Nikada/iStock Unreleased via Getty Images

Apple (AAPL) is the victim of its own success, having developed the most successful product ever (by a considerable margin) and extended that success into a range of highly successful peripherals, they now face the difficult task of creating tens of billions of dollars of profit to support the stock price. To perform in line with the market over the next decade, Apple likely has to find at least another 150 billion USD in profit. The automobile market is one option being considered by Apple’s management, and in many ways the merging of electric vehicle and autonomous driving technology has created an attractive opportunity. Even if an Apple car were to be successful though, it is not clear that the potential profits are sufficient to be meaningful for Apple shareholders.

Strategic Logic

Developing an autonomous vehicle is not necessarily a good fit for Apple’s competencies. While they have deep expertise in the development of hardware and software, they are not particularly well known for their machine learning capabilities. Developing a self-driving car is largely an operational problem requiring a brute force solution, not areas that Apple has traditionally excelled in. This may not be important though as Apple likely views autonomous vehicle technology as an enabler of a new vehicle experience, in a similar manner to how lithium batteries and RISC chips enabled a new smartphone experience. It is not particularly important who supplies these technologies, but rather what Apple can do with them.

Autonomous technology will abstract the vehicle and turn it into a space where users are confined for a period of time, creating an opportunity to turn the inside of a vehicle into an entertainment / productivity space, areas that Apple excels at. The Apple car is rumored to have no steering wheel or pedals and a U-shaped seating plan as a potential design feature, creating a limousine-like experience. This layout points towards the creation of an inward focused social space, rather than a typical cars outward focused seating layout. Apple will likely choose to concentrate on aesthetics and features that impact the user experience (hardware, software, interior, sensors, ride quality) while outsourcing the rest of the vehicle, and this could well involve the autonomous technology as well. Tesla (TSLA) has stated that it is willing to license autonomous driving technology to other companies and has even had preliminary discussions with some OEMs. It is likely other companies may choose to license their technology as well, particularly if the robotaxi market becomes crowded.

Apple have forayed into developing their own autonomous vehicles over the past few years, but the amount of progress they have made is unclear. They have been testing self-driving Lexus RX450h SUVs on public roads since 2017. These efforts have ramped up over time and it is believed Apple now has more than 60 test vehicles on the road. They also acquired the self-driving start-up, Drive.ai in June 2019.

Disengagement data in California indicates that while Apple is beginning to drive a reasonable number of miles, it isn’t close to the capabilities of leaders like Cruise and Waymo. While this type of data may be somewhat indicative of the capabilities of each company’s vehicles, it is not clear how comparable they are. A company that operates their vehicles primarily on open highways with limited amounts of traffic would have far fewer engagements than a company operating in a busy city, regardless of which company truly had better technology. Apple’s relatively poor performance could be because they are driving more challenging routes, their drivers are abundantly cautious, or it could be because its self-driving software is less advanced.

Leading autonomous vehicle companies have a disengagement approximately every 40,00 miles. In comparison the average driver crashes every 400,000 km. Again, cautioned should be used when comparing these types of numbers but it gives an idea of extent of the problem remaining, particularly if autonomous vehicles are targeting significantly improved safety.

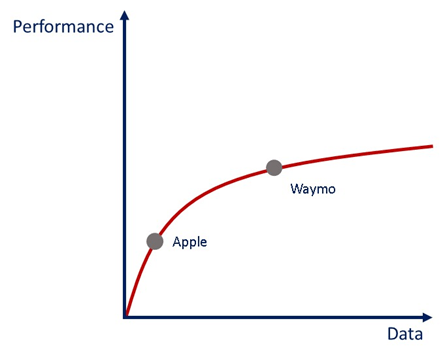

Apple is driving more miles in California than most companies, but far less than leaders like Waymo and Cruise. This gap is actually larger when taking into account the fact that Waymo drives the majority of its miles outside of California. This does not mean that Apple cannot still catch up though. There are diminishing returns to data and autonomous driving is far from a solved problem.

Figure 1: Machine Learning Model Performance Improvement with Increasing Volume of Data (source: Created by author)

While Apple is not renowned for its AI capabilities in the same way as Google (GOOG) or Facebook (FB), their products have become increasingly reliant and advanced machine learning for applications like:

- Facial recognition

- Health tracking

- Siri

- Translation

- Handwriting recognition

- Augmented reality

Apple also has experience with machine learning hardware, with most of their devices now including dedicated hardware for AI driven functionality. The more that autonomous vehicles require tight integration between software and hardware, the more successful Apple is likely to be. Most of Apple’s hardware efforts have been focused on low-power chips rather than the highly-parallelized processing units used in machine learning, but their capabilities are expanding and their Bionic chips have neural engines offering rapidly improving performance.

Apple’s OS has long been considered one of the best and translating this to a mobile phone is one of the reasons the iPhone was so successful. To do this, Apple needed to develop hardware expertise as their performance requirements were beyond what was available on the market at the time. Apple has since taken that combination of tightly integrated hardware and software to tablets and watches with great success. Interestingly, Apple’s hardware expertise is now also improving their competitive position in laptops. Apple likely wants to extend their hardware and operating system across as many user experiences as possible. This would provide customers with compatibility and the same experience across devices, with the car being just one more device. To succeed Apple still needs to be able to offer a better user experience than existing devices and there may be a reluctance to have one company so integrated in a users’ life, although Apple is trying to minimize this concern with its privacy focus.

Apple excels at providing an excellent user experience and autonomous vehicles would allow users to focus on the experience inside the car, rather than driving the car. Similar to Apple’s approach to the mobile market they are likely to try and tightly integrate the stages of the value chain that matter (batteries, hardware, software, interior, styling) while outsourcing those that don’t (drivetrain, chassis).

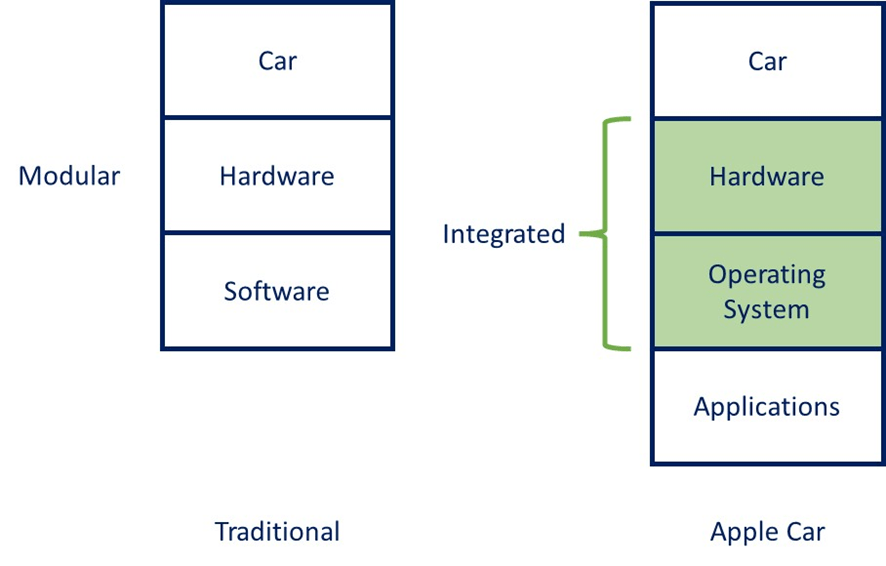

Figure 2: PC and iPhone Tech Stacks (source: Created by author)

A self-driving car that acts as a mobile office / entertainment space would elevate the importance of software and potentially create another platform for application developers. Apple is far more experienced at fostering growth of a third-party developer ecosystem than any other company currently competing in the auto industry. This would raise serious security and privacy concerns though, other areas that Apple excels in.

Figure 3: Automotive Tech Stack (source: Created by author)

Apple’s technology expertise and vast resources do not guarantee success and while Apple has had a string of successes over the past 20 years, they also have a history of failure when moving into radically new market, like the Apple Pippin. Much of Apple’s past success has been in areas of computing which have been resource constrained. This will be a less important consideration in an electric autonomous vehicle, although the energy usage of hardware will be an important contributor to vehicle mileage.

Apple’s previous success has also primarily been in portable consumer devices. Apple is a fashion statement as much as a consumer device and could be considered a form of conspicuous consumption. This could point towards success in the car market though, as cars are often considered a status symbol and aesthetics are generally quite important.

Apple is reportedly reviewing every detail of car engineering and manufacturing, likely in an attempt to isolate where they can add value. For example, they are reportedly developing improved battery technology to extend vehicle range. This is not surprising given that battery technology is likely to remain an important determinant of cost and performance for many years. While Apple has significant resources to throw at these types of problems, they are not magicians and most of their success has been in fairly specific areas. Whether they can rapidly develop a lead in an area like batteries is highly questionable given the amount of industry R&D focused on this area in recent years. Apple also has limited experience with mechanical devices and it would be unreasonable to expect Apple to be able to significantly improve on existing car designs. The number of electronic components in vehicles is increasing rapidly though, with Intel predicting that chips will account for 20% of the cost of a premium vehicle by 2030, up from 4% in 2019.

Apple are planning on working with a partner on manufacturing, which points towards a continuation of Apple’s strategy of outsourcing perceived low-value activities so they can focus on areas where they can add value. Hyundai has been mentioned as a potential partner, amongst others, but it questionable how valuable an Apple partnership would be for an existing manufacturer. An Apple car is likely to expensive and hence relatively low-volume and Apple is notorious for capturing all of the economic value in its deals.

It has been suggested that Hyundai Mobis would be in charge of design and production for some Apple car components and Kia could provide a US production line in Georgia. Hyundai Mobis is the parts and service arm of Hyundai Motor Company and is one of the leading automotive suppliers globally. As part of an agreement Apple planned to invest 3.6 billion USD in Kia Motors, which would help to align incentives. Hyundai executives were said to be divided over the prospect of a deal with Apple though.

While Hyundai may make quality cars, they are far from being a prestigious brand, which points towards how Apple views the actual vehicle. They simply want a partner who can manufacture a large volume of vehicles with decent quality and likely prefer someone they have negotiating leverage over. Hyundai’s concerns probably stem from the fact that any deal may not provide them with much benefit, as Apple will probably not provide the volume to make a manufacturing partnership particularly appealing.

Apple is also supposed to have approached Nissan but the negotiations were brief due to the proposed terms of the deal. Nissan was worried that it would be reduced to a commodity supplier, a completely valid concern. Apple has also reportedly investigated contract manufacturers like Foxconn due to difficulties finding an appropriate automotive partner. Foxconn is the main assembler of iPhones and recently unveiled an electric vehicle chassis and software platform. This points towards the commodification of the actual vehicle and how the automotive supply chain is evolving in response.

Apple has also reportedly been in negotiations with LG Magna e-Powertrain, despite their relatively small manufacturing capacity and held talks with the electric vehicle company Canoo in 2020, although these talks did not progress.

Timing

It is no coincidence that the rise of electric vehicles has spurred new entrants into the car market. Electric vehicles are much simpler than ICE vehicles, lowering the barriers to entry and making it feasible for a new entrant like Apple to succeed. The increased reliance of automotive companies on suppliers over time has also lowered barriers to entry. Companies like Tesla have been able to enter the industry by initially assembling parts manufactured by suppliers, a far easier proposition than having to design and manufacture tens of thousands of components.

Apple began work on an electric vehicle in 2014, with in excess of 1,000 employees committed to the project. The project has been plagued with management and senior personnel turnover issues though, which could point towards underlying problems. It is now being reported that the Apple car team is being dissolved, which raises questions about the timeline of the project.

Suggested dates for the launch of an Apple car range from 2025 to 2028, or possibly even later. An extremely long timeline given Apple’s initial foray in 2014. By the time Apple has a product on the market, the electric vehicle market will already be decided. The extremely slow pace at which Apple has moved from its initial forays in car development to realistic launch date suggests that they are not committing to the market until autonomous vehicles are a reality. This makes sense given that the strategic logic for Apple entering the car market is based on the availability of autonomous driving technology.

While autonomous driving technology is improving, it is still not clear when it will be widely available. Timelines keep pushing back, although the technology is improving. Company’s like Waymo and Cruise appear to have solutions that work reasonably well, it may just be a matter of extending that solution to more environments and building a better understanding of edge case behavior. Although, autonomy is the type of problem where a solution could remain elusive long after the problem seems largely solved.

Waymo now has a fully autonomous robotaxi service operating in Arizona and Cruise are launching one in California. Tesla also continue to claim that they are on the verge of full autonomy. Apple’s program is far less mature and a licensing arrangement would appear to be the fastest way to market at this stage. Even once the technology is adequate there are still regulatory and insurance liability questions.

Valuation

The value of an Apple Car will depend on both whether Apple can develop a unique value proposition and the business model they choose to implement. Apple appear to be developing their own vehicle rather than licensing a hardware and software package to other manufacturers. Licensing could be a good match for Apple’s capabilities and a relatively low-risk way to capture value from the automotive industry value chain, but Apple is unlikely to place their brand in the hands of other companies like this.

As a premium auto manufacturer Apple will not be able to achieve the large volumes and high margins of their other consumer devices. This could still be a worthwhile opportunity if they are successful though. Whether this is the case is questionable as they will be entering a mature market by the time, they have a vehicle ready. Apple will always have a measure of success in any new market as many Apple customers will buy their products regardless of quality or price.

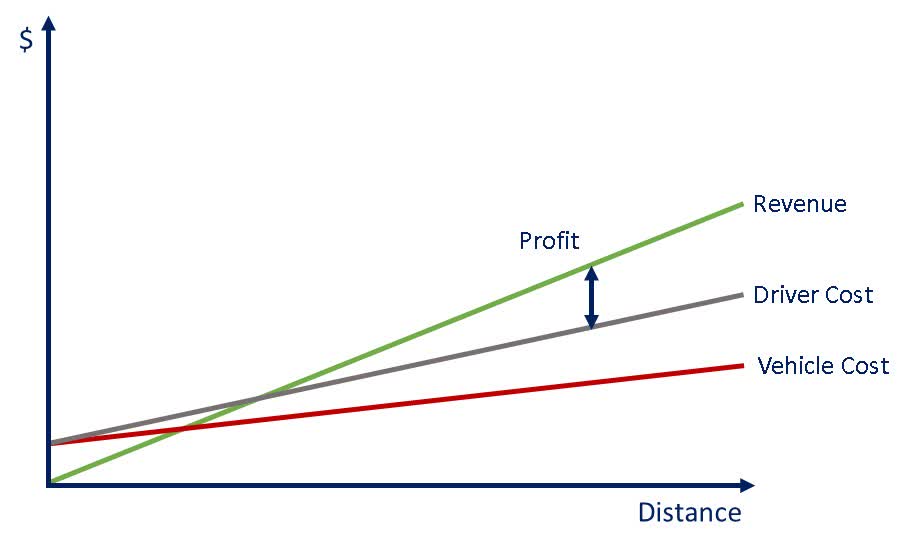

It has been suggested that the first Apple vehicle released will be completely autonomous and hence could find application in food delivery and robotaxi operations. While high-end robotaxis are a possibility, food delivery seems highly unlikely as this will be a commodity service focused on cost, the antithesis of Apple’s business. Apple operating their own robotaxi service also seems unlikely as it will be an operations intensive business that could potentially have poor economics.

Ridesharing is a business that is currently plagued with poor economics due to the fact that the consumers’ willingness to pay is in line with the cost of operating a vehicle. In addition, taxis / ridesharing is a commodity service that faces price competition wherever there is more than one strong operator.

Figure 4: Taxi Profit per Unit Distance (source: Created by author)

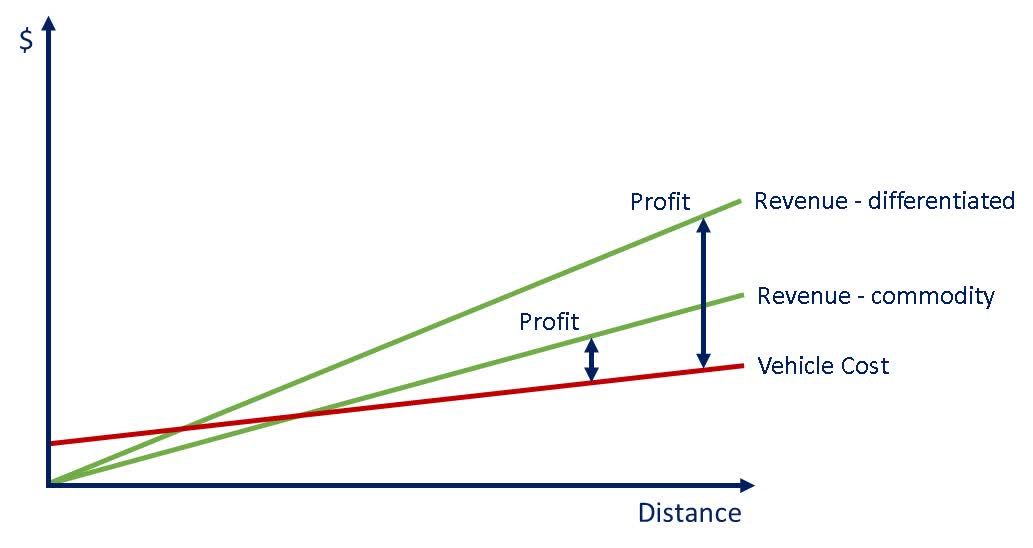

Robotaxis could improve the economics of the market by eliminating the cost of drivers, but this will depend on whether taxis remain a commodity service or if a monopoly forms. If only one company successfully develops autonomous driving technology, they should achieve high margins due to their lower costs relative to ordinary taxis. If one company has a differentiated service (safer, smoother ride, etc.) they may also be able to achieve high margins by charging a higher price. With Waymo, Cruise and Tesla all appearing to be making progress towards autonomy, it may end up being that robotaxis end up being a boon for consumers but a disappointment for service providers.

Figure 5: Robotaxi Profit per Unit Distance (source: Created by author)

Transportation in general has poor economics and most auto manufacturers are no exception. The increasing importance of electronics and software and the rise of electric vehicles has the potential to change the industry’s profitability though.

Table 1: Comparable Company Revenue and Market Capitalization (source: Created by author using data from Seeking Alpha)

General Motors expect margins to expand to 12-14% by 2030, driven in large part by their new businesses portfolio which they expect will have margins in excess of 20%. Revenue is expected to grow to 275-315 billion USD by 2030, with the new businesses portfolio growing approximately 50% annually.

Table 2: General Motors’ New Businesses Portfolio 2030 Opportunity

In addition to product sales, the Apple Car could also offer Apple another platform with potential service revenue. This could be in the form of a take rate on an App Store or through services like insurance.

A realistic current value for Apple’s car business is probably something like 100-200 billion USD, assuming that Apple is a niche vendor with high margins and associated service revenue. While this would be a massive opportunity for most companies, it is not much more than a rounding error for Apple, particularly given that this may be more than a decade away and is a high-risk opportunity. Apple must also weight the risk of brand damage that could occur if the Apple car performed poorly or there were safety issues with the self-driving system. Customer backlash across the Apple ecosystem could drastically outweigh any potential upside.