Justin Sullivan/Getty Images News

As predicted and denied by most Apple (NASDAQ:AAPL) bulls, the tech giant reported a rather weak FQ3’22 earnings report last week. Revenues were near the weakest in the tech giant space and crucial Mac revenue actually declined YoY. My investment thesis remains Bearish on the stock, as the stretched valuation only grows with the recent rally back above $160.

Beats Aren’t Enough

One of the biggest problems facing Intel (INTC) shareholders was the focus on the quarterly earnings beats while ignoring the otherwise weak results. The chip market finally fell apart and the chip giant ended up reporting a horrible quarter causing the stock to collapse.

While Apple has reported some strong quarters, the market appears to have completely ignored that the June quarter revenues only grew by 1.9%. The headlines appear to paint a far better quarter than the reality.

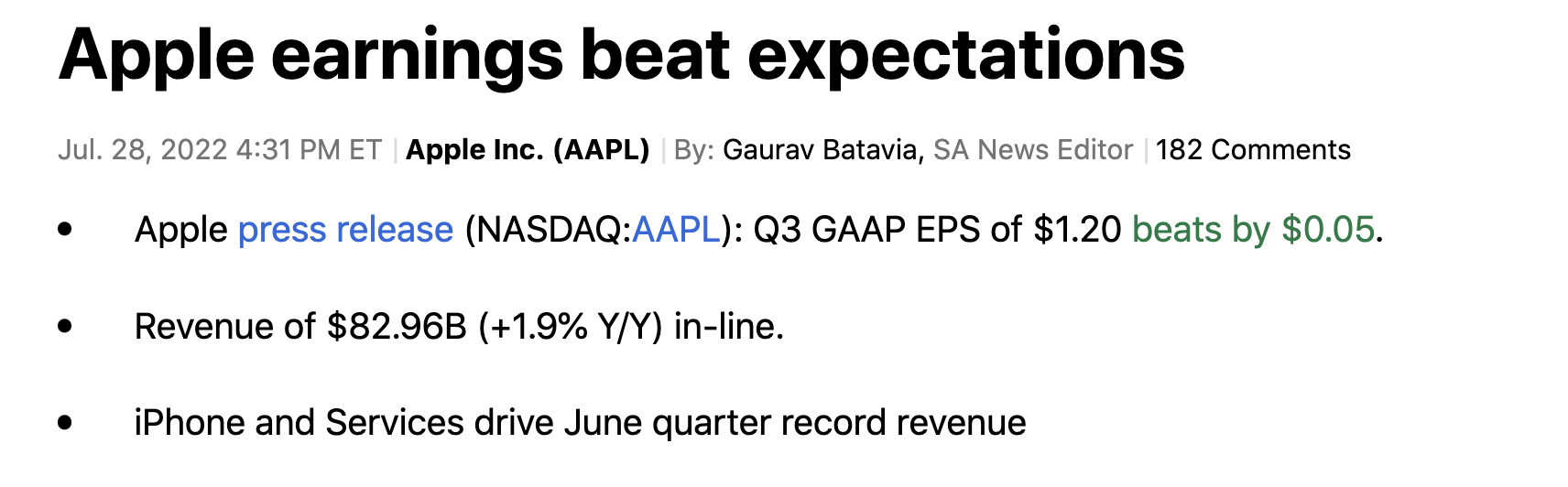

Source: Seeking Alpha

The tech giant beat EPS estimates by $0.05, but in general the numbers weren’t impressive. Over the last decade, Apple has generally reported as many quarters similar to the low growth in FQ3’22 as those in the boom times where revenue growth exceeded 10%.

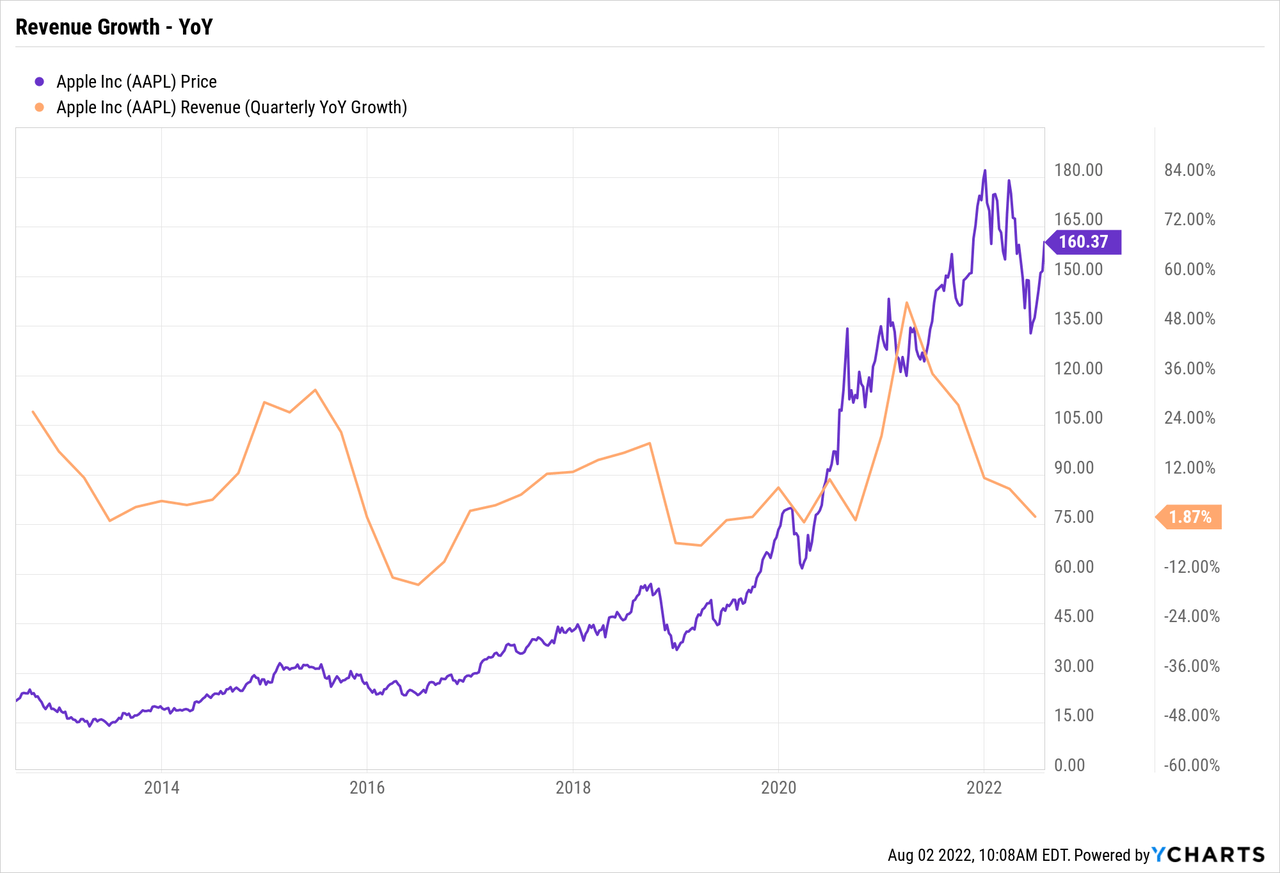

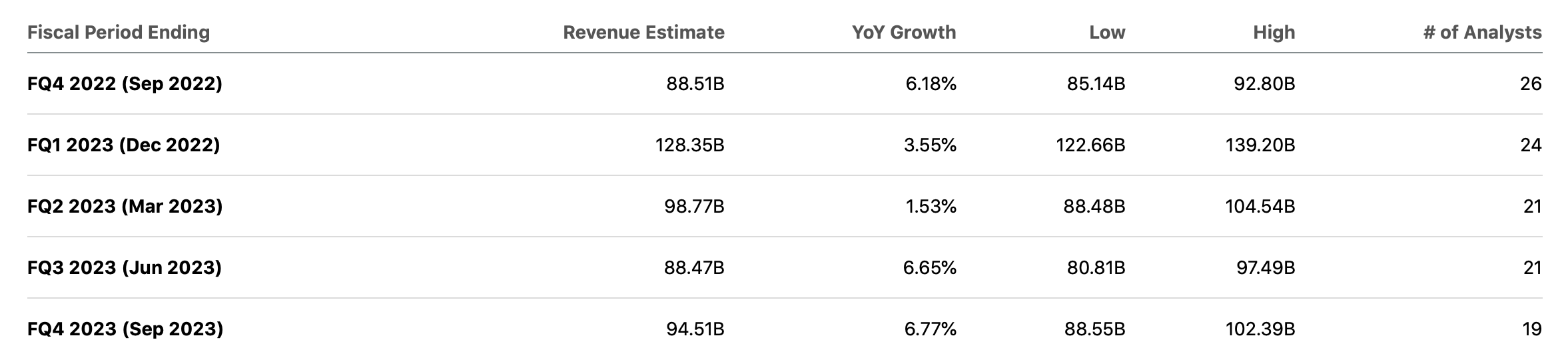

A few days after a quarterly report, an investor should start reviewing the updated analyst estimates to see how the numbers and management comments on the earnings call shaped future forecasts. Over the next few quarters, analysts again predict a period where revenue growth sees significant struggles.

Source: Seeking Alpha

The highest forecasted growth rate doesn’t top 7% through the end of FY23 next September. Apple is forecast to see 2 quarters where revenue growth doesn’t top 4%. After the tech giant just reported a quarter with revenues inline with analyst estimates at 1.9% growth, investors should start to see these numbers as solid. The period of smashing analyst targets during covid is officially over.

During the quarter, Apple saw Mac revenues decline YoY due in part to supply chain issues, but also due to strong covid pull forwards. The company got hit by the same problems as other tech companies where the massive growth from 2021 makes for tough comps in 2022.

Mac revenues for the quarter were $7.4 billion, down 10% from last FQ3. The new M1 and now M2 chips provide the potential for an extra boost in Mac sales, but the product has long struggled to gain much traction due to price and enterprises entrenched with PCs. The FQ3’22 revenues bring Mac sales right back to the same level reached in FQ1’19.

Source: SixColors

Due to the limited growth reported in the quarter, CFO Luca Maestri even felt the pressure to comfort shareholders with statements on the FQ3’22 earnings call to promote higher growth rates in future quarters:

Overall, we believe our year-over-year revenue growth will accelerate during the September quarter compared to the June quarter despite approximately 600 basis points of negative year-over-year impact from foreign exchange. On the product side, we expect supply constraints to be lower than what we experienced during the June quarter.

Priced For Perfection

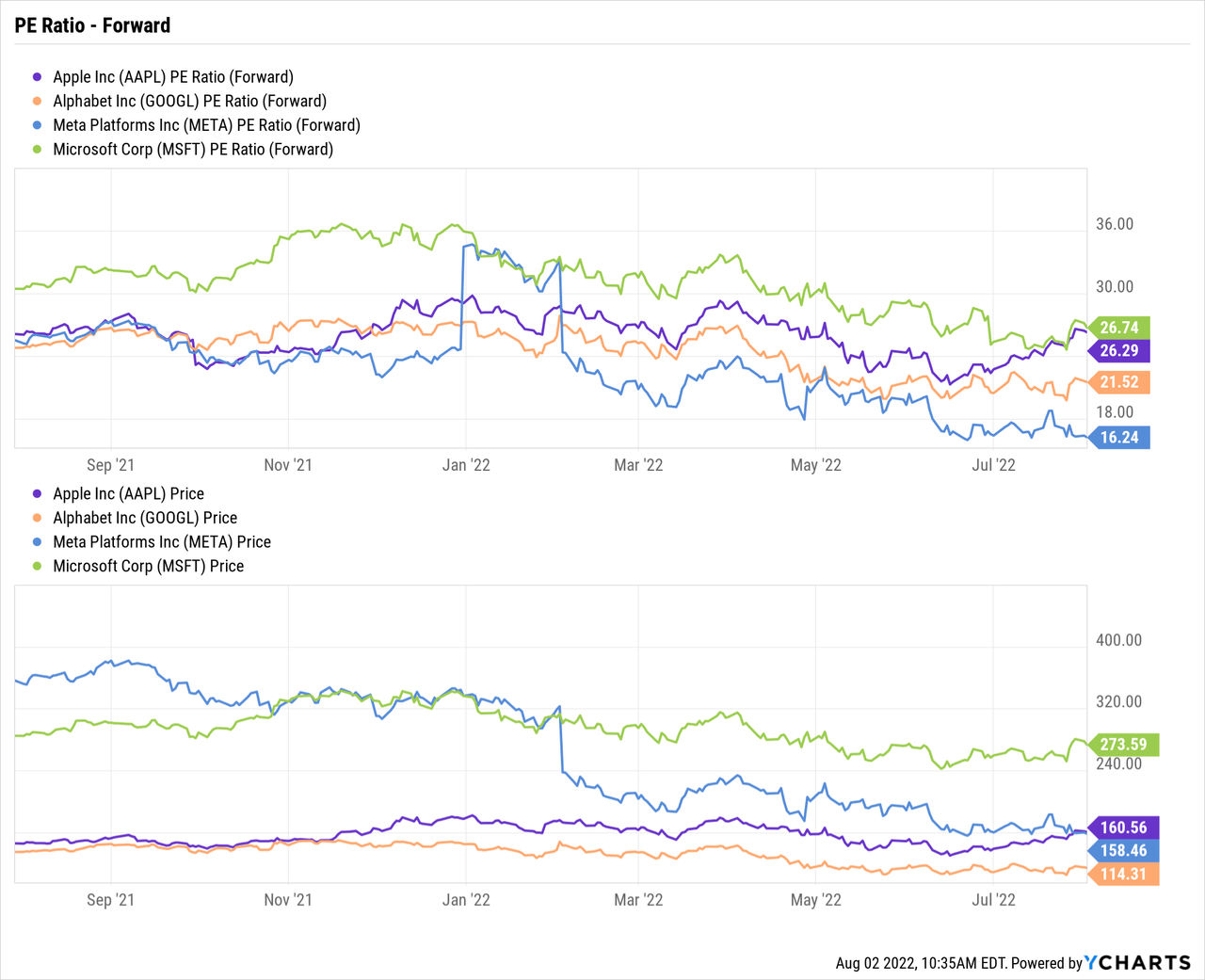

The biggest problem with Apple is that the stock still remains priced for near perfection. The stock now trades at 26x forward EPS estimates despite not even reporting 2% revenue growth in the last quarter.

Microsoft (MSFT) has the same forward PE multiple after reporting 12.4% growth in the June quarter. Alphabet (GOOG, GOOGL) trades at a much lower PE multiple and the internet search giant reported the fastest growth of the tech giant group at 12.6%.

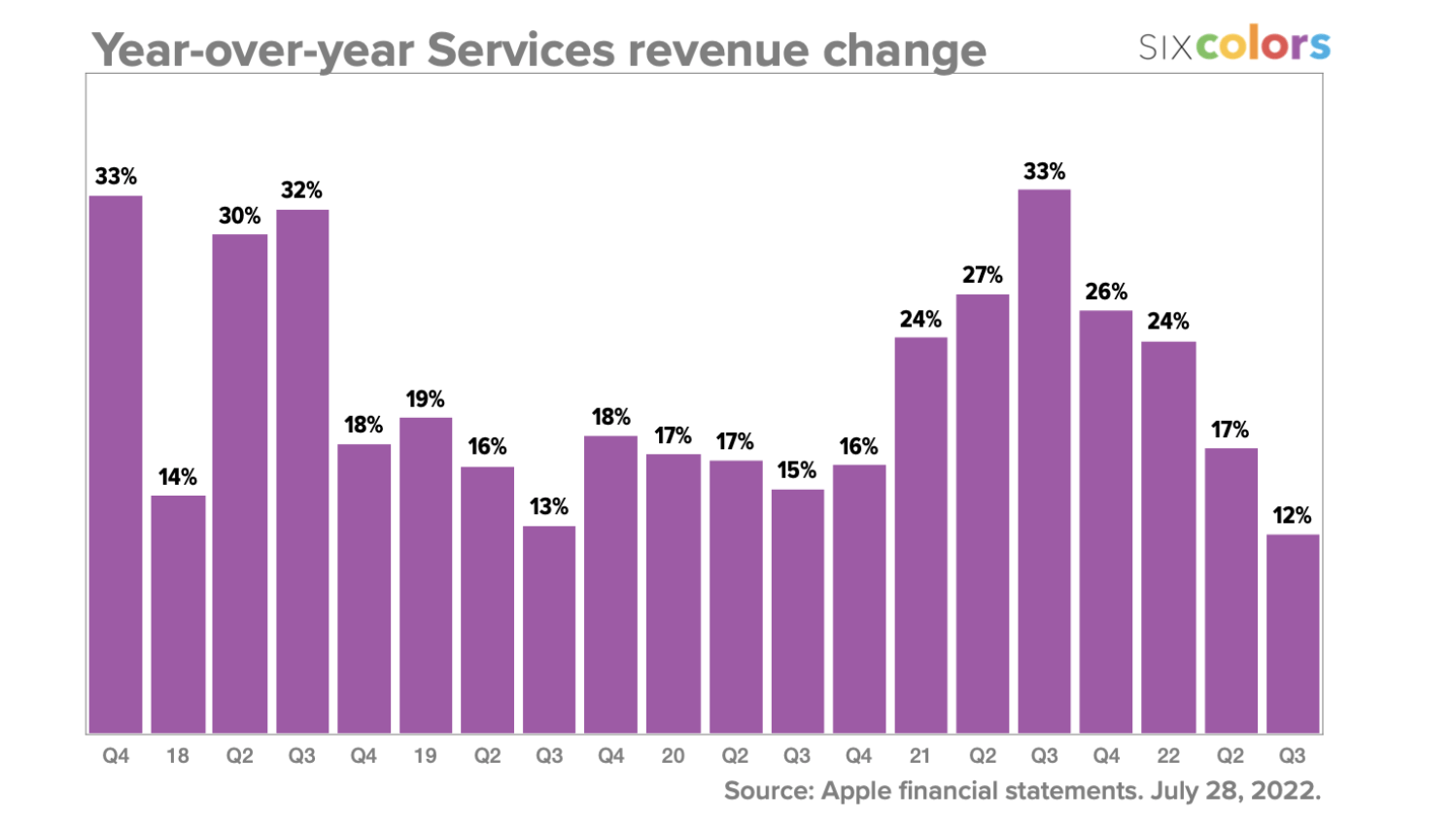

Both Microsoft and Alphabet have business models more focused on recurring revenue streams. Apple Services only grew 12% in the quarter further highlighting how such recurring revenues are very dependent on the growth of Products to drive faster growth.

Source: SixColors

For Apple, Services only amount to ~24% of total revenues, yet the tech giant is already seeing these growth rates slow to similar rates as the companies with full business models generally more focused on recurring revenue streams. Microsoft is focused on business software and Alphabet digital adverting to generate fast growth rates for the whole businesses.

Apple remains a great company, but the business is still highly reliant on more cyclical product purchases boosted during covid. The tech giant could face years where consumers pause purchases of Macs and iPads after loading up on such tech gear during 2020/21.

Per CFO Luca Maestri, Services are forecasted to slow even further during the September quarter to the lowest growth rate at least in recent years:

Specifically related to Services, we expect revenue to grow but decelerate from the June quarter due to macroeconomic factors and foreign exchange.

Takeaway

The key investor takeaway is that Apple remains a great company, but the stock is disconnected from the actual results reported by the tech giant. If Apple trades at 15x FY23 EPS estimates of $6.46 similar to the multiple applied to Meta Platforms (META), the stock would trade at $97.

My thesis remains that Apple will continue to trade flat to down for years, as investors eventually face the reality of the slow growth scenario at the tech giant.