Sam Diephuis/DigitalVision via Getty Images

Part 1

Overvalued

For me personally, quarterly results are of less value compared to how these results affect the assessment of the company’s potential in the eyes of market participants. By and large, it is expectations that are important, not history.

One of the markers of such expectations are analysts’ forecasts. I treat these forecasts with a certain degree of skepticism, but if we consider them not selectively, then they are very useful.

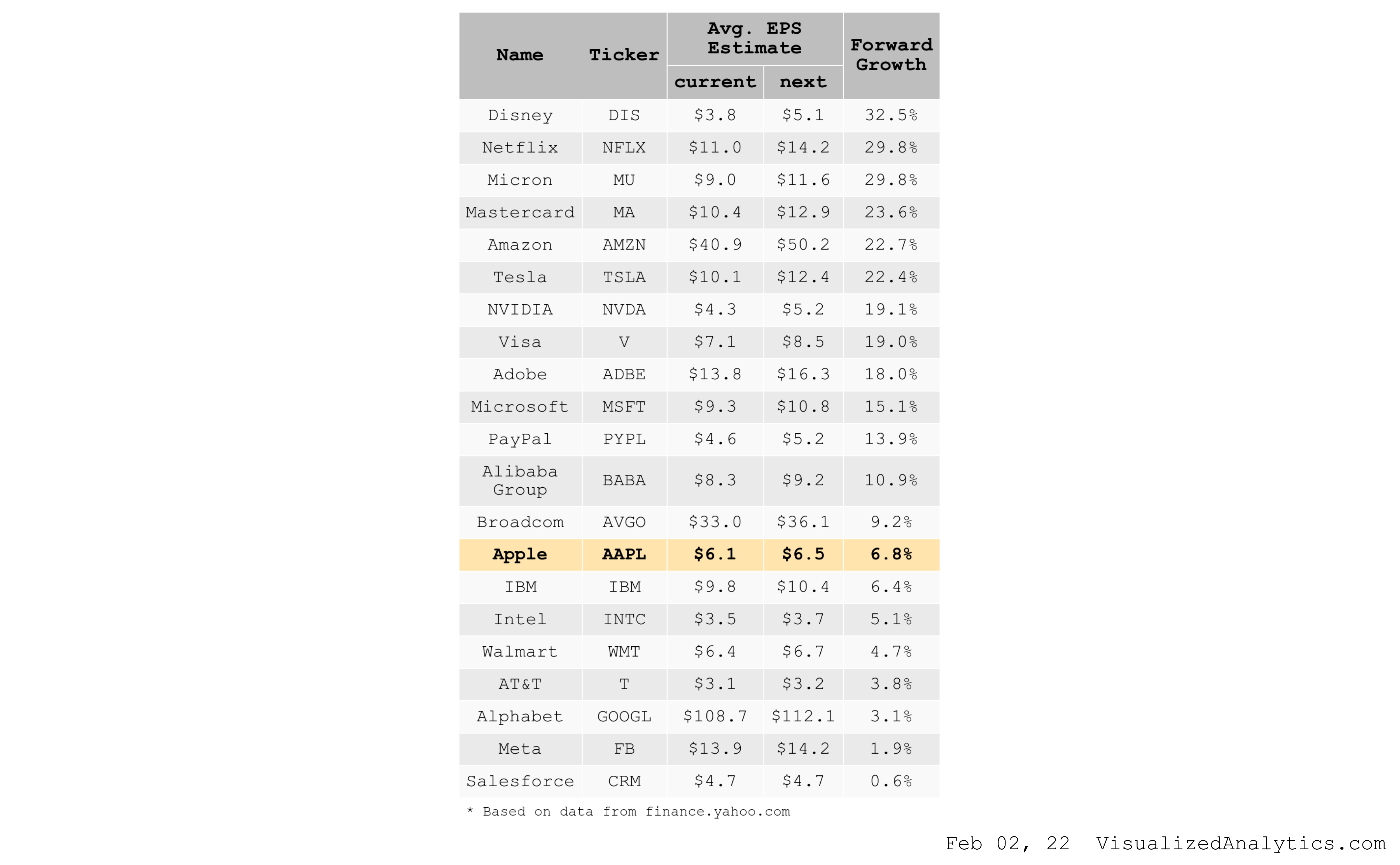

Apple (AAPL) subjectively showed good results for the past quarter, but the average analyst expectations suggest only a 5.6% increase in the company’s revenue in the coming fiscal year. This is close to what is expected from IBM (IBM) and Broadcom (AVGO). And this is even lower than the current inflation in the US. For example, Salesforce (CRM) revenue is expected to grow by 20%. So, Apple is nowhere near the top of the list:

VisualizedAnalytics

Expected earnings growth is somewhat higher but still very modest compared to other companies:

VisualizedAnalytics

So, the market does not expect rapid growth from Apple, either in qualitative or quantitative terms. And this directly affects the fundamental value of the company.

First, let’s look at the key multiples.

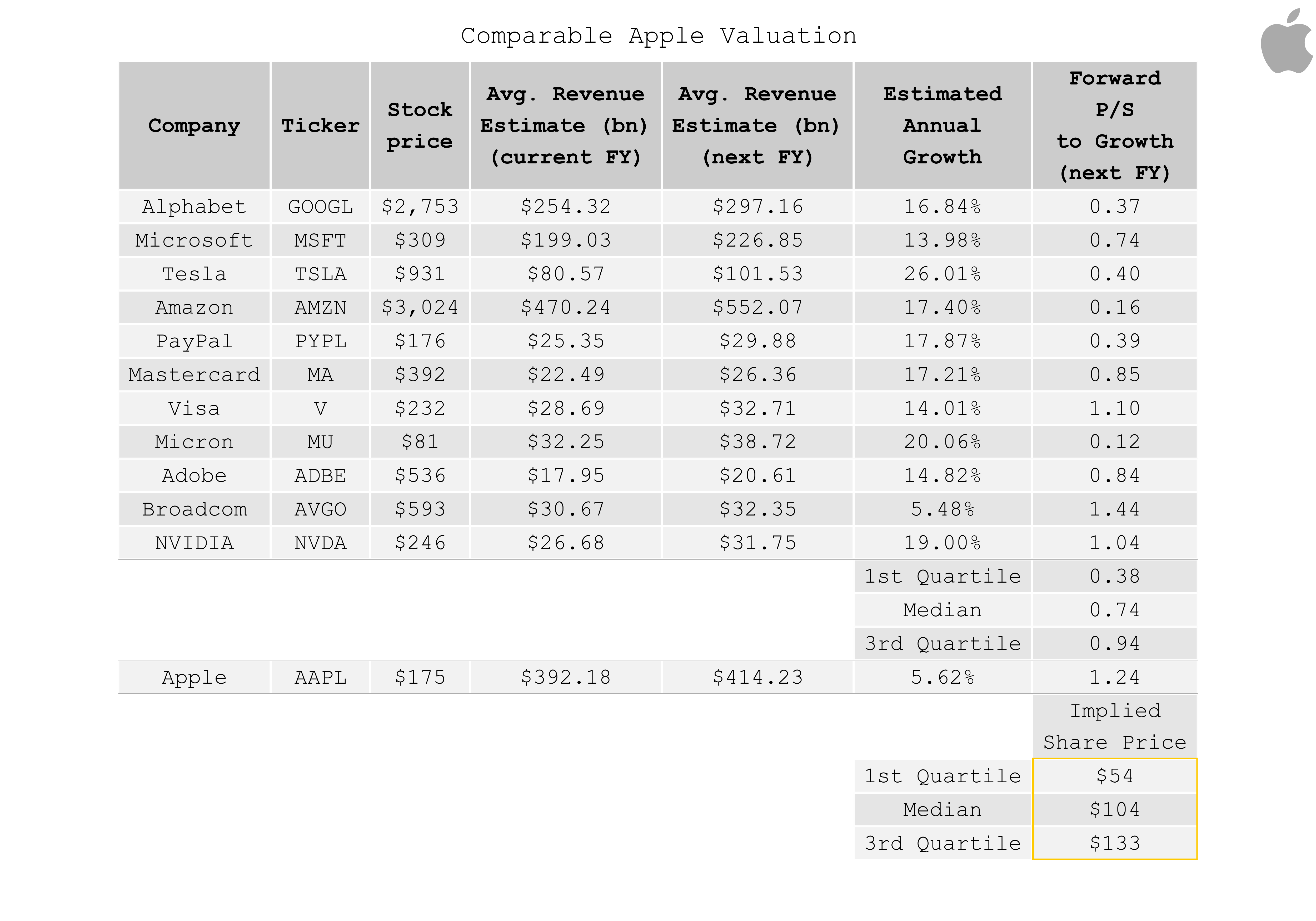

Multiples are very sensitive to the company’s life cycle. And the life cycle is usually reflected in the growth rate of the company. Therefore, it is reasonable to adjust multiples for growth rates before comparing.

This is what we get analyzing the P/S to growth (forward) multiple:

Author

Apple’s adjusted forward P/S multiple is х1.24, one of the highest in my sample.

This is what we get analyzing the growth of EPS, i.e. the P/E to growth (forward) multiple:

Author

This Apple’s multiple is also well above the median.

As you can see, Apple’s comparative valuation cannot justify the company’s current price when considering expected growth.

Now let’s look at Apple’s intrinsic value using DCF modeling.

I will not describe in detail the stages of building the model. I will only note that the revenue forecast was based on the average expectations of analysts. When forecasting the company’s operating margin, I also relied on analysts’ expectations of EPS growth and assuming that the company will continue the share buyback. The remaining parameters were averaged or extrapolated.

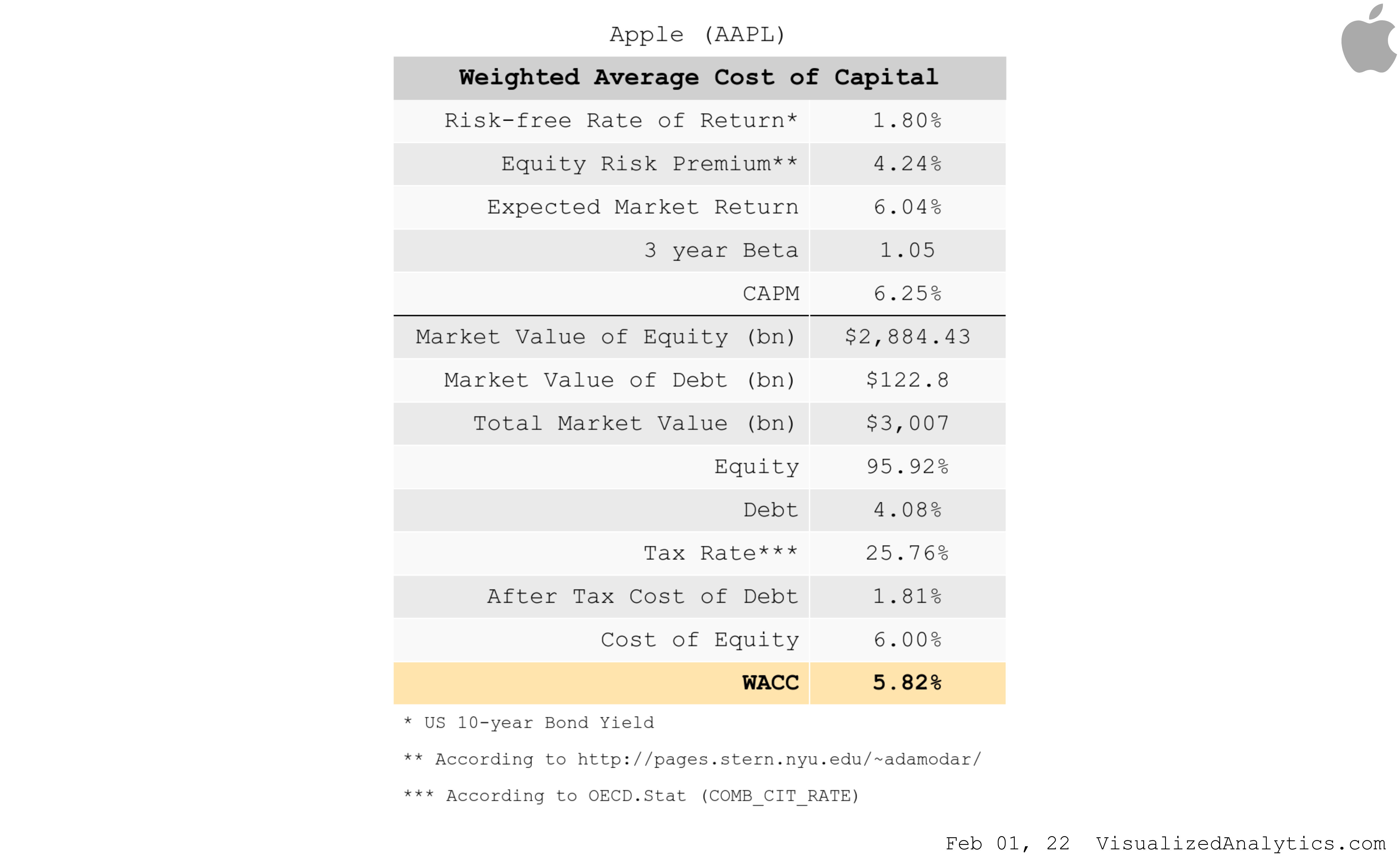

Here is the calculation of the Weighted Average Cost of Capital:

VisualizedAnalytics

And here is the model itself:

VisualizedAnalytics

This model shows Apple is overvalued by 5%. You can argue about the nuances, but the model does not exactly indicate that the company is undervalued.

Part 2

But Will Be Even More Overvalued

If you exclude romance from the process, then an investor buys shares in the hope that in the future there will be another investor who will agree to buy these shares more expensive. In the case of Apple, that other investor is the company itself.

Stable share buybacks are a kind of artificial deflation that steadily, without much regard for fundamental factors, increases the price of shares. And as long as this process continues, everything that I wrote about in the first part does not really matter:

It is necessary to distinguish between price and value. The price is the result of the balance between supply and demand in the market. And the value is a kind of modeled price based on fundamental internal and external factors:

Author

In theory, price tends to balance with value. But in practice, there are exceptions. And one exception is buybacks, which simply shift the stock supply curve to the left, which raises the balanced price.

In order to achieve its goal of net cash neutral, Apple will need to continue the share buyback. According to rough estimates, the company will continue to buy back shares for $80 billion annually over the next three years. This factor will ensure a stable excess of the price over the value.

Bottom Line

I believe that Apple is fundamentally not undervalued. But this does not prevent the company’s share price from rising to $200 in the next six months.