ljubaphoto/E+ via Getty Images

Apple Hospitality (NYSE:APLE) is a lodging-focused real estate investment trust (“REIT”) that owns one of the largest portfolios of upscale hotels in the U.S. Their portfolio includes over 200 hotels, principally under the Marriott (MAR) and Hilton (HLT) brands, with nearly 30k guest rooms located in 86 markets across 36 states.

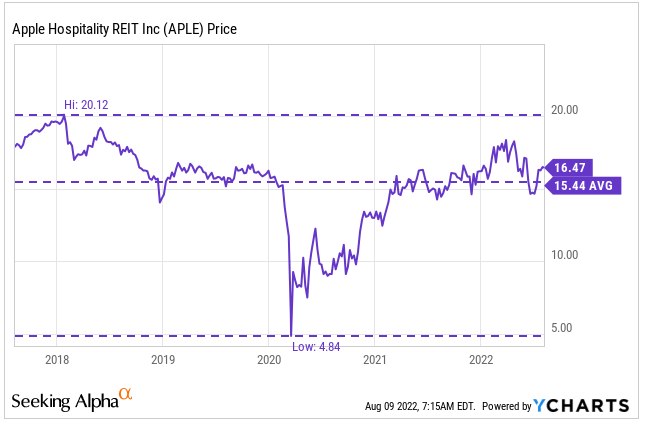

Following their share-price low of less than $5 in the early part of 2020, shares have since rebounded 240%. Over the past one year, however, shares have traded in a tight range, separated by less than $5 in their 52-week range.

YCharts – APLE’s Recent Share Price History

At present, APLE trades at 10.5x forward funds from operations (“FFO”), an enterprise multiple (“EV/EBITDA”) of 14.2x, and at the midpoint of their 52-week range. Shares were boosted following their recent earnings release on increased optimism on future travel demand. Though already up 10% on the month, the rally still has room to run.

Continued strength in leisure travel complemented by improvements in business travel are likely to support further earnings growth in subsequent periods. An eventual return of the dividend to pre-pandemic levels is also not out of the question. For investors seeking to capitalize on roaring demand for travel and services, APLE presents an attractive upside opportunity.

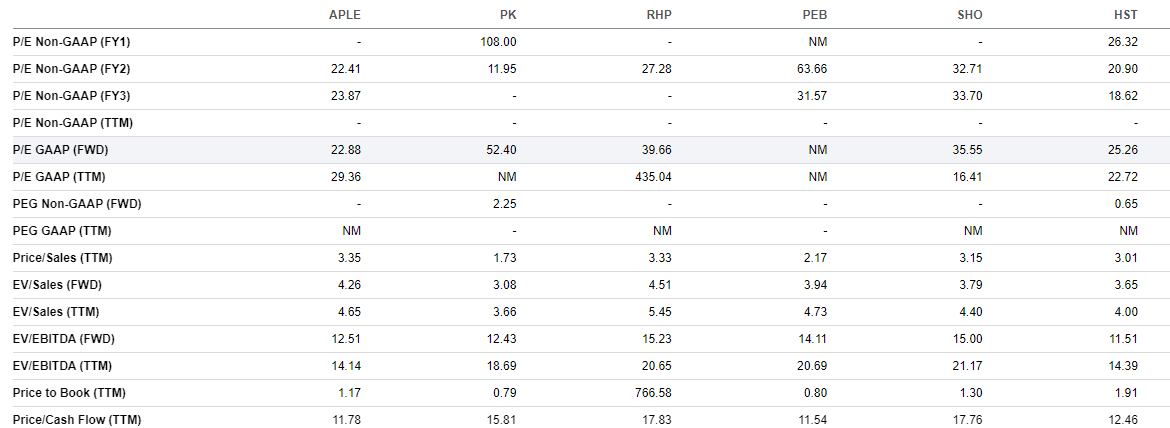

How APLE Stacks Up Against Their Peers

Within the overall REIT lodging sector, Host Hotels & Resorts (HST) is the largest component and the only one to have a current market cap of over +$10B. With a cap of +$3.4B, Park Hotels & Resorts (PK) is the most comparable peer to APLE, though other names trade at similar levels as well.

Seeking Alpha Peer Comparison Tool – Total Market Cap

Over the past month, the sector has experienced a strong run higher, with shares of most up nearly 10%. Still, with the exception of PK, their YTD performance is lagging the returns they have delivered over the past three years, approximately 12% in the case of APLE.

Seeking Alpha Peer Comparison Tool – Total Returns

On valuation, APLE appears to be discounted to their peers with an enterprise multiple of 14x. While this is similar to their larger peer, HST, it’s a few points lower than their smaller counterparts.

Given the company’s strong financial position and their dividend paying capacity, along with the growth opportunity afforded to them by continuing improvements in business travel, it’s not unreasonable to input a 16x multiple to TTM EBITDA. This would be more in-line with the sector median and closer to their historical averages.

Seeking Alpha Peer Comparison Tool – Valuation Metrics

Robust Travel Demand Is Accelerating APLE’s Recovery

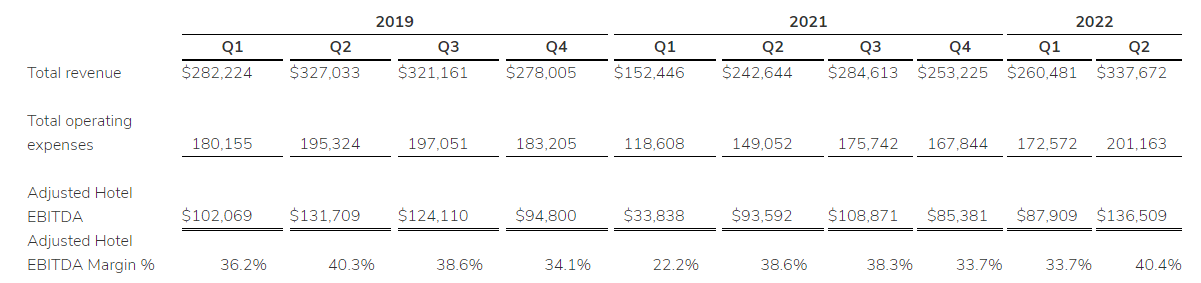

APLE’s most recent earnings release showcased continuing recovery across their portfolio. On the top-line, total revenues were up 36.5% in the quarter, driven by a 27.2% increase in average daily rates (“ADR”). The significant increase in rates resulted in growth in revenues per available room (“RevPAR”) of 40% to $119.41. This was also up 4% compared to the second quarter of 2019.

Overall occupancy came in at 78%, up 10% from 2021 but still down about 4% from 2019, mainly due to the lag in recovery from the business sector. In a positive sign, weekday occupancy, which tends to be weighted towards business travel, reached 75% during the quarter. Comparatively, weekend occupancy came in at 85% for the quarter, which was not only better than last year but also 160 basis points (“bps”) greater than the same period in 2019. Building momentum on weekday bookings combined with continued strength on the weekends should present favorable conditions for future earnings growth.

Challenging labor conditions marked with higher wages continues to impact earnings. The company, however, appears to be successfully navigating around it through effective cost control and growth in ADR. Excluding payroll costs, for example, same-property expenses were actually down 4% per occupied room compared to 2019. This resulted in EBITDA margins of approximately 40%, up 10bps from 2019.

Q2FY22 Earnings Release – Summary of Operating Results

In July, rates continued to increase, according to management, but overall occupancy in the month was down 6% from 2019 due primarily to lower business demand on the fourth of July holiday. This is slightly worse than the 4% gap during Q2. Nevertheless, there is a high degree of confidence that earnings will move beyond pre-pandemic levels in the near-term if current trends continue.

56% of the portfolio, for example, produced RevPAR above pre-pandemic levels during the quarter. In addition, bookings were up 38%, with weekend metrics already surpassing expectations and weekday occupancy in the months of April and May down just 8% compared to 2019.

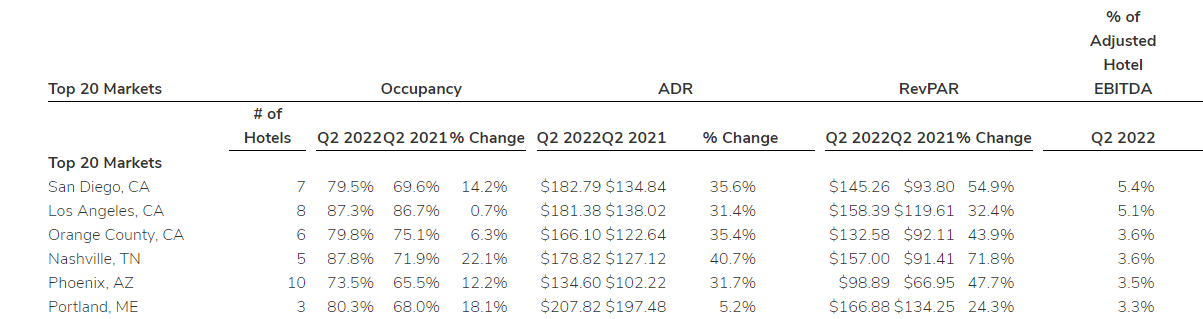

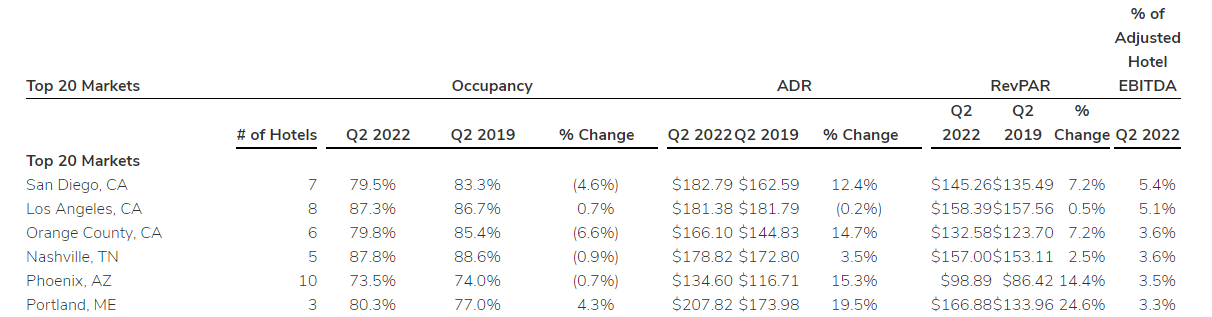

Furthermore, APLE appears to be making significant strides in their top 20 markets, with occupancy up double-digits compared to last year. And in the Portland market, occupancy was up 4% versus 2019, with ADR growth of nearly 20%.

Q2FY22 Earnings Release – Snapshot of Performance of Top 20 Markets Compared to 2021 Q2FY22 Earnings Release – Snapshot of Performance of Top 20 Markets Compared to 2019

In the past, APLE has benefitted from acquisition activity. While activity is expected to slow, given the current environment, management still intends on capitalizing on opportunities as they arise. In the meantime, they intend on spending a yearly total of +$55M to +$65M investing in their own properties, which represents approximately 5-6% of total revenues, in-line with their historical averages.

Manageable Debt Load, Despite Greater Holdings Of Variable-Rate Debt

APLE’s current debt load is +$1.4B, which is just 26% of their total capitalization on a net basis. As a multiple of TTM EBITDA, leverage stood at 3.7x. This is manageable, considering close peer, PK, recently reported a leverage multiple of 4.91x.

Though they aren’t overly leveraged, APLE does have a sizeable number of near-medium term maturities. Over 80% of total debt, for example, is due prior to 2027. In addition, 66% of total debt is structured as variable-rate. This increases interest rate risk during periods of rising rates, as is the case in the current market environment. Given the inversion in the yield curve, however, it’s likely rates will trend lower in 2023/2024. The risks, therefore, are likely to be negated over time.

Q2FY22 Form 10-Q – Summary of Debt Maturities

During the quarter, APLE was an active participant in the debt markets. In addition to repaying a +$56M note issued last year in connection with their purchase of a fee interest in the land at the Seattle, Washington Residence Inn, APLE refinanced their primary unsecured credit facility, which provided improved pricing and an upsizing in available funds. The increase in available funds provides the company with greater access to liquidity, which currently stands at +$350M, for strategic growth and other initiatives.

A Dividend That Is Likely To Double In Future Periods

The lower debt load provides APLE the flexibility to provide a monthly dividend payment of $0.05/share. While this is down from the monthly rate of $0.10/share the company was paying prior to 2020, there is room for growth. The current payout ratio as a percentage of modified FFO, for example, was just over 30% for the quarter. In addition, the company generated +$152.2M in operating cash through the first six months of the year.

Even when factoring in their investing activities, their payouts were still covered in excess of 2.50x by free cash flows. Clearly the company has the cushion to grow the payout in future periods. In fact, after being questioned about it on the earnings call from Anthony Powell of Barclays, Justin Knight responded favorably and left open the possibility of future increases.

Q2FY22 Form 10-Q – Partial Cash Flow Statement

The Worst Is Behind APLE, And The Outlook Is Promising

APLE is a quality lodging-focused REIT with a portfolio of over 200 upscale, rooms-focused hotels operating under industry-leading brands, such as Marriott and Hilton. On their most recent earnings release, the results suggested that leisure travel is roaring back, with top line figures already above pre-pandemic levels even without a full recovery in business travel. With overall occupancy still down 4% compared to 2019, there is still upside to be realized in subsequent periods.

Though there are various macroeconomic concerns relating to higher food and energy costs, in addition to a potential slowdown in the economy due to higher interest rates, consumers are not letting these concerns deter them from engaging in experiences that they missed during the lockdowns at the height of the COVID-19 pandemic.

Favorable data on travel and restaurant bookings also indicate consumers are reallocating their discretionary spending priorities from goods to services. This can also be seen in the recent slump in video game sales, as individuals are increasingly engaging in activities outside of their homes.

APLE stands to benefit from the continued strength in leisure travel and an improving outlook in the business sector. This will benefit shareholders in the form of share-price appreciation and material dividend growth.

Currently, the company’s annual dividend payout is $0.60 less than what they were paying pre-pandemic. Their strong balance sheet, however, comprised of a low degree of leverage provides them with the wherewithal to begin raising the payout in future periods. A return to a pre-pandemic payout would represent a yield of 7.3%. This would be on top of potential share price upside of nearly 20%, when applying a 16x EV multiple to TTM EBITDA. With the worst behind them, the future appears promising for APLE and their long-term shareholders.

")