Gerald Corsi /iStock via Getty Images

Introduction

As stock investors, it is important to make a distinction between a good business and the stock of a good business. This article is intended to be a warning to investors in Apple (AAPL) and Alphabet (GOOGL) stock, that even though these are fantastic businesses, the stocks will still succumb to the next bear market, and right now, it looks like the odds for the next bear market occurring within the next 24 months are very high.

Additionally, I’ll zoom out in this article and offer some wider portfolio strategy thoughts about how I’ve been dealing with what I call “Boom/Bust” danger at the portfolio level. This is important because the market caps of the stocks in question are huge, so they affect the major indices in a significant way and I suspect they could be overweighted in many investors’ portfolios. They are also extremely high-quality businesses that are likely to perform well as businesses over the long term. When we put all of these things together, there are enough cross-currents that a simple all-or-nothing approach probably isn’t the best approach right now. Due to all these factors, this article will possess some nuance. That nuance will make for a less excitable article, but hopefully a more useful one for intelligent readers.

I’m going to begin by examining what really happened to Meta (FB) stock this year. By understanding that, investors can hopefully gain some insight into what is likely to happen to Apple and Alphabet within the next 24 months.

Understanding the Boom/Bust Dynamic with Meta

I bought Facebook stock a little over a year ago on 1/28/21, and I shared that idea on Seeking Alpha in my article a week later titled “Most Big Tech Is Expensive, But Facebook Is Worth Buying“. Unless you have been living under rock, you know that investment isn’t doing so well. Right now, it’s down about -23% from my purchase date and -46% from its highs a few months ago. In this article, I’m going to make the case that a significant decline is likely for Apple and Alphabet stocks as well, for similar reasons that Meta stock fell. The timing and the depth of the falls may vary, but the dynamic is the same.

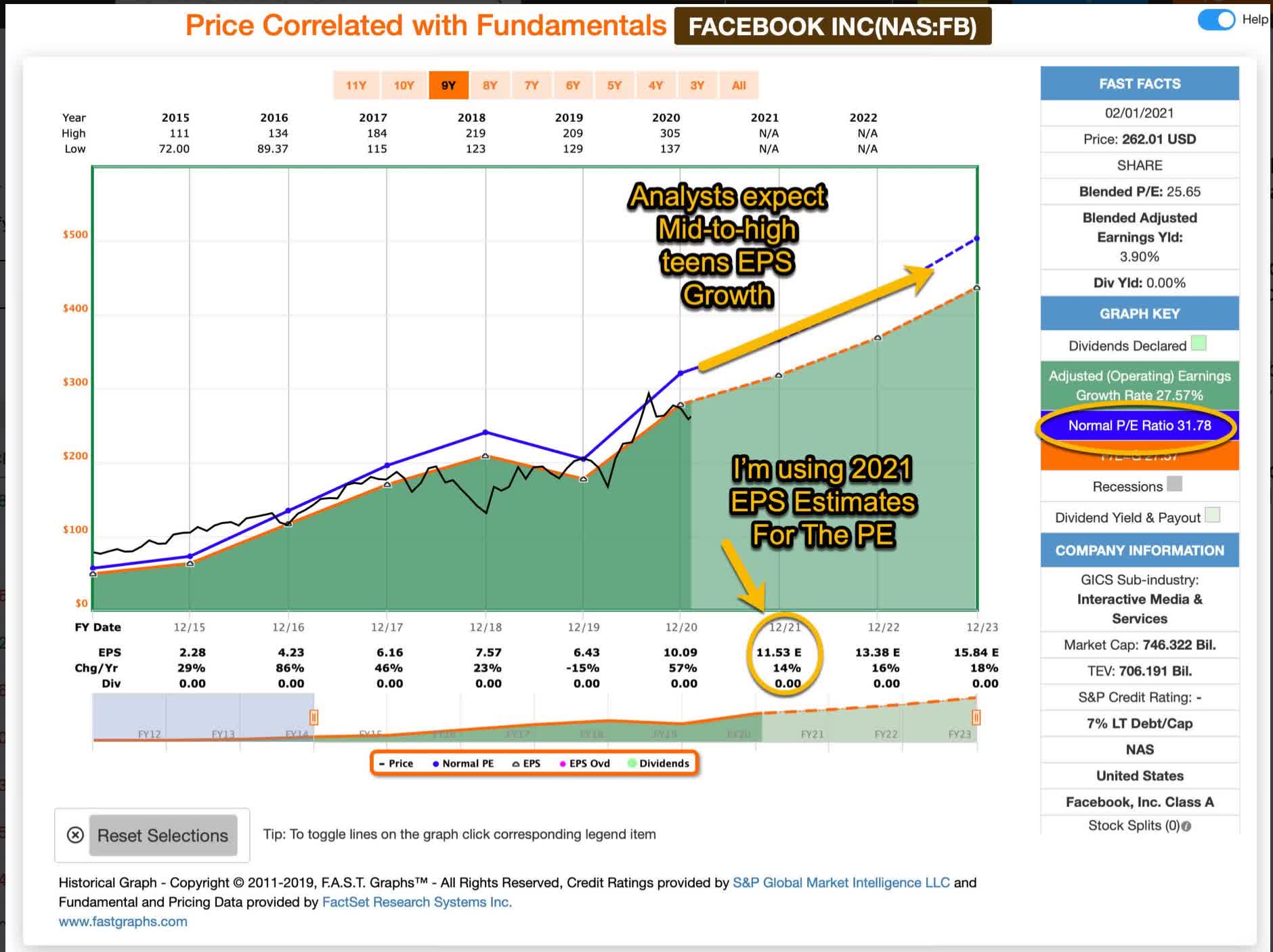

Below is a copy of the Fast Graph that I shared in my original Facebook article in February of 2021.

Meta Expectation from February 2021 (Fast Graphs (With annotations by Cory Cramer))

What I would like readers to focus on here are analysts’ expectations for Meta’s earnings per share in 2021, 2022, and 2023. As you can see, one year ago the expectations were $11.53, $13.38, and $15.84 per share, respectively for three years of forward earnings.

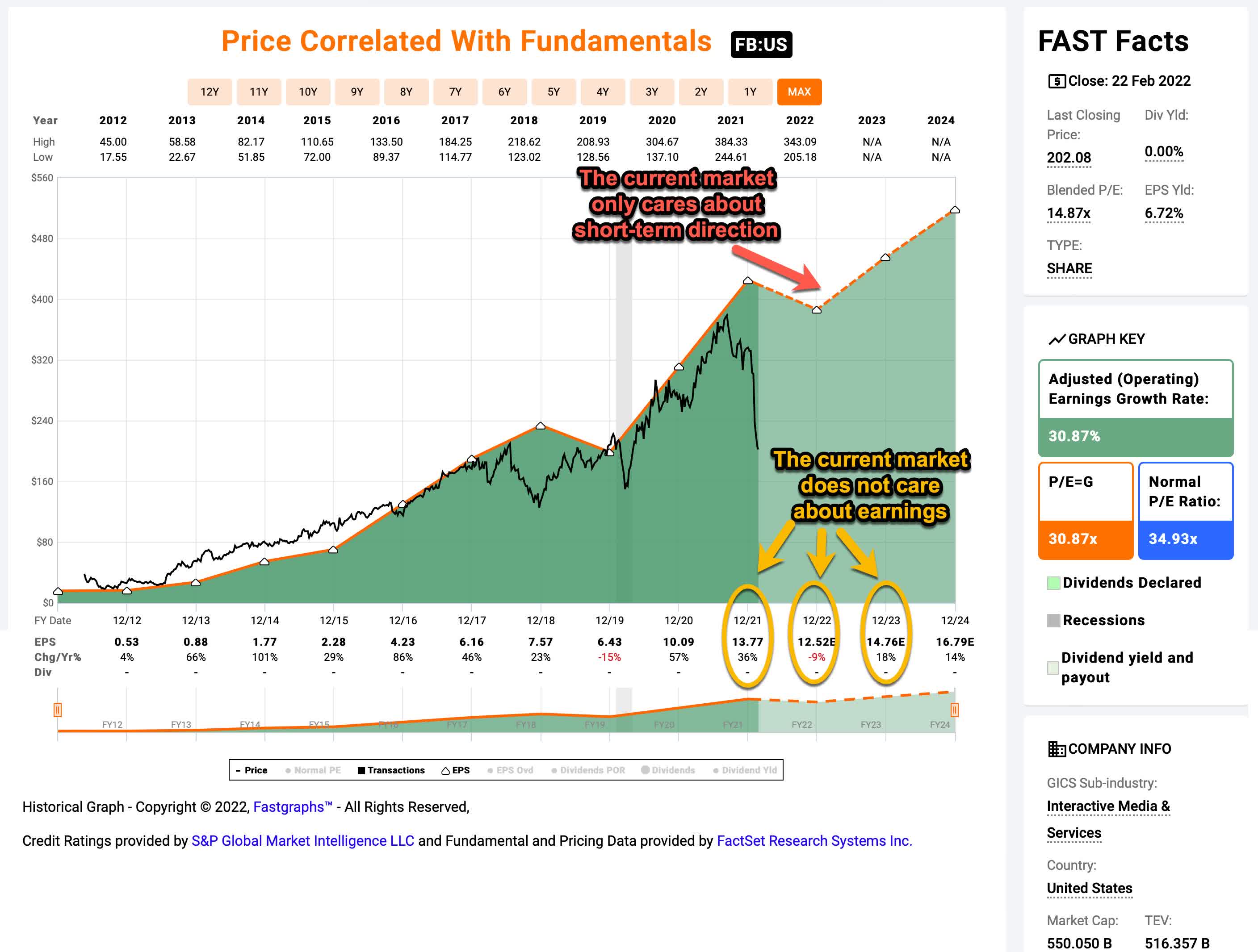

Now let’s look at 2021’s actual EPS and current expectations for 2022 and 2023.

Meta Current Expectations (Fast Graphs (With annotations by Cory Cramer))

My investment in Meta stock was an earnings-based investment. For earnings-based investments, what I care about most is how much earnings per share the company collects over time, and how much I pay for those earnings. Compared to stocks like Apple and Alphabet, I paid considerably less for Meta’s future earnings when I bought it. So, I don’t think that is the main factor that explains the difference in performance between these stocks. That leaves us with whether or not Meta’s actual earnings failed to meet the market’s expectations at the time I purchased the stock. So let’s compare earnings expectations then and now to find out.

| Year | Analysts’ 2021 Expectations | Actual, or Current Analyst Expectations |

| 2021 | $11.53 | $13.77 |

| 2022 | $13.38 | $12.52 |

| 2023 | $15.84 | $14.76 |

| Total | $40.75 | $41.05 |

What we see here is that Meta’s 2021 actual EPS exceeded expectations significantly, and while 2022 and 2023 expectations are now lower than they were in 2021, if we combine all three years together, Meta has actually exceeded 3-year EPS expectations. Yet, the stock price is now almost -50% off its highs. (Also analysts expect 2024 to resume Meta’s previous upward trend with expectations at $16.79 per share, so, it’s not as though analysts expect that Meta is in permanent decline or stagnation.)

My point of sharing the fact that Meta stock, while not being particularly overvalued relative to peers (or even on an absolute basis) last year, and while exceeding cumulative earnings expectations so far, can still fall almost -50% from its highs is that this market cares about the short-term direction of earnings rather than the earnings themselves. Almost any stock that fits Meta’s profile and has a significant slow-down in earnings growth, or a reversal of earnings growth is likely to experience a similar decline. And it doesn’t have to be a tech company.

Earlier this year, on January 23rd, 2022, I warned investors about this pattern in my article “Why I Took Profits In LKQ“. Last year, LKQ grew EPS by 55%, this year earnings growth is now expected to be flat, LKQ fell about -15% after they reported earnings last week. When I first wrote about and bought LKQ in November of 2020, analysts expected 2022 EPS to be $3.05 per share. Now they expect 2022 EPS to be $3.96 per share, which is far higher than previously expected, but the stock dropped a lot on the news and will probably continue to do so. The important takeaway here is that this is about the pattern and not the particular industry or individual business. While there will certainly be differences between how far Meta stock falls and how far Apple and Alphabet stocks will fall, I expect the larger pattern to be similar.

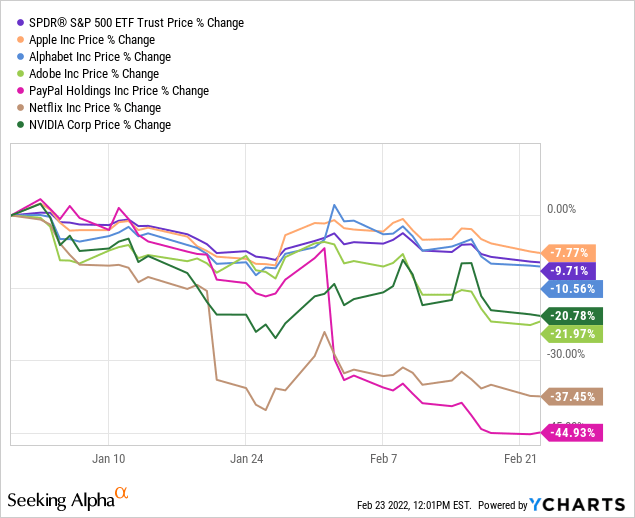

Below is a sampling of how far some of these stocks have fallen since the beginning of the year compared to the S&P 500 index.

While all of these stocks are down, along with the index, Apple and Alphabet are down far less, and they are much more in line with the overall returns of the index than tech stocks in general. The rest of the stocks in this sample are effectively in a bear market.

I think it’s possible that holders of Apple and Alphabet stock may have breathed a sigh of relief after January’s earnings season, so this article is simply an attempt to warn them why they shouldn’t breathe easy so soon.

Understanding boom/bust cycle for Apple & Alphabet

I showed the earnings pattern of the current boom/bust cycle with Meta, but I also want to take a moment to write about the causes of the boom. What has gone largely missing in the current state of discussions about the Federal Reserve raising interest rates, Russia/Ukraine, supply chain problems, and inflation, is that US federal government stimulus was the key driver of the “boom”. The US government paid out approximately $3.5 trillion dollars in stimulus and stopped payments on over a trillion dollars in student loan debt over the past two years. A great deal of that money was given directly to the American people, and a significant portion of those people have spent the money, or will spend the money this year.

This is a vastly different situation than we had after the 2008/9 recession when there was very little stimulus given directly to the American people. There was no “boom” after 2009 because there effectively was no stimulus. All we got was low interest rates and QE from the Fed, and bailouts to save the organizations that contributed the most to the crisis to begin with. In that environment, most of the levers of the economy were in the Fed’s hands. This time is different. While the recent hawkish pivot of the Fed (provided they actually follow through on it) will effectively remove the so-called “Fed Put” from the market, all that does is mean the Fed probably won’t step in the same way they did in Q4 of 2018 to prevent a stock market decline because back then inflation was low, and it’s not low anymore. But the removal of the Fed Put is not the primary cause of the upcoming “bust” any more than it was the primary cause of the “boom”. Rates were low in 2009 and we had a weak recovery and rates were relatively high in the late 1990s and we had one of the biggest stock market booms in history. The Fed certainly did it’s part in March of 2020 to prevent a depression, but the heavy-lifting behind the boom in 2021 was caused by the massive amount of direct fiscal stimulus from the Federal government to the American people.

It became clear to me at the end of December 2021 when Senator Joe Manchin rejected continuing stimulus, and a general inflation phobia set in amongst the US public and policymakers, that the odds of an abrupt shift from boom to bust had become very high. Here is how I described the situation last month in my article “Six Financial Stocks I Recently Sold, And Two I Will Hold for the Long Term“

There were two types of direct stimulus to the American people in 2021, one type was quick “one-time” payments, of which, there were two: one in January and one in March. This was the equivalent of giving someone, say $4,000, twice, and then not giving them any more money. But there were two additional forms of ongoing fiscal stimulus that directly affected many Americans. The enhanced child tax credit, and the pause on student loan repayments. These were different in that they were ongoing forms of stimulus, that for the average family with two kids who have student loans, amounted to roughly $400 per month each. One of them, the child tax credit created money that flowed into a household in the form of increased income of about $400 per month, and the other prevented an approximate $400 outflow per month to pay back student loans. Combined, these two forms of stimulus are far more important, and underrated by the market than they should be. This is an amount roughly equal to 20% of the affected families’ take-home pay. One can only imagine the percentage of disposable income those two forms of stimulus accounted for in the second half of 2021. This stimulus was, without a doubt, a very, very high percentage of disposable income for many people in 2021.

Near the end of December, we got the news from Senator Joe Manchin that he would not support the bill that would extend the enhanced tax credit. Once that happened at the same time the Fed speakers dramatically turned into inflation hawks, I put my trailing stops on. Biden, soon after Manchin’s decision, extended the student loan pause until May, so that potential removal of stimulus was delayed, but we still don’t know how long the delay will last, and in May, it could be gone.

As far as I’m concerned, the potential for this fiscal stimulus boom/bust cycle is far, far, greater than any Fed interest rate decision. The Fed would have to hike short-term rates to double digits to have the same effect on working families and the economy as the removal of this stimulus will have. All that extra demand for goods from the stimulus that has been contributing to inflation will disappear in a few quarters if the tax credit isn’t extended and borrowers have to start paying back their students loans. Inflation will quickly be replaced by disinflation, a bear market, and probably a recession. This is the real danger to the price of these stocks (and many others).

So, that’s my big picture view of the boom and the likely bust. Add onto that the unique COVID consumption patterns that favored Apple and Alphabet in 2020 and 2021, and it simply adds yet another boom/bust dynamic on top of the stimulus dynamic, likely amplifying it even more.

Now let’s examine Apple’s earnings for a clearer picture of the stimulus money boost these businesses received.

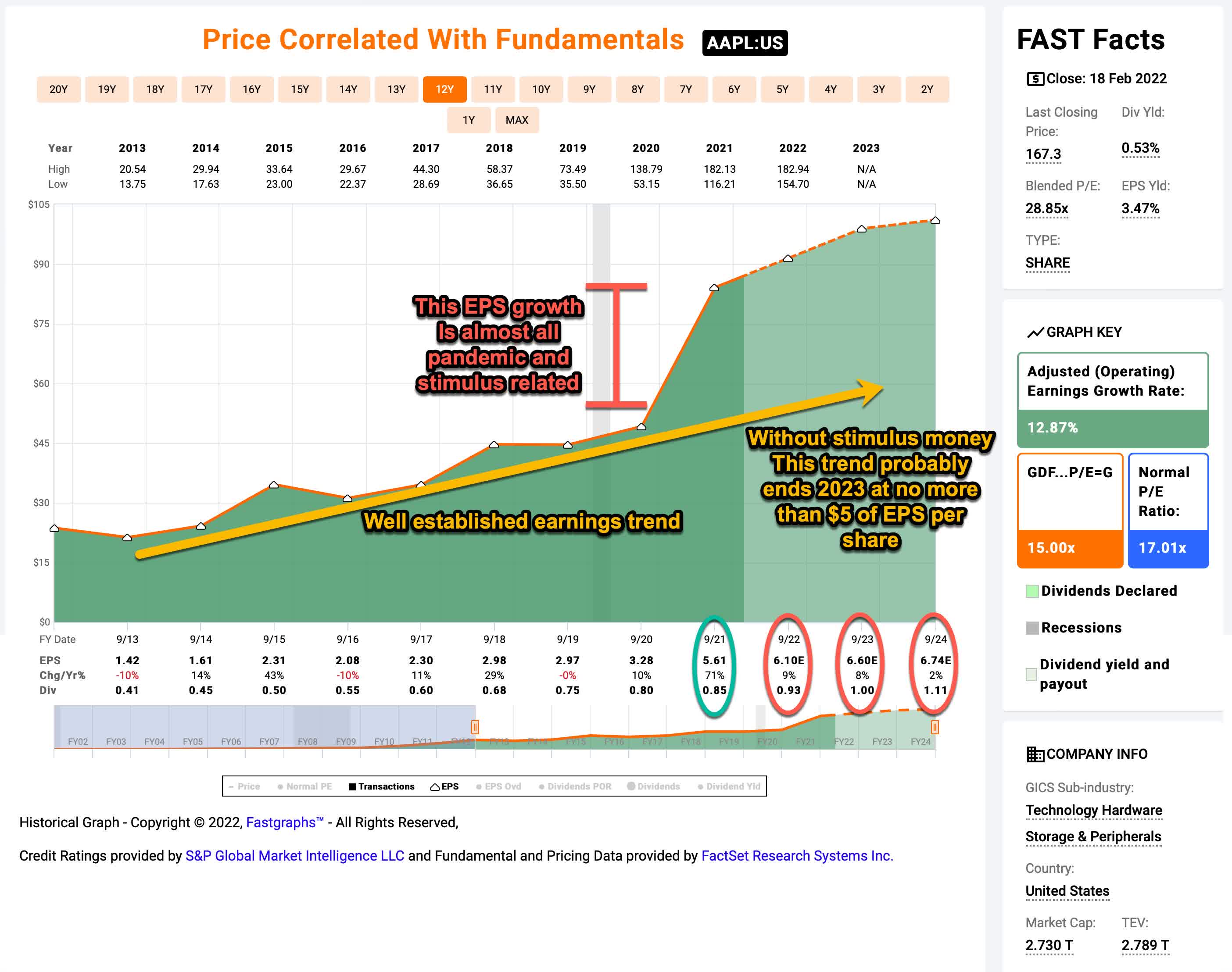

Apple EPS trend (FAST Graphs (With annotations by Cory Cramer))

In the FAST Graph above I have removed all the metrics except for the EPS trend and started the chart around the time the iPhone reached maturity in 2013. What I want to show readers here is just how much federal stimulus money affected Apple’s EPS growth in 2021. Because Apple’s fiscal year ends in September, their 2021 fiscal year captured almost all of the stimulus payment effects in a single year. In 2020, they grew EPS 10%, which is what I projected when I took profits in Apple in January of 2020, so their earnings growth was right on target with the expected trend until 2021. It should also be noted that because Apple buys back massive amounts of stock, these EPS growth numbers are inflated. If a person backs out the effects of share repurchases, then Apple was only growing earnings leading up to the pandemic in the low single digits.

So, we went from a range of low single-digit to up to 10% earnings growth for Apple from 2013-2020 to +71% earnings growth in the single year of 2021. The question I think Apple investors need to truly ask themselves is if, by the end of 2023 when most of the stimulus money has been spent, whether Apple’s earnings are likely to grow, shrink, or stay about the same? Right now, analysts think EPS is likely to grow in the single digits over this time period. The market has priced Apple’s stock as though it will grow much faster than that (with a 28-30 P/E ratio, I would estimate that requires a 15% EPS growth rate to support that valuation over the medium-term). I think the odds are very high that EPS growth will actually be negative by the end of 2023.

My thesis is that Apple’s EPS is more likely to be closer to $5 per share in 2023 than the $6.60 analysts expect. If we were to extrapolate their EPS growth trend pre-COVID through 2023 it would be around $4.50 per share, but I’m sure they added more customers to their very sticky ecosystem in 2020 and 2021, and there will be permanent benefits from that. So, an expectation of them earning between $5 and $5.50 per share in 2023 seems reasonable to me. If I am even remotely close in my estimates, then Apple’s stock price has a very high probability of a deep sell-off during this time period, and a bear market decline of -20% has an extremely high probability. Just as we have seen with the likes of the other tech companies this year, I think it’s totally reasonable to expect that Apple stock could ultimately fall -50% off its highs unless we see more government stimulus in the next year or two because the stock price has become so far detached from reasonable medium-term expectations.

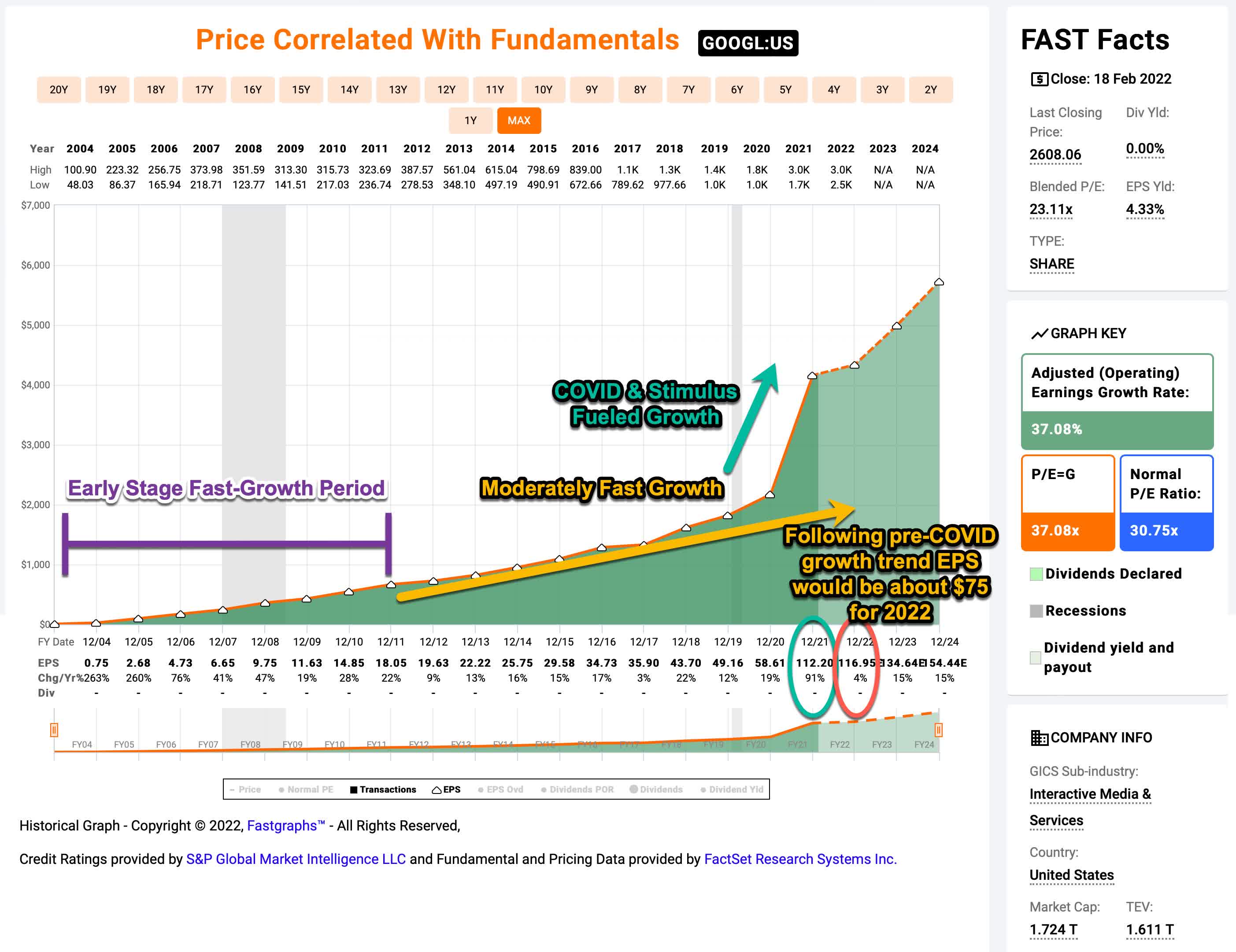

Alphabet has a similar profile

Fast Graphs (With annotations by Cory Cramer)

We see a very similar pattern with Alphabet as we saw with Apple, except Alphabet’s EPS actually grew an incredible 91% in 2021. One look at the FAST Graph of historical EPS shows what an anomaly this year is. It’s the very definition of a “boom”, and the odds are very high that by the end of 2023 there will be a “bust”. I estimate that without COVID stimulus Alphabet’s previous EPS trend would have had them earning about $75 per share in 2022, and right now analysts are expecting about $116 per share. As with Apple, these additional stimulus earnings will likely help adjust the previous trend upward a bit, and that money will continue to circulate in the economy for a while, so, perhaps EPS won’t fall all the way down to the previous trend line, but I think for analysts to expect $134 per share of earnings in 2023 is wildly optimistic.

An additional consideration for investors is that during the last recession of any length in 2008, Google managed to grow EPS at over 40% per year because they were then still a relatively small and fast-growing business. Now they are a $1.7 trillion company. Most of Alphabet’s revenue comes from advertising, and advertising has a long history as a cyclical industry. Investors should expect that EPS growth will be deeply negative during a “normal” recession. Now add on top of that a recession that is preceded by an advertising boom fueled by what is likely to be one-time stimulus money, and it sets up GOOGL stock for a potentially very steep decline. The stock price will almost certainly fall far enough to reach bear market territory, and I probably wouldn’t consider buying it until it was -40% or -50% off its highs.

Portfolio Considerations and Strategy

I recently went through all of the stocks in the portfolio in my private service, The Cyclical Investor’s Club, and I sold about 75% of the stocks I owned with this sort of “Boom/Bust” profile in January as a way to de-risk my overall portfolio. There were a few that I decided to keep like Meta (FB), BlackRock (BLK), Tractor Supply (TSCO), AutoZone (AZO), and Signature Bank (SBNY). So, I understand why an investor might decide to simply hold Apple and Alphabet stock through a potential downturn since they are high-quality businesses. But combined, these stocks that I shared above represent less than a 10% weighting in my portfolio. All the rest of the stocks I owned with “Boom/Bust” profiles like Apple and Alphabet have, I have sold.

The intention of this article is simply to warn investors who hold these stocks that now is a time to consider reducing exposure and to point out that even though 2021 earnings were good, and the prices of these stocks have held up well relative to many other tech stocks this year, they are highly likely to succumb to the same forces that drove these other stocks down already. And Apple and Alphabet, while they may seem invincible right now, have very high and extremely unrealistic expectations built into their prices over the next two years. I don’t know what the exact timing will be before they crack, but the stimulus that drove the growth in 2021 is unlikely to continue in 2022 and will be almost fully wound down by the end of 2023. And we live in an age where mega-cap stocks can fall -25% literally overnight.

I am a long-only investor and so far in 2022 I have been fully invested and holding no cash. Yet, with the S&P 500 down almost -10% for the year as of this writing, my portfolio is only down about -3% and has actually been pretty boring to watch at the portfolio level. This begs the question of why don’t I hold some cash if I’m as bearish as I seem to be? In the future, I might very well hold cash, but there are three key reasons I’m not doing so now. The first is that I could be wrong (though I think the odds are increasingly in my favor). The second is that I am well diversified. I own many stocks I think will be defensive, or countercyclical, at least in 2022, I have about 20% international exposure, and close to 10% metals exposure, and some real estate exposure as well. All of the money from the stocks I’ve sold this year I have put into a 60/40 proxy iShares Core Growth Allocation ETF (AOR), which is now over a 15% weighting. Even my holding in Meta was only a 1% initial weighting compared to the 3.8% weighting it had in the S&P 500 index at the start of the year, so even where I am exposed to these boom/bust stocks, I’m exposed less than most others.

And the third reason I’ve not shifted anything to cash, yet, is that policymakers can still change their minds. We saw the Fed do this in a dramatic way in Q4 of 2018, and in 2008, House Republicans first rejected the option of any bailouts, but then they went back to their home districts and got an earful from their constituents, and when they returned to Washington they passed a bailout. When we are in a boom the public might care a lot about inflation, but I’m not so sure when the residents of West Virginia are jobless en route to a recession they won’t change their minds about more stimulus. Joe Biden initially didn’t want to forgive more than $10,000 in student loans, but it’s not unthinkable that if Congress is uncooperative with regard to other measures, he might not forgive $50,000 as some of his other Democratic colleagues have suggested. To be clear, I’m not particularly optimistic about any of these changes happening any time soon. But I also think that given the amount of new money floating around in the economy that a recession probably isn’t yet right at the doorstep. For these reasons, a well-diversified, yet mostly defensive portfolio is where I’m at right now.

I just wanted to share this boom/bust dynamic because I think far too much attention is being focused on the Federal Reserve and interest rate hikes than is being paid on this much bigger “Boom/Bust” danger. While low interest rates might have contributed to the stock price “Boom” in terms of the high valuations some investors were willing to pay for high-quality tech stocks, rates have almost nothing to do with the “Bust” dynamic that will be caused by the sudden removal of stimulus money. Rising rates, assuming tech investors ever really cared about rate comparisons to begin with, might be relatively slow and gradual over the next year or two, but the removal of stimulus, which has a much more direct effect on business earnings, will not be nearly as gradual. The stock market has already shown us this year with stocks like Meta and others that its reaction to earnings disappoints will be anything but gradual. Be careful out there.

Ukraine Invasion Post-Script

As I was doing my final review and edit of this article this morning, I see Russia has fully invaded Ukraine. It’s unclear what the full market reaction will be to this or what sort of retaliatory sanctions will be put in place. I’m going to take a couple of days to think about whether this moves up the timeline of a recession enough for me to raise cash rather than just being defensively diversified. Higher commodity prices likely move up the recession time-line, but they also increase the chances that the government might stimulate the economy more. So it’s hard to tell how this affects the overall market. What I will say is that the “Boom/Bust” danger to Apple and Alphabet in particular will remain high enough that if an investor would prefer not to experience a deep drawdown, they should lighten their exposure.