Shahid Jamil

By The Valuentum Team

Apple Inc (NASDAQ:AAPL) and its namesake brand is arguably one of the best known companies and brands in the world, and for good reason. The firm is a financial powerhouse backed up by an expansive and ever growing slate of products and services geared towards tech consumers of all types. We are huge fans of Apple’s capital appreciation and dividend growth potential. Shares of AAPL yield ~0.6% as of this writing.

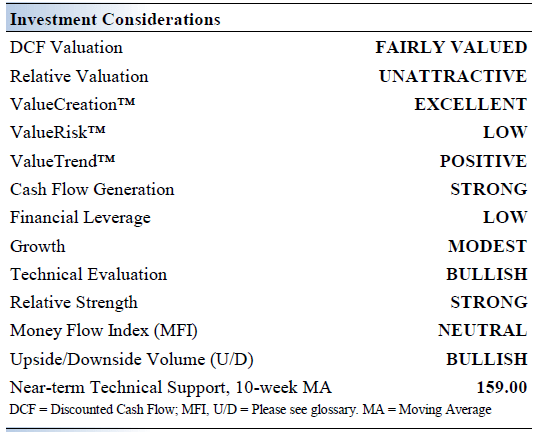

Apple’s Key Investment Considerations

Image Source: Valuentum

Apple is as much a brand as it is one of the world’s most innovative companies. The firm is no longer known for its iPods and personal computers thanks to the proliferation of the iPhone over the past decade. The company’s execution remains top notch, and we expect it to continue to roll out innovative products in smartphones and wearable technology.

On September 7, Apple is set to host a product launch event that will reportedly see the latest edition of its iPhone lineup get announced. Apple’s rollout of future iterations of the iPhone should propel its fundamentals. Though we’re not embedding another blockbuster hit in our enterprises cash flow model, we wouldn’t be surprised if Apple delivers another. The sky is the limit when it comes to innovation at Apple.

Apple’s growing Services segment bodes well for its long-term profitability, and the segment is growing like a weed. Apple Pay is now accepted by a large percentage of US retailers, and paid subscriptions are surging. Wearables has been an area of strength, and Apple holds a large share of global smartwatch market. Its customer loyalty and installed base of devices are key competitive advantages over its peers.

Though we’re not too worried given Apple’s bargaining power over suppliers, investors should pay close attention to the firm’s gross margin. Pricing and cost pressures may be unavoidable at times, and currency exchange rates should not be ignored as Apple generates roughly three-fifths of its revenue outside the US.

Apple’s cash hoard is more than the market caps of some the largest firms in the S&P 500. It retains tremendous flexibility, and its dividend growth potential may be unmatched. During Apple’s latest earnings call, management reiterated the firm’s commitment to become net cash/debt neutral over the long haul, though such a process will likely take a long time. While we would prefer for Apple to maintain its fortress-like balance sheet, the company is aggressively distributing cash back to shareholders via enormous share buyback programs and substantial dividend increases.

Earnings Update

On July 28, Apple reported third quarter earnings for fiscal 2022 (period ended June 25, 2022) that beat both consensus top- and bottom-line earnings estimates. Apple’s GAAP revenues rose by 2% year-over-year in the fiscal third quarter to reach $83.0 billion, with 12% growth at its ‘Services’ sales offsetting a 1% decline at its ‘Products’ sales (growth in the sales of its iPhone offerings were offset by declines elsewhere).

Broken down by geographic market (on a year-over-year basis), Apple reported sales growth in the Americas (up 4%), Europe (up 2%), and the Rest of Asia Pacific (up 14%) regions though its sales in the Greater China (down 1%) region and Japan (down 16%) declined last fiscal quarter. Declines in the Greater China region could potentially be due to China’s recent COVID-related economic lockdowns, and the eventual easing of those lockdowns should benefit Apple’s revenue generation potential going forward (along with Apple’s supply chain given how many of the company’s components and products are made in the country).

The shift towards higher margin Services sales, which includes revenues generated by its App Store, Apple Care, various digital subscriptions (such as Apple TV+), and more, is helping Apple maintain its strong gross margins in the face of major exogenous shocks.

In the fiscal third quarter, Apple’s Products gross margin declined by ~150 basis points year-over-year to reach 34.5%, as inflationary pressures and supply chain hurdles took their toll. However, Apple’s Services gross margin rose by ~170 basis points year-over-year to reach 71.5% last fiscal quarter. As its Services sales continued to grow as a share of Apple’s total quarterly revenues, rising segment-level gross margins here along with a favorable sales mix shift supported Apple’s gross margin performance last fiscal quarter, with its GAAP gross margins coming in at 43.2% (down marginally year-over-year).

Apple’s operating expenses rose by 15% year-over-year in the fiscal third quarter as the company needs to invest heavily in R&D to remain competitive while competition for tech talent is fierce, requiring sizable pay boosts to retain key employees. The firm’s GAAP operating income declined by 4% year-over-year to reach $23.1 billion last fiscal quarter.

A large year-over-year increase in its income tax provision along with the modest decline in its operating income, factors that were somewhat offset by a meaningful year-over-year reduction in Apple’s outstanding diluted share count, saw Apple post $1.20 in GAAP diluted EPS in the third quarter of fiscal 2022 (down 8% year-over-year).

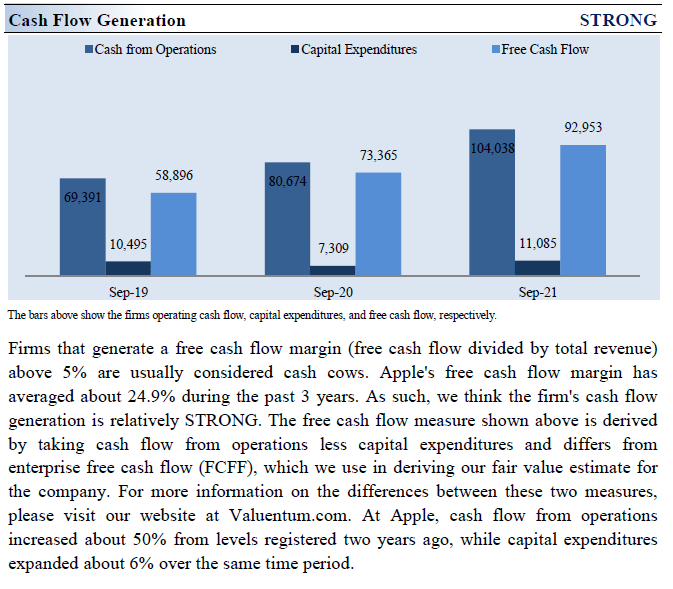

During the first three quarters of fiscal 2022, Apple generated $90.6 billion in free cash flow (defined as net operating cash flow less capital expenditures), up from $76.0 billion in the same period in fiscal 2021. Apple spent $11.1 billion covering its dividend obligations and another $65.0 billion buying back its stock during the first three quarters of fiscal 2022, activities that were fully covered by its free cash flows. We are impressed that Apple is a stellar free cash flow generator in almost any operating environment.

Apple exited the fiscal third quarter with $59.6 billion in net cash on hand (inclusive of noncurrent marketable securities and short-term debt). We are huge fans of Apple’s fortress-like balance sheet.

Guidance Update

During Apple’s latest earnings update, management provided a qualitative overview of their expectations for the company’s near term performance. Here is what management had to say during Apple’s latest earnings call:

As we move ahead into the September quarter, I’d like to review our outlook… Given the continued uncertainty around the world in the near term, we are not providing revenue guidance but we are sharing some directional insights based on the assumption that the macroeconomic outlook and COVID-related impacts to our business do not worsen from what we are projecting today for the current quarter.

Overall, we believe our year-over-year revenue growth will accelerate during the September quarter compared to the June quarter despite approximately 600 basis points of negative year-over-year impact from foreign exchange. On the product side, we expect supply constraints to be lower than what we experienced during the June quarter. Specifically related to Services, we expect revenue to grow but decelerate from the June quarter due to macroeconomic factors and foreign exchange. – Luca Maestri, Senior VP and CFO of Apple

The strong US dollar seen of late is expected to weigh negatively on Apple’s near term revenue performance, while supply chain hurdles and inflationary pressures represent headwinds to Apple’s near term earnings performance. With these headwinds in mind, Apple possesses the operational prowess to navigate through these obstacles with its longer term growth runway firmly intact, in our view.

Apple’s Economic Profit Analysis

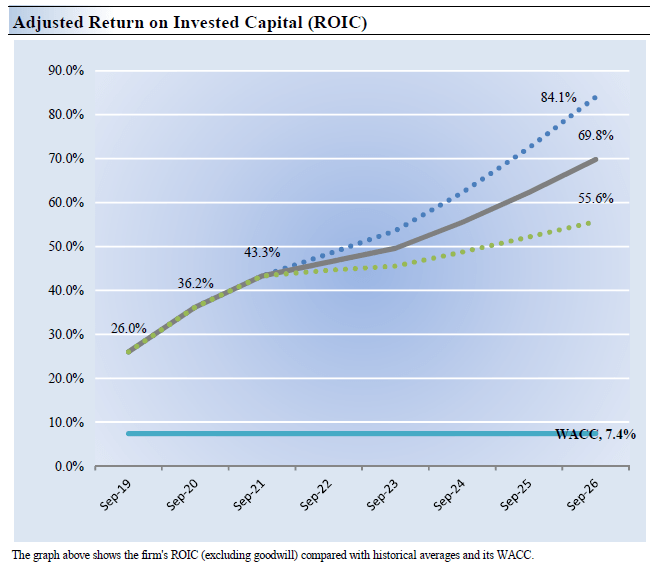

The best measure of a company’s ability to create value for shareholders is expressed by comparing its return on invested capital [‘ROIC’] with its weighted average cost of capital [‘WACC’]. The gap or difference between ROIC and WACC is called the firm’s economic profit spread. Apple’s 3-year historical return on invested capital (without goodwill) is 35.2%, which is above the estimate of its cost of capital of 7.4%.

In the chart down below, we show the probable path of ROIC in the years ahead based on the estimated volatility of key drivers behind the measure. The solid grey line reflects the most likely outcome, in our opinion, and represents the scenario that results in our fair value estimate. As you can see, Apple has historically been a rock-solid generator of shareholder value and we forecast that will continue being the case going forward.

Image Source: Valuentum

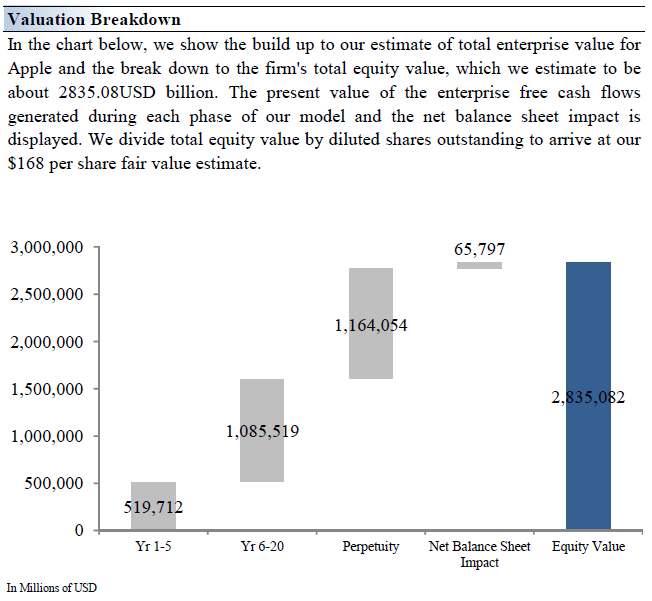

Apple’s Cash Flow Valuation Analysis

Image Source: Valuentum

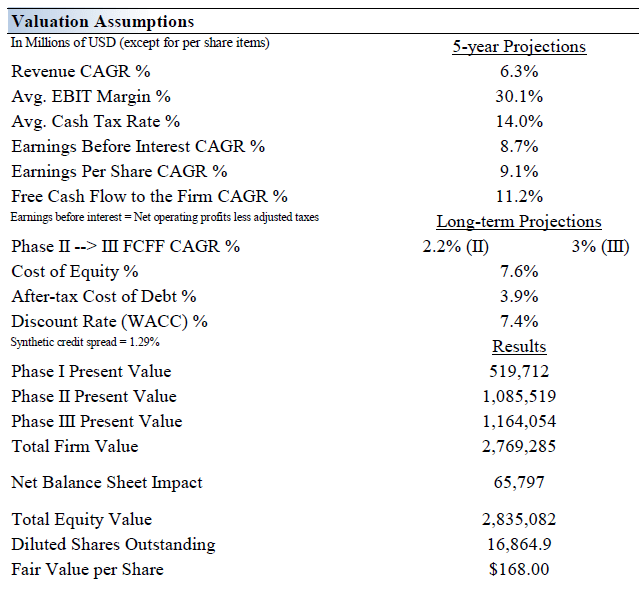

Our discounted cash flow process values each firm on the basis of the present value of all future free cash flows, net of balance sheet considerations. We think Apple is worth $168 per share with a fair value range of $134- $202 per share. The near-term operating forecasts used in our enterprise cash flow models, including revenue and earnings, do not differ much from consensus estimates or management guidance. Given that Apple expects its performance to improve going forward, we see room for shares of AAPL to test the upper end of our fair value estimate range.

The upcoming graphic down below highlights the key valuation assumptions used in our enterprise cash flow model. Our model reflects a compound annual revenue growth rate of 6.3% during the next five years, a pace that is lower than the firm’s 3-year historical compound annual growth rate of 11.3%. Our model reflects a 5-year projected average operating margin of 30.1%, which is above Apple’s trailing 3-year average. Beyond Year 5, we assume free cash flow will grow at an annual rate of 2.2% for the next 15 years and 3% in perpetuity. For Apple, we use a 7.4% weighted average cost of capital to discount future free cash flows.

Image Source: Valuentum Image Source: Valuentum

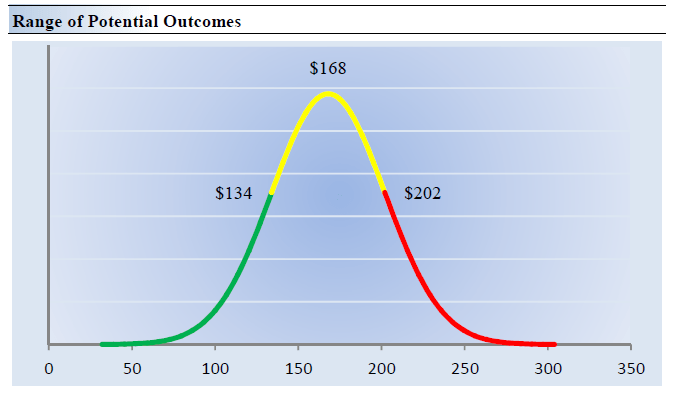

Apple’s Margin of Safety Analysis

Image Source: Valuentum

Although we estimate Apple’s fair value at about $168 per share, every company has a range of probable fair values that’s created by the uncertainty of key valuation drivers (like future revenue or earnings, for example). After all, if the future were known with certainty, we wouldn’t see much volatility in the markets as stocks would trade precisely at their known fair values.

In the graphic up above, we show this probable range of fair values for Apple. We think the firm is attractive below $134 per share (the green line), but quite expensive above $202 per share (the red line). The prices that fall along the yellow line, which includes our fair value estimate, represent a reasonable valuation for the firm, in our opinion.

Dividend Considerations

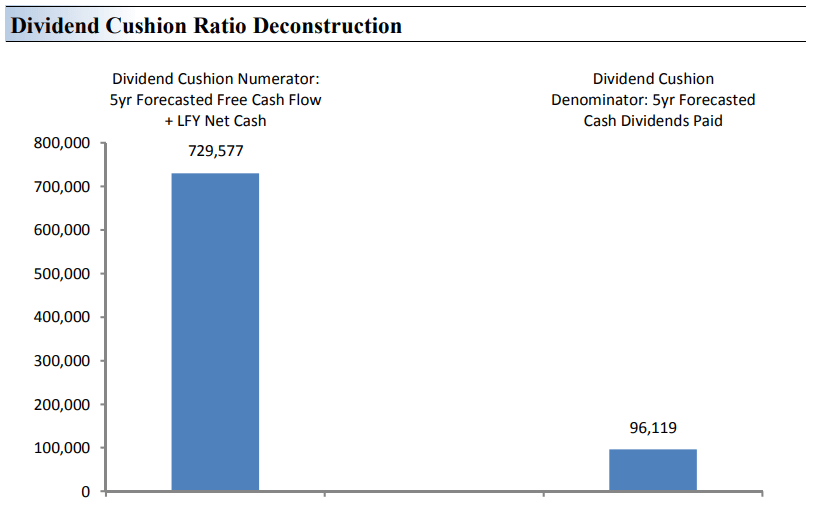

Dividend Cushion Ratio Evaluation (Image Source: Valuentum)

The Dividend Cushion Ratio Deconstruction, shown in the image above, reveals the numerator and denominator of the Dividend Cushion ratio for Apple. At the core, the larger the numerator, or the healthier a company’s balance sheet and future free cash flow generation, relative to the denominator, or a company’s cash dividend obligations, the more durable the dividend. In the context of the Dividend Cushion ratio, Apple’s numerator is larger than its denominator suggesting strong dividend coverage in the future.

The Dividend Cushion Ratio Deconstruction image puts sources of free cash in the context of financial obligations next to expected cash dividend payments over the next 5 years on a side-by-side comparison. Because the Dividend Cushion ratio and many of its components are forward-looking, our dividend evaluation may change upon subsequent updates as future forecasts are altered to reflect new information. Though there may be a lot of moving parts in the coming years, Apple has a very strong dividend at the moment!

Concluding Thoughts

Along with being one of the most innovative companies, Apple boasts unparalleled brand strength, giving it a material competitive advantage. We love what it has built through its ecosystem of apps and the presence it has in the everyday lives of consumers. A core tenet of Apple’s investment thesis, and its dividend strength, is its massive net cash position. The company’s tremendous free cash flow generation allows such a position to proliferate while continuing to pay a growing dividend.

We have a difficult time finding large drawbacks in Apple’s dividend growth profile. Competing capital allocation options have the potential to impact the pace of dividend expansion moving forward, specifically through strategic acquisitions of differentiated technology and share repurchases (which has been enormous in recent fiscal years). While we’re not particularly fond of Apple’s decision to go to a cash-neutral balance sheet, it will take a long time for that to occur.

In our view, Apple possesses ample capital appreciation upside potential, and its financial strength underpins a powerful dividend growth story.

This article or report and any links within are for information purposes only and should not be considered a solicitation to buy or sell any security. Valuentum is not responsible for any errors or omissions or for results obtained from the use of this article and accepts no liability for how readers may choose to utilize the content. Assumptions, opinions, and estimates are based on our judgment as of the date of the article and are subject to change without notice.