Nikada/iStock Unreleased via Getty Images

Apple’s (AAPL) strategy to build a strong subscription business is facing new headwinds as competition increases in many services. Apple Music is facing higher competition from Amazon Music (AMZN) and YouTube Music (GOOG), which can lead to a fall in ranking within the streaming music industry. Apple TV+ is also showing poor subscriber additions with a very high churn rate. This is despite Apple gaining several award-winning shows and investing billions of dollars in this service. Higher investment in TV+ to gain subscribers will be one of the biggest drags for future earnings growth.

Poor subscriber additions have led to a massive correction in Netflix (NFLX) and Disney (DIS) stock. If Apple fails to impress Wall Street with its subscription strategy, we could see an increase in bearish sentiment towards the stock. The core issue within Apple’s lineup of subscription options is that it does not have an anchor service that acts as a must-have for customers. Amazon has built such a service in its core Prime membership, which has allowed the company to show over $30 billion in trailing twelve-month revenue within its subscription segment with a year-on-year growth of 30%. Investors should closely follow the subscriber additions of Apple to gauge the long-term potential of the stock.

Increase in competition

There has been a massive increase in competition in businesses where Apple offers subscription options. Apple Music is facing greater headwinds due to the growth of Amazon Music and YouTube Music. Both Amazon and Google have a strong base of smart speaker users which allows them to offer seamless service within the music streaming business. Google’s YouTube has been a particular surprise. It has rapidly gained over 50 million paid subscribers within its Premium and Music plan. This is quite high when compared to the last Apple Music subscriber base announcement of 60 million.

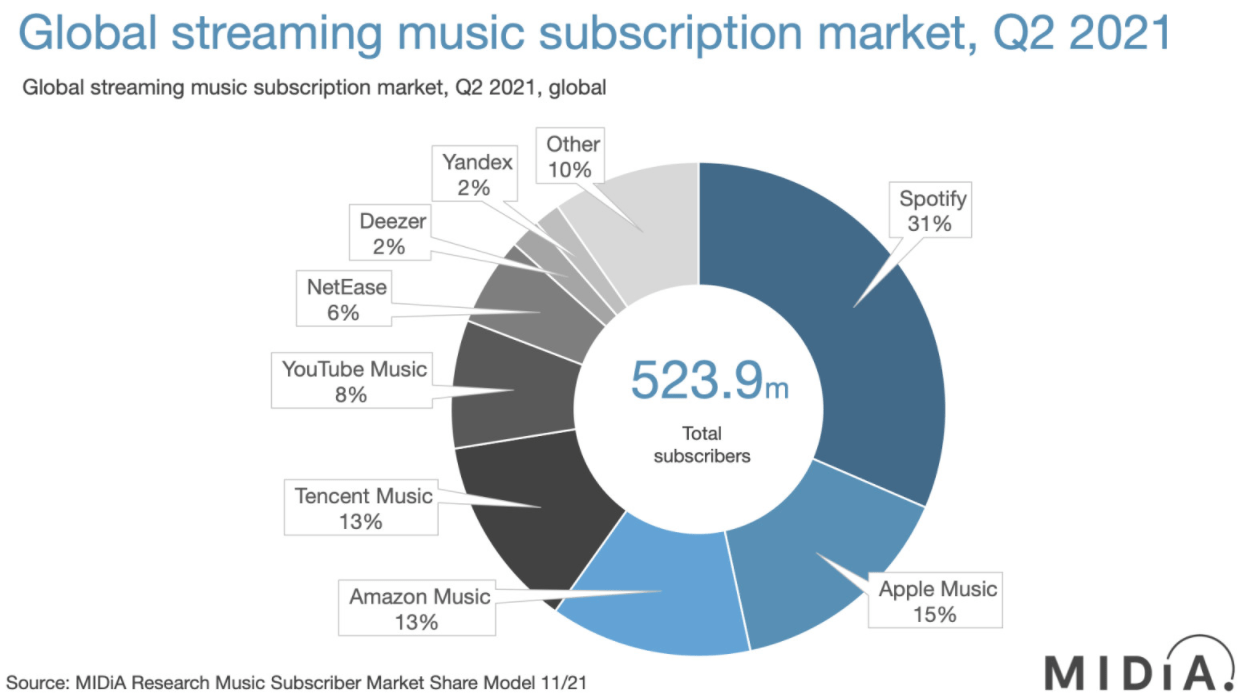

Figure 1: Apple Music is closely followed by Amazon Music and YouTube Music. (MIDiA Research)

A recent report from MIDiA Research shows that Apple Music had 15% paid subscribers in this industry while Amazon Music had 13% and YouTube Music has 8%. It would not be shocking if Amazon and Google overtake Apple Music by the end of 2023. A big change in streaming music rankings will be viewed as negative for Apple stock.

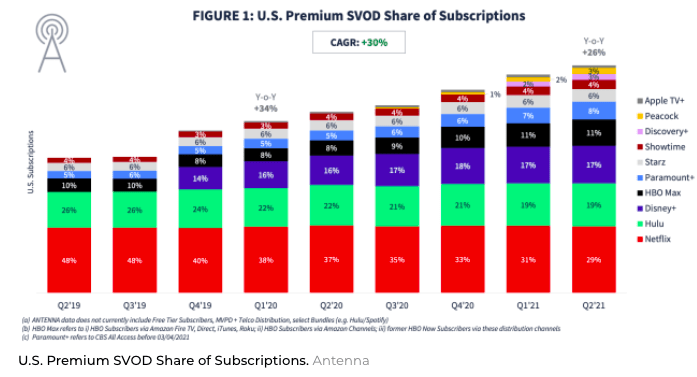

Apple TV+ is also facing challenges as the competition heats up in this space. Disney has announced annual investment of over $30 billion while Netflix has been investing over $15 billion in its content. Amazon had a content budget of $11 billion in 2020. Compared to this, Apple TV+ has an annual spend of $6.5 billion which is quite low. Despite delivering some good content, Apple TV+ has a very low subscriber base. According to Variety, the company mentioned recently that it had less than 20 million paid TV+ subscribers in US and Canada.

Figure 2: Apple’s slow progress in the SVOD industry. (Observer, Antenna)

No anchor service

Apple has added new services like Fitness+ to its subscription options. But without a strong anchor service, Apple would find it difficult to gain customers to its bundled One plan. Amazon has done an excellent job in building its Prime membership as an anchor service. It is now adding new services to this membership, which has helped in improving the subscription revenue over the last few quarters.

Figure 3: Amazon’s subscription revenue is over $30 billion in trailing twelve months. (Amazon Filings)

Amazon has recently announced another price hike for Prime membership in the U.S. and has also made a 50% price hike in India which shows the confidence of the management to retain its members despite higher prices. At the current growth rate, Amazon’s subscription revenue should cross $100 billion level by 2025. This will lead to an improvement in the company’s moat. Amazon could also end up increasing its investment in original content using subscription revenue which will create a flywheel effect for other services of the company.

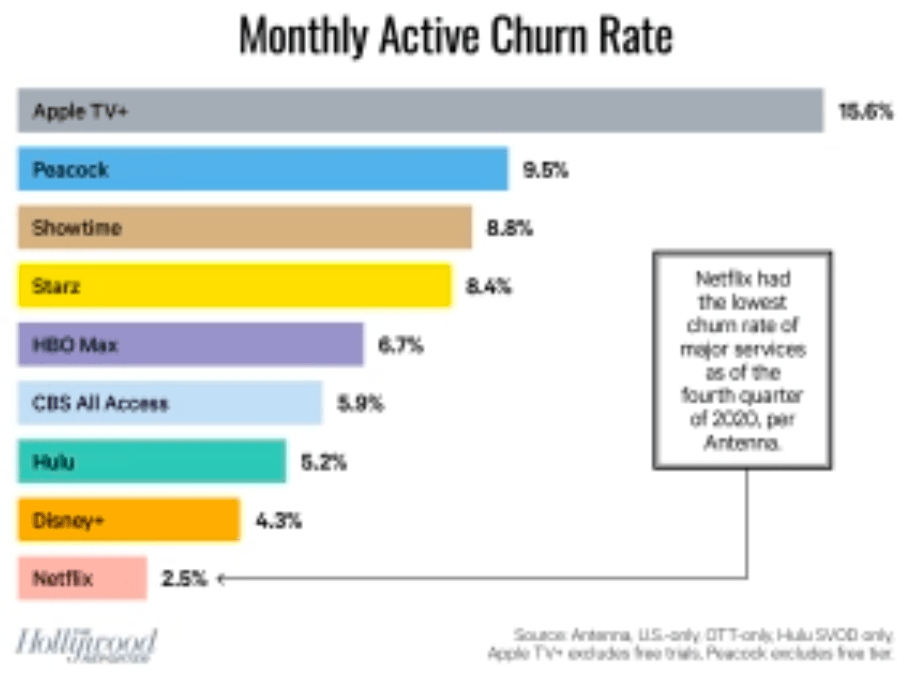

Figure 4: Apple TV+ has the highest churn rate in the industry. (Antenna, Hollywood Reporter)

Apple has a massive installed base of devices and has a lot of subscribers on its App Store. However, it would be difficult to move them to its own subscription services or the bundled option due to lack of an anchor service.

Money pit

It takes a long time to build a strong subscription business. Amazon has been investing in its logistics business to improve the value proposition for Prime users for over a decade. Disney and HBO have built subscription services with the help of their past original content investment. Apple is also making big investments which might hopefully lead to a better subscriber base in the future.

These investments are not peanuts even for Apple. It is spending close to $6 billion on streaming video, which is equal to 10% of its net income in fiscal 2020. We should see a ramp-up of investments in this space as the company tries to keep up with other competitors. It is possible that Apple spends as much as 20% of its net income on original content over the next few years. This will certainly drag down the earnings and put more pressure on management to show progress in the subscriber base.

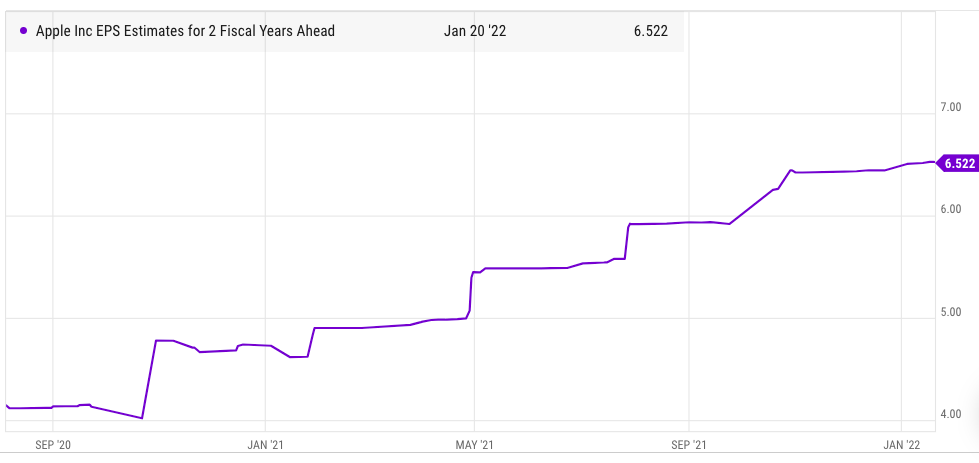

Figure 5: EPS estimates for two fiscal years ahead for Apple. (YCharts)

The EPS forecasts for Apple are still very strong, showing steady growth in the near term. However, any big spending jump in streaming video will be a headwind for net income and EPS growth. Apple is in a tight spot where it needs to show Services growth, which can only be achieved through good subscriber additions.

This requires heavy investment in TV+ over the next few quarters. Poor growth metrics or high churn rate will be taken as a big negative by Wall Street and could cause a bearish outlook towards the stock. Netflix and Disney have already seen a correction in their stock due to lower than expected subscriber additions. Investors need to pay close attention to Apple’s progress in TV+ and its overall subscription revenues to gauge the future direction of the Services segment and its stock.

Investor Takeaway

Apple is facing increasing competition within its subscription services of music and video streaming. The company is making massive investments in this segment. If this does not result in good subscriber numbers, we could see a negative sentiment towards the stock. Apple does not have an anchor service through which it can build a strong bundled subscription platform. This will remain a major hurdle for the company in the next few years.

The investment rate in streaming video can also lead to a dip in net income and EPS which would hurt the stock as it is already trading at close to its highest P/E ratio.