Nikada/iStock Unreleased via Getty Images

Apple (NASDAQ:AAPL) and Alphabet (GOOG) (GOOGL) have a close working relationship due to their licensing agreement. However, they are also involved in an epic battle due to the rapid growth of Google’s products and services in business segments where Apple is the leader. Google has already proved its mettle in the smart speaker segment where it is in the second spot behind Amazon. Apple is lagging in this business despite trying to increase market share for a number of years.

Apple has provided free TV+ service to incentivize customers to upgrade their devices. Google also has its YouTube Premium services which has over 50 million paid subscribers and is showing the fastest growth rate in that industry. The launch of Pixel Pass gives Google a significant edge over Apple as it combines YouTube Premium, YouTube Music Premium, Google One, and other services along with a new Pixel phone at a modest price of $45/month. Investors should closely look at the changing dynamics within the smartphone industry and Google’s future ambitions to gauge the returns potential in Apple stock.

Licensing deal between Apple and Google

According to WSJ, the licensing deal between Apple and Google is now worth over $10 billion annually. It was less than $1 billion in 2014. This revenue stream is probably pure profits for Apple because it is merely selling the real estate on its devices for Google’s apps. This deal is also in the regulatory crosshairs because it gives Google a strong competitive edge over other players in the same field.

Apple has over a billion devices and Google needs access to these devices in order to maintain its hold over the Search market and other major services. However, the massive payment from Google is a major headwind for its margins. As a result, Google has tried to increase its own product sales. Google has done a great job in building a strong smart home devices business. Its smart speakers are placed in the second spot, just behind Amazon (AMZN). Apple has not been able to make much headway in this industry and has finally decided to sell a budget HomePod Mini.

Apple’s biggest headache

Google has recently given orders to double the production of its Pixel devices. This will take the production volume of these devices to close to 10 million. However, this scale is still lower than Apple which sells over 200 million units of iPhones every year. But Google has a major ace up its sleeves. Apple is trying to push more customers to upgrade their iPhones by offering free TV+ subscription. This will also increase the long-term loyalty of customers and allow the company to monetize its massive userbase.

Google has over 50 million YouTube Premium paid customer base. The growth rate of this service is very high. At the current growth trends, it is possible that YouTube Premium could surpass 200 million subscribers by 2025. Google has also launched its combo subscription offer of Pixel Pass which gives users a new phone plus other services at a low monthly subscription price.

The details of the licensing deal between Google and Apple are not completely known to the public. However, it is likely that Google’s payment is linked to the usage of its services on Apple devices. If Google’s own Pixel userbase increases, it would reduce the payments to Apple. Hence, Google has a very high motivation to ramp up its smartphone sales, even if there are short-term losses in this segment.

CIRP, Geekwire

Figure: Poor growth trajectory of Apple’s smart speakers compared to market leaders Google and Amazon. Source: CIRP, Geekwire

The rapid growth of Google devices will increase competitive pressure on Apple and limit the pricing leverage that it enjoys. We have already seen this in the smart speaker segment. Apple had to close the production of HomePod as it was deemed too expensive compared to good alternatives by Google and Amazon. Finally, Apple had to launch HomePod mini at a price close to Google’s own devices.

Branding and resources

The biggest moat for Apple in the last few years has been its brand image which is associated with premium products. This has allowed the company to take market share in key segments despite being a latecomer. Even Samsung has struggled against Apple despite having the first-mover advantage in several product categories. However, the gap in the perceived brand image of Google and Apple is likely to be very small. Apple’s failure in building a good market share for HomePod against Google’s smart speaker shows the strength of Google’s brand image and its product quality.

Google has a significant cash pile and massive free cash flows. This reduces any advantage Apple has due to its own massive resources. Google has been launching budget smartphones for the past few cycles. It is possible that Google would give a better deal within its Pixel Pass subscription to gain new subscribers and smartphone users. Google can easily absorb losses in order to build a more robust product segment. This will put pressure on Apple within the lower-priced versions of iPhones.

Impact on Apple stock

The smartphone industry has been saturated. The specifications within the flagship devices of most 5G smartphone makers are also not very different. In this scenario, the biggest differentiating factor would be the services attached to these devices. If Google shows massive growth in YouTube Premium and provides a more attractive combo deal of this subscription with Pixel and other devices, it will be a major advantage for the company.

Apple is trying to increase paid subscriptions to its own TV+ service but they are still less than 20 million despite being the cheapest option in this industry. Google has the resources and branding power to gain a massive following for its products and services. This can become a major headwind for Apple over the next few quarters as the company tries to improve the Services segment.

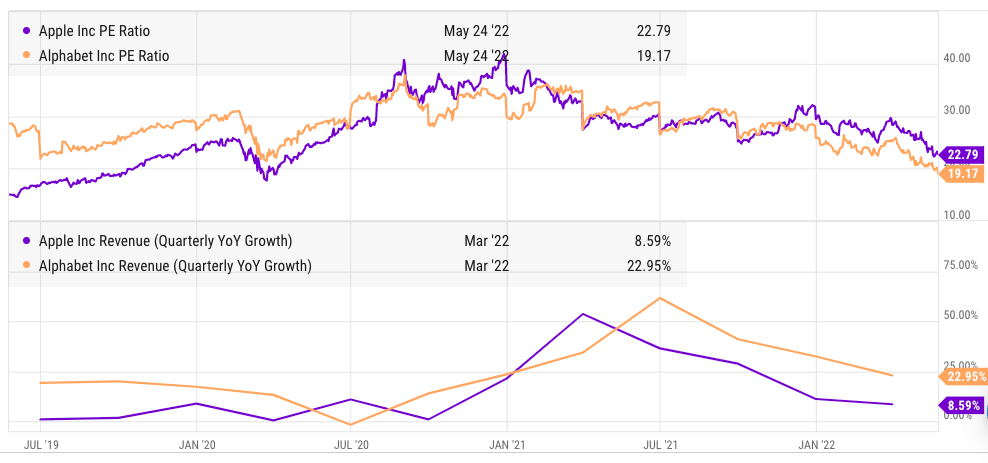

Ycharts

Figure: Apple is trading at a premium compared to Google despite lower revenue growth. Source: Ycharts

After the recent correction, Apple’s PE ratio has dropped to 22. However, it is still significantly above the average PE ratio of 15 during the last decade. Apple is also trading at a premium to Google despite lower revenue growth. Google is in a perfect spot to take advantage of the changing dynamics within the smartphone industry by increasing subscriptions on YouTube and giving more attractive combo deals through Pixel Pass. This will be a major headwind for the future growth trajectory of Apple in the smartphone category and many other products and services which the company hopes to launch in the next few quarters.

This challenge has not been priced in the current stock price of Apple and we could see lower returns from Apple stock if Google is successful in building a strong hardware and subscription business.

Investor Takeaway

Apple is the undisputed leader in smartphone industry with a very strong ecosystem. However, the dynamics of this industry are changing as more importance is given to services. Google is becoming the biggest competitor of Apple and has already announced a production target of close to 10 million units of Pixel devices. Google also has a rapidly growing YouTube Premium subscription with over 50 million paid users. If Google provides a more attractive combo deal of Pixel devices and YouTube Premium subscription, it will increase the attraction of the smartphone lineup and YouTube subscription.

Strong competition from Google can increase the headwinds for Apple’s iPhone and smart device segment. It can also limit the growth within the licensing deal which is one of the most lucrative revenue streams for the company. Investors need to price in the changing market dynamics to gauge the long-term potential of Apple stock.

")