alvarez/E+ via Getty Images

Hotel REITs are cheap but also fundamentally challenged. This article will discuss the underlying mechanisms that make life as a hotel REIT difficult. At the same time, the sector is potentially poised for a rebound with travel restrictions subsiding. Within the turbulent sector, I think Apple Hospitality (APLE) is best positioned.

The tailwinds

With the pandemic winding down and countries starting to remove travel restrictions, there is likely to be a significant rebound in travel in general. I tend to think the rebound in leisure and tourism will be significantly stronger than the rebound in business travel, but both should get a nice reversion toward pre-pandemic mean. There might even be a catchup period in which pent-up demand is finally released causing a spike above pre-pandemic levels for a while.

This demand spike, in combination with the lowered market prices of the hotel REITs has caused a newfound interest in value hunting in the space. Here are the stats that make hotels interesting as potential buys.

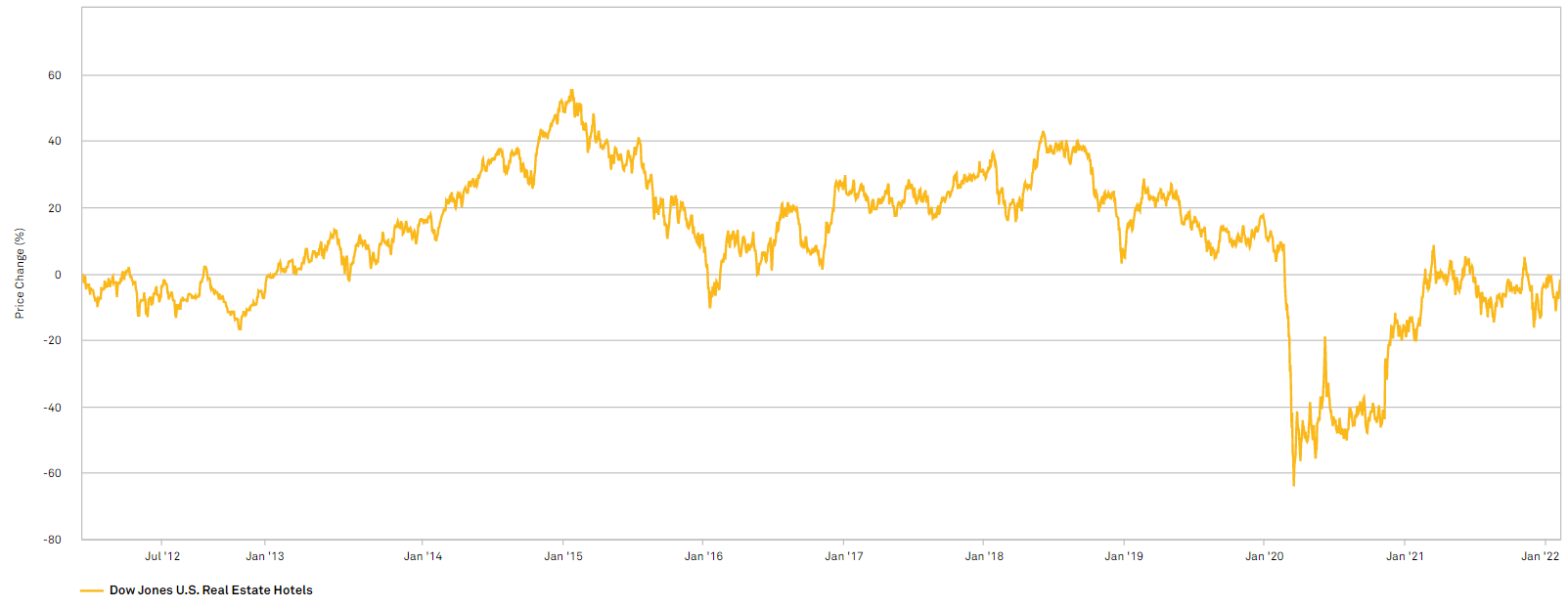

Even as the rest of the market surged past 2019 pricing, hotels remain about 20% below pre-pandemic market prices.

SNL financial

The sector also trades at 85% of net asset value making it one of the most discounted areas.

While I do appreciate stocks trading at discounts, I would emphasize caution in this sector because there are some structural difficulties that persist even as demand rebounds.

Competitive mechanisms and other headwinds

I have frequently discussed how the industry structure favors the middlemen over the property owners. Online travel agencies and the brands get to capture a significant portion of the profits while leaving the risks and costs of ownership on the hotel REITs. For more information on this dynamic, please see our feature length piece.

This headwind remains a challenge, but there are also new challenges that are arising.

Labor costs – staffing levels

Hospitality is a labor-intensive industry. They have managed to cut out much of the front-end staff with technology such as automatic check-in and using guest’s cell phones as their key cards. The back-end staffing, however, is more demanding than ever with new regulations on cleaning frequency and procedures. In addition to having to hire for more hours, the per hour wages have increased dramatically – great for the staff, not so great for the hotels.

Competition – Airbnb and its clones

Real estate is at its most profitable when supply is constrained, forcing tenants to pay up to get their space. Hotel supply and demand has always been somewhat challenging to balance because of the seasonality and even weekly cyclicality of travel. It becomes a balancing act in which a certain number of 50% occupancy nights are suffered in order to have enough supply to handle surge nights in which demand might be 150% of room supply.

The bulk of hotelier profits each year are earned on just a handful of surge nights in which they get both 100% occupancy and dramatically higher prices. Since hotels are generally thought of as a luxury, this practice is not considered gouging. It is just the way the industry works.

Over the years, developers occasionally overshot on supply, particularly in New York City, but generally market forces kept a reasonably good balance between supply and demand. That was until a massive glut of new supply came out of the woodwork in the form of Airbnb (ABNB) and its peers.

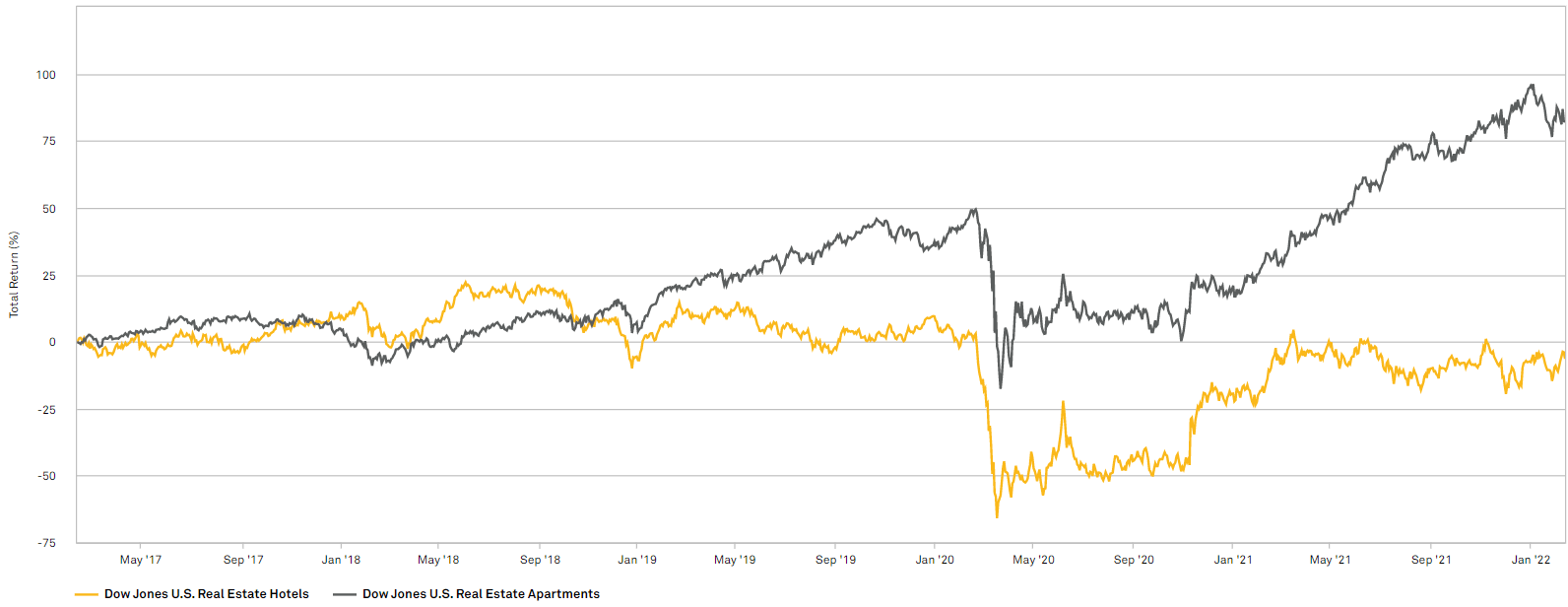

With millions of homes and apartments getting listed as hotels, it was as if a large number of residential properties suddenly converted to hotels. The physical real estate did not change materially, but because the function changed, it was a big negative supply to apartments/single-family homes and a big positive supply to hotels.

I suspect this is one of the contributing factors as to why multifamily has outperformed hotels.

SNL Financial

The end result is that hotels are materially oversupplied which is bad for hotel owners and bad for Airbnb.

Room rates are not keeping up with expense increases and margins are low.

Paid amenities are becoming free amenities

Remember checking into a hotel and then having to pay an additional $20 to use their WiFi? Such tack-ons were a key source of revenue for the hotel owners because the additional revenues were not part of booking the room and could allow the hotel owner to get away from having to share that revenue with the brands or the booking agencies.

This source of revenue seems to be going away as competitive pressures are turning WiFi into a must-have for free. Note how free WiFi is listed front and center on Expedia allowing guests to easily screen out hotels that do not offer free WiFi.

Expedia

Maintenance capex

A rundown hotel cannot charge nearly as much per room night as a well-maintained hotel. As such, wise hotel owners will perform significant maintenance on a continuous basis and major renovations every decade or so. The expense of this practice can be seen in their earnings.

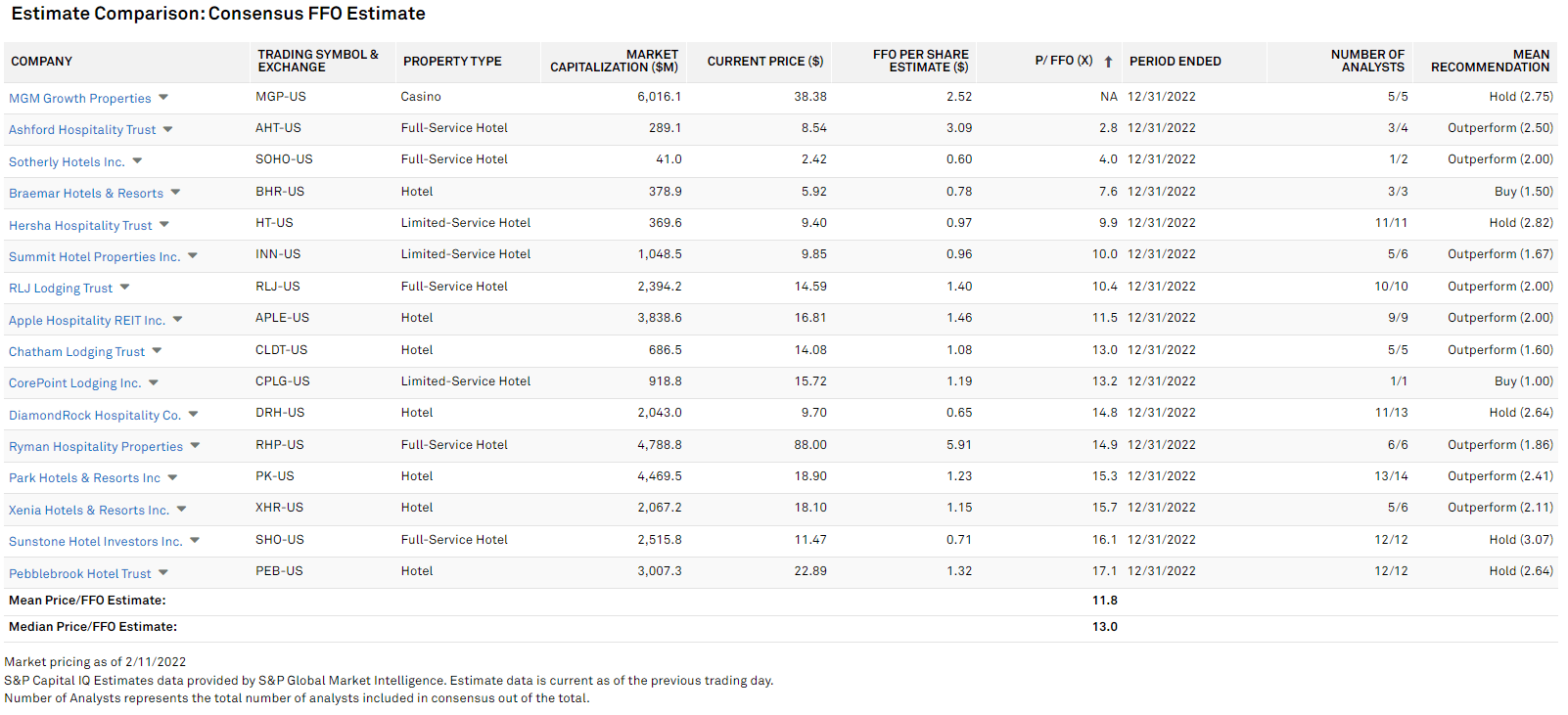

The mean and median hotel REIT trade at 11.8x and 13.0x 2022 estimated FFO, respectively.

SNL Financial

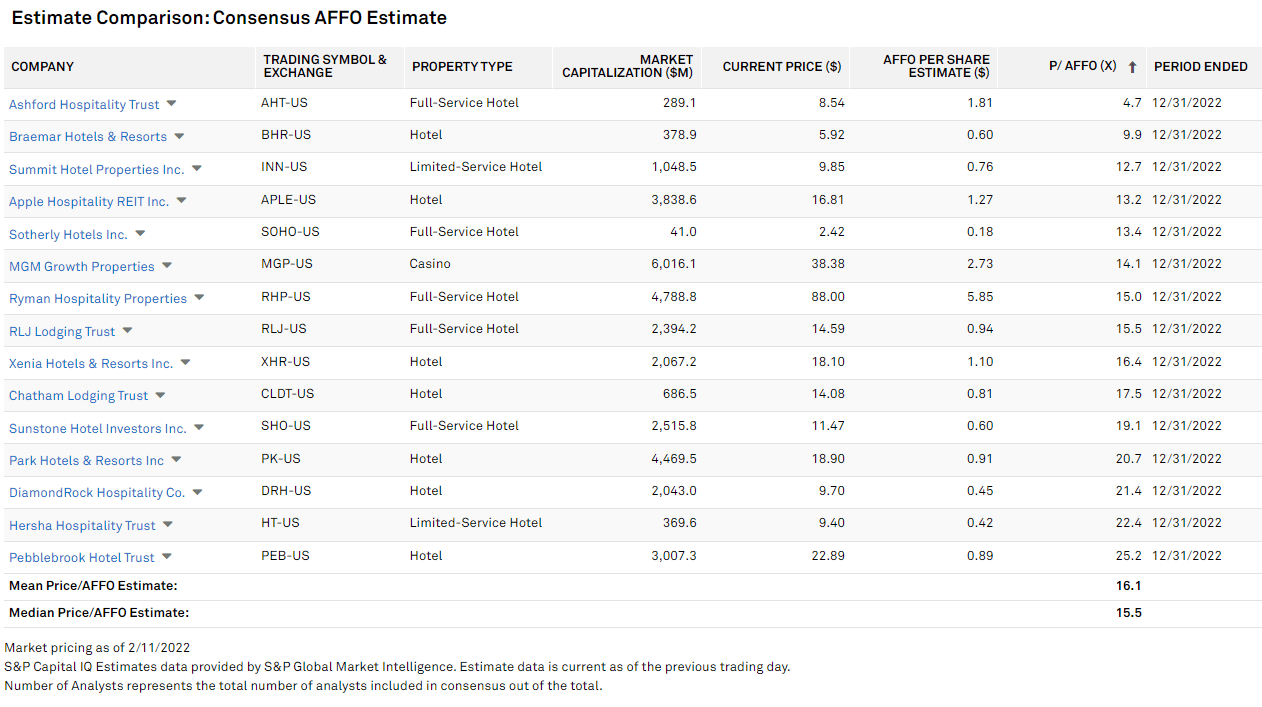

In contrast, they trade at 16.1x and 15.5x mean and median 2022 estimated AFFO, respectively.

SNL financial

A large portion of the difference between FFO and AFFO is maintenance capex which is not counted in FFO and deducted from AFFO.

As such, this is one of the REIT sectors, along with office and retail that generally should be valued on AFFO rather than FFO.

The Outlook

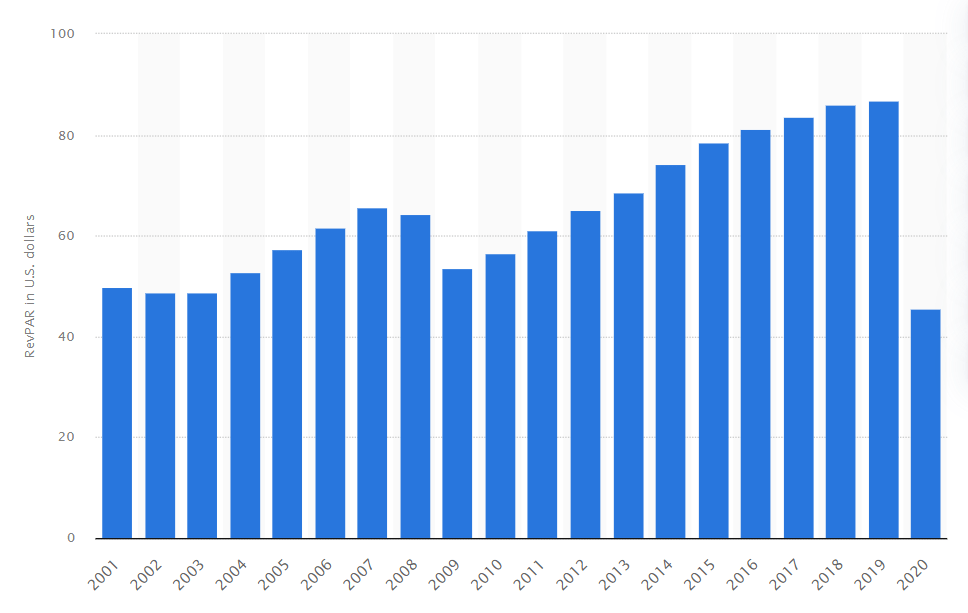

RevPAR or revenue per available room dropped just about in half in 2020.

Statista

In 2021, RevPAR increased significantly but still remains below 2019 levels.

According to Smith Travel Research, occupancy in 2021 was 57.6% and RevPAR was $71.87. In theory, this leaves significant room for further rebound. If occupancy and rates were to recover to the previous normal plus an adjustment for inflation, there is substantial FFO/share growth ahead for the sector.

The best positioned hotel REIT

Apple Hospitality is my pick in the sector due to a superior mix of fundamentals and value. A clean balance sheet and strong property mix have allowed it to outperform fundamentally and I think they can continue that momentum as the sector rebounds.

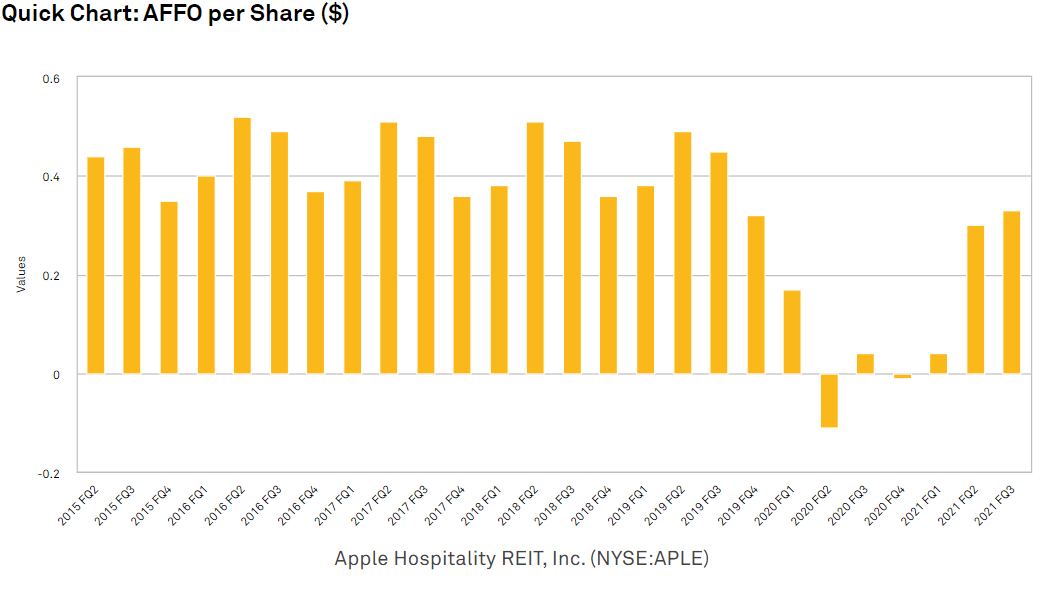

It suffered notably less distress through the pandemic, allowing it to come out in a much better position. APLE’s earnings only briefly dipped negative as measured by AFFO.

SNL financial

Compare the above chart to that of Pebblebrook (PEB) which is broadly considered to be among the strongest hotel REITs.

SNL Financial

I think one of the biggest mistakes hotel investors make is conflating luxury with quality.

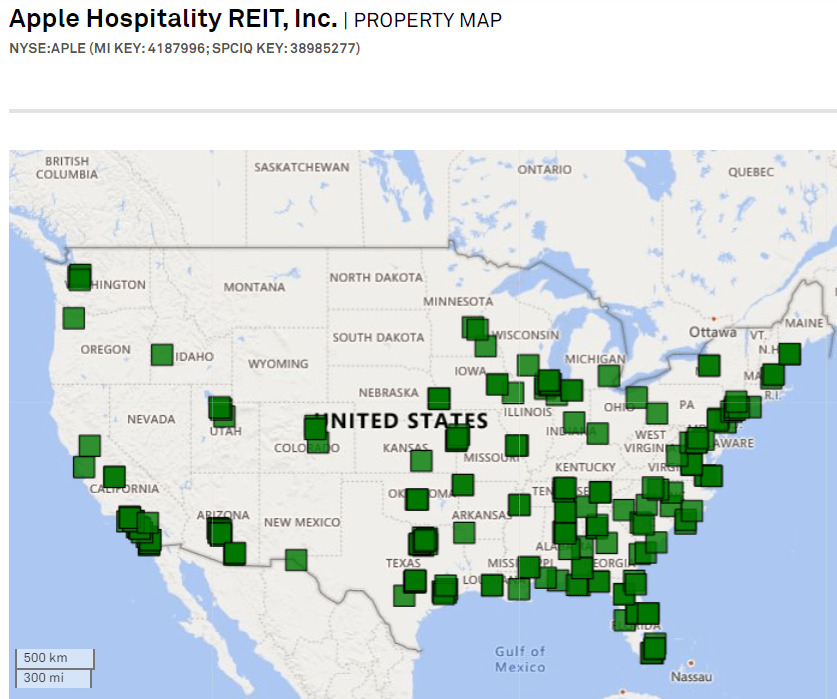

Higher room rate properties are glamorous, but not necessarily more profitable. APLE has significantly lower average RevPAR than peers and is spread throughout the country rather than concentrated in gateway markets.

SNL Financial

It also has a substantial exposure to extended stay hotels.

I like extended stay going forward because it fares better with high labor costs. The bulk of the cleaning requirements happen between guests, rather than during a guest’s stay. As such, longer lengths of stay are far more efficient for the hotel.

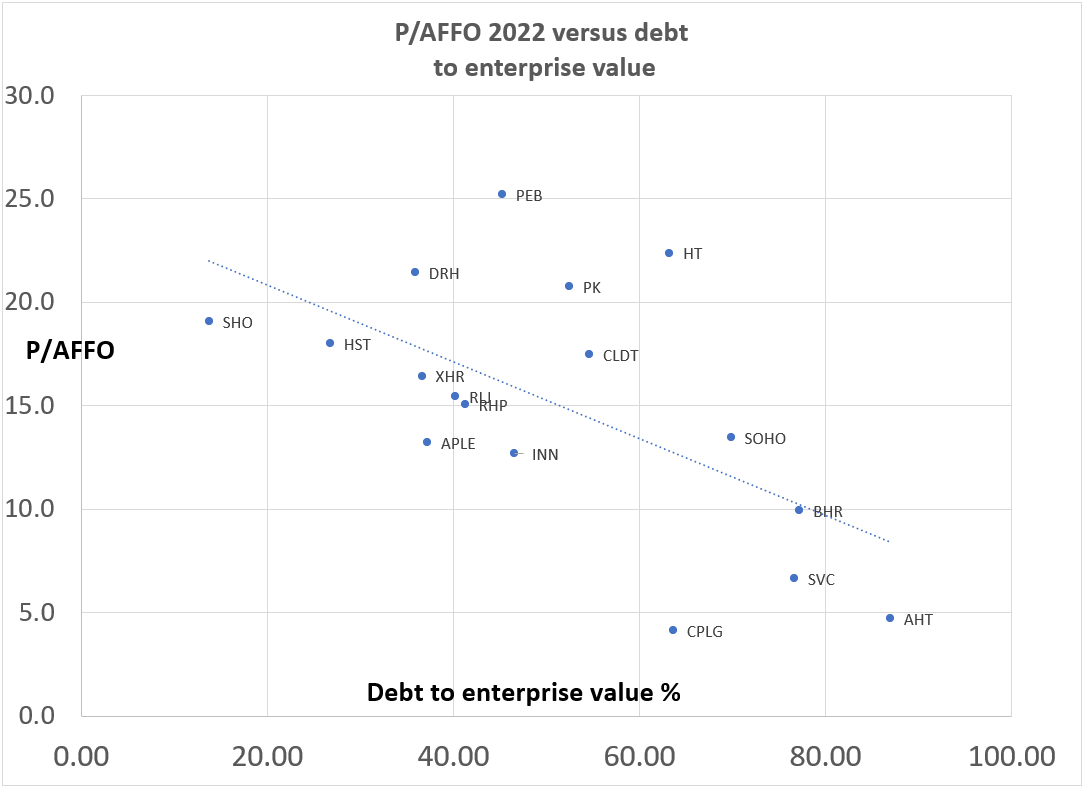

APLE is also one of the most attractively valued hotel REITs. Below I have plotted the price to AFFO multiple on the Y-axis and the Debt to EV on the X-axis.

Author generated using company data

Given the volatility in hotels, I think a low debt ratio is a must and the market seems to agree with a strong trendline correlation between low debt and high multiple.

The REITs falling below the trendline are better values with APLE having a great mix of both low debt and low AFFO multiple.

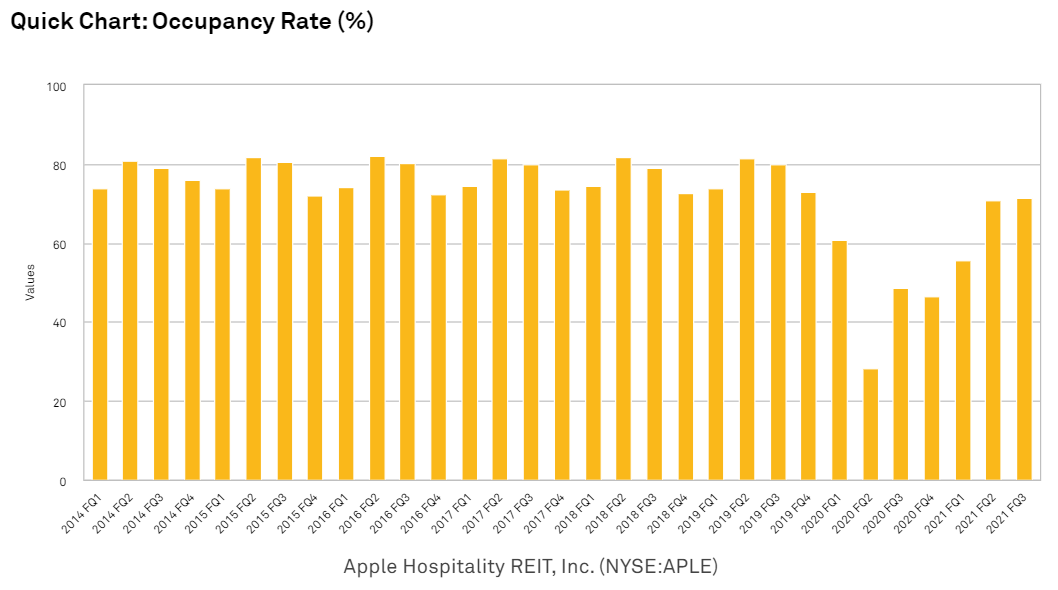

During the pandemic, hotel REITs were faced with a choice of whether to cut rate to keep occupancy or to keep rates up and lose occupancy. APLE largely chose to keep rates reasonably high and suffered on the occupancy front.

SNL financial

The advantage of this strategy is that it preserved their pricing power, allowing them to already bring rates back up to pre-pandemic levels.

SNL Financial

Assuming room demand returns to normal, there is about 10% upside remaining to occupancy. As occupancy grows, margins grow also since the fixed costs will not rise. Thus, a 10% increase to occupancy translates to significantly more than 10% in earnings.

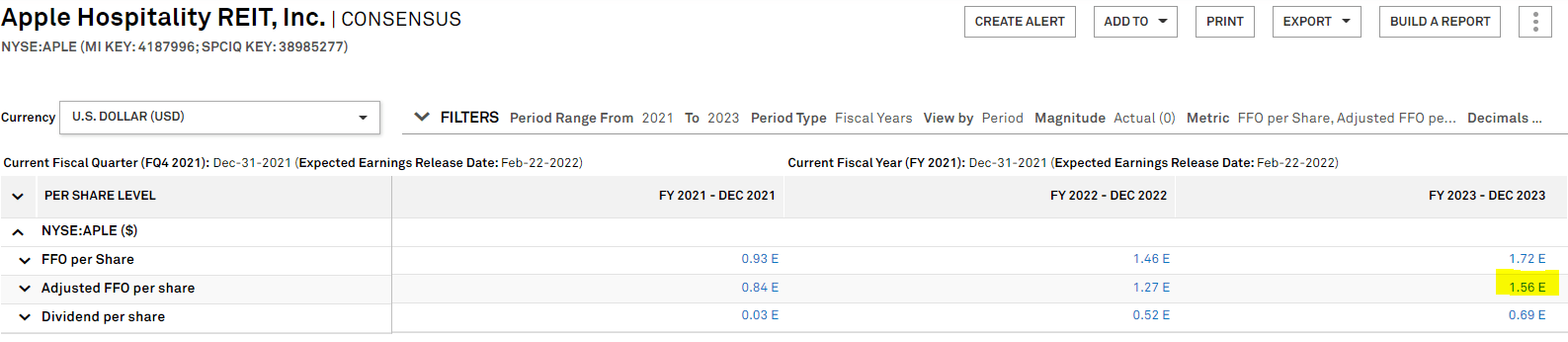

Consensus estimates call for AFFO/share growing to $1.56 by 2023.

SNL Financial

My hunch is that it will come in a bit south of this number, but it is still a low multiple against the sub $17 market price.

Wrapping it up

I remain generally bearish on the hotel sector, but APLE seems to be significantly better positioned than peers. If we assume no new variants surface and the travel restrictions ease, the pent-up demand along with restored tourism could make for a nice recovery play. I think APLE is the best way to play it.