peterschreiber.media/iStock via Getty Images

One of the better pair trades to execute right now is going long Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL) and short Apple (NASDAQ:AAPL). Both companies fall into the FAANG group of giant tech stocks out of favor in the current market, but Apple remains far too beloved in comparison to Alphabet. Not to mention, one of the more long-term bullish thesis for Apple is actually better played via the more beaten down Alphabet. My investment thesis remains very Bullish on Alphabet, while shorting Apple provides a hedge for downside protection in this bear market.

Similar Innovation Paths

The main reason Apple maintains a premium valuation is the looming release of an AR/VR device and the expected ultimate launch of the Apple Car in a few years. Both of these market opportunities are massive, but Alphabet already has a lead in the AV market with the long-term investment in the Waymo division.

Only a couple of years ago, Waymo was estimated as worth $175 billion by Morgan Stanley. The division raised $2.25 billion at only a $30 billion valuation last year, as the reality of self-driving technology set into the difficult market reality.

The massive valuation dip for Waymo should highlight why investors shouldn’t place much value in a pending Apple Car release in future years. Waymo is already offering robotaxi rides in the metro Phoenix area, testing driverless rides in San Francisco and working with Uber Freight on self-driving trucks that offer a lot of near-term promise for autonomous highway driving. Even the latest California DMV report has Waymo leading the sector in testing miles at nearly half the 4.1 million miles driven by AVs on California’s public roads last year.

Apple Car is only a rumored product, with investors uncertain whether Apple plans to actually build a car with the help of an auto OEM or build an AV technology package that fits into existing cars. The likely outcome is a business similar to Waymo focused on the advanced technology for self-driving and hiring someone else to manufacture the EV.

Either way, investors should heed the current valuation of both the self-driving technology companies such as Waymo and the recently public Aurora Innovation (AUR). Aurora is only worth $2 billion after nearly a year of being public, and EV stocks are down substantially as well. The excitement of an Apple Car should fade, similar to how Waymo and Aurora Innovation no longer have valuations worthy of moving the needle for Alphabet.

The other area of excitement is the mixed reality devices Apple is working on releasing starting in the next few quarters. The latest rumor has the first device release announcement delayed until early 2023 pushing a full year of sales into FY24.

Influential Apple analyst Katy Huberty from Morgan Stanley has already squashed the potential for this division to move the needle in the next few years. The analyst forecast FY26 sales of 31 million units for revenues of $29 billion, based on an ASP of ~$750.

Remember, Apple is heading toward $400 billion in annual revenues, so a niche device expected to sell for less than the iPhone isn’t likely to move the needle. The AR/VR devices will contribute to the growth of Apple similarly to the Watch, but neither product alone moves the needle like the iPhone and growing Services bucket.

Besides, a top analyst just suggested Apple failed to produce a 5G modem to replace QUALCOMM (QCOM) modem chips in the iPhone. For the time being, Apple will remain 100% reliant on Qualcomm modems.

Apple struggling to build a functional 5G modem should make investors hesitant to just believe the tech giant can produce an autonomous electric vehicle in the next few years. One shouldn’t doubt the tech giant can become successful with a 5G modem or an electric AV, but the path is likely far more difficult than thought by the market. Besides, Alphabet remains the better bet with their Waymo division leading AV development going back for years now.

On top of Waymo, Google Cloud and YouTube are great growth drivers for Alphabet. Not to mention, Google Glass is a new entrant by Alphabet into the smart glass segment, following an unsuccessful attempt back a decade ago. According to Android Authority, the glasses appear similar to the spectacles acquired from startup Focal back in 2020.

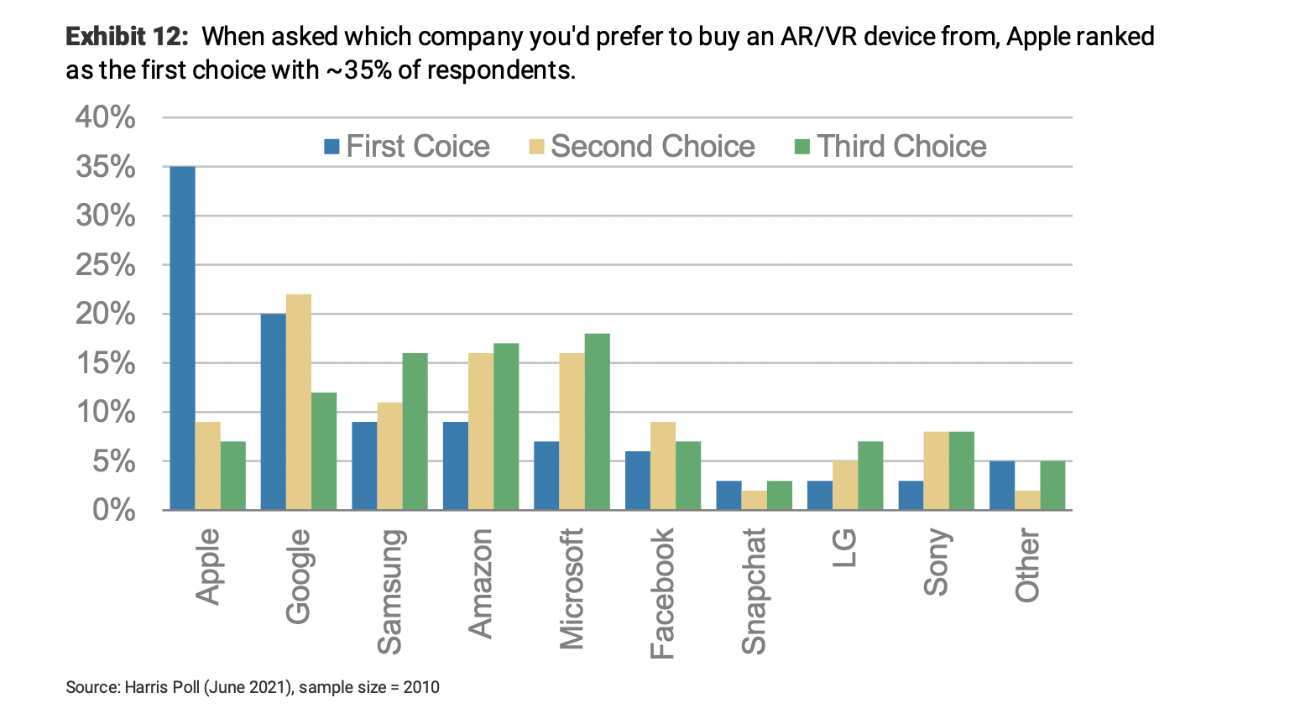

If anything, Alphabet again has a stronger history in another sector ascribed as the growth engine of Apple. Even Morgan Stanley acknowledged that Google ranked right behind Apple as the preferred choice for an AR/VR device. Interestingly, Meta Platforms (META), formally Facebook, ranked sixth despite having the popular Oculus headset already in production.

Source: MS/Harris Poll

Growth Rates Don’t Match

Investing shouldn’t be done with emotions, but most investors get emotional about stocks. One looking at the growth rates of Alphabet and Apple should come to an easy conclusion on the company with the better growth opportunity through 2025.

- FY22: Alphabet -0.4% vs Apple 9.5%

- FY23: Alphabet 18.9% vs Apple 6.4%

- FY24: Alphabet 13.7% vs Apple 5.5%

- FY25: Alphabet 15.9% vs. Apple 7.9%

Alphabet is forecast to double the growth rates of Apple over the next 3+ years. When breaking down the actual growth rates for the rest of 2022 though the next couple of years, Alphabet has the far superior growth rates.

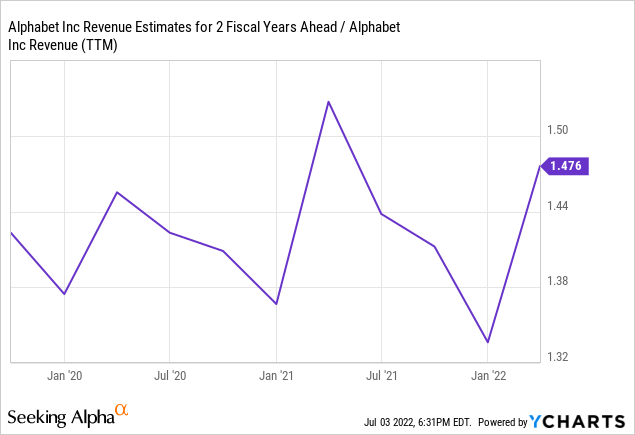

The following charts highlight the revenue growth discrepancy between the two stocks when stacking on the revenue after the March quarter. Alphabet is forecast for 2024 revenues to grow nearly 50% from TTM revenues of $270 billion.

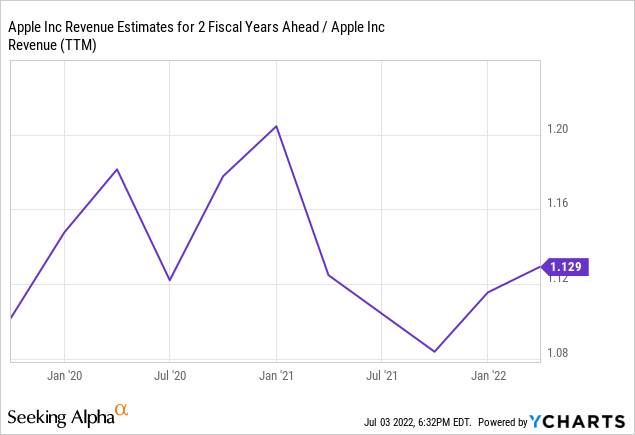

Apple is forecast to have minimal growth going forward. The June quarter isn’t expected to generate much growth, and the consensus estimates of analysts predict revenues only grow 13% over the next couple of years until the end of FY24.

Of course, analyst estimates aren’t always accurate, but this comparison is between two tech giants that equally smash analyst targets on a regular basis. Investors shouldn’t have the mindset that Apple is going to materially beat targets while downgrading the growth potential of Alphabet.

Alphabet has gotten into smartphones and other hardware, but the internet search giant is a lot more reliant with the digital advertising market. Apple remains the company highly reliant on the cyclical iPhone product, with revenues accounting for about 50% of sales. Throw in the Mac and iPad, and Apple relied on these hardware products for 70% of FY21 sales.

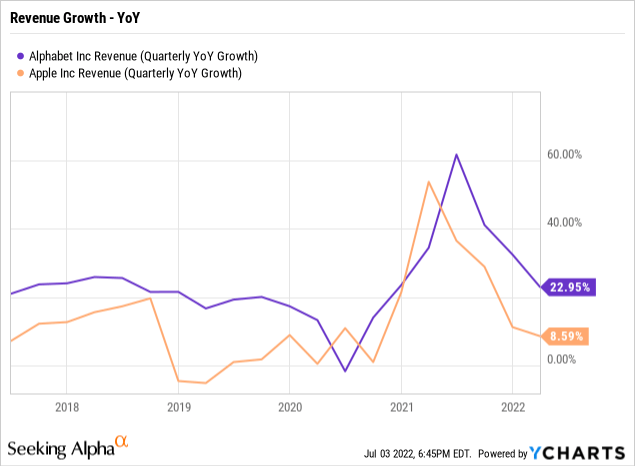

The amazing part is that the historical data confirms this thesis. Over the last 5 years, Alphabet consistently had the better growth rate. Only in a few quarters out of a period with 20 quarters did Apple exceed the growth rate of Alphabet.

The prime reason for the faster growth by Apple in the March 2021 quarter was the comparison to the tough March 2020 quarter when Covid-19 shutdowns started followed by booming demand for iPhones and Macs due to work from home requirements. The additional hardware needs quickly faded back to increasing demand for digital advertising and services offered by Alphabet. Again, Apple only exceeds the growth rates of Alphabet in periods where the iPhone cycle booms, such as the above period where WFH demand was strong, and the company launched the important 5G iPhone.

Investors shouldn’t expect the revenue growth trend of the next 5 years to differ any from the last 5 years, when Alphabet consistently had the faster growth rates.

Valuations Aren’t Comparable

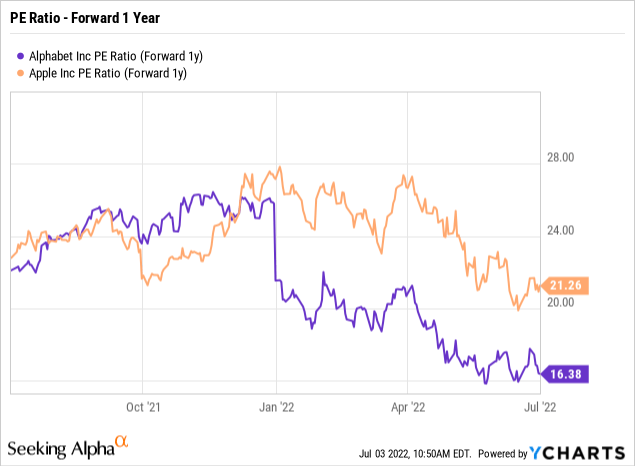

The above data highlights how Alphabet has faster growth targets than Apple and a similar, if not better, product innovation roadmap. All the data adds up to where Alphabet should trade at a higher multiple, yet Apples trades at 21x forward EPS targets and Alphabet is down at 16x.

Even more remarkable is that these are GAAP numbers. Alphabet has substantial stock-based compensation charges that greatly reduce their EPS. Apple doesn’t spend as much on SBC, limiting the impact to earnings.

In the last quarter, Alphabet spent $4.5 billion on SBC while Apple spent $7.9 billion for all of FY21. As discussed in my previous research, Alphabet only trades at 14x 2022 EPS estimates after stripping out SBC, and factoring in the large cash balance worth nearly 10% of the market cap.

Apple has 16 billion shares outstanding, so the after-tax impact of SBC to the tech giant is far less than $0.50. If one added $0.50 to the FY23 EPS targets of $6.53, Apple would still trade at ~20x the non-GAAP numbers.

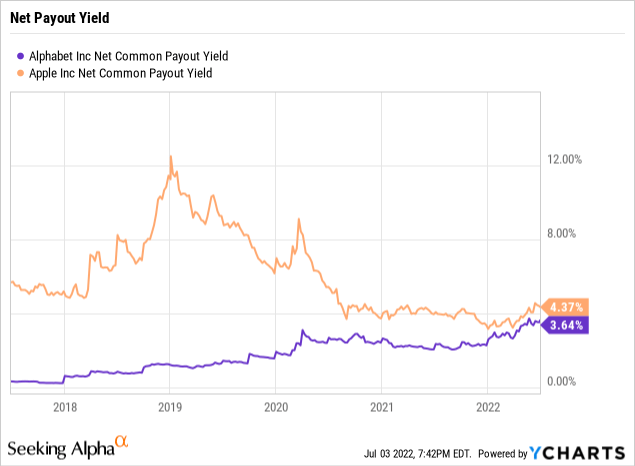

A lot of investors focus on the large stock buybacks of Apple as a huge benefit to owning the stock. The surprise here for most investors is that Alphabet now spends a nearly equal amount on share buybacks as a percentage of the market cap as Apple.

The net payout yield combines the dividend yield and the net stock buyback yield. Apple has a net payout yield of 4.4% with a dividend yield of 0.7%. Alphabet has a 3.6% yield with no dividend, making the net stock buyback yield nearly identical.

A big key here is that Alphabet has a similar yield and the company isn’t trying to reach a cash neutral position. Apple is aggressively repurchasing shares and paying dividends, reducing the net cash position. At the end of the March quarter, the smaller Alphabet had a net cash position of $119 billion, while Apple is down at only $73 billion. Apple ended the March quarter last year with net cash of $83 billion, yet the net payout yield was only 4.4% despite the tech giant reducing the cash balance.

Different Risks

The risk profiles of these two stocks just aren’t similar. Both stocks could fall during another major step down of the market, but my opinion is that Apple is far more fragile, with the stock still trading at an elevated valuation.

Alphabet has 10% of the market cap in net cash, while Apple only has ~3% of the market cap in cash. Alphabet can cushion the blow with more relative share buybacks.

The likely scenario over the next few years is that under a bullish scenario, Alphabet could possibly double while Apple flatlines. All of the financial metrics support Alphabet trading at a higher multiple down the road, while Apple won’t hardly grow earnings and can’t justify a higher multiple.

Under a bearish scenario where a massive recession hits, my thesis has already discussed Apple having a logical value closer to $100. The stock could see more downside than the already prescribed 28% dip.

On the flip side, Alphabet already trades at a non-GAAP EPS multiple of their EV of only 14x. The stock might fall on further market weakness, but the tech giant has the earnings stream to support the current price.

Of course, the biggest risk to both stocks is an innovative company coming along and disrupting the businesses of either Alphabet or Apple. Neither company could end up a winner in AVs or AV/VR device, leaving future growth prospects limited.

Takeaway

The key investor takeaway is that Alphabet makes a great pairs trade with an Apple short. Both stocks will participate with any general move in the stock market, whether up or down, but Alphabet has the best potential upside going forward.

The scenario is pretty much set up where either Alphabet wins big in a bull market or Apple loses substantial value in a bigger bear market. Either way, the pair trade would win.