Marco Bello

“We have never seen this much innovation evolving at the same time”

Cathie Wood

Cathie Wood is certainly right about that. However, assuming all new tech would work as intended, grow profitably and indefinitely, and have little competition turned out to be another matter.

A big part of our future will be determined by innovations, so, let’s have some fun and try to predict the future.

Purpose of the Article

This article will start with the amazing amount of factors that came together to create this historic surge in innovation and stock market wealth, in the U.S. It will discuss why it happened in the U.S. It will then look at how much these factors will continue into the future. Finally, we will look at Apple specifically as a leader and personification of recent innovation.

A big part of our future will be determined by innovations. So, let’s have some fun and try to predict the future. If you have different predictions than mine, please add them to the comment section.

Background

The last 20 years have been a golden era of innovation that propelled the stock market up. In the 20 years ended January 1, 2022, the S&P 500 increased 400% despite two recessions.

On December 2, 2019, I published an article titled The Golden Age Of American Mega Growth Stocks. In the past the largest companies had underperformed due to the law of large numbers limiting growth. In the years leading up to that article, the largest American tech stocks had outperformed the market to the point they became the biggest factor driving the whole market forward.

While many have pointed toward the Fed’s policy of easy money, the real source of the strong stock market was massive innovation by American companies of all sizes. This was further enabled by offshoring of labor which kept costs and inflation down. That is because stock prices are comprised of two factors; earnings and a PE ratio (or multiple of earnings to account for future growth). The Fed through interest rates primarily impacts the latter. Most of the stock market gains the last 20 years were due to the former, increased earnings. That came from the proliferation of new markets driven by innovation. The Fed has a lot of impact in the intermediate term, but not in the long term. That has more to do with innovation, management and competitiveness.

Interestingly, the vast majority of this innovation and growth came from American companies. The U.S. has about 4.3% of the world’s population but close to 50% of the market capitalization of all stocks in the world. It is not beating the world by 10%, its more like by 1000%. Let’s look first at why this is.

Why so Much Innovation in the U.S.?

On January 19, 2019 I published an article titled America’s Edge: America Is Still Great Here’s How

In it I listed 12 reasons for our superior performance. These are summarized below.

1. Innovation – Despite having 4.3% of the world’s population, over 50% of all inventions the past 20 years have been in the U.S. A lot of that is coming from our mega cap growth stocks.

2. Better Universities – There is a reason millions of the best foreign students go to U.S. universities. Many stay here and add to our economy.

3. Immigration – We still lead the world in immigration though recent policies are causing this to falter. Immigrants tend to work hard to take advantage of the opportunities in the U.S. Some become CEOs such as Elon Musk and Lisa Su.

4. Capital – We have by far the largest capital markets. In fact, the value of our stock market is almost as large as the rest of the world combined. Our bond market, private equity and banking system are also the largest.

5. Startups– Startups are more prevalent here than anywhere else. What helps new businesses and large ones entering new markets is the scale of the U.S. market, free enterprise protections, and access to talented employees and capital.

6. Infrastructure– Don’t believe the criticisms here. Our roads, airports, ports, transportation and utilities are world class and reliable. Power outages are rare.

7. Military – The U.S. has by far the strongest, best funded military. This has led to numerous innovations to upgrade weapons and infrastructure. It also means more business for corporations.

8. Stability – Despite the current political divide, our government is more stable than most. We only have two significant political parties, which is unusual. There is a strong rule of law, freedom of the press, and a system of checks and balances.

9. Culture – U.S. culture has had the most influence on the rest of the world. However, there is also a corporate culture that has developed that involves non-discrimination, prohibitions of harassment, teamwork, learning and well defined opportunities.

10. Natural Resources – The U.S. is blessed with natural resources and has most of what it needs available domestically. Our farmland is also among the best in the world.

11. Accounting – While there will always be cheating, investors trust the numbers in the U.S. much more than in emerging economies.

12. Large corporations – Believe it or not, this is my number one reason for America’s edge. I spent much of my article America’s Edge: Yes America Is Still Great Here’s How explaining it. But it starts with American innovation, so let’s go there.

Innovation by Large U.S. Corporations

Why is innovation so strong in the U.S. versus elsewhere? First of all, we have a strong patent and patent protection system. Companies that innovate get paid and have recourse to sue if their IP is taken without compensation. This is a big reason the Chinese have not come close to matching us despite all their efforts. Secondly, we are importing highly skilled and highly motivated immigrants. They have to be highly motivated if willing to leave their homeland, friends and families to come here. Thirdly, our brand of capitalism allows an unlimited payoff. There is no cap to how much a person or company can be paid from executing on a good idea. Fourthly, the payoff is bigger here than elsewhere due to the size of our economy, the largest in the world by far. Fifth, we are willing to pay what it takes to get qualified people to carry out the research and for management. We just pay more. The highest paying fields are IT and medical, the same fields where most of the innovation is. Finally, we are more willing to take risks. This is due to the potential payoff just mentioned but it’s also part of our culture as it is praised. Private equity is willing to lose a lot of money funding good ideas in order to invest in one that makes it big.

Innovation the Past 20 Years

Below is a list of new markets created just in the past 20 years. While the technology in many cases predated that, these markets started generating large revenues and became world changing in the last 20 years.

-GPS

-Streaming

-The Cloud

-Online search and ads

-Smart phone

-Apps

-Solar farms

-Wind farms

-Electric vehicles

-Social media

-Cryptos

-Online payments

-Online gaming

-Artificial intelligence

-Fracking (saved oil industry in U.S. and pushed back peak oil)

-Private space

-HD TV

-Smart TV

-Genetic mapping

-CRISPR (gene editing)

-Video conferencing (trend to remote working)

-Drones Ride hailing

-4G and 5G

Of these, smart phones and social media have had the most impact and are ubiquitous in our lives. Additionally, there have been huge strides and growth in software. Software has been around much longer than 20 years but as the cliché goes, it has eaten the world. Many of the fastest growing companies the past decade were software providers.

A major problem is that many of the major new markets that have driven innovation and revenue growth are maturing. These include GPS, smart phones, social media, online advertising, streaming, apps, online payments, fracking, HD and smart TV, video conferencing, ride hailing and telecommunications (now 5G).

Future Innovation Sectors

There is certainly more coming which are not big revenue generators yet today. Those already in the works include;

-Self-driving cars and trucks

-Small modular reactors (small safer nuclear plants)

-Virtual reality (already here but not generating much revenues yet)

-Drone deliveries

These are addition to growth in the innovation categories previously listed. There will always things we didn’t think of that turn out to be big. My best guess is a major growth area in the future will be around extended life. Specifically stem cell grown organs and anti-aging treatments.

Innovation the Next 20 Years

There remains a lot of growth ahead. In addition to the coming innovation sectors, I mentioned just above, there remains a lot of growth left in those that have grown tremendously the last 20 years. These include;

-Solar farms

-Wind farms

-Electric vehicles

-The cloud

-Online gaming

-Artificial intelligence

-Private space

-Genetic mapping

-CRISPR (gene editing)

-Drones

-The cloud

Of those above, I see the biggest growth in AI, the cloud, and genetics such as CRISPR. I still expect the largest innovation from U.S., though the rapid development of other parts of the world should narrow the lead some. Specifically, there has been a lot of technological development in Southeast Asia, and not just China.

Innovation Needs

To keep innovation going at or above historical levels the following is needed.

-Capital

-Capitalism – profit incentives

-Risk takers

-Rule of law

-Educated workforce

Things that can slow it down include;

-Excessive regulation

-Excessive taxes

-A major geopolitical event

Some of the negatives are already happening. The US and European governments pushing back against monopolies held by the largest tech companies. In fact, I believe the Golden Age of mega caps is probably over. They will face a continuing tide of regulation and government pushback.

For that reason, a lot of the new innovation may need to come from smaller more nimble companies.

The Next 3-5 Years

I expect a slowdown or lull in innovation for the following reasons;

1. The biggest trends the last 20 years were in software, smart phones and social media. Those markets are maturing. Newer ones are not yet large enough to carry the baton forward at the same speed.

2. The IPO market is temporarily mostly shut down. This cuts off a major source of capital to the new generation of innovators.

3. We usually enter an age of sobriety following major innovation periods. Bubbles pop, excess capacity is reduced, and investors are less willing to take risks. I believe we will see this for several years.

4. We are moving away from globalization which is almost always a negative toward economic development as it reduces potential markets, suppliers and access to capital and is inflationary.

5. We are likely entering into a recession. I have written three articles on SA about why I expect a recession. Recessions slow R&D spending and capital raising.

Innovation in the U.S. will not go away and may not even slow. There is a critical mass of well-educated and trained scientists, engineers, mathematicians, IT professionals and managers to keep it going. But the days of accelerating innovation are probably over for a while.

Apple

Apple, Inc. (NASDAQ:AAPL) essentially invented some of the largest markets in the world today, including the smart phone, the PC, tablets, the app store, and the current method of online music sales. It used to be large corporations couldn’t move quickly with new innovations but Apple has historically proven that wrong. However, Apple has introduced few new products or services in recent years. It’s CEO, Tim Cook, who I greatly admire, has focused more on improving the existing products and efficiencies and moving more into services.

Revenue growth has slowed due to a maturing of most of its markets, especially the iPhone. The iPhone represented 49% of total revenues in the most recent quarter and its revenue growth was only 2.5% YoY. The latest iPhone 14 had few significant new features. Perhaps after 14 generations Apple is running out of new ideas. Apple lately seems to be maintaining a slow growth in smart phones. Apple gets a huge profit margin on its phones versus competitors in part because it has created a sticky ecosystem for them and because it has more features.

Revenue growth was 33% in 2021 after being only 3% in the two years ended 2020. The year 2021 appears to be anomaly due to Covid, and the huge stimulus package that followed. Revenues totaled $304.2 billion in the nine months ended June 25, 2022, up 8% from one year earlier. However, revenues slowed to up only 2% in the most recent quarter. EPS growth has been better and is currently running up 5-10%. This is primarily due to stock buybacks and improved margins.

Apple has done better in recent years expanding existing markets than introducing new products. Tim Cook is a great manager and operator, but not the innovator Steve Jobs was. To be fair, no one is. Apple clearly will need new markets if it is to resume solid revenue and earnings growth. It has a history of little significant M&A activity indicating growth will need to come organically. Their best prospect for a new market appears to be autonomous car software. However, based on obstacles run into by Tesla (TSLA), Waymo and others, getting that last 1% of development needed will be tough. It does not appear to be something that will help in the next few years. Instead, Apple has been growing EPS more with stock buybacks and improved margins.

Recent headlines indicate things are slowing and even declining.

1. Bank of America Analyst Wamsi Mohan recently lowered his rating on Apple to neutral from buy and cut his price target to $160 from $185, while also lowering fiscal 2023 estimates. “We see risk to this outperformance over the next year, as we expect material negative [estimates] revisions driven by weaker consumer demand (Services already in slowdown and we expect products to follow),” Mohan wrote in a note to clients.

2. Bloomberg reported on September 28, 2022, Apple is pulling back on iPhone production

3. On October 3, 2022 Apple announced the App Store saw net revenue decline 5% year-over-year in September. This had been a significant growth area in the past.

4. On October 6, 2022, UBS noted that wait times for the new iPhone 14 product line have eased, indicating “flattish” year-over-year growth for the September quarter.

Apple Valuation

Apple currently trades at a PE ratio of 23.5 versus the average S&P 500 PE ratio of 15. Does Apple deserve an above market PE ratio despite below market revenue growth? Let’s look at the reasons it does first then why it doesn’t.

Apple is the bluest of blue chips right now which makes it a defensive holding in a recession or economic slowdown. That makes it similar to other slow growers with big moats like P&G (PG) and Coke (KO) which have similar above market PE ratios. Apple also has a very large moat, a strong balance sheet and one of the best CEOs. It has the ability to juice growth through acquisitions though it has done little of size in the past. Apple has a large enough R&D budget that can still create products with very large total addressable markets, though none appear imminent.

There are also a number of reasons it shouldn’t have this much of a premium over the market. Its growth is at or below the market average at this point. Apple is facing the law of large numbers. The bigger you are the harder it is to grow. There are a lot less $25 billion new potential markets than $1 billion new markets. Apple is also probably not recession-proof based on its high-end products. Consumers trade down in a recession. It has not gone through a real recession with most of its current products. Apple gets huge margins on its largest product, the iPhone. Those margins may not be sustainable with innovations to the iPhone diminishing.

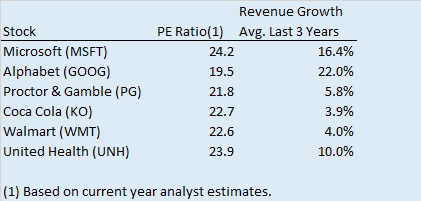

I compared Apple to other extremely strong but slower growing companies and two mature mega cap blue chip tech companies. The non-tech peers are all blue chips with huge moats, and extremely strong balance sheets but slower growing like Apple is now. The two tech peers are also extremely strong with huge moats, but faster growing than Apple.

Yahoo Finance and Value Line

Apple currently has a PE ratio of 23.5 to current year estimated earnings which is slightly above the non-tech peer group and similar to its tech peers, despite much lower growth. Revenue growth for Apple YoY was 8% in the last 3 quarters and 3% in the most recent quarter. That makes it more similar to the non-tech blue chips. Based on this comparison Apple should have a moderately lower PE ratio. It should also be noted, Apple is probably more cyclical in a recession than all but Alphabet.

Normally, I would rate Apple a hold based on the factors listed above. That is what I expected to do when I started this article. But the peer comparison, recent headlines along with a looming recession and the likely impact on Apple moves me to a sell recommendation. The stock closed at $146.40 on October 5, 2022. My 1 year price target assumes a PE ratio of 22 based on the comparables above, and is $134.

Takeaway

Apple is symbolic of a slowdown in innovation among the mega cap tech companies but not innovation overall. Innovation at Apple has slowed to the point where, along with other reasons, it no longer deserves a well above market PE ratio so I recommend a sell.

I believe American innovation will continue, though with a bit of a lull (due to reasons previously given), as long as we remain a capitalist nation that doesn’t penalize innovation.

I have identified a number of new and existing markets where major innovations are probably coming. Please feel free to discuss others you see in the comment section below.

Packs a Punch at $399")