I own one dividend growth stock that is officially part of the technology sector. That stock is Apple Inc. (NASDAQ:AAPL). It’s one of my favorite investments despite its somewhat subdued exposure in my portfolio and the fact that I rarely cover the stock. I have 3.7% of my portfolio in Apple, which is below my portfolio average of 4.3%.

Author Portfolio

The reason why I haven’t covered the stock since May 9, 2021, is the same reason why the stock is still way too small in my portfolio: macro developments. In this article, I will explain why Apple is doing so poorly after I wrote in 2021 that inflation would become a serious issue – especially with regard to the Federal Reserve’s actions. However, while the current stock market isn’t fun for long-only (long-term) investors, I’m actually incredibly excited to see that Apple is doing so poorly. It provides us dividend growth investors with an opportunity to add at much better prices that will provide us with long-term opportunities to add substantial wealth to our portfolios. Apple is one of the stocks that need serious weakness to make sense for dividend growth investors.

In this article, I invite you to read my thoughts on macro, Apple, and my strategy in this market.

I will also explain why buying a very low yield makes sense for the “average” dividend investor.

So, let’s get to it!

A Quick Look Back

Let’s start with some transparency. I bought Apple in 2021 at an average price of $123.68. I haven’t bought more shares since then for one big reason: I wasn’t a fan of technology and “growth” stocks given the macro environment.

Last year, I wrote the following paragraph:

When I say Apple’s Achilles’ heel, I mean its sensitivity in times of rising inflation. I am not afraid of the competition potentially beating Apple long-term (i.e., Microsoft (MSFT)), and I am not afraid of recessions. While a recession will keep pressure on Apple for 1-2 years (on average), underperformance due to inflation is Apple’s real enemy.

Also, the following part applies here given what I’m about to show you next:

While highly speculative stocks get butchered, Apple is holding up very well as the company is what I consider to be the perfect mix of growth AND value. The company is not only expected to generate high growth in the future but also reward its investors already with massive buybacks and significant dividend hikes.

Inflation & Key Macro

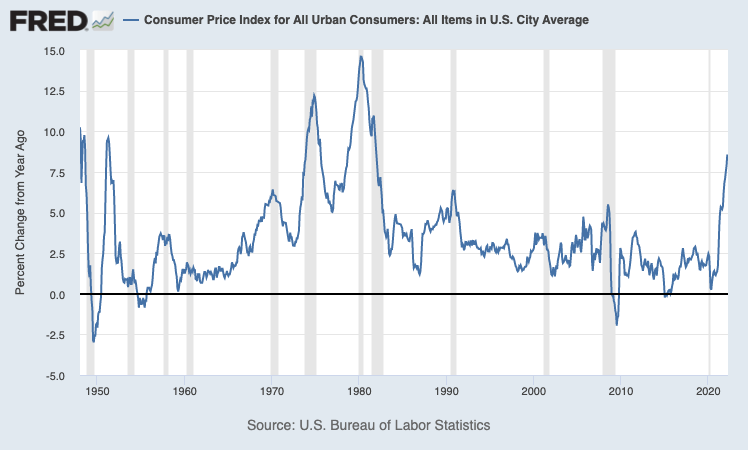

Unfortunately, I was right as inflation did become a big issue. Consumer price inflation in the United States is now above 8%. The situation in key markets like Europe isn’t much better as the reasons why inflation is high are similar in various economic “hotspots.”

St. Louis Federal Reserve

It all started in 2020 when lockdowns hurt supply chains. Inventories were empty and demand imploded in various sectors/industries. Then, demand came back roaring, yet there was no way for supply to rebound just as quickly. It hurt global shipping, manufacturing input prices, commodity prices, and much more. These problems still aren’t gone as China started to lock down its cities again. Right now, this is once again causing supply chain issues to worsen in US ports. Add to this that energy markets are seeing severe supply/demand imbalances as drillers aren’t able or willing to increase production. Oil prices are above $100 despite Chinese lockdowns, economic growth fears, and an aggressive Federal Reserve.

Add to this the war in Ukraine and the (related) food crisis that is slowly weakening the consumer where it hurts most: in essential purchases.

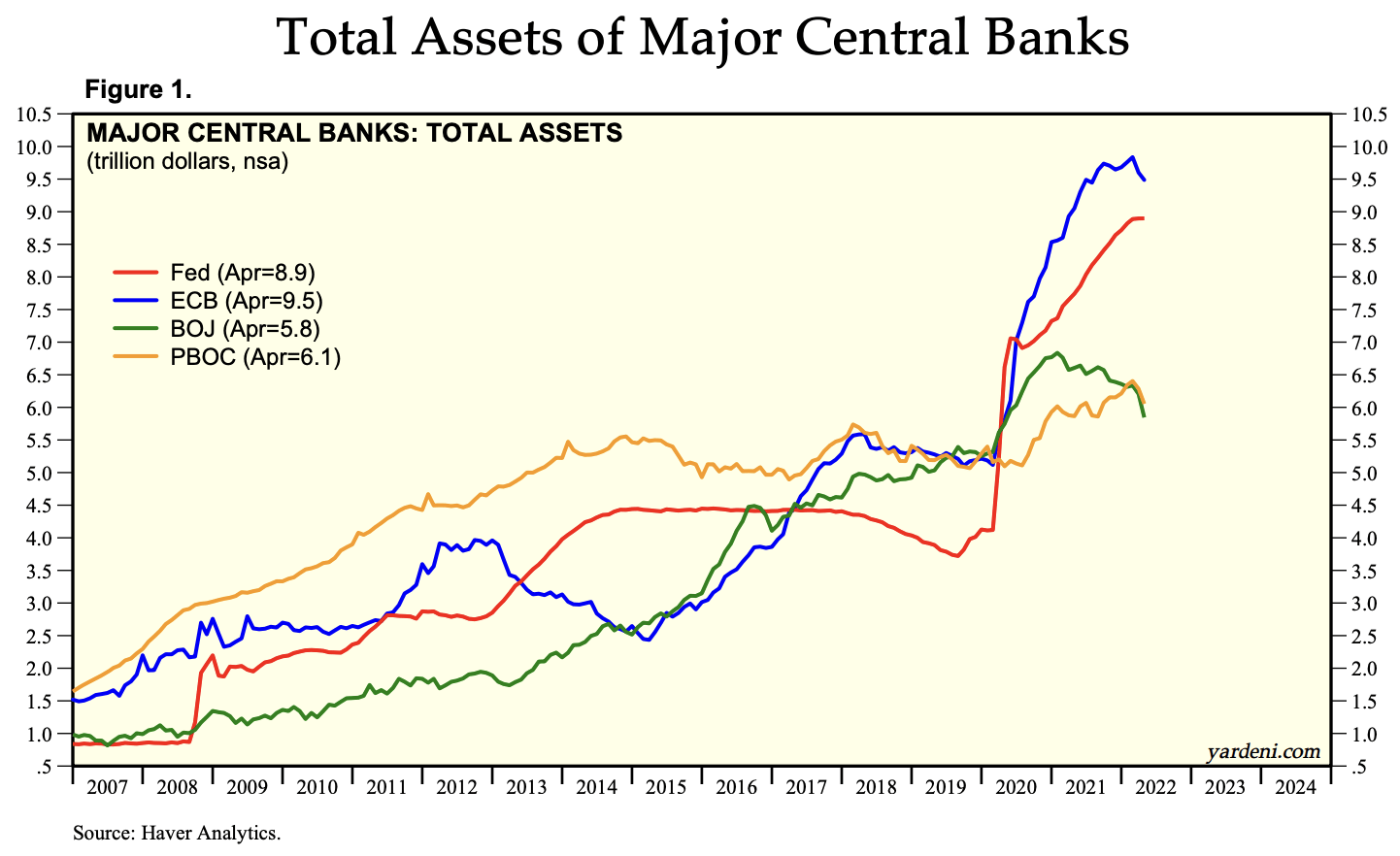

Moreover, central banks blew up their balance sheets like there was no tomorrow in 2020. Between the start of 2020 and the end of 2021, major central banks (Fed, ECB, Bank of Japan, People’s Bank of China) raised their combined assets from $21 trillion to more than $31 trillion.

Yardeni Research, Inc

In other words, a decreasing number of goods (and services) due to supply chain issues were chased by an ever-increasing amount of cash. It supported stock prices, home values, crypto, NFTs, and pretty much everything else that was perceived to have value.

Fast forward to 2022 and we’re in a situation where things are different. Inflation is high, supply chains are still broken, economic growth is slowing, and the Federal Reserve is expected to hike aggressively – in this case, while economic growth is weakening.

As my friend and macro expert Nick Glinsman wrote last week, the Fed could be even more aggressive to tame inflation than some expect right now.

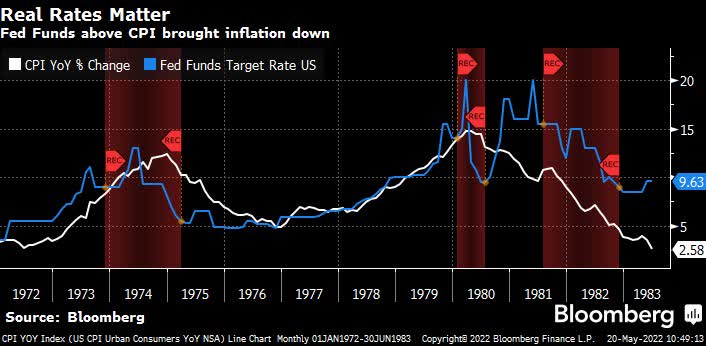

When thinking about the Federal Reserve’s job in getting inflation down, we often talk about real rates as measured by TIPS. However, instead we should be thinking about the gap between the Fed Funds rate and the consumer price index. This measurement, what I would call the “real” real rate, shows just how far we are from having a positive reading. It may be the case the amount of tightening needed to tame inflation is much greater than many realize. In fact, if the Fed were to ignore this measure, it risks throwing the economy into a recession without actually getting inflation under control.

Real 10-year rates measured by TIPS are just barely positive right now, whereas there’s a much larger gap between US CPI at 8.3% and the Fed Funds rate at 1%. If you look at the last inflationary period during the 1980s, it took years of the Fed Funds rate exceeding CPI for the Paul Volcker-led Fed to bring inflation down durably.

Bloomberg

What this means is that the Fed Funds futures’ terminal rate estimate of 3.25% in March 2023 may not be enough to tame inflation. The Fed said it will keep raising rates until inflation falls towards its 2% target. As it’s doubtful that inflation will fall to 3.25% by March, more aggressive hikes might be needed.

After all, a big part of inflation is caused by issues the Fed cannot influence. The Fed cannot solve the war in Ukraine, it cannot increase oil production, it cannot add labor supply, and it cannot convince China to refrain from implementing new lockdowns.

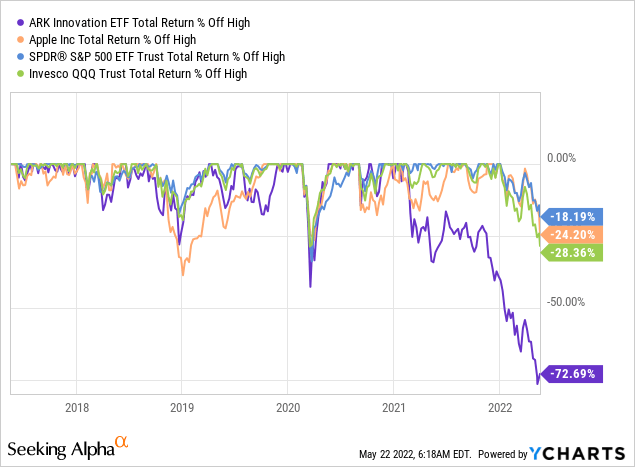

As a result, investors are de-risking their portfolios. The S&P 500 is down roughly 18.2% from its all-time high including dividends. The ARK Innovation ETF (ARKK) is down 73% from its all-time high as investors have sold high-growth stocks. The tech-heavy QQQ ETF (QQQ) is down 28.4%. Apple has lost roughly a quarter of its value.

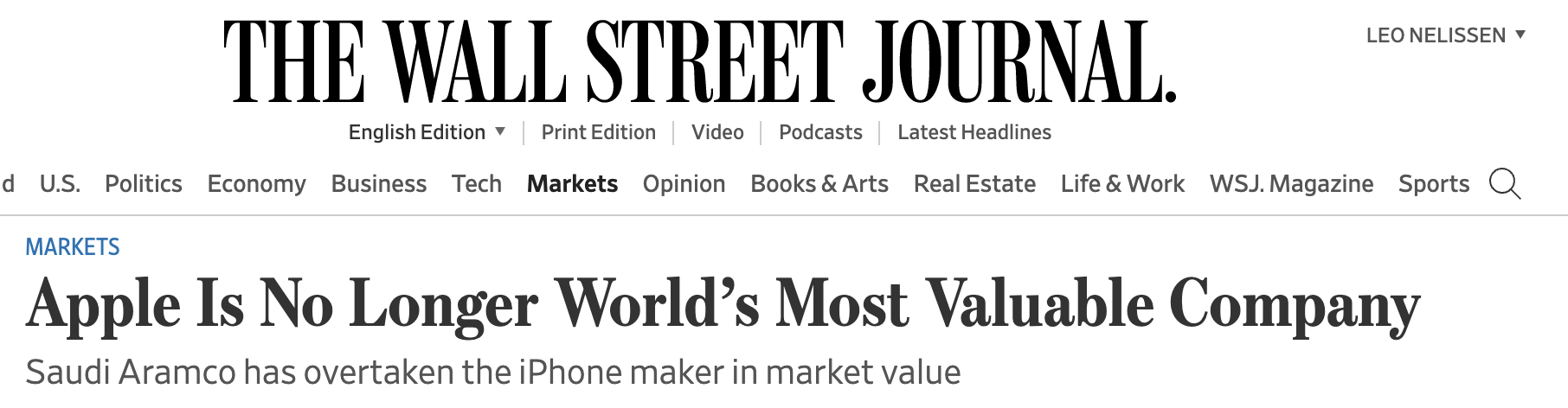

In other words, not only has Apple been one of the best performers since the pandemic, but it’s also doing rather well during the ongoing pandemic – compared to stocks that also shined prior to the sell-off. However, the company is not the world’s most valuable company anymore, as it has been overtaken by oil giant Saudi Aramco as reported by the Wall Street Journal.

Wall Street Journal

With that said, I could not care less. If anything, I’m very happy that Apple is down because I expected that inflation would hurt growth stocks.

On top of that, long-term investors should cheer on these buying opportunities as Apple is far more than a “growth” stock. As I wrote in 2021 and in this article, Apple is the perfect mix between growth and value. It helped the stock outperform the market in the past and it protects investors in times when pure-growth plays are getting butchered.

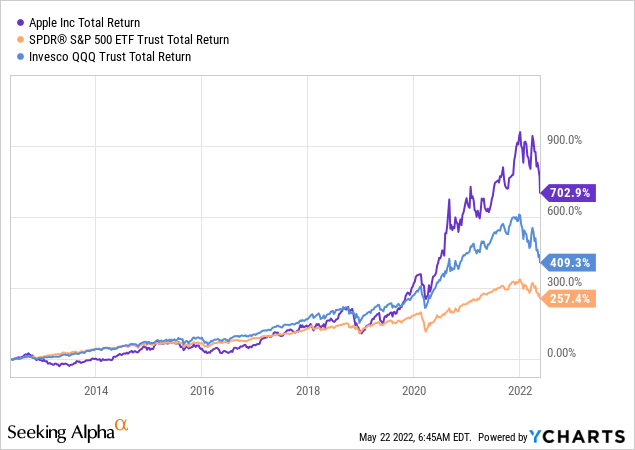

Over the past 10 years, Apple is still up more than 700% including dividends. That’s more than twice the return of the S&P 500.

With that said, market turmoil is opening up new opportunities that I want to use given my rather low Apple exposure.

Apple’s Growth & Value

Not only did I rename my Twitter account to Growth & Value, but the growth and value approach is also the cornerstone of my dividend growth portfolio, which is roughly 95% of my entire net worth.

As the current market environment shows so well, the stocks that deliver both growth and value are the best performers. In this case, I consider “value” to be a company’s ability to generate free cash flow used to maintain a healthy balance sheet and pay a growing dividend and the option to buy back shares. The “growth” aspect is straightforward as I dislike companies that are only able to pay a high yield without being able to grow, i.e., sales, EBITDA, and whatnot.

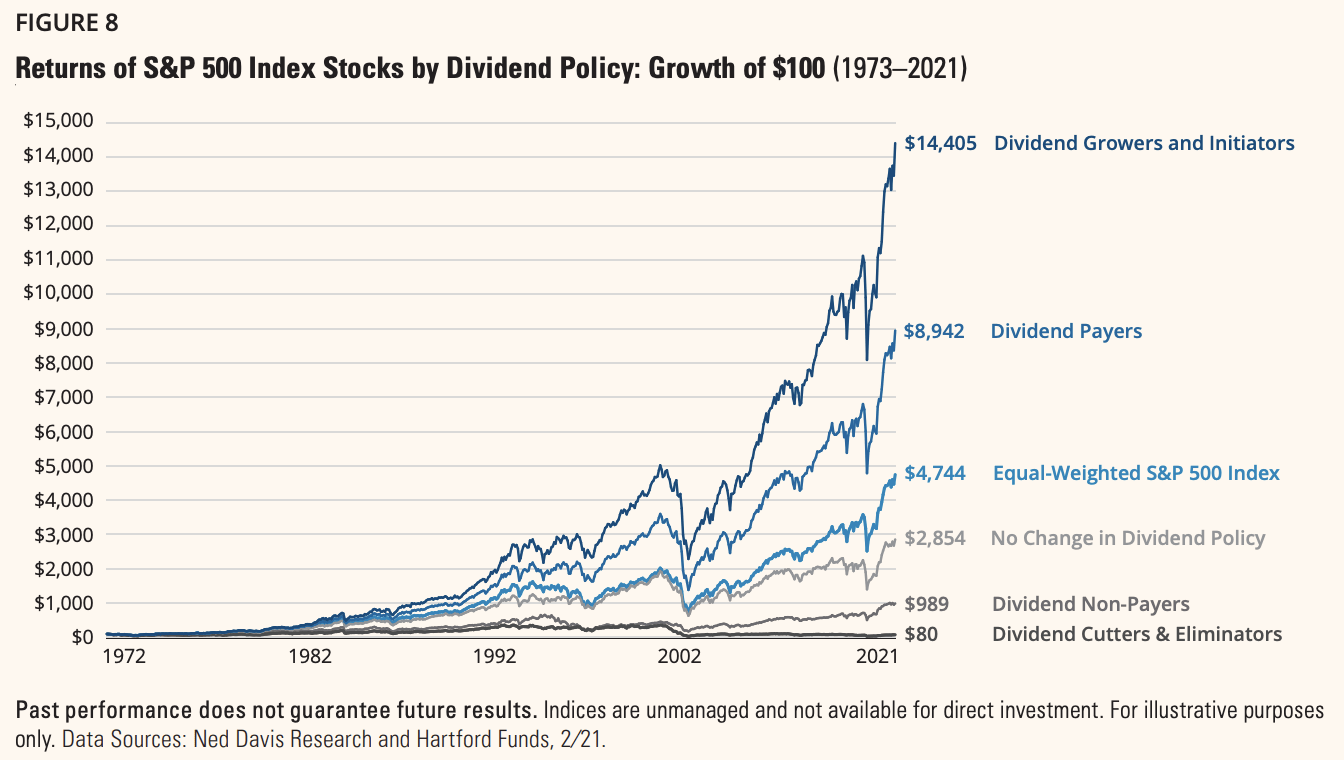

The graph below is important for what I’m about to say next. I used this graph in a recent dividend growth-focused article as it shows that historically speaking companies with both growth and value have outperformed the (equal-weight) market by a mile. Dividend growers are not just providing a stream of cash for shareholders, but the fact that they are able to pay a growing dividend shows that their businesses are in a good place. Companies that paid a dividend without growth did also well, yet they underperformed growers by a mile.

Hartford Funds

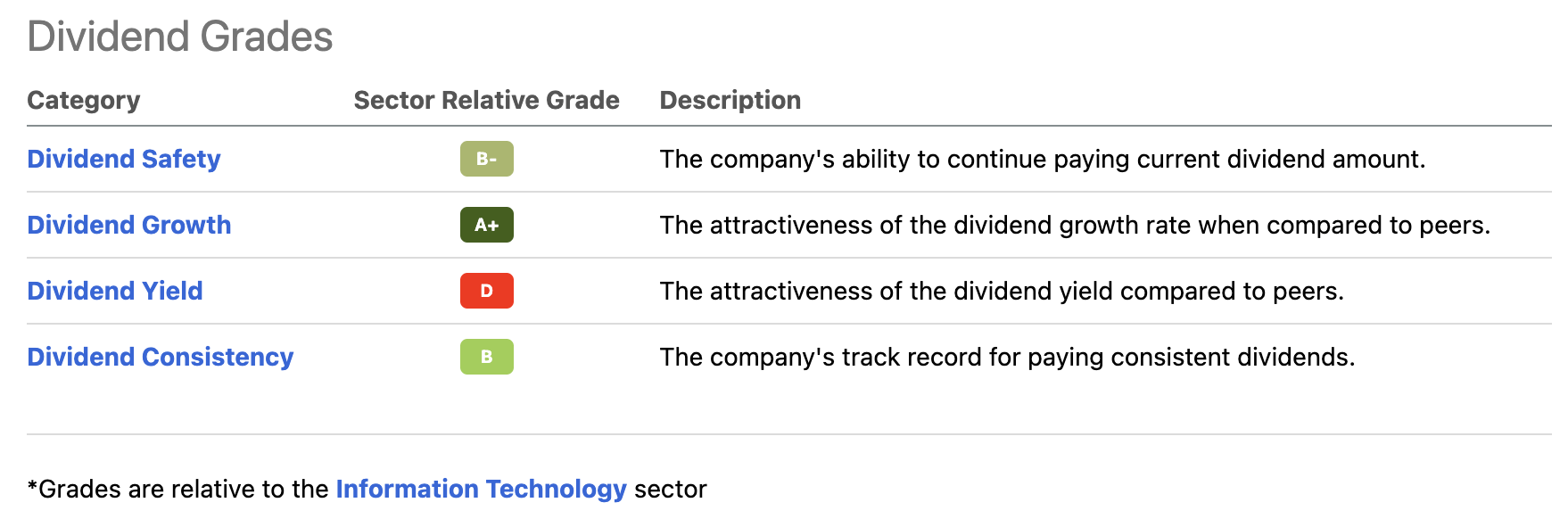

Apple has consistently grown its dividend since 2012, when it initiated a dividend for the first time since 1995. Seeking Alpha rates Apple’s dividend growth “A+” compared to its industry peers.

Seeking Alpha

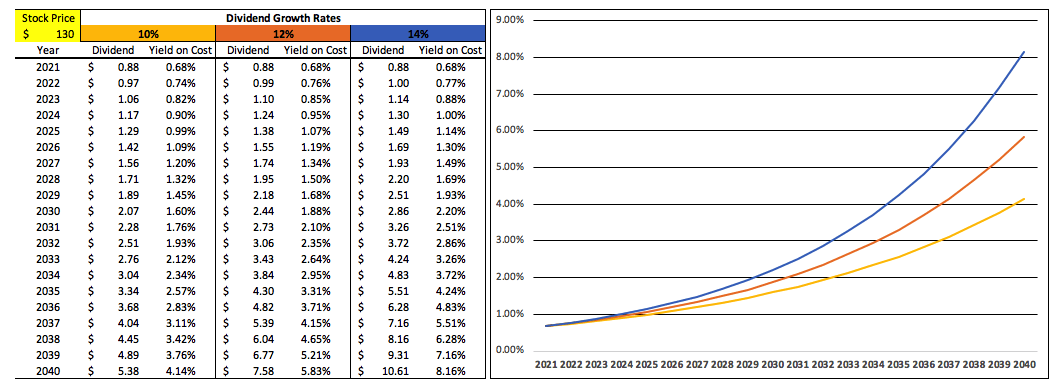

The current quarterly dividend is $0.23 per share after the company announced a 4.5% hike on April 28. This translates to $0.92 per year, which is a 0.67% yield based on a $138 stock price. This means the chart I used last year is relevant again (the one below). Back then, the yield was 0.68% based on a $130 stock price. It happens every now and then that dividend investors get upset when I give them a company with a yield of 0.7%. 0.7% isn’t a lot, that’s right. $10,000 invested in Apple will result in $70 annual dividends. That won’t get you very far – and $10,000 is a lot of money to a lot of people.

Last year, the company hiked its dividend by 7.3%. In 2020, the company hiked by 6.5%. In 2019, the company hiked by 5.5%. Over the past 5 years, the average annual hike is 8.8%.

For the sake of simplicity, let’s assume the company maintains long-term dividend growth of 10% (above its current average). That would result in a yield on cost of 4.2% in 2040. That’s roughly 18 years from now.

Author

4.2% on cost ends up being $420 in dividends (based on the $10,000 example – without adding shares). I doubt that will get us very far in 2040.

So, why am I still so happy to discuss this dividend growth opportunity?

The key is that Apple will not become a high-yield stock anytime soon. Growth is high and Apple generates a LOT of free cash flow.

When Apple announced the aforementioned 4.5% dividend hike on April 28, it also announced a $90 billion increase to its existing buyback program.

This is what the company commented on its 2Q22 earnings call:

Given the continued confidence we have in our business now and into the future, today our Board has authorized an additional $90 billion for share repurchases, as we maintain our goal of getting to net cash neutral, overtime. We’re also raising our dividend by 5% to $0.23 a share and we continue to plan for annual increases in the dividend going forward.

In that quarter, Apple bought back $22.9 billion worth of stock while returning $3.6 billion in dividends. In other words, the company’s priority is obvious. It will distribute cash in the most tax-efficient way, which also benefits its bottom line. A lower number of shares outstanding equals higher earnings per share.

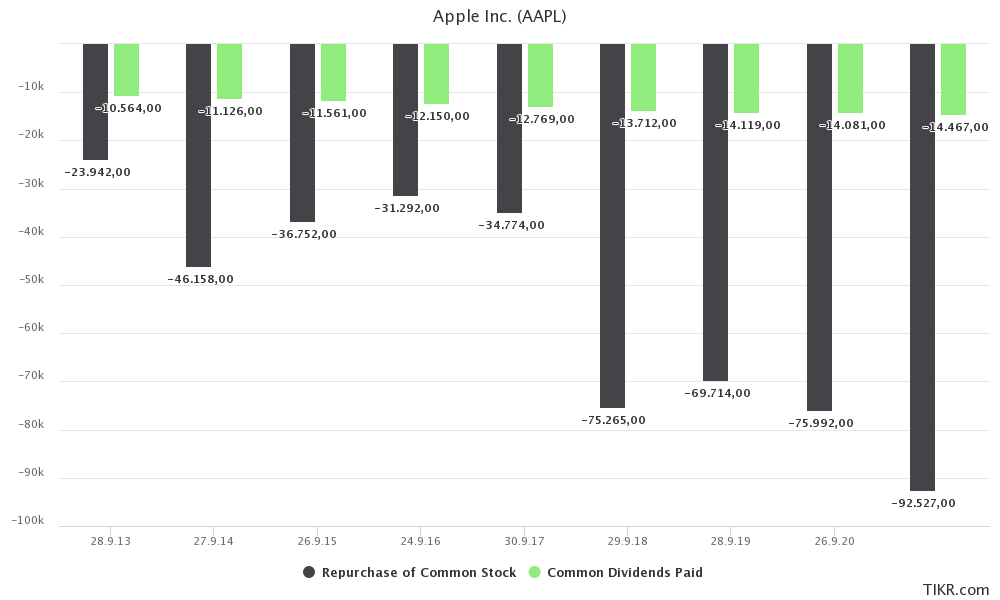

The graph below shows annual repurchases and dividends. Repurchases have exceeded $69 billion every single year since 2018.

TIKR.com

These buybacks allowed the company to reduce shares outstanding from 20.9 billion in 2017 to 16.7 billion at the end of 2021. That’s a decline of 20% or roughly 4.4% per year.

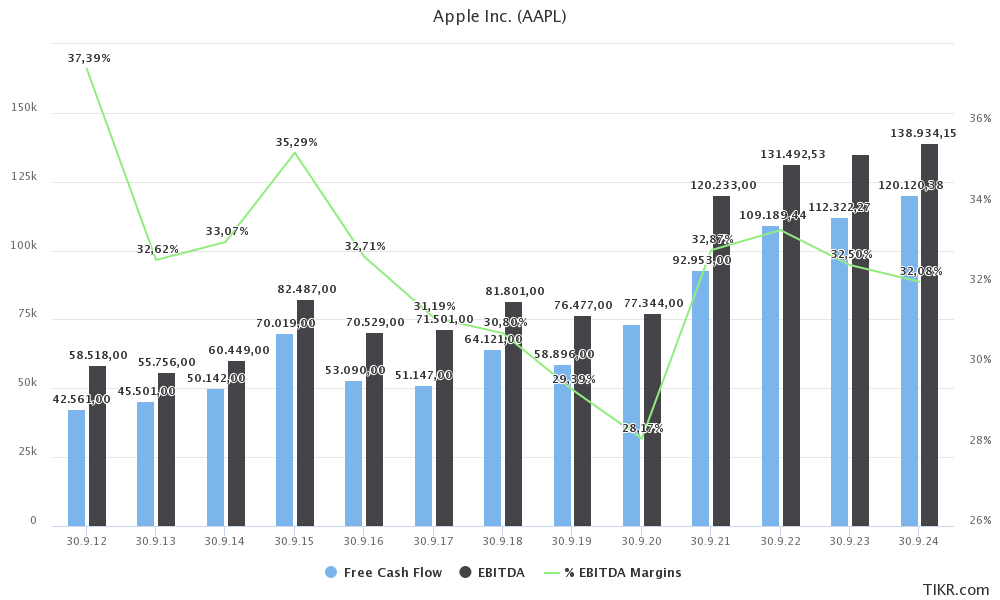

While the company is not expected to be able to maintain its (EBITDA) margins in the years ahead, top-line growth is expected to provide a basis for $112 billion in FY2023 free cash flow and close to $120 billion in FY2024 free cash flow.

TIKR.com

Using $112 billion in expected FCF as an example translates to an implied FCF yield of 5.0% of the company’s $2.23 trillion market cap. In other words, the company could pay a dividend of 5.0% in FY2023 or buy back 5.0% of shares outstanding without using external funding or existing cash reserves.

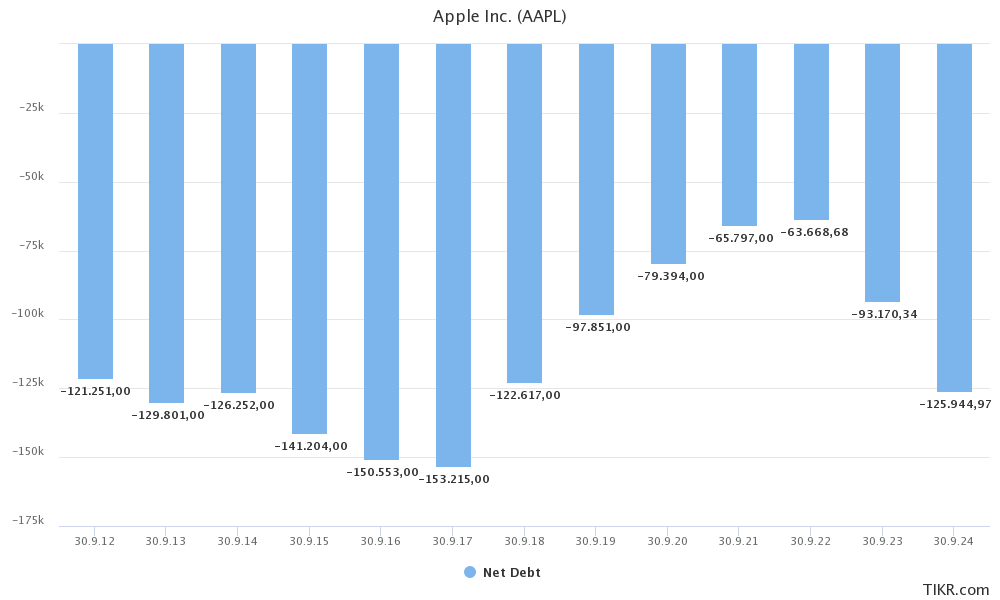

With that said, there’s a lot more cash to distribute. Apple’s target to become net-cash neutral means it will have to distribute not only all of its free cash flow but also its net cash balance. Net cash occurs when a company has more cash than gross debt. It’s negative net debt. Most companies have positive net debt. Apple has more cash than gross debt. At the end of FY2021, the company had $66 billion in net cash. Analysts expect that number to rise to more than $120 billion in the years ahead if the company doesn’t buy back shares rather aggressively.

TIKR.com

It also opens the door to major M&A, which is why people have speculated that Apple may buy a company like Peloton (PTON), which is currently getting crushed on the stock market. However, while Apple isn’t denying looking for bigger opportunities, it seems to work on its own products based on smaller acquisitions, which I believe is the way to go in that space.

We acquire a lot of smaller companies today and we’ll continue to do that for IP and for great talent. And — but we don’t discount doing something larger either if the opportunity presents itself.

Now, onto the valuation.

Valuation & Timing

Apple is down 22.5% year to date, which pushed its market cap to $2.23 trillion. When subtracting $93.2 billion in expected FY2023 net cash, we get an enterprise value of $2.14 trillion.

This is 15.8x next year’s expected EBITDA of $135 billion. 15.8x is still above the company’s pre-pandemic valuation, but well below prices investors were willing to pay in 2021 and most of 2020.

The stock price is now back to where it was in early 2021 after investors pushed the stock to more than $180 at the end of 2021.

FINVIZ

It’s hard to predict where the stock will bottom. If ongoing issues are persistent, we could see $120, which is where the stock found a lot of support in the first half of 2021. Below that, I could see $110.

My strategy is to buy as close to my initial entry as possible ($123.69), if it falls below $120, I will buy more aggressively.

If you’re new to Apple and looking to initiate a position, I think it’s best to break up an initial investment. For example, buy 25% now and add gradually over time. That way investors get to average down if the stock continues its decline while it gives them a foot in the door if the stock suddenly bottoms and takes off.

Takeaway

Apple has gone nowhere since last year as inflation and related factors have made it impossible for growth stocks to continue their post-pandemic uptrend. However, Apple offers a great mix of both growth and value, which is why the damage to its stock price is somewhat limited compared to pure-growth plays. Apple is my favorite tech/consumer stock for a reason, which is its ability to generate a load of cash on top of its already stunning net cash position.

The company is dedicated to distributing its existing cash position and most of its free cash flow via buybacks on top of steadily growing dividends. While the dividend yield is low, I still recommend AAPL to dividend growth investors. As long as investors are not dependent on income from their investment, I have little doubt that investors will enjoy long-term outperforming capital gains thanks to aggressive buybacks and a business model relying on its successful tech products and services.

With that said, the ongoing market environment is tricky. As I explained in this article, the Fed is trying to get inflation down to 2%, which is a tough task due to factors the bank cannot directly influence. As a result, the Fed may have to be more aggressive than anticipated, which could hurt the economy more than expected at a time when consumers are already in a tough spot.

Nonetheless, in order to make Apple a successful long-term investment, we need stock price weakness. The valuation has gotten a lot better and if the stock continues to drop, I will add more aggressively.

Again, the stock market environment isn’t fun, but buying Apple at better valuations is absolutely worth it as it gives us a high chance of long-term outperformance and wealth creation.