iPhone 15 Pro and iPhone 16 Pro

Apple continues to gradually expand its direct iPhone sales to consumers, but most U.S. buyers still get their devices through carriers like Verizon, AT&T, and T-Mobile.

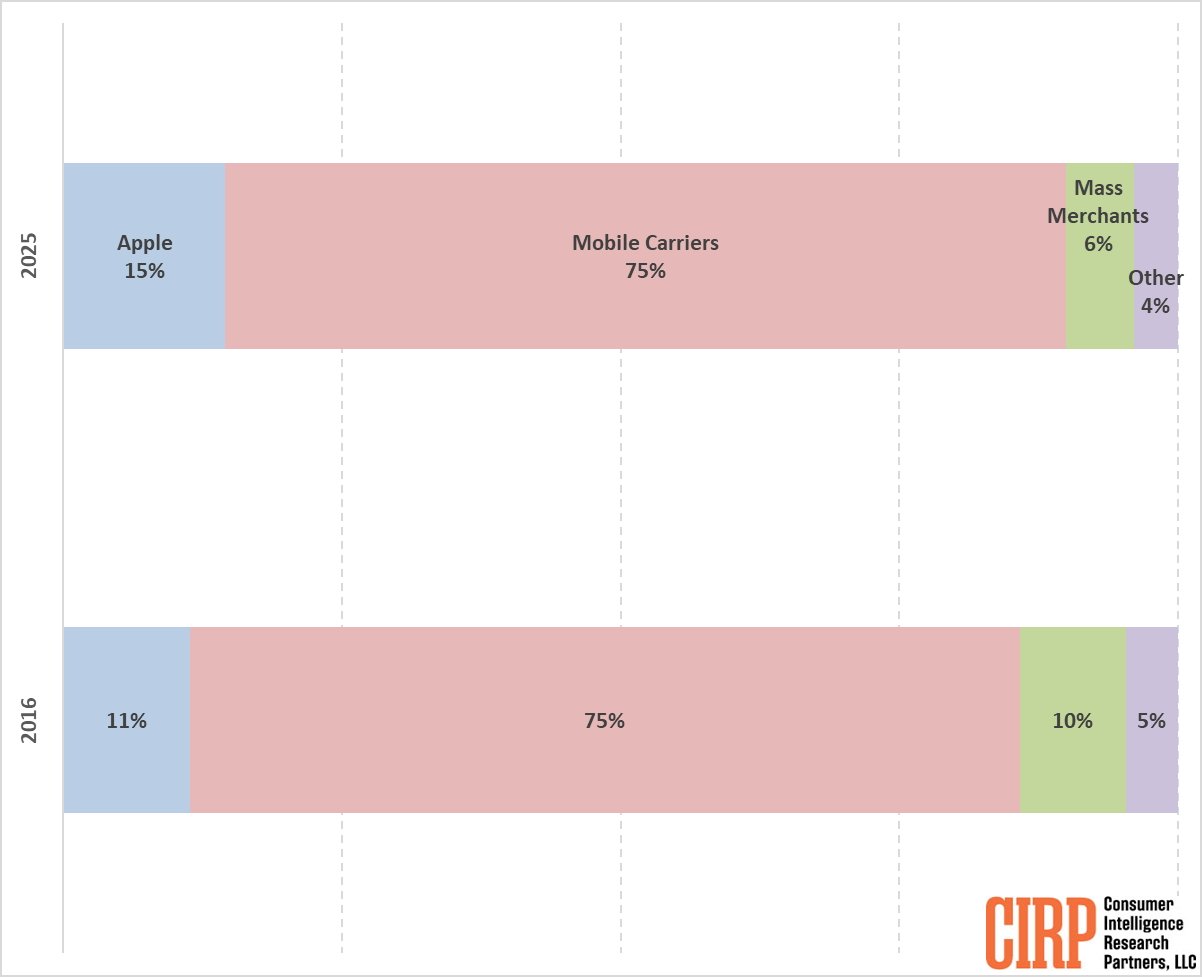

Mobile carriers including AT&T, Verizon, and T-Mobile accounted for 75% of iPhone sales in the U.S. as of late 2023, according to Consumer Intelligence Research Partners. Apple’s own retail stores and website made up 15%, with the remaining share held by big-box retailers like Best Buy and Target.

The balance has held steady for more than a decade. In 2015, carriers already claimed 75% of U.S. iPhone sales, while Apple’s share stood at 11%. Apple has crept up, but mostly gained share from third-party retailers, whose role in smartphone sales continues to shrink.

Carriers have long benefited from structural advantages. With thousands of locations and existing billing relationships, they make it easy for customers to finance phones as part of their monthly plans.

Trade-in deals, promotional pricing, and in-store availability give carriers powerful tools to drive upgrades and lock customers in.

Apple has steadily refined its direct-to-consumer efforts through the iPhone Upgrade Program and a streamlined online store. However, after ending zero-interest Apple Card financing for unlocked iPhones in 2023, its appeal to SIM-free buyers has narrowed

Instead, the company seems content to preserve its role as a premium sales channel while leveraging carriers for scale.

Low-cost iPhone 16e helps Apple grow share

Apple has gained momentum within those channels by offering more affordable iPhones. According to Counterpoint Research, Apple’s share of smartphone sales at the top three U.S. carriers rose from 70% in Q1 2024 to 72% in Q1 2025.

Breakdown of iPhone sales by retailer during each March quarter. Image credit: CIRP

That growth came during a period of overall market contraction. U.S. smartphone sales declined 2% year-over-year in the first quarter of 2025, with the premium segment falling even faster.

Apple’s new iPhone 16e, launched in February 2025, helped offset that downturn. Positioned as a lower-cost entry into the iPhone 16 lineup, the 16e starts at $599 and offers a modern design, A18 chip, and Apple Intelligence support.

Carriers have leaned heavily on the model in promotions, making it an appealing option for budget-conscious consumers delaying flagship upgrades. By broadening its lineup, Apple has kept customers in the iOS ecosystem, even as economic pressures push more buyers toward midrange devices.

Tariff strategy shifts retail dynamics

Newly enacted U.S. tariffs on China-made electronics are shaping retail behavior, influencing pricing and supply strategies. To avoid midyear price hikes, Apple and other smartphone makers have stockpiled U.S. inventory and increased alternate production, especially in India.

Apple’s retail and carrier partners may prioritize existing inventory in upcoming promotions. That could affect which models are most visible to buyers and how aggressively they’re priced.

While the approach helps Apple avoid short-term disruption, it also highlights its continued exposure to global supply volatility.

Apple balances reach & control

The company’s approach to iPhone distribution is one of strategic compromise. Carriers deliver volume and market coverage, while Apple retail offers high-margin experiences and brand reinforcement.

The division reduces conflict and lets Apple serve distinct customer segments without undermining its partners. Still, relying on carriers has drawbacks.

Apple continues to diversify its supply chain

Carrier marketing controls much of the upgrade narrative, and Apple has limited influence over how its devices are positioned. Financing plans through carriers often define upgrade cycles more than new features do.

Yet despite these limitations, the model continues to work. Apple not only maintained a dominant presence in the U.S. smartphone market, it also achieved the top global position in Q1 2025, capturing 19% of worldwide smartphone shipments.

As long as Apple maintains this momentum, it’s likely to continue its dual-channel strategy, which strikes a balance between retail expertise and carrier reach.