P. Kijsanayothin/iStock Unreleased via Getty Images

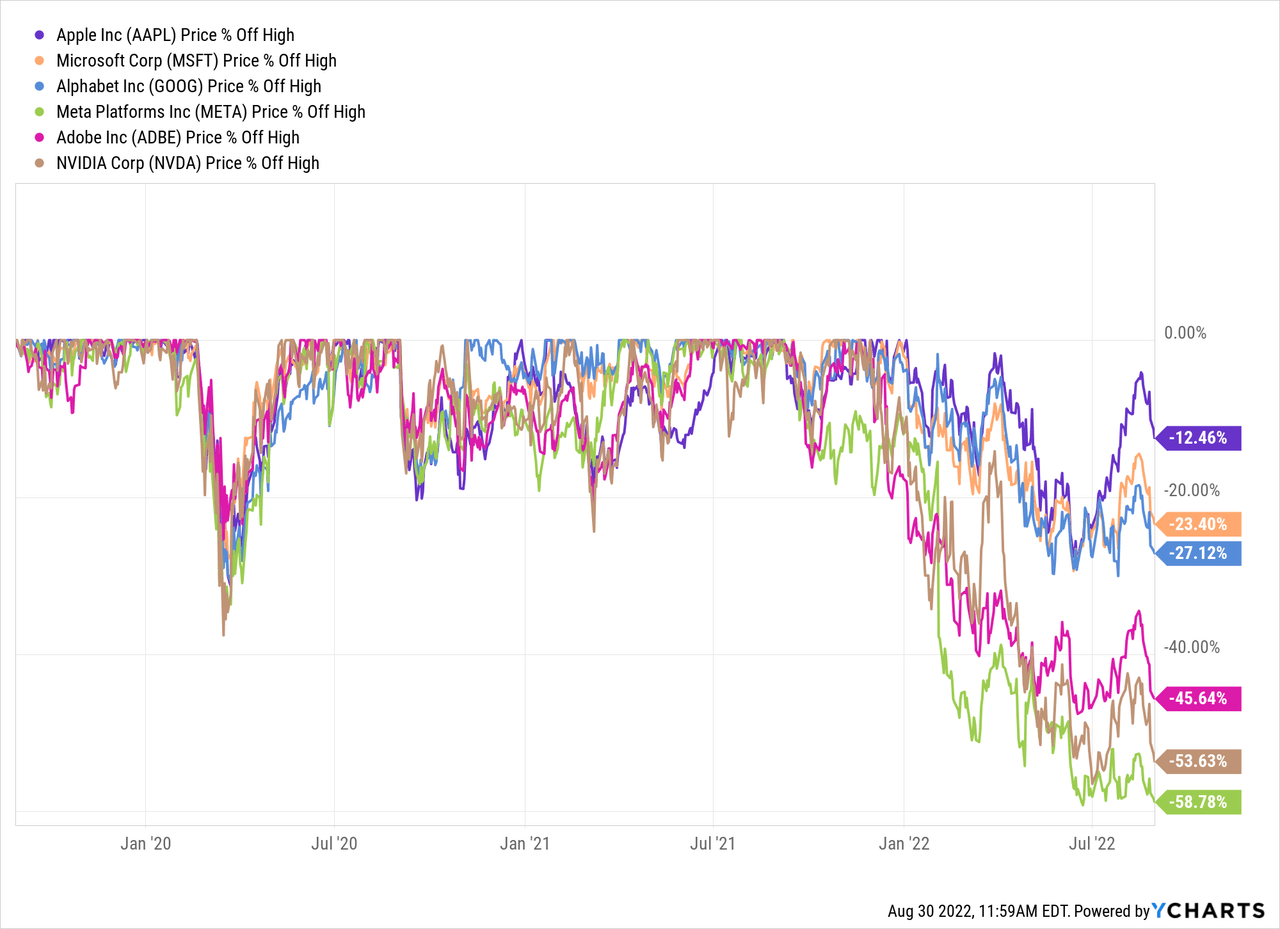

The U.S. stock market saw one of the steepest declines in the last few years. And especially many stocks from the technology sector declined extremely steep. When looking at the declines from the previous all-time highs, Microsoft (MSFT) declined 23%, Alphabet (GOOG) declined 27%, Adobe (ADBE) declined 46%, NVIDIA (NVDA) declined 54% and Meta Platforms (META) declined 59%.

Since I started writing this article several days ago, Apple’s (NASDAQ:AAPL) stock declined a bit – but it is surprising how close to its all-time high Apple is still trading. Right now, Apple is trading 12.5% below its previous all-time high and Apple is therefore one of the best performing major technology corporations and not really affected by the recent market sell-off. This is not only interesting and needs an explanation but might also be an example of investors ignore some risks. Apparently, investors assume that Apple doesn’t need a discount while most other technology stocks are trading much lower. In my opinion, Apple could (!) be overvalued and in the following article we explain why this could be the case.

Quarterly Results

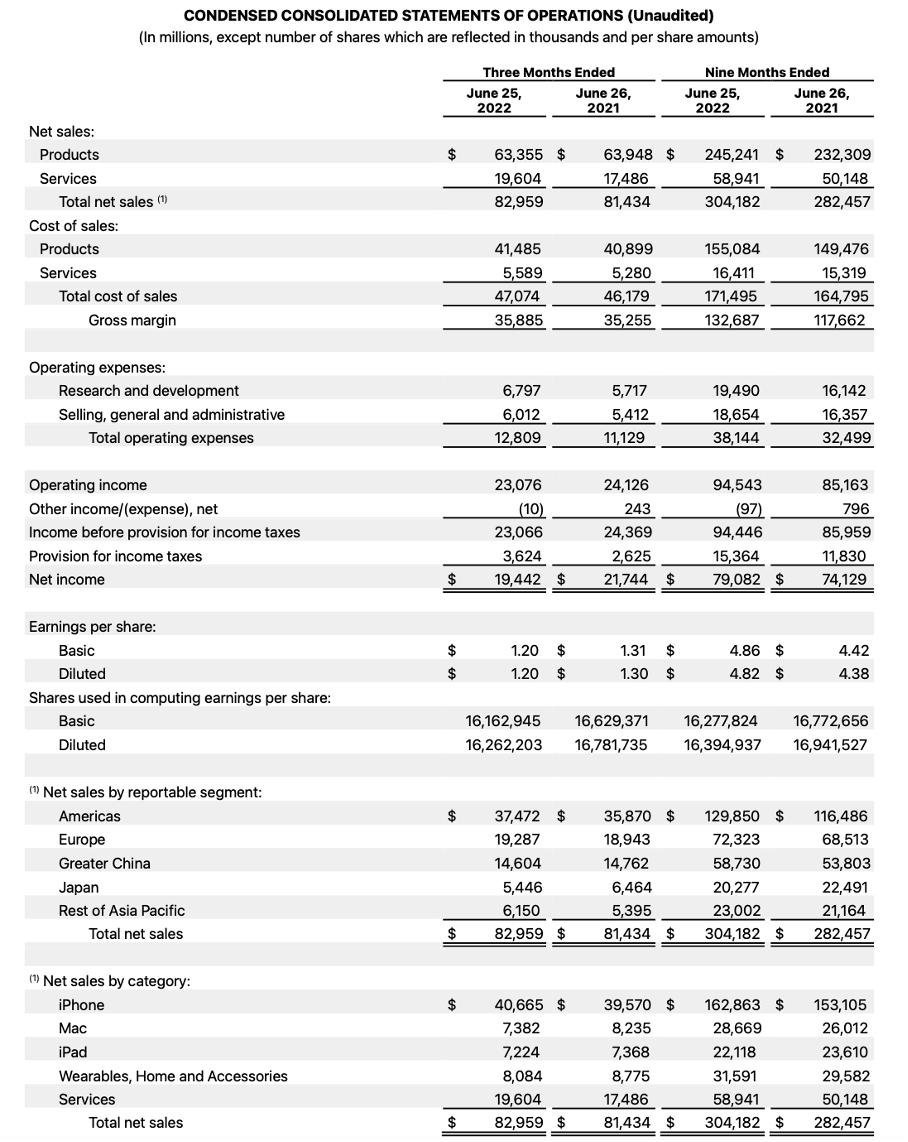

When looking for signs of weakness, third quarter results might be one piece of information. When looking at the top line, net revenue was $82,959 million in Q3/22 compared to $81,434 million in Q3/21 resulting in 1.9% year-over-year growth. And while service sales could still increase (12.1% year-over-year growth), product sales already declined (0.9% year-over-year decline). Operating income also declined 4.4% year-over-year from $24,126 million in the same quarter last year to $23,076 million this quarter. And finally, diluted earnings per share declined from $1.30 in Q3/21 to $1.20 in Q3/22 – a decline of 7.7% YoY (net income declined even a bit more, but the reduced number of outstanding shares could offset the decline a bit).

Apple Q2/22 Earnings Release

When looking at the net sales by category, service sales increased (as already mentioned above) and iPhone sales increased (2.8% year-over-year) but sales for Mac, iPad and “Wearables, Home and Accessories” declined.

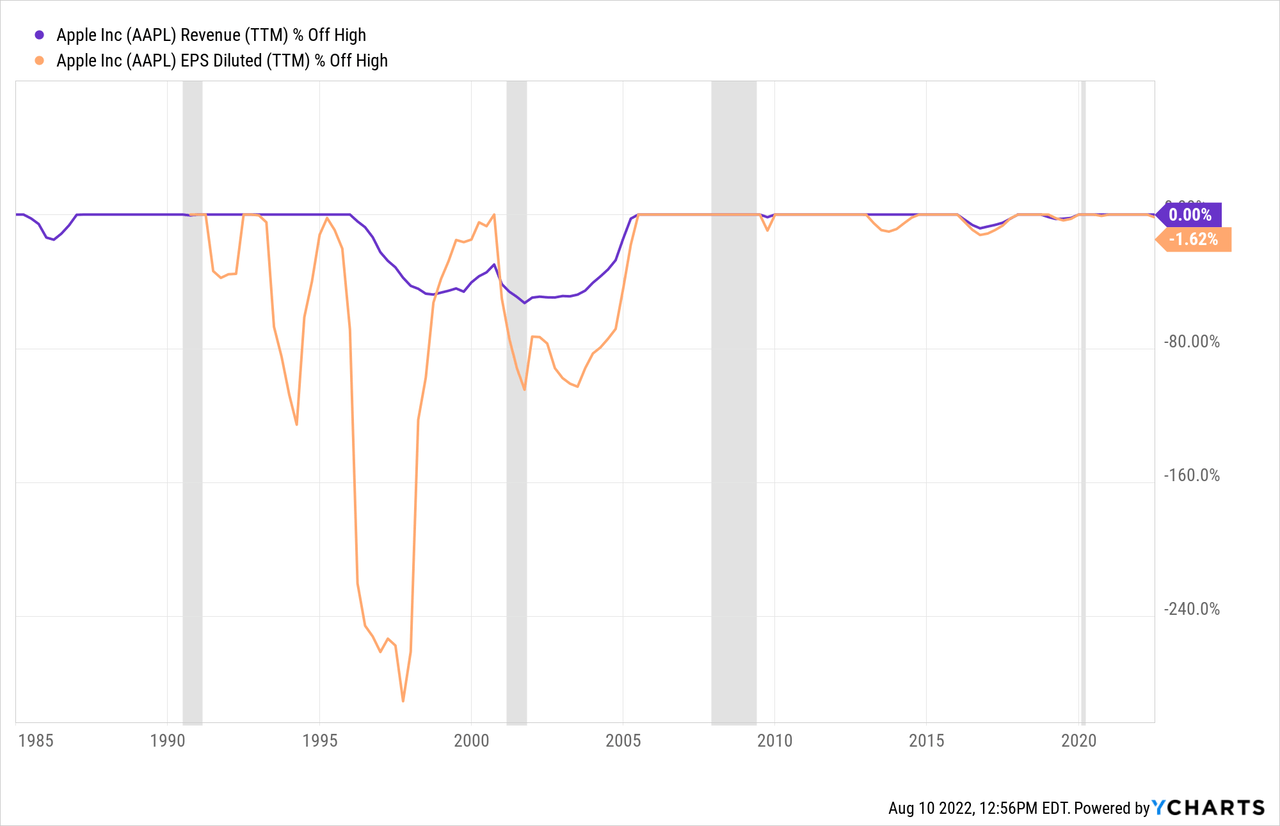

And when looking not only at one single quarter the picture is also not great. Similar to many other technology companies, growth rates are declining. Growth rates for revenue, gross profit, operating income, and earnings per share are now declining for five quarters in a row. However, Apple is trading close to its all-time high while most other huge technology corporations saw declining share prices in the last few months.

Recession

So far, we see declining growth rates, but also must keep in mind that growth rates in 2020 as well as 2021 were extremely high due to the pandemic and most technology companies profited. It is not surprising that most technology companies could not keep up the high growth rates.

But we also must talk about the risk of seeing further declines for Apple due to a potential recession. I have mentioned several times that I see the United States very close to a severe recession (and I am not the only one). When looking at past recessions, it does not seem like Apple is affected by a recession, but I don’t know if past results are a good indication for future results (especially in this case). During the Great Financial Crisis, Apple has just released its iPhone and started its impressive story of growing sales and increasing popularity of the iPhone.

In my opinion, Apple can’t repeat that success during the next recession and we will not only see declining iPhone sales, but sales for the iPad, the Mac, and wearables (like the Apple Watch) will decline even more. The iPhone is an important everyday item for many people. However, I would expect that during a recession a lot of people will postpone the purchase of a new iPhone for several quarters or maybe even one or two years. And as additional items like an Apple Watch or AirPods are even less important, purchases might be postponed even more (and longer). According to estimates, about 1 billion people have an iPhone worldwide and in 2021, Apple sold about 240 million iPhones meaning people are replacing the iPhone every four years on average. It is certainly possible to replace an iPhone only every 5 years (or switch to a cheaper alternative). And it is enough when 1/3 or ¼ of iPhone purchases are postponed for one year to have a severe negative impact on revenue.

While hardware sales will be affected, service sales might be more robust. In my last article I wrote:

Service sales are including revenue from the app store, Apple music, Apple Pay or Apple TV+ and these sales can be seen as more consistent than iPhone sales as we are dealing with subscription models, and this is leading to more consistent revenue streams. And it might also help iPhone sales to be more consistent. If I have paid for several apps, maybe use Apple Music (although there are many other similar providers to which I can switch) and have stored my data in Apple’s cloud, the incentive is much higher to buy an iPhone again to be able to use the services in a similar way.

The problem remains that product sales were responsible for 81% of total sales in fiscal 2021. Service sales might be more robust in a recession but with only 19% of total sales stemming from services, I still expect revenue to decline in case of a recession.

Apple vs. Meta

In the following section, I will focus on the competition of two major technology companies – Apple Inc. on the one side and Meta Platforms Inc. on the other side. It is not surprising to hear that these two corporations are in competition – a statement that has been true for years. But especially since Apple’s App Tracking Transparency Feature was released and had a huge negative impact on the ability of Facebook and Instagram to generate revenue, the two companies seem to have “irreconcilable differences”.

But this is not the main reason why Apple and Meta are in a deep philosophical competition – the main reason is the fight over the Metaverse. While Meta Platforms is rather focusing on virtual reality and its Oculus headsets, Apple is rather focusing on augmented reality. As augmented reality is using a real-world setting, the iPhone – which is already embedded in a real world setting by millions and millions of users – can easily be used to “access” the augmented reality. And this is probably a huge advantage for Apple compared to Meta Platforms. The iPhone is already in the hands of millions of users worldwide while Meta Platforms needs customers to buy the Oculus headset first. When looking at 2021 sales numbers, Apple sold about 240 million iPhones while Meta Platforms sold about 8.7 million Oculus devices. When Apple is rolling out AR features, million users might be able to take advantage right away while Meta Platforms first needs to convince people to buy an Oculus.

Right now, it might seem like Apple is the unchallenged leader in hardware and Meta Platform doesn’t stand a chance. However, it is worth pointing out that Nokia was also once the dominant leader in mobile phones and had a market share above 50% in 2007. This story is especially interesting as Nokia (NOK) was overthrown by Apple and although it seems unlikely (as it was unlikely in 2007), Apple might also be overthrown. In sectors that depend on constant innovation, it is extremely difficult to fight off competitors over several decades. And Meta Platforms certainly has the financial power to challenge Apple.

One could make the argument, that Zuckerberg (and Meta Platforms) doesn’t want to be just an app in somebody else’s app store (for example Apple’s app store). Meta Platforms wants to be the app store and have its own hardware, software, and ecosystem. And that is what the Metaverse vision of Zuckerberg is about. To achieve that goal, Meta Platforms must enforce a shift from the smartphone towards VR headsets. And I am aware that Buffett is considering Apple to be a great business with a wide economic moat. I argued in my last article that Apple is widening its moat, but there is only a weak moat around the iPhone. Apple’s moat is stemming from the apps, the app store, and the resulting switching costs.

And if virtual reality should succeed, Meta Platforms is in a good position. Although Oculus sold only 8.7 devices in 2021, 80% of all VR headsets were Oculus Quest 2 and Meta Platforms is therefore the dominant player in this market. It seems also possible that Apple and Meta Platforms will co-exist as augmented reality will be used in different ways than virtual reality.

Intrinsic Value Calculation

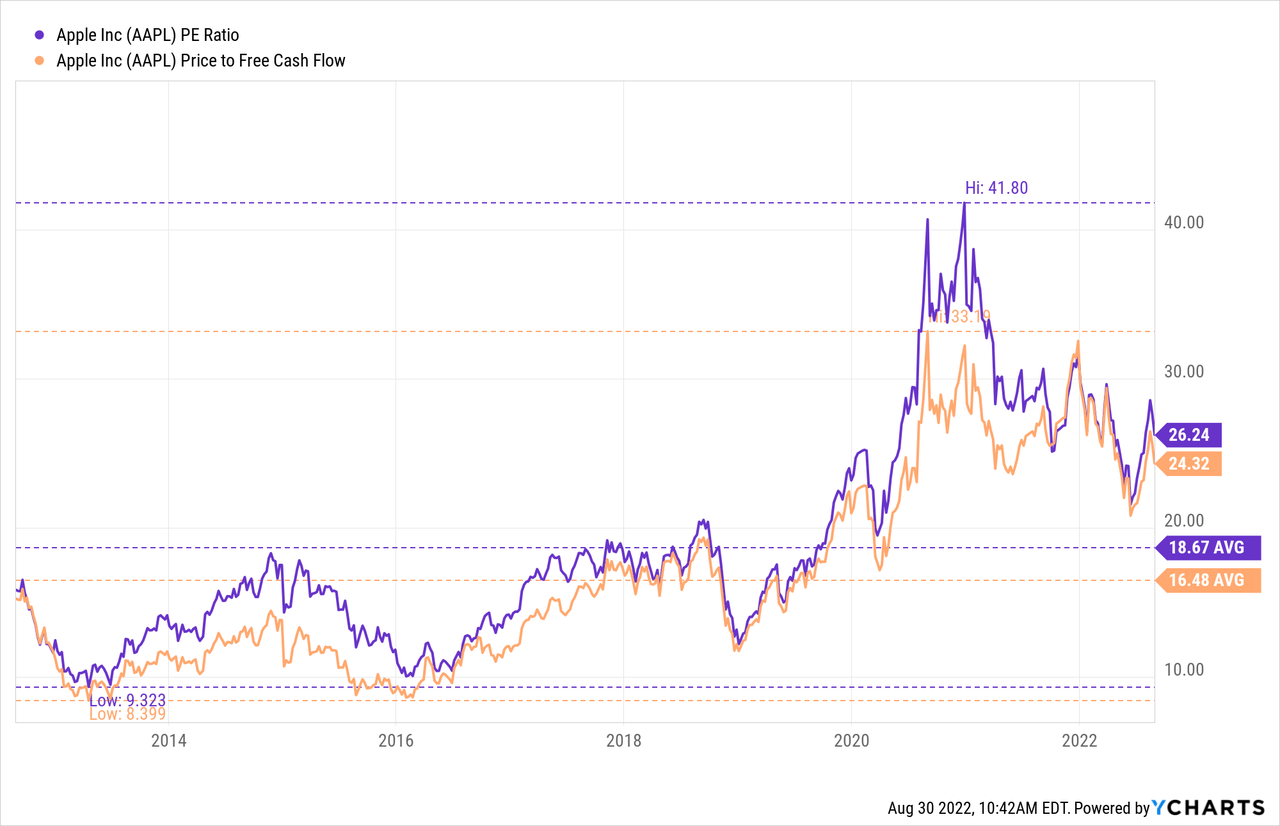

A final problem for Apple could be the rather high valuation, which is generating some downside potential – at least over the next few quarters. According to Seeking Alpha, Apple is extremely overvalued at this point. And we certainly can make the case that Apple’s stock is rather expensive. Not only is the stock clearly trading above its average P/E ratio and P/FCF ratio of the last ten years, but the stock is also trading for one of the higher valuation multiples of the last decade. This perspective is also based on the fact, that many big technology companies declined rather steep (as already mentioned above) while Apple is trading rather close to its all-time high.

But there is also a different perspective about Apple. When considering that Apple grew its earnings per share with a CAGR of 18.96% in the last ten years, with a CAGR of 21.98% in the last five years, and a CAGR of 23.51% in the last three years, we can easily make the argument that Apple is deserving a much higher valuation multiple. And we can also make the argument that Apple was undervalued in previous years when the stock was trading only for 10 to 20 times earnings (or free cash flow).

No Crystal Ball

In case of Apple, it all depends on the growth rates the company can achieve in the years to come and these growth rates depend on big consumer trends, shifts in technology and habits that are extremely difficult to predict. We all know the statements about the iPhone by Steve Ballmer in 2007 or the statement of Decca Records about “The Beatles” in 1962. But while it is easy to make fun of these people in retrospect, we must acknowledge it is extremely difficult to predict these trends and even more difficult to time these trends.

In retrospect, Nokia was extremely overvalued in 2007 as the risk of Apple inventing the iPhone was not reflected by the stock price. But on the other hand, who could have known. And now it’s the same with Apple. If a major shift should happen – and it is possible – Apple could be extremely overvalued because without the iPhone sales Apple is an entirely different company and might generate only a fraction of its revenue – as Nokia did a few years after the iPhone was introduced.

Conclusion

Apple is a difficult company to predict and make estimates. The company has no clear moat in my opinion but was nevertheless reporting phenomenal growth rates during the last 15 years. And analysts obviously had similar concerns about Apple (and probably difficulties to evaluate the stock), which might be part of the explanation why Apple was trading for such low valuation multiples despite high double digit growth rates.

We can argue that Apple is better prepared than Nokia in 2007. Apple is obviously focusing on the Metaverse for a similar long time as Meta Platforms (maybe even longer) and might be able to compete eye-to-eye with Meta Platforms if the shift towards virtual reality should happen suddenly. But we should not ignore the risk of the iPhone suddenly not being the technology everybody uses anymore.