tashka2000

Investment Thesis

- Apple (NASDAQ:AAPL) presented strong quarterly results: the company generated a revenue of $90.1B, implying an increase of 8% compared to the same quarter of the previous year.

- Apple’s excellent quarterly results reflect the company’s strong competitive advantages, such as its own ecosystem, strong brand value and high customer loyalty.

- I maintain my buy rating for Apple although the company is currently not cheap.

- According to the HQC Scorecard, Apple can be considered as attractive in terms of risk and reward. At this moment in time, Apple is rated as very attractive in terms of Economic Moat, Profitability, Innovation and Expected Return. In terms of Financial Strength and Growth, the company is rated as attractive. Only in the category of Valuation, is the company rated as moderately attractive.

- In my opinion, Apple is particularly appealing for dividend growth investors. The Seeking Alpha Dividend Grades confirm this statement by showing strong results for the company in the categories of Dividend Growth, Dividend Safety and Dividend Consistency.

- I consider the risk of investing in Apple as being relatively low when you invest with a long investment-horizon.

Apple’s 4Q22 Results

Apple presented strong 4Q22 results: the company, headquartered in Cupertino, California, generated a revenue of $90.1B, which is an increase of 8% compared to the same quarter of the previous year. At the same time, Apple presented quarterly earnings per diluted share of $1.29, implying an increase of 4% when compared to the year before.

Luca Maestri, Apple’s CFO, commented on the company’s results with the following words:

“We continued to invest in our long-term growth plans, generated over $24 billion in operating cash flow, and returned over $29 billion to our shareholders during the quarter. The strength of our ecosystem, unmatched customer loyalty, and record sales spurred our active installed base of devices to a new all-time high. This quarter capped another record-breaking year for Apple, with revenue growing over $28 billion and operating cash flow up $18 billion versus last year.”

Apple’s excellent quarterly figures reinforces my opinion to maintain my buy rating for the company.

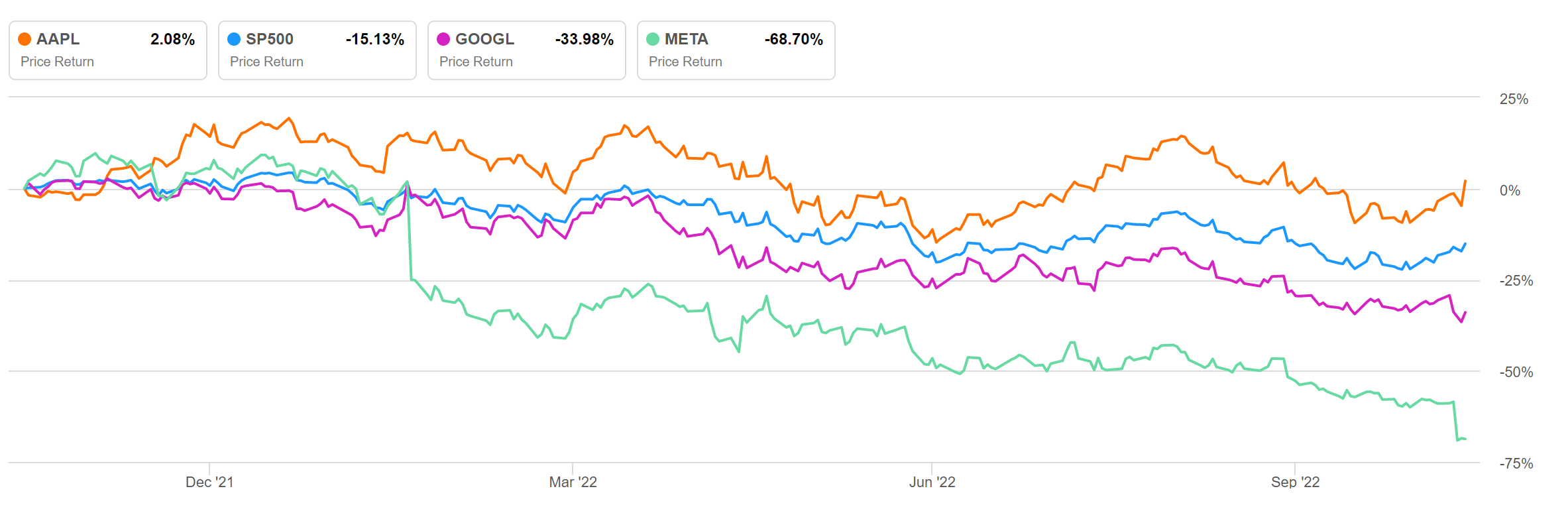

If we compare its performance over the last 12 months with the performance of the S&P 500 index, we obtain the result that Apple is up 2.08%, while the S&P 500 index is down 15.13%. When comparing Apple’s performance with that of other companies from the technology sector, clear differences are visible: Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL) has shown a decline of 33.98% while Meta (NASDAQ:META) has shown a decline of 68.70% over the last 12 months.

Source: Seeking Alpha

The Competitive Advantages and Growth Drivers of Apple

In a previous analysis on Apple, I discussed in more detail the company’s strong competitive advantages. One of its main advantages is the fact that it has successfully established its own ecosystem:

“Apple has succeeded in building a complete ecosystem. This means the system-wide integration of Apple products, which ensures an even better user experience if you own several Apple products. An example of this would be to unlock your Mac with your Apple Watch or to receive messages on all of your Apple devices. I see the company’s own ecosystem as one of its growth drivers in the years to come.”

In my opinion, when evaluating the value of companies, the meaning of a strong brand is often underestimated. For me, considering the brand value of a company is always a crucial factor before taking an investment decision. Its enormous brand value is one of the reasons that I made Apple the largest position of my investment portfolio.

I discussed this enormous brand value in my previous analysis on Apple:

“In various rankings, Apple is listed as the most valuable brand in the world. This is also the case with the Brand Finance ranking of 2022, where Apple is listed with a brand value of $355,085 million, ahead of Amazon (AMZN) (with a brand value of $350,273 million) and Google (GOOG) (GOOGL) ($263,425 million). According to this ranking, Apple’s brand value increased by almost 35% in 2022 compared to 2021. According to Forbes, Apple is also listed as the most valuable brand in the world. Here, Apple is ahead of Google, Microsoft (MSFT) and Amazon.”

Another strong competitive advantage I see for Apple is the fact that the company has successfully proved its ability to integrate other companies from the technology sector into its business. In 2021, Apple CEO Tim Cook explained to the company’s shareholders that Apple had bought about 100 companies in the past six years.

I continue to see Apple’s strong competitive advantages as growth drivers for the company in the years to come and these growth drivers contribute to my buy rating.

The Valuation of Apple

Discounted Cash Flow [DCF]-Model

I have used the DCF Model to determine the intrinsic value of Apple. The method calculates a fair value of $159.89 for the company. Its current stock price of $155.74 gives Apple an upside of 2.7%. In my calculation, I assumed a Revenue and EBIT Growth Rate of 8% for Apple in the upcoming 5 years and calculated with a Perpetual Growth Rate of 4% afterwards. Due to Apple’s strong competitive advantages, I expect the company to grow with a slightly higher Growth Rate than the GDP of the United States (which is 3% on Average).

My calculations are based on these assumptions as presented below (in $ millions except per share items):

|

Apple |

|

|

Company Ticker |

AAPL |

|

Tax Rate |

13.3% |

|

Discount Rate [WACC] |

8.75% |

|

Perpetual Growth Rate |

4% |

|

EV/EBITDA Multiple |

18.1x |

|

Current Price/Share |

$ 155.74 |

|

Shares Outstanding |

16,070 |

|

Debt |

$132,480 |

|

Cash |

$23,646 |

|

Capex |

$10,708 |

Source: The Author

Based on the above, I have calculated the following results for Apple:

Market Value vs. Intrinsic Value

|

Apple |

|

|

Market Value |

$155.74 |

|

Upside |

2.7% |

|

Intrinsic Value |

$159.89 |

Source: The Author

Internal Rate of Return for Apple

The Internal Rate of Return [IRR] is defined as the expected compound annual rate of return earned on an investment. Below you can find the Internal Rate of Return as according to my DCF Model. I assume different purchase prices for the Apple stock.

At Apple’s current stock price of $155.74, my DCF Model indicates an Internal Rate of Return of approximately 10% for the company. (In bold you can see the Internal Rate of Return for Apple’s current stock price of $155.74.)

|

Purchase Price of the Apple Stock |

Internal Rate of Return as according to my DCF Model |

|

$125.00 |

16% |

|

$130.00 |

14% |

|

$135.00 |

13% |

|

$140.00 |

12% |

|

$145.00 |

11% |

|

$150.00 |

11% |

|

$155.74 |

10% |

|

$160.00 |

9% |

|

$165.00 |

8% |

|

$170.00 |

7% |

|

$175.00 |

6% |

|

$180.00 |

6% |

Source: The Author

Please note that the Internal Rates of Return above are a result of the calculations of my DCF Model and changing its assumptions could result in different outcomes.

Apple’s Fundamentals

In the following, I will compare the fundamental data of Apple to some of its competitors:

It can be highlighted that Apple’s market capitalization of $2.45T is higher than its competitors such as Microsoft (with a market capitalization of $1.87T) and Alphabet ($1.20T). It is also significantly higher than the likes of HP (NYSE:HPQ) ($27.74B) or Dell (NYSE:DELL) (27.66B). Apple’s high market capitalization is evidence of its market power and provides an additional indicator that the risk of investing in the company is relatively low when compared to some of its competitors.

Comparing Apple’s EBIT Margin of 30.53% with competitors such as HP (8.71%) or Dell (5.12%), we get further evidence of the company’s excellent competitive position within the Technology Hardware, Storage and Peripherals Industry.

When it comes to growth, we can identify that Apple (with an Average Revenue Growth Rate [CAGR] of 11.64% over the last 5 years) is behind Alphabet (21.95%) and Microsoft (15.41%), but clearly ahead of rivals such as Dell (7.69%) or HP (5.07%).

Apple’s Return on Equity of 175.46% is a strong indicator of the company’s enormous ability to use shareholders equity to generate income. Its Return on Equity is significantly higher than that of both Microsoft (42.88%) and Alphabet (26.89%).

When comparing Apple’s EBITDA of $129.56B with Microsoft ($98.84B), Alphabet ($93.73B), Dell ($8.75B) and HP ($6.42B), it suggests that an investment in the company brings less risks than an investment in those competitors. In the Risks section of this analysis, I will provide further evidence regarding the risk factors Apple investors should take into account before investing.

|

Apple Inc. |

HP Inc. |

Dell Technologies Inc. |

Microsoft Corporation |

||

|

General Information |

Ticker |

AAPL |

HPQ |

DELL |

MSFT |

|

Sector |

Information Technology |

Information Technology |

Information Technology |

Information Technology |

|

|

Industry |

Technology Hardware, Storage and Peripherals |

Technology Hardware, Storage and Peripherals |

Technology Hardware, Storage and Peripherals |

Systems Software |

|

|

Market Cap |

2.45T |

27.74B |

27.66B |

1.87T |

|

|

Profitability |

EBIT Margin |

30.53% |

8.71% |

5.12% |

41.69% |

|

ROE |

175.46% |

NM |

145.49% |

42.88% |

|

|

Valuation |

P/E GAAP [FWD] |

24.46 |

7.53 |

10.05 |

24.31 |

|

Growth |

Revenue Growth 3 Year [CAGR] |

14.37% |

3.37% |

5.30% |

16.09% |

|

Revenue Growth 5 Year [CAGR] |

11.64% |

5.07% |

7.69% |

15.41% |

|

|

EBIT Growth 3 Year [CAGR] |

22.47% |

9.93% |

41.71% |

22.83% |

|

|

EPS Growth Diluted [FWD] |

25.22% |

17.67% |

-4.44% |

12.61% |

|

|

Dividends |

Dividend Yield [FWD] |

0.62% |

3.64% |

3.49% |

1.18% |

|

Dividend Growth 3 Yr [CAGR] |

6.27% |

15.99% |

– |

10.46% |

|

|

Dividend Growth 5 Yr [CAGR] |

8.45% |

13.50% |

– |

9.71% |

|

|

Consecutive Years of Dividend Growth |

8 Years |

11 Years |

0 Years |

17 Years |

|

|

Income Statement |

Revenue |

387.54B |

64.86B |

106.96B |

203.07B |

|

EBITDA |

129.56B |

6.42B |

8.75B |

98.84B |

|

|

Balance Sheet |

Total Debt to Equity Ratio |

205.98% |

NM |

NM |

44.44% |

Source: Seeking Alpha

The High-Quality Company [HQC] Scorecard

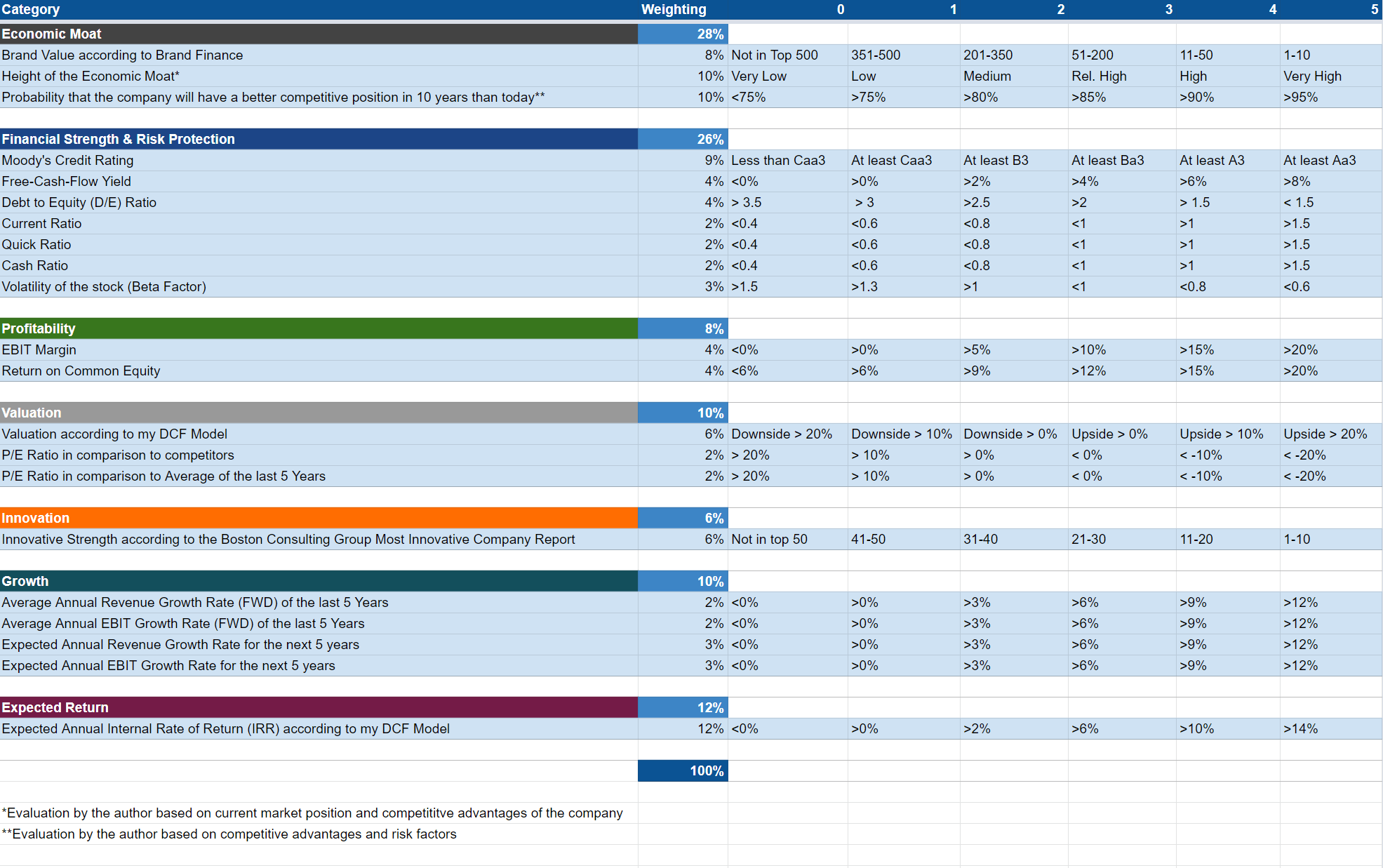

The aim of the HQC Scorecard that I have developed is to help investors identify companies which are attractive long-term investments in terms of risk and reward.

Overview of the Items on the HQC Scorecard

In the graphic below, you can find the individual items and weighting for each category of the HQC Scorecard. A score between 0 and 5 is given (with 0 being the lowest rating and 5 the highest) for each item on the Scorecard. Furthermore, you can see the conditions that must be met for each point of every rated item.

Source: The Author

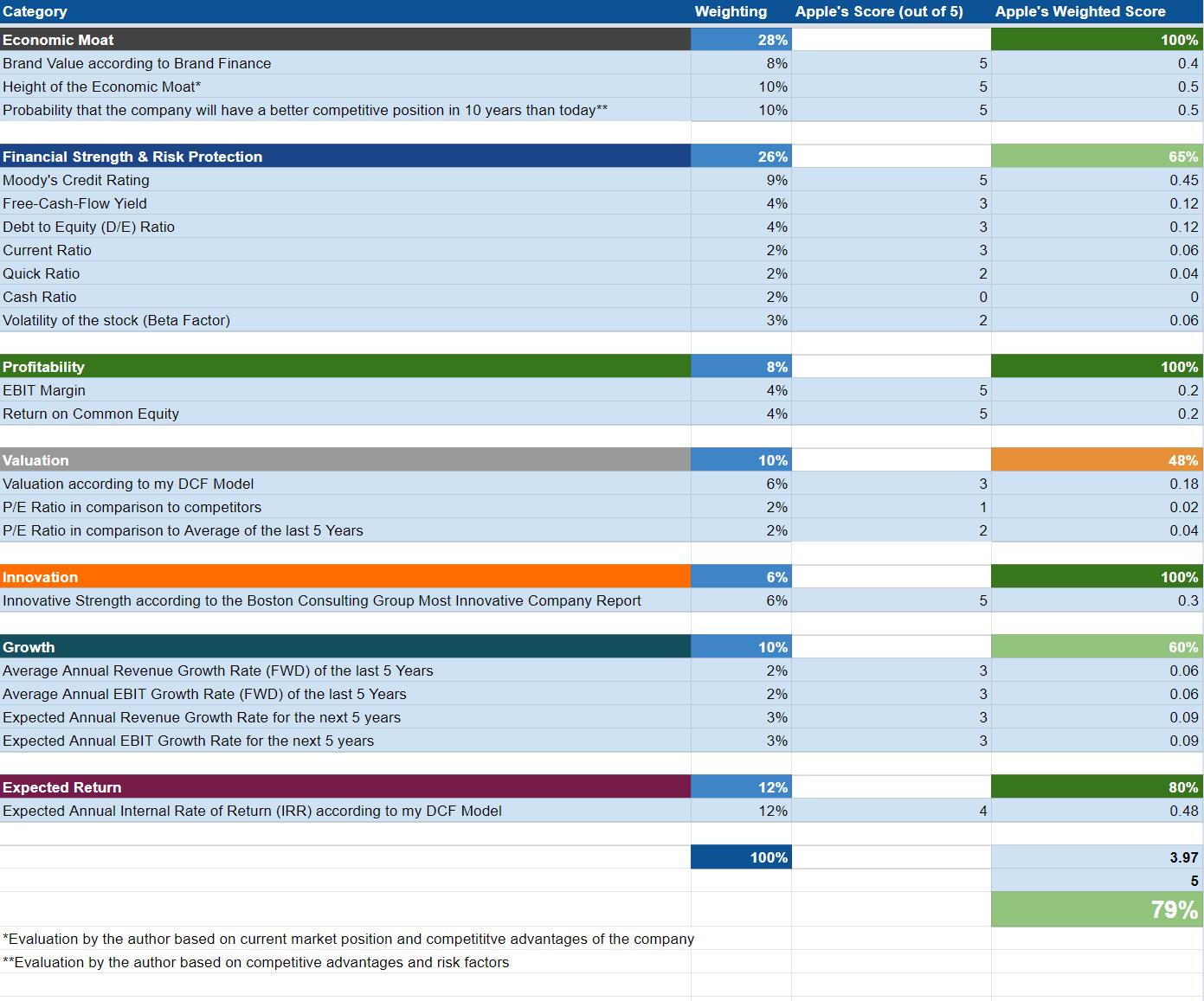

Apple According to the HQC Scorecard

Source: The Author

At this moment in time, Apple receives 79/100 points as according to the HQC Scorecard. This is an attractive rating in terms of risk and reward.

In the categories of Economic Moat, Profitability and Innovation, Apple receives the highest possible rating (100/100 in each).

In the category of Expected Return, Apple receives 80/100 points, implying a very attractive rating in terms of risk and reward.

In the categories of Financial Strength (65/100) and Growth (60/100), Apple is ranked as attractive.

Only in the category of Valuation (48/100), is Apple ranked as moderately attractive in terms of risk and reward.

Compared to when I analyzed Apple back in June, the company currently scores 79/100 points while it scored 85/100 points in June. Apple’s currently lower valuation as according to the Scorecard, is particularly a result of the company’s lower scoring in the category of Valuation.

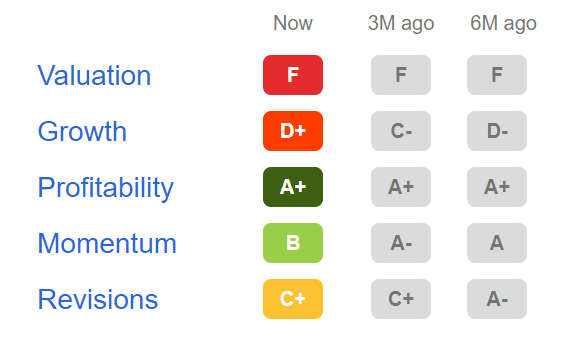

Apple According to the Seeking Alpha Quant Factor Grades

In the following, I will look at the Seeking Alpha Factor Grades. When it comes to Valuation, Apple is currently rated with an F. For Growth, Apple receives a D+ rating. For Profitability, Apple gets an A+ and for Momentum, a B. For Revisions, the company gets a C+ rating.

Source: Seeking Alpha

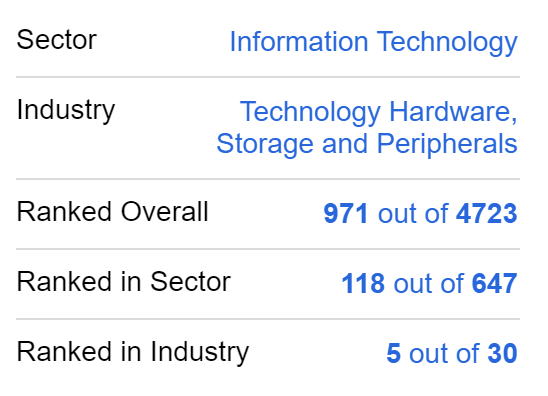

Apple According to the Seeking Alpha Quant Ranking

Let’s take a look at the Seeking Alpha Quant Ranking: Apple is ranked 5th (out of 30) within the Industry of Technology Hardware, Storage and Peripherals and 118th (out of 647) within the Information Technology Sector. In the overall ranking, Apple is ranked 971st out of 4723.

Source: Seeking Alpha

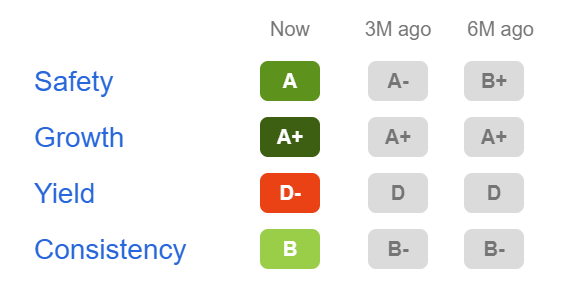

Apple According to the Seeking Alpha Dividend Grades

The Seeking Alpha Dividend Grades shows strong evidence for the fact that Apple is a great pick for dividend growth investors: for Dividend Safety, Apple is ranked with an A rating. For Dividend Growth, it gets an A+ rating. For Dividend Yield, the company receives a D- and for Dividend Consistency, a B.

Source: Seeking Alpha

Risks

In my opinion, there are several risk factors, that investors should take into consideration when deciding whether or not to invest in Apple. In my previous analysis on the company, I discussed that I see the biggest risk for investors being if an event would cause its brand value to decrease. In this case, a lower brand value could have enormous consequences for the company’s financial results.

Another risk factor I see are the current macroeconomic risk factors for the company that could also cause its profit margins to decrease. However, I see this kind of risk to be less for long-term investors: over the long-term, the price of the stock will follow the company’s profits. For this reason, I would suggest that you look at Apple as a long-term investment and invest into the company with a time horizon of at least 7 years.

An additional risk factor for Apple is the intense competition that the company faces in the different industries in which it operates. I discussed this topic in more detail in my analysis on Apple in the month of June.

“An additional risk factor for Apple is the fact that the company operates in a large variety of industries. To name just a few, it operates in the desktop, laptop and tablet computer market as well as in the smartphone industry. Apple’s presence in different segments makes the company compete with a large number of companies such as HP (HPQ), Samsung (OTC:SSNLF), Dell (DELL) and Lenovo (OTCPK:LNVGY) among many others.”

However, due to Apple’s strong competitive advantages, that help the company to build an economic moat over its competitors, I see the risk of investing in Apple as being relatively low when investing with a long investment-horizon. The relatively low risk of investing in Apple strengthens my theory to rate the company as a buy. The HQC Scorecard confirms Apple’s strong economic moat while rating the company with the highest possible rating in this category (100/100). The Scorecard also confirms that Apple is an attractive choice regarding risks and reward (rating the company with 79/100 points).

The Bottom Line

Apple’s excellent quarterly results reflect the strong competitive advantages it has over its competitors. Even though its valuation (with a P/E [FWD] Ratio of 24.46) is not low, I continue my buy rating on the Apple stock.

In my opinion, Apple’s strong competitive advantages will contribute to the growth of the company in the upcoming years: particularly, the company’s creation of its own ecosystem, strong brand value, and high customer loyalty. I have shown in the Risk section of this analysis, that I see the risk of investing in Apple as being relatively low when investing with a long-term investment horizon.

From my point of view, Apple is a great choice for dividend growth investors that plan to benefit continuously from the receipt of a growing dividend. The Seeking Alpha Dividend Grades confirm the strength of Apple’s dividend while rating the company with an A+ for Dividend Growth, an A for Dividend Safety and a B for Dividend Consistency.

My buy rating for the Apple stock is also underlined by the fact that the company is the largest position of my own investment portfolio.