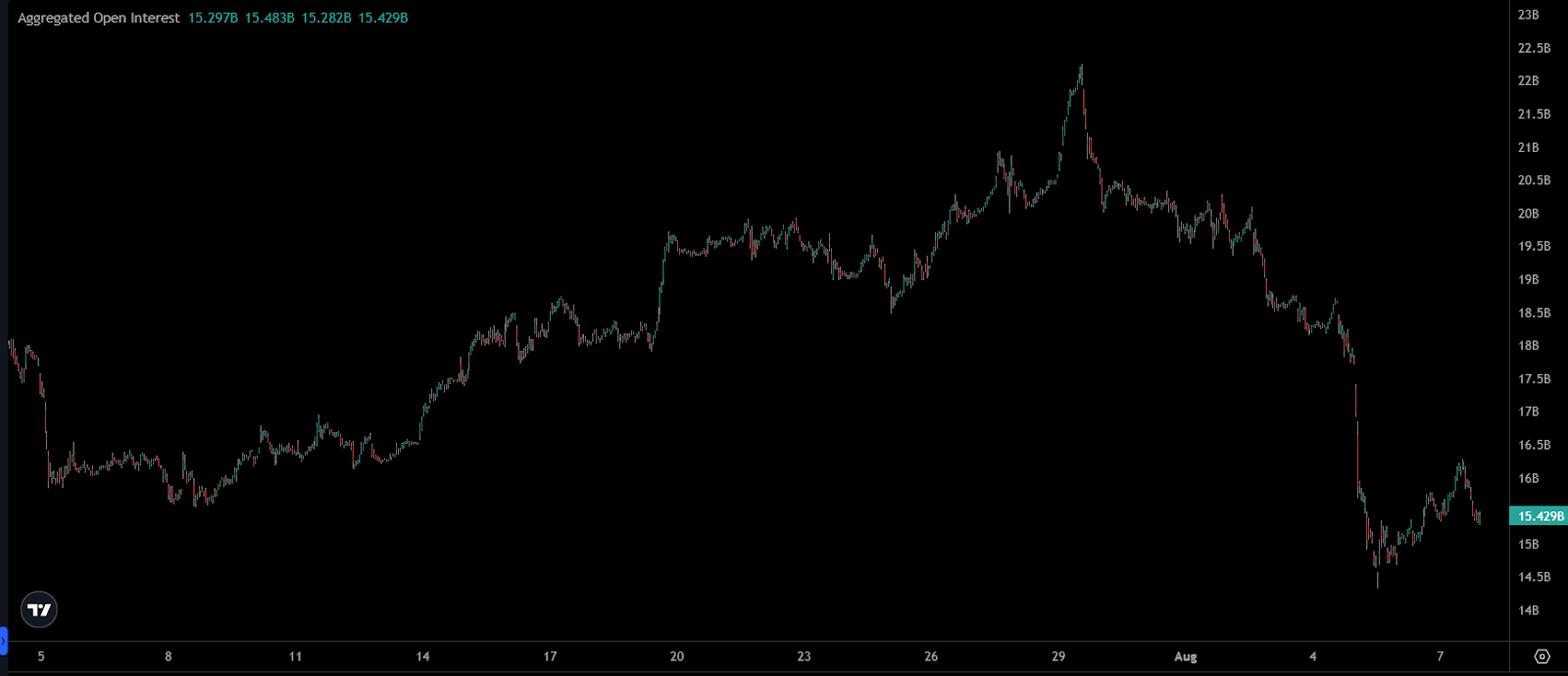

Positive funding rates are indicative of net bullish (long) positions on BTC. Funding rates are a cash flow that is exchanged between longs and shorts on a daily basis to force the price of the derivative to track the value of the underlying. When funding rates are positive, it means leveraged traders are paying extra to be long the underlying. A build-up of positive funding rates could indicate overt bullishness. And actually, I think we can conclude this is exactly what happened seeing that open interest had risen 50% from mid-July before peaking on 29 July, just 2 days before the BoJ’s rate hike.

Open interest on Bitcoin (Coinalyze)

There was clearly a lot of leverage in the system, and it had to be violently washed out via liquidations, and this is what caused the collapse in the price.

I like this explanation more. It is a classic function of crypto markets. In this case, BTC is simply another risk asset to trade, and the traders got washed out, and the price action laid it bare for all to see.

Theory 3: Most Investors See Bitcoin As High Beta QQQ Right Now

This is my personal explanation, which I’ve been aware of for a while. BTC’s reaction to SVB was certainly a contradiction of this theory, but let’s look at a long-term chart.

TQQQ and BTC (Seeking Alpha)

BTC really does track together with the ProShares UltraPro QQQ ETF (TQQQ), a 3x fund of the Nasdaq-100. There is no good reason to expect this perception to change anytime soon, so if this is what people perceive, then that sentiment will be what drives the market price of BTC.

The explanation really can be that simple, because it’s not that much of a stretch to say that people create markets, and the price is just as much a reflection of people’s collective perception of reality as it is a reflection of reality.

For this relationship to break, more people who are actively involved in trading BTC must come to understand it as something more than a high beta version of tech-heavy indices. Until that happens, BTC won’t be any more of a flight to safety than TQQQ.

Conclusion

BTC completely failed as a flight to safety asset this time. I believe Bitcoin bulls need to be honest about this, reflect, and add more nuance to their thesis.

I think BTC remains a Buy. I see extremely bullish developments. For instance, some corporations are beginning to adopt BTC treasury strategies, inspired by the indisputable outperformance of MicroStrategy. I wrote an article that explained the options available to a corporation exploring such a strategy. The article was a breakdown of what I thought was the most important moment in the recent Bitcoin Conference in Nashville.

I view corporate adoption as the most bullish medium term-factor in Bitcoin’s evolution. As more companies buy into BTC with their excess cash, they unlock optionality they would never have had access to before. And it isn’t just publicly traded companies that are doing this. Various private companies are exploring it too, no doubt in their search for an asset which can store their accumulated earnings for the long haul without leaking purchasing power. A large list of known Bitcoin treasuries can be found on this website here.

In the long term, I think this kind of corporate adoption will be consequential in decoupling BTC from TQQQ. I also think corporate adoption will be the leader that pushes for regulatory dovishness and overall government acceptance of BTC as an asset, which is at least politically self-destructive to oppose. These should help change BTC’s perception over time, and maybe next time it will pass the flight to safety test.

Really Is")