kmwphotography

Top-down approach

I have outstanding sell ratings on S&P 500 (SPY) and NASDAQ 100 (QQQ). Note, Apple (NASDAQ:AAPL) is almost 14% of QQQ by weight, and almost 8% of SPY – the most influential stock in both of these broad stock market indices. Thus, indirectly, I am also recommending a sell on AAPL, as it’s hard to see a significant drop in SPY and QQQ without at least a modest drop in AAPL.

As a result, it is important to individually analyze Apple, to determine whether the bear case for the broader market still holds true. Note, this is a top-down analysis of an individual stock.

The bottom-up approach usually starts with the company itself, looking at the different firm-specific variables (product, services, management, ratios…). The top-down approach starts with the broad macro analysis (based on monetary/fiscal policy, trade policy, and geopolitics), and from there it goes to the effect on different sectors, and finally the individual stocks.

Is Apple stock recession-proof?

The top-down approach to analyzing individual stocks boils down to the estimating of the probability of an imminent recession and assessing how the individual stocks would be affected by the predicted recession.

So, let’s start with the discussion whether the potential recession would significantly negatively affect Apple’s financial performance. Rather than trying to be opinionated about this issue, I am interested in knowing what the Company itself says about the effect of market risk (systematic risk) on the Company’s financial performance. I retrieved the latest AAPL annual report (10K statement) and looked for the “risk factors”. This is what I found (text bolded by the author): Apple Inc. | 2021 Form 10-K

The Company’s operations and performance depend significantly on global and regional economic conditions and adverse economic conditions can materially adversely affect the Company’s business, results of operations and financial condition.

The Company has international operations with sales outside the U.S. representing a majority of the Company’s total net sales. In addition, the Company’s global supply chain is large and complex and a majority of the Company’s supplier facilities, including manufacturing and assembly sites, are located outside the U.S. As a result, the Company’s operations and performance depend significantly on global and regional economic conditions.

Adverse macroeconomic conditions, including inflation, slower growth or recession, new or increased tariffs and other barriers to trade, changes to fiscal and monetary policy, tighter credit, higher interest rates, high unemployment and currency fluctuations can materially adversely affect demand for the Company’s products and services. In addition, consumer confidence and spending can be adversely affected in response to financial market volatility, negative financial news, conditions in the real estate and mortgage markets, declines in income or asset values, changes to fuel and other energy costs, labor and healthcare costs and other economic factors.

In addition to an adverse impact on demand for the Company’s products, uncertainty about, or a decline in, global or regional economic conditions can have a significant impact on the Company’s suppliers, contract manufacturers, logistics providers, distributors, cellular network carriers and other channel partners. Potential effects include financial instability; inability to obtain credit to finance operations and purchases of the Company’s products; and insolvency.

A downturn in the economic environment can also lead to increased credit and collectibility risk on the Company’s trade receivables; the failure of derivative counterparties and other financial institutions; limitations on the Company’s ability to issue new debt; reduced liquidity; and declines in the fair value of the Company’s financial instruments. These and other economic factors can materially adversely affect the Company’s business, results of operations and financial condition.

So, without the need to provide my own opinion, I infer from Apple’s management discussion that the potential recession would “materially adversely affect the Company’s business, results of operations and financial condition” through multiple channels, ranging from the lower consumer demand, higher interest rates, increased credit risk, stronger USD, global demand…, the list is long. Based on the “risk factors” statement, it appears that Apple management likely does not think that Apple stock is recession-proof.

What is the probability of an imminent recession?

Given that AAPL is probably not a recession-proof stock, the top-down approach can be used to predict AAPL’s performance. The critical variable is, however, to accurately estimate the recession probability.

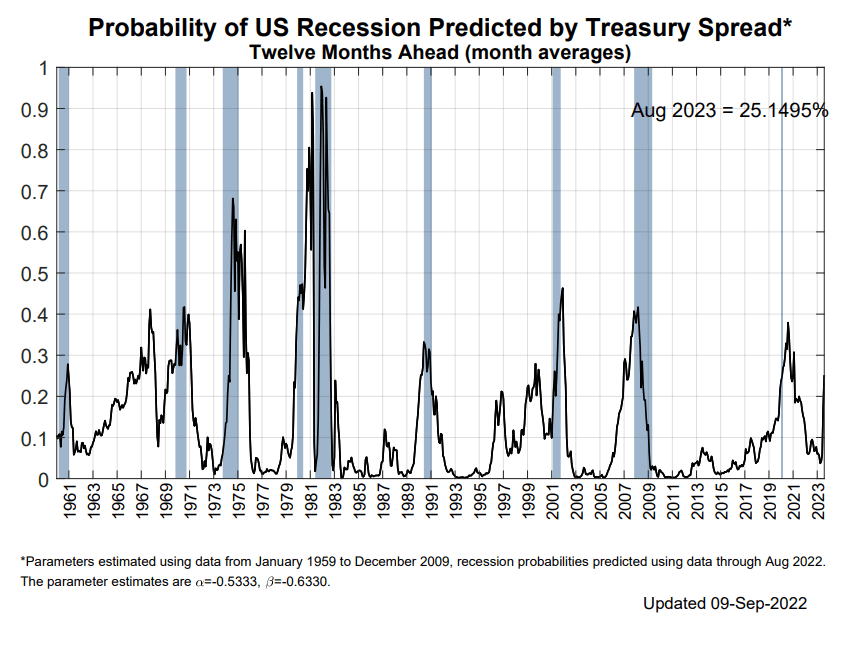

Again, without the need to be opinionated about an imminent recession, we can obtain the recession probability directly from the NY Fed. The NY Fed uses the proprietary logit model to estimate the recession probably over the next 12 months solely based on the spread between the 10Y Treasury Bond and the 3-month Treasury Bill. As the 10y-3mo spread narrows towards the 0 level, the recession probability increases, and when it inverts up to the certain level, an imminent recession becomes almost a certainty (very few false signals over the long period of time). More specifically, when the estimated recession probability exceeds the 30% level, the recession follows in all cases since 1961.

Currently, the NY Fed recession probability is at 25.149%, as updated on September 9, 2022. Note, the 10y-3mo has narrowed since, but it’s still positive. However, as the Fed increases the short-term interest rates on Sep 21, it is likely that 10y-3mo spread will invert, which will send the recession probability over the 30% threshold – and signal an imminent recession. Here is the NY Fed recession probability chart:

NY Fed

What kind of company is Apple?

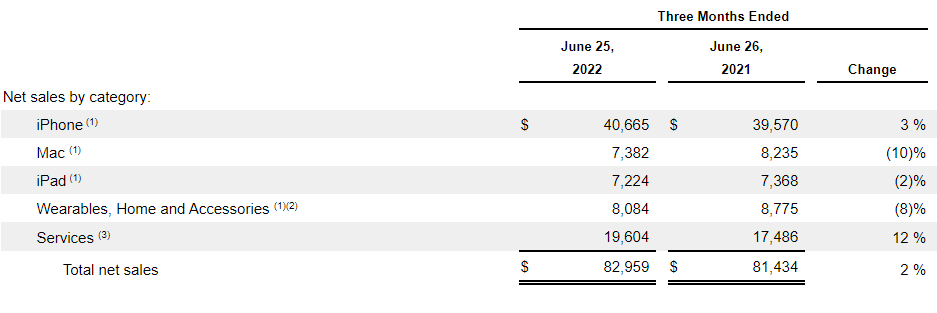

From the macro point of view, Apple is essentially a one-product company. Based on the latest quarterly report Apple 10Q July 29th 2022 Apple derives almost 50% of sales from iPhone. Services represent nearly 25% of the sales, but these services are likely related to iPhone. Other products are also likely part of the iPhone ecosystem. (There is “somebody I know” who needs to buy a new laptop, and when asked what kind of laptop he wants for school purposes, the person says Mac, so it can be connected to his Apple AirPods, which work with iPhone. And the same person keeps asking me to buy more cloud storage for his iPhone.)

The table below shows that iPhone sales have grown by 3% over the same quarter in 2021, while it appears the services are growing at a high rate of 12%. Clearly, Apple is trying to compensate to slower product sales with higher services sales.

Apple 10Q

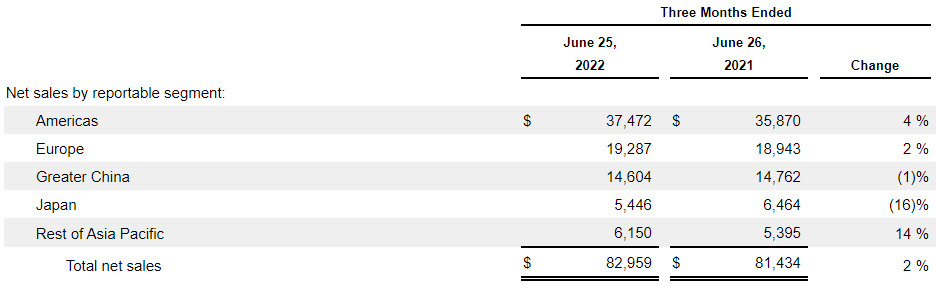

Apple is also an international company, with almost 50% of sales from of the Americas, and almost 25% from Europe, and over 15% from China. Thus, Apple is significantly exposed to the dire economic situation in Europe, and the geopolitical situation in China, in addition to the weakening US economic situation.

Apple 10Q

Thus, it appears that Apple is severely exposed to the dire economic situation in the US and globally. Yet, the analysts are predicting that Apple’s EPS would grow from $6.10 in 2022 to $6.44 in 2023, or by 5.5%. I think this is an unrealistic forecast, given the high probability of an imminent recession over the next 12 months. Not only do I think that the analysts should downgrade the earnings growth, but also they likely should consider factoring in the earnings decline over the next 12 months.

More importantly, Apple’s forward PE ratio, which considers the current earnings growth, is at 24. This is likely overvalued for a company that has only modest growth in its key product. But, when considering the very high recession probability, those expected earnings will likely be downgraded, which would also require a significant valuation contraction in my opinion.

|

Fiscal Period Ending |

EPS Estimate |

Forward PE |

|---|---|---|

|

Sep 2022 |

6.10 |

24.69 |

|

Sep 2023 |

6.44 |

23.39 |

Implications

Based on the “risk statement” in Apple’s 10K statement, Apple is probably not a recession-proof stock. Currently, the probability of an imminent recession is very high. Thus, if an actual recession follows within the next 12 months, Apple’s financial performance is likely to be materially affected.

However, Apple’s stock is likely not priced for a recession. The valuation metrics are overstretched, and the analysts are still predicting a 5.5% EPS growth in 2023.

Thus, I think Apple’s stock has a significant downside, as the earnings expectations likely get downgraded to reflect an imminent recession, and as the valuation multiple is likely to be contracted.