Amy Sussman

“Buy the bad news” is one of the most common sayings in investing. Basically, it means that when companies are going through tough times, they’re likely to rebound later. In many cases, this wisdom holds true, but there have been plenty of cases in history in which buying on bad news was followed by yet more downside.

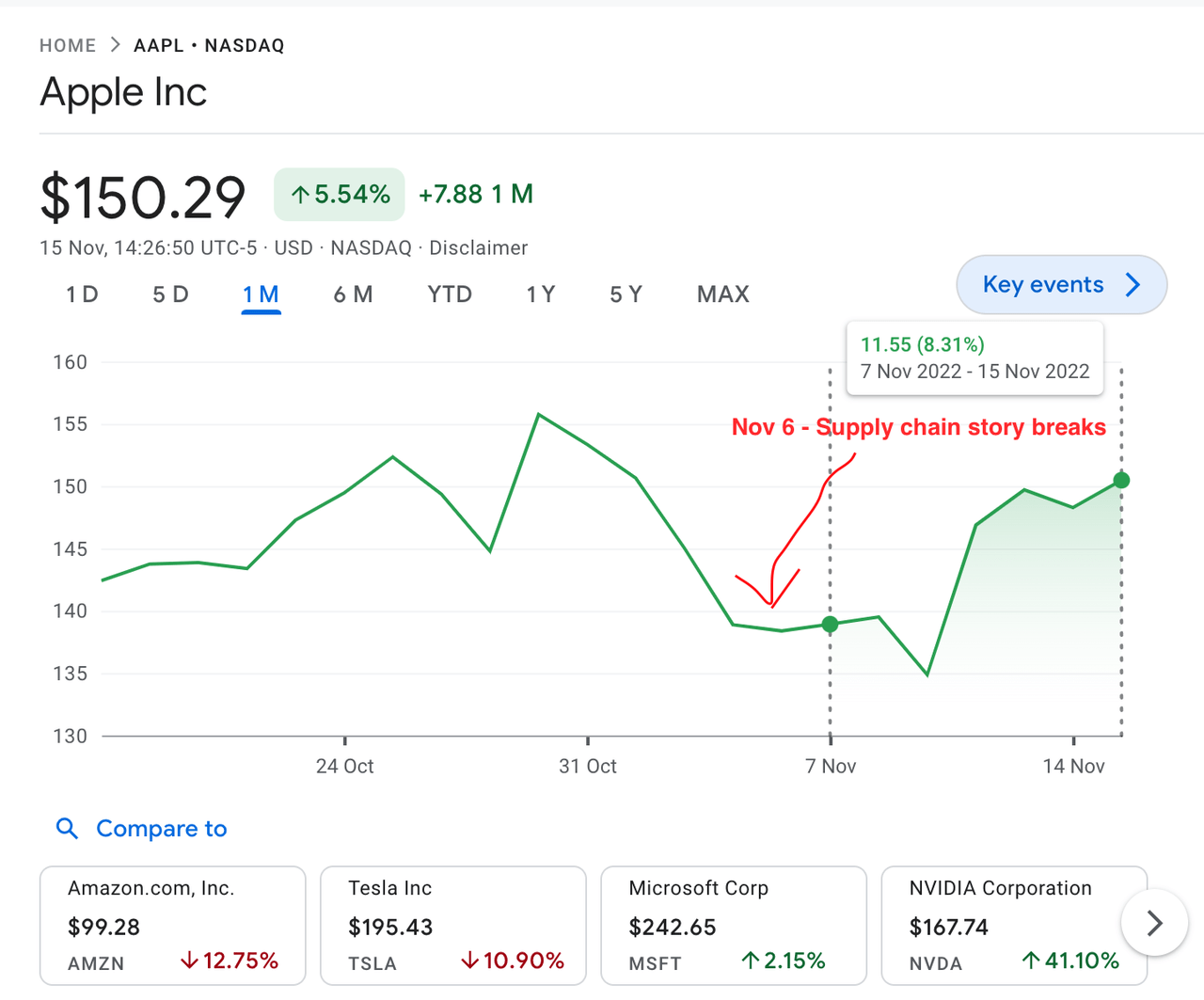

Apple Inc (NASDAQ:AAPL) is one of those stocks that makes the saying “buy the bad news” look good. Historically, if you had bought Apple when the news seemed bad, you’d have made a handsome return. For example, if you had bought on the “Chinese lockdown supply chain” story last week, you’d have bagged a quick 8.3% gain by November 15.

Apple rally after negative report (Google finance)

Why does Apple keep recovering from everything the economy throws at it, when other companies take real damage from weakening macro conditions?

There are many reasons for this. Some of them I’ve covered in past articles. The quick and dirty explanation for why Apple is so resilient is that it has a solid competitive position and a great brand. Apple enjoys high market share in several verticals, and it has a brand that keeps customers loyal. On top of that, it has an integrated ecosystem of software and hardware that incentivizes repeatedly buying Apple products.

The above goes a long way in explaining why Apple tends to thrive long term. It is a good business with great marketing, and organizations with those characteristics tend to thrive. However, there is a simpler explanation for why Apple usually rebounds from its temporary setbacks:

Very often, negative news about the company does not translate into bad earnings releases, because the negative publicity is usually about the iPhone supply chain, but the company does a lot more than just design the iPhone. It also makes other hardware, and software. In recent years, services has emerged as one of Apple’s largest and most profitable segments. So, Apple can do well even if negative reports about the iPhone turn out to be true.

Apple’s Business By Segment

In Apple’s most recent quarter, it did $90.14 billion in sales. The breakdown was:

-

$42.62 billion in iPhone sales.

-

$28.3 billion in other hardware sales.

-

$19.19 billion in services revenue.

As a result, the percentages of the total for each segment were:

-

iPhone: 47%.

-

Other hardware: 31.3%.

-

Services: 21.2%.

What does this have to do with Apple being a bad news buy?

To answer that question, we need to look at what most bad news stories about Apple pertain to.

When I did a Google News search for ‘Apple shipments,’ I found titles like:

In total, eight of the top 10 search results pertained to the iPhone. The MacRumors article, in particular, zeroed in on the iPhone 14 plus, one of four new iPhones launched this year. In other words, it dealt with 25% of the entire iPhone 14 lineup. It in no way implied that all iPhone sales would decline. In addition to the 14 plus, Apple sells the iPhone 14, the 14 Pro, the 14 Pro Max, and old models. 25% times 47% is a mere 11.75%, yet still, Apple stock took a notable dip on the day the iPhone 14 Plus report came out.

It should come as no surprise that Apple’s subsequent earnings release beat estimates. Investors apparently sold the stock on a report of weakness in one model in one product line. When a company has multiple products, weak demand for one of them doesn’t mean the whole company will underperform. But investors sometimes trade Apple stock based solely on news reports dealing with one of its products. Taking the other side of their trades may be profitable, as they are trading based on incomplete information–their conclusions are likely to be faulty.

Apple – a Free Cash Flow Valuation

Having looked at a major reason why Apple is able to overcome bad news about it, we can now proceed to a valuation. Knowing that Apple can do well even if it faces a headwind to one product’s sales is a positive, but it doesn’t mean it’s necessarily a buy. No stock is worth an infinite price. So, we need some estimate of what Apple’s intrinsic value is.

I’ve covered Apple’s multiples extensively in past articles. In general, Apple has higher earnings and cash flow multiples than many companies, but is not ‘extremely’ expensive compared to other tech companies. Given the mixed signals from multiples, it would help to do a discounted cash flow analysis on Apple to determine what it is truly worth.

In the last 12 months, Apple’s free cash flow components included:

|

Q1 |

Q2 |

Q3 |

Q4 |

TOTAL |

|

|

Net income |

$34.36B |

$25B |

$19.4B |

$20.7B |

$99.46B |

|

Non-cash costs |

$5.81B |

$5.5B |

$2.8B |

$5B |

$19.11B |

|

Fixed capital investments |

$200M |

$2.5B |

$2.1B |

$3.28B |

$8.08B |

|

Working capital investments |

$3.78B |

$2B |

$3.36B |

$3.28B |

$12.42B |

|

Net borrowing |

$-2.47B |

$-1.75B |

$971M |

$1.65B |

$-1.599B |

|

FCF |

$33.7B |

$24.2B |

$17.7B |

$20.79B |

$96.39 |

So, we get $96.39 in free cash flow to equity for the last 12 months. If we were calculating free cash flow to firm, we’d have to add in after-tax interest expense, since bond holders collect that rather than pay it, but this is an equity analysis, so I won’t include that one. With Apple’s 16.1 billion shares outstanding, we get $5.98 in FCF to equity per share. That’s step one in doing a discounted cash flow valuation for Apple.

The next question is, where will FCF go in the future? This is important because a company’s value is based on its future cash flows, not its past ones. In order to value the cash flows, then, we need an estimate of what they will look like going forward.

One method we could use is to simply value the last 12 months’ cash flows assuming no growth. This is a very conservative assumption, so we can use the current 10 year treasury yield as the discount rate. As of this writing, it was at 3.67%, but the average for the year has been about 4%, so I’ll use 4%. With a 4% discount rate, Apple’s $5.98 in FCF per share provides a target price of $149.5, which gives slight upside of 0.47%.

Another approach we could use is to assume a slight amount of growth. We can’t assume that a company of Apple’s size will grow at past rates going forward, so a slight growth rate of 5% seems reasonable here. This gives us the following FCF trajectory over five years:

- Year 1: $6.279.

- Year 2: $6.59.

- Year 3: $6.92.

- Year 4: $7.26.

- Year 5: $7.63.

Now, because we’re assuming some growth, we need to use a higher discount rate. The discount rate reduces the present value of future cash flows. In theory, the treasury yield is the discount rate, as it is the investor’s opportunity cost, but when you have risk in the picture, you raise it to account for uncertainty. Using 6% as the discount rate, the cash flows above sum to $29.04, as shown in the table below:

|

Year 1 |

Year 2 |

Year 3 |

Year 4 |

Year 5 |

TOTAL |

|

|

Un-discounted cash flow (“CF”) |

$6.279 |

$6.59 |

$6.92 |

$7.26 |

$7.63 |

N/A |

|

Discount rate |

1.06 |

1.123 |

1.191 |

1.262 |

1.338 |

N/A |

|

Discounted CF |

$5.92 |

$5.86 |

$5.81 |

$5.75 |

$5.70 |

$29.04 |

Now, if we assume no growth beyond year five, then the cash flows level out at $8.01. That provides a $133.2 terminal value in year 5. We then discount that back to the present, giving us $93.79 in terminal value today. Finally we add the present value of our five years’ cash flows to that and we get $123 in total present value.

So, we get a higher fair value estimate assuming zero growth and a low discount rate, than we do assuming modest growth and a high one. This gets at something I’ve said about Apple in my past articles: the stock at today’s prices is very sensitive to interest rates. It only needs to move up a few dollars from here to be a little overvalued. Of course, investors place a premium on an economic moat; it could be there’s something more to Apple than the numbers alone can tell us. Personally, though, I prefer to buy this stock well below $140.

The Bottom Line

The bottom line on Apple is that it’s a great company whose stock is just straddling the boundary of fair value. Depending on how you model it, you can get anything from a small bit of upside, to downside. The way I’ve been playing Apple this year is to buy it below $140. I feel like $139 is a reasonable price to pay for AAPL given its likely earnings trajectory and current interest rates. But this thesis would not survive a scenario where the Fed hikes rates to levels way beyond what the market currently expects.

Combine all of the above with Apple’s known tendency to beat earnings estimates after negative reporting, and we can see that AAPL is a classic “buy the bad news” stock. You can’t buy it at any price, but sentiment swings provide entry points often enough.