CasPhotography/iStock Editorial via Getty Images

Introduction

Apple Inc. (NASDAQ:AAPL) recently published its annual dividend hike. The consensus expectations were a hike somewhere between 5-10% in line with previous years, not least due to Apple’s very low payout ratio, strong cash generation, and arguably the question as to whether a continued acceleration in the share buyback made sense due to its steep valuation. However, investors were left surprised, as a 4.5% hike was published while the buyback program once again received a substantial allocation in form of an additional $90 billion.

Arguments can be made for and against, as some prefer to avoid the tax associated with receiving dividends in comparison to a reduction in the float, while others are hoping that Apple will one day turn into a dividend nest egg. One look at the comments from SA members as the news broke, and the dilemma is clear.

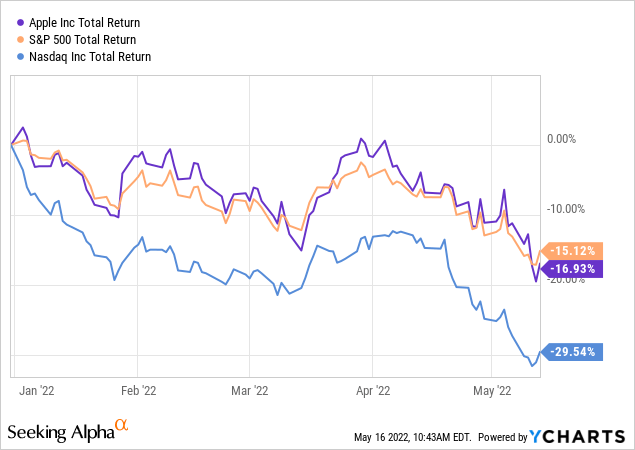

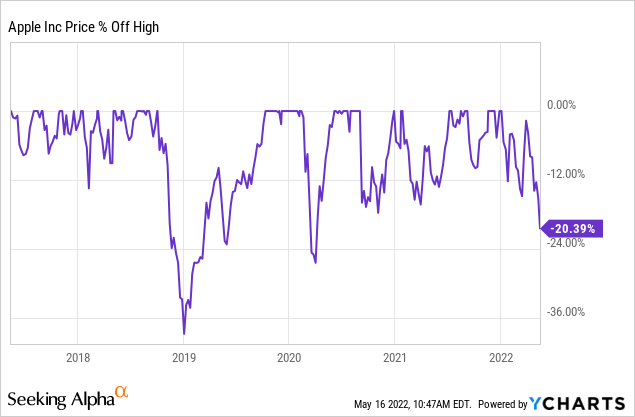

In line with the broader market sell-off, Apple has finally also had to give in, being down in conjunction with the broader index despite beating the Nasdaq in a YTD comparison, and both indices if comparing on a six-month basis. Apple only recently started to downtrend, and was up compared to the index until news broke that the company expected revenue headwind during the summer due to prolonging Covid-19 issues. I’ll come back to why that doesn’t matter in the big picture.

If we zoom out, Apple has done nothing but grow its top- and bottom-line in the last decade, with the very strong free cash flow generation and adaption of new product offerings amongst consumers suggesting Apple will continue to secure returns for its investors going ahead – making the pull-back a welcome opportunity for those looking to expand their position.

In conjunction with the quarterly results published on April 28th, management communicated a potential $4 to $8 billion impact from the continued China and raw material-related Covid-19 issues, which caused the recent sell-off as the share price suffered the following days. However, for the long-term investor, this only serves as an opportunity, as it doesn’t impact the general outlook for Apple. Management didn’t act scared, either, with their increased $90 billion allocation to the existing share buyback program.

Losing $4 to $8 billion in sales would be devastating for most companies. However, in the case of Apple, the real impact is probably that customers will simply have to wait a bit longer to execute on their buys, as the underlying demand for Apple’s products and services remains. Effectively, it’s a matter of postponement more than a total loss of sales. Despite the impact, Apple is well on its way to beating the FY21 result.

Apple Key Metrics

Apple closed its FY2021 with a remarkable $365.8 billion in revenue, $154.8 billion in gross profit, $94.7 billion in net income, and $92.9 billion in free cash flow. The pure numbers are remarkable, and Apple is one of the few companies on earth that is earning so much cash that it simply doesn’t know where to put it. Management pours billions into share buybacks only to discover the next quarter generated a ridiculous amount of free cash flow.

What’s even more impressive is that Apple is well on its way to breaking its own record when we look to the expected FY22 results. With 2022-Q2 in the books, Apple managed to secure $221.2 billion in sales compared to $201 billion YoY, a 10% increase. Services increased total sales to $39.3 billion, up from $32.6 billion the year prior, while costs associated with sales of services only increased from $10 billion to $10.8 billion, meaning the bottom line looked very strong as net income grew from $52.3 billion to $59.6 YoY. The additional $7.2 billion in net income translates to a 13.8% growth YoY – stunning. Just to highlight the magnitude, Apple makes more in net income than Texas Instruments (TXN) and Broadcom (AVGO) make in combined revenue, $45.8 billion.

Apple Investor Centre 10-Qs

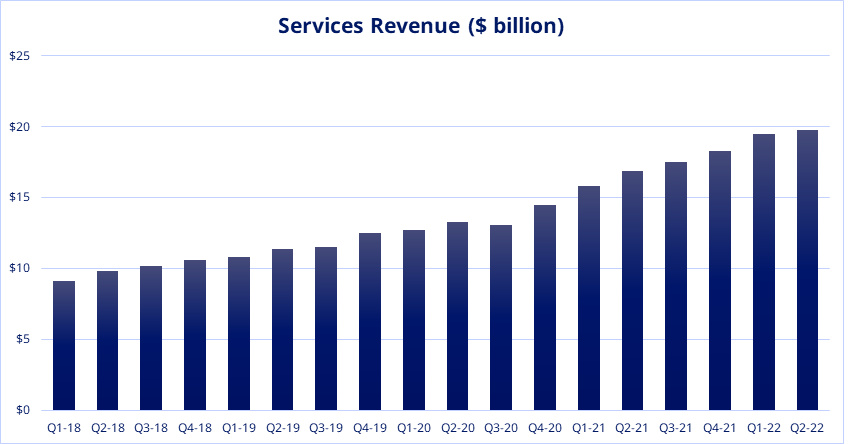

While Apple used to be all about the iPhone, which raked in $192 billion for FY21, the company has also managed to secure itself a very strong wearables and services business, both of which have surpassed the Mac sales which used to be the second largest division. Wearables secured $38.4 billion in FY21 sales, while services contributed with a whopping $68.5 billion. The graph above shows the ever-growing nature of services, whereas all the other segments have seasonality effects due to the X-mas season. The reason we love services as investors is that they are a high-margin businesses, and Apple is growing theirs consistently. Remember this is quarter-on-quarter comparisons, therefore now illustrating the YoY difference, but instead they consistently grow the business every single quarter.

Q2-22 revenue for wearables of $23.5 billion and $39.3 billion for services are well on the way to toppling the strong performance during FY21. In other words, despite the expected $4 to $8 billion impact, Apple could very well be expected to provide a FY2022 result that will exceed the stellar FY2021. Even better, what will FY2023 look like, when the headwinds are mitigated?

If we take on the true long-term horizon, Apple currently has in excess of 825 million subscriptions related to its services segment. Depending on how growth will look like, exceeding $100 billion in revenue from services doesn’t seem like a stretch, which would contribute to reducing the dependency for iPhone upgrade cycles in order to secure a continued streak of record top-line performances. Furthermore, it would result in even more free cash flow going Apple’s way.

Apple Investors Centre

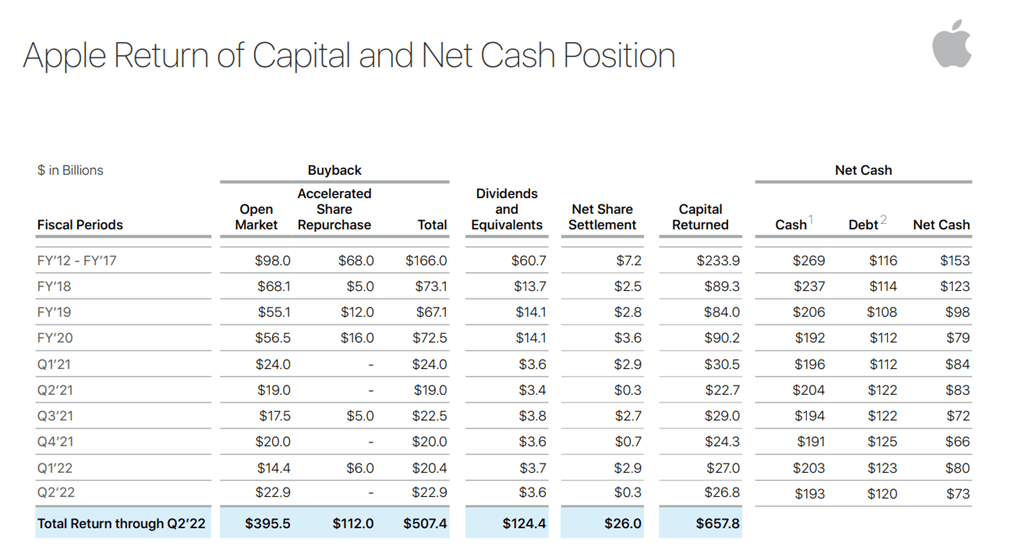

Apple has maintained a return on invested capital exceeding 30% on average for the last five years, accelerating in recent years, creating much more cash than what management knows what to do with. Companies should pursue attractive investments, but if there aren’t any opportunities meeting the expected returns of invested capital, management can decide to reward shareholders via either M&A’s, buyback, or dividends. As such, one of my preferred overviews for each earnings season is the updated capital returns overview provided by Apple.

As can be seen above, Apple bought back $22.9 billion worth of its own stock during last quarter, equating to just below $370 million on each trading day during the quarter. During FY21, Apple bought back a total of $85.5 billion of its own stock, totaling $246 billion counting FY18 up until today. Still, Apple holds $51.5 billion in cash on its balance sheet, with an additional $141.2 billion in long-term investments. Apple can continue playing this game for a very long time.

The amount of buybacks is a meaningful contributor for investors, resulting in them owning a growing amount of the company’s equity and cash flow as the float is continuously reduced. In the last decade, the combined total of buybacks has resulted in the number of outstanding shares having been reduced by 36%. That capital deployment strategy of Apple is a smart way to reward shareholders, who continue to hold their shares, as opposed to the immediate return in the form of a dividend. With a payout ratio below 15%, Apple has plenty of room to grow its dividend.

Apple And Its Dividend

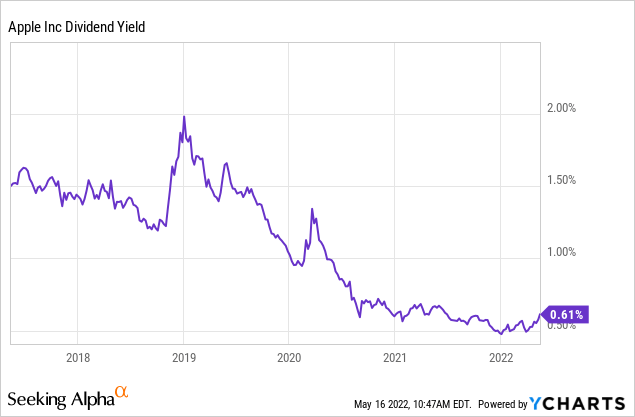

With the recent 4.5% dividend hike, Apple now holds a ten-year dividend hiking streak. With a current payout ratio below 15%, it’s as safe as it gets. Is Apple’s dividend yield good? No, I don’t believe it is, but it is extremely safe, and Apple has embarked upon the dividend growth highway. There is no reason to suspect they shouldn’t continue hiking it.

Seeking Alpha

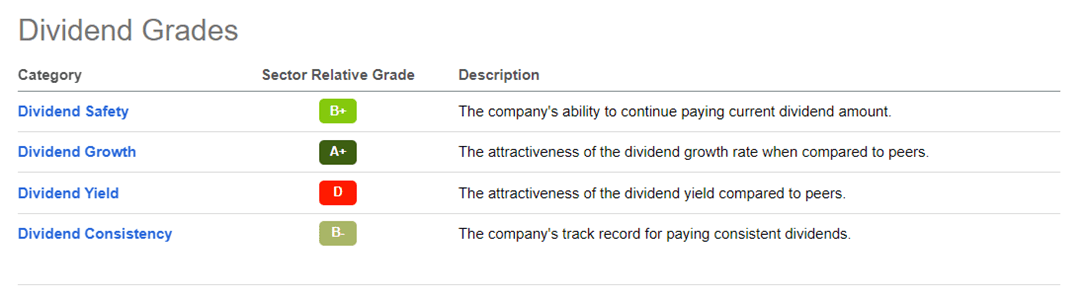

If we look at the dividend grading tool found via Seeking Alpha, it underlines why we should feel comfortable to receive a growing dividend, as the company has absolutely no problem funding its dividend, and the consistency score will eventually climb towards a better score as they maintain the streak. The score is given relative to its sector peers, and here Apple scores an A+ grade for its dividend growth. While this may objectively be true on a comparable scale, I’d provide it a lower grade due to the low hikes due to the capital strategy employed by management. The forward consensus expectations for next year’s hike are once again a 4.5% hike, with the following year consensus being a 7.5% hike. Apple could easily hike much more aggressively but has chosen a different capital deployment strategy.

Due to Apple’s quality as a company, it also means the initial yield is the soft spot. It consistently hovers below 1% seen on a multiyear horizon. Especially as the market has begun rewarding Apple with a higher valuation in the recent years.

However, let’s put it into perspective, as the dividend yield shouldn’t keep one from determining if Apple is at an interesting price point.

Apple has beaten both the S&P 500 and Nasdaq on a 10-year and 5-year horizon, so management is evidently creating substantial value for shareholders through their choice of capital allocation. As such, I’ll collect the paltry dividend and play the long game while management continues to grow the business and reward my patience, as Apple has proven to be a very good stock for long-term holders. Personally, I had hoped for a more substantial dividend hike, and will continue to hope so, but as long as Apple continues to drive strong returns through appreciation supplemented by a growing dividend, I don’t see a reason to complain. Furthermore, I don’t see a reason why the low initial yield should keep investors away from Apple even if their strategy is focused on accumulating dividend payers.

Normally, I’d await a pullback to obtain the best possible initial yield, but as the yield plays such a small part of the overarching story for Apple, I’d ignore that and instead consider the pullback from a total perspective and the fact that it likely provides an interesting starting point. Apple is simply too strong a company from a financial standpoint.

Valuation, Investor Strategy & Conclusion

I believe comparing Apple to Microsoft (MSFT) is a fair approach, even though Microsoft is growing its revenue at a faster pace due to its exposure to cloud offerings while also coming from a lower revenue and FCF basis. On a price to free cash flow basis, Microsoft is valued at 31 times FCF in comparison to Apple’s 23 times FCF. On a five-year horizon, both of these companies are trading above average, but only to a slight extent, while the ten-year horizon shows a clear gap in comparison to the average as they are trading well above their historical levels. Similarly, Microsoft is trading at P/S of 10.2, with a forward P/S of 9.8 in comparison to Apple’s P/S of 6.3 and forward P/S of 6.0. Seeing that Apple continue to grow its revenue with its earnings growing even faster due to a shrinking float but also a growing service segment commanding higher margins, I don’t find a forward P/S of 6 to be a bad deal.

As an investor, however, I can’t help but also notice that the stock is trading well above its historical levels as shown above. While I’m already long Apple, if I were to initiate a position today, I’d dollar cost average my way into the company. Meaning, that one can risk losing out if the stock suddenly goes up, but also avoid a downturn if the market continues dropping. It’s a personal preference, after all, but I don’t believe Apple is a “screaming buy,” and as such I’d go with that approach.

Apple is quality, and it’s not possible to find a company churning out as impressive numbers as Apple on such a massive scale. However, it’s still not in real bargain territory despite the recent pullback. With Apple, however, the massive quality delivered by the company also means that it’s rarely trading well off its recent high, and in fact the current set back is the largest since the general market crash in connection to Covid-19 during early 2020. Even here, the company was only pushed roughly 25% off its prior peak.

Conclusion

Wrapping it up, while Apple doesn’t provide an interesting yield, it should, over time, be able to grow that dividend many times over, considering it’s not done growing its FCF and that the current payout ratio is below 15% – in fact, should the yield even matter for the investment thesis at this point? Further, Apple has managed to beat the market on both a 5-year and 10-year horizon, and while history doesn’t guarantee future performance, Apple generates incredible amounts of cash that it uses to reward shareholders while still growing all of its divisions year-on-year if comparing the Q2 results of 2022 to those of 2021 with the iPad sales being the exception. However, also being the smallest, all the other products and services more than make up for it, with Apple on track to beat its FY21 performance despite an expected headwind during this summer due to Covid-19 still being a factor in relation to supply chains.

Apple remains a strong tech company with low risk due to stickiness of products resulting in growing sales despite the massive top-line.

Can Shock Market, Bitcoin’s (BTC) Explosive Performance Is Coming, Shiba Inu (SHIB): Make It or Break It By U.Today – Investing.com")