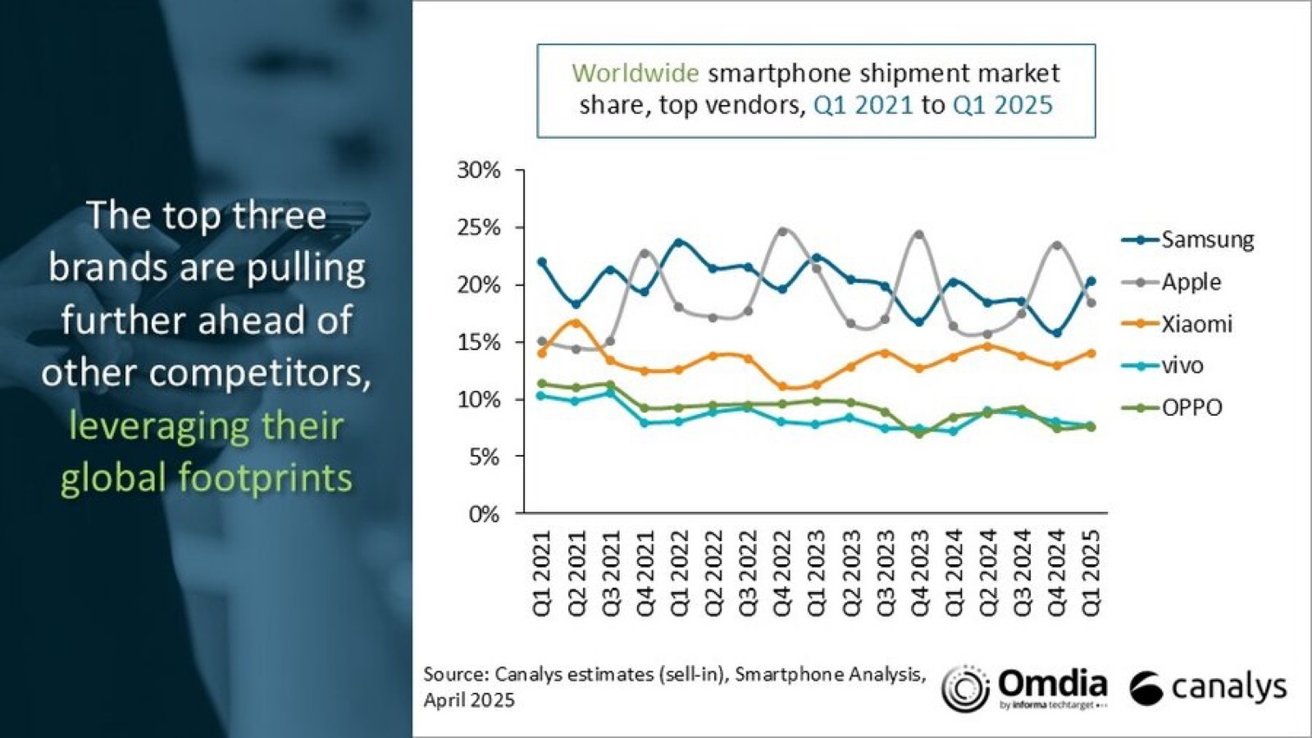

Apple gained significant market share in early 2025, growing 13 percent while the global smartphone market remained essentially flat.

Apple outpaced the broader smartphone market in Q1 2025, shipping 55 million iPhone units and increasing its global share to 19 percent, up from 16 percent a year earlier, according to Canalys Research’s April report.

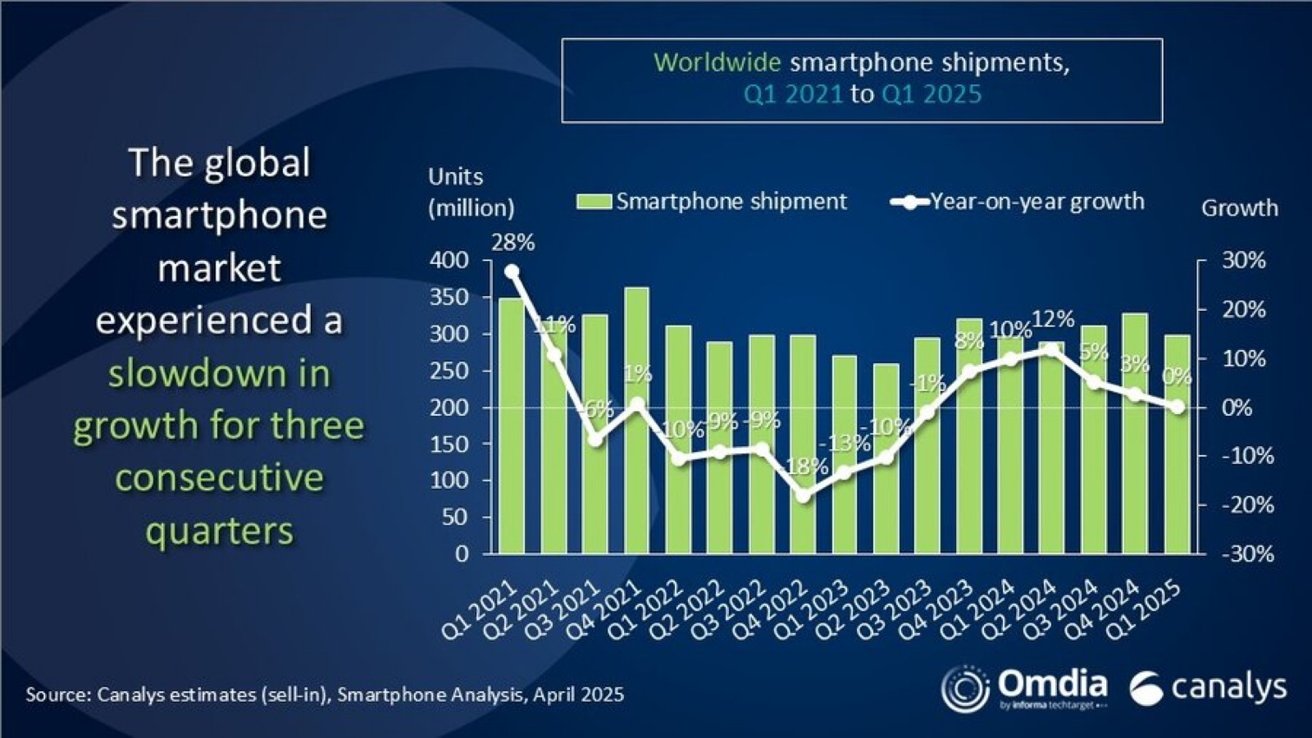

The overall smartphone market grew just 0.2 percent year over year, reaching 296.9 million units. Apple’s 13 percent growth stood out, driven by strong demand for the budget-focused iPhone 16e and sales momentum in the United States and emerging Asia Pacific markets.

iPhone 16e launch reshapes early-year sales

The iPhone 16e, launched in February, gave Apple an unusual boost during what is typically a slower post-holiday quarter. Most vendors see Q1 dips as holiday-driven demand fades, but Apple’s timing helped it sustain interest and expand reach in more price-sensitive regions.

Worldwide smartphone shipments. Image credit: Canalys

Samsung remained the top global vendor with 60.5 million units shipped, essentially flat year over year. Xiaomi grew 3 percent to 41.8 million units, while vivo increased 7 percent. OPPO declined 9 percent, and smaller vendors collectively lost market share, dropping from 34 percent to 32 percent.

Apple’s performance was also shaped by its strategic response to global trade risks. The company built up U.S. inventory ahead of potential tariffs and accelerated production in India for the iPhone 15 and iPhone 16 series.

Top three brands. Image credit: Canalys

These moves reduced its reliance on Chinese manufacturing and gave it more pricing flexibility in volatile markets.

China remains a challenge for iPhone growth

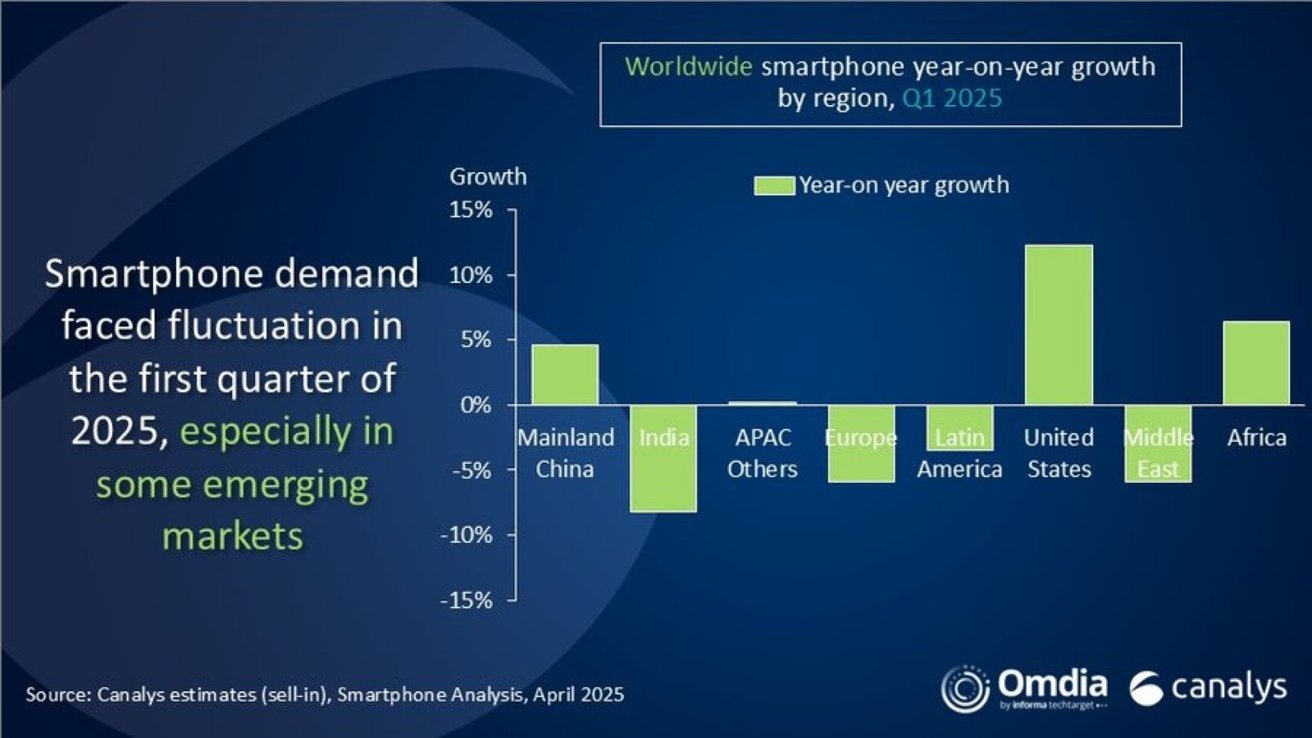

The U.S. smartphone market grew 12 percent in Q1, with Canalys attributing most of that growth to Apple. While iPhones built in China still made up the majority of U.S. shipments, India is now covering standard and Pro models — giving Apple insulation from future policy shifts.

Not all regions were as favorable. In China, iPhone shipments declined 9 percent year over year. Government subsidies and growing local competition challenged Apple’s pricing power in the mid- and low-end segments.

Android brands are now feeling the squeeze in the $200 to $400 range. Consumers are becoming more cautious, upgrade cycles are lengthening, and pricing pressure is growing.

Smartphone demand. Image credit: Canalys

Apple, with its bundled services, software ecosystem, and aggressive trade-in offers, is better positioned to weather these shifts than most of its rivals.

For now, Apple remains one of the few smartphone makers showing clear upward momentum. Whether that trend continues will depend on its ability to manage production, stay ahead of tariff headwinds, and maintain product appeal across premium and entry-level segments.