On-chain data from Glassnode suggests the role of Bitcoin miners in the asset’s valuation has been going down over the years.

Bitcoin Miners’ Issuance Now Only Makes A Small Part Of Daily Realized Value

In a new report, the on-chain analytics firm Glassnode has studied the different components that contribute to Bitcoin’s “realized cap.” The realized cap is a capitalization model for the asset that assumes that the real value of any coin in circulation is the price at which it was last transacted on the blockchain.

This is different from the normal market cap, which simply takes every token’s value to be the same: the current spot price. Since the last transaction price of a coin is essentially its “buying price,” the realized cap serves as a measure of the aggregate value stored inside the cryptocurrency.

Another way to look at the realized cap is through the three metrics it essentially represents: the realized profit, realized loss, and issuance. The realized profit and loss metrics are self-explanatory: they keep track of the profits and losses that the investors have been harvesting through their selling.

Since the act of loss-taking or profit-taking reprices the tokens being sold at a lower or higher price, it naturally affects the realized cap. The third indicator of interest here, the issuance, represents the fresh supply that the miners are minting.

These chain validators “issue” supply in the form of the block rewards that they receive for solving blocks on the network. Any coins freshly minted are priced the same as the spot price at the time their block was found.

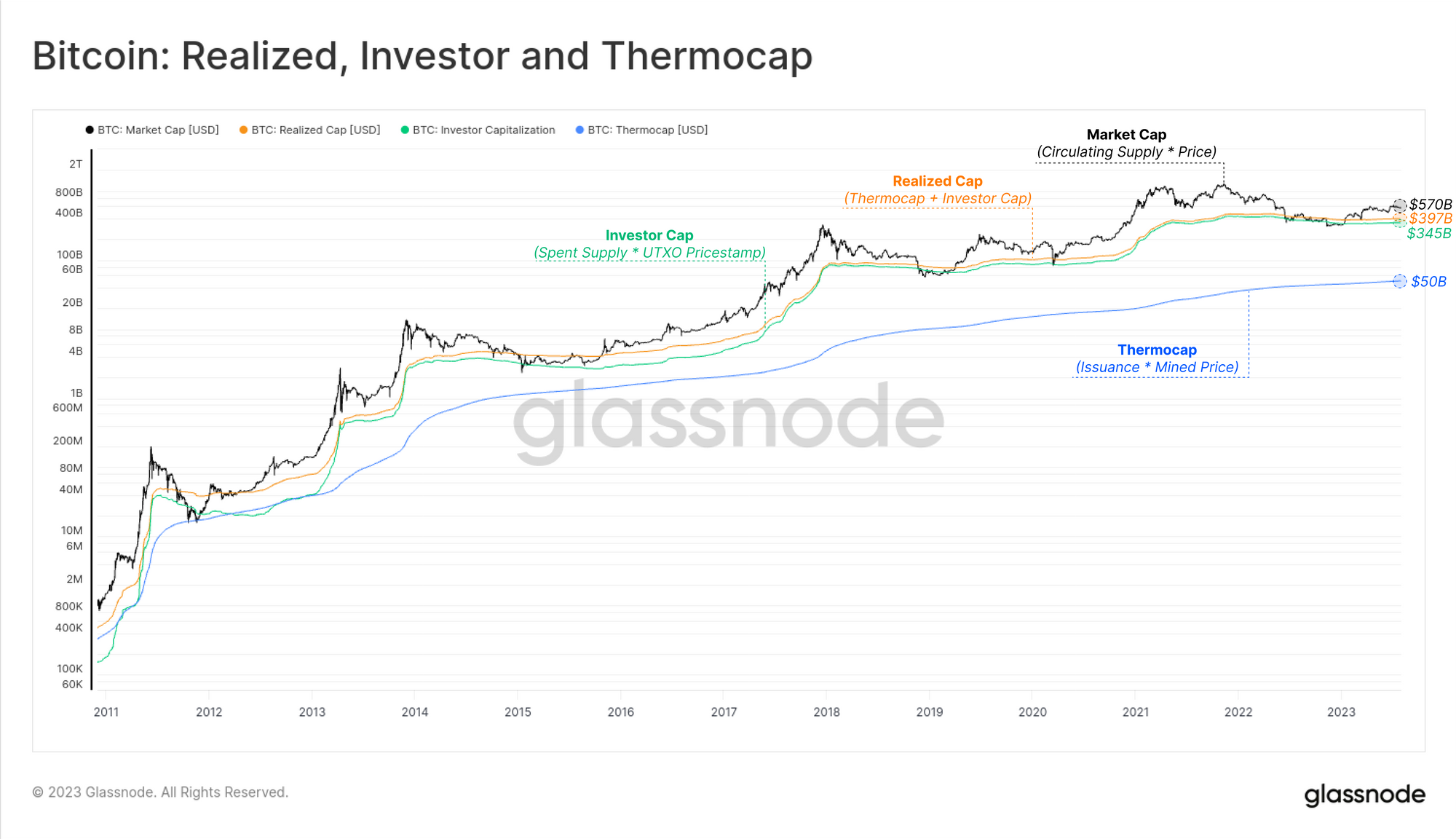

Now, here is a chart that shows how the aggregate issuance (called the “thermocap” here) has compared against the net profit/loss that the holders have been realizing (the “investor cap”) and the realized cap over the years:

The trend in the realized, investor, and thermo caps | Source: Glassnode

From the graph, it’s visible that the thermocap didn’t have as much of a gap from the others in the early years of the cryptocurrency, but lately, the metric has significantly diverged.

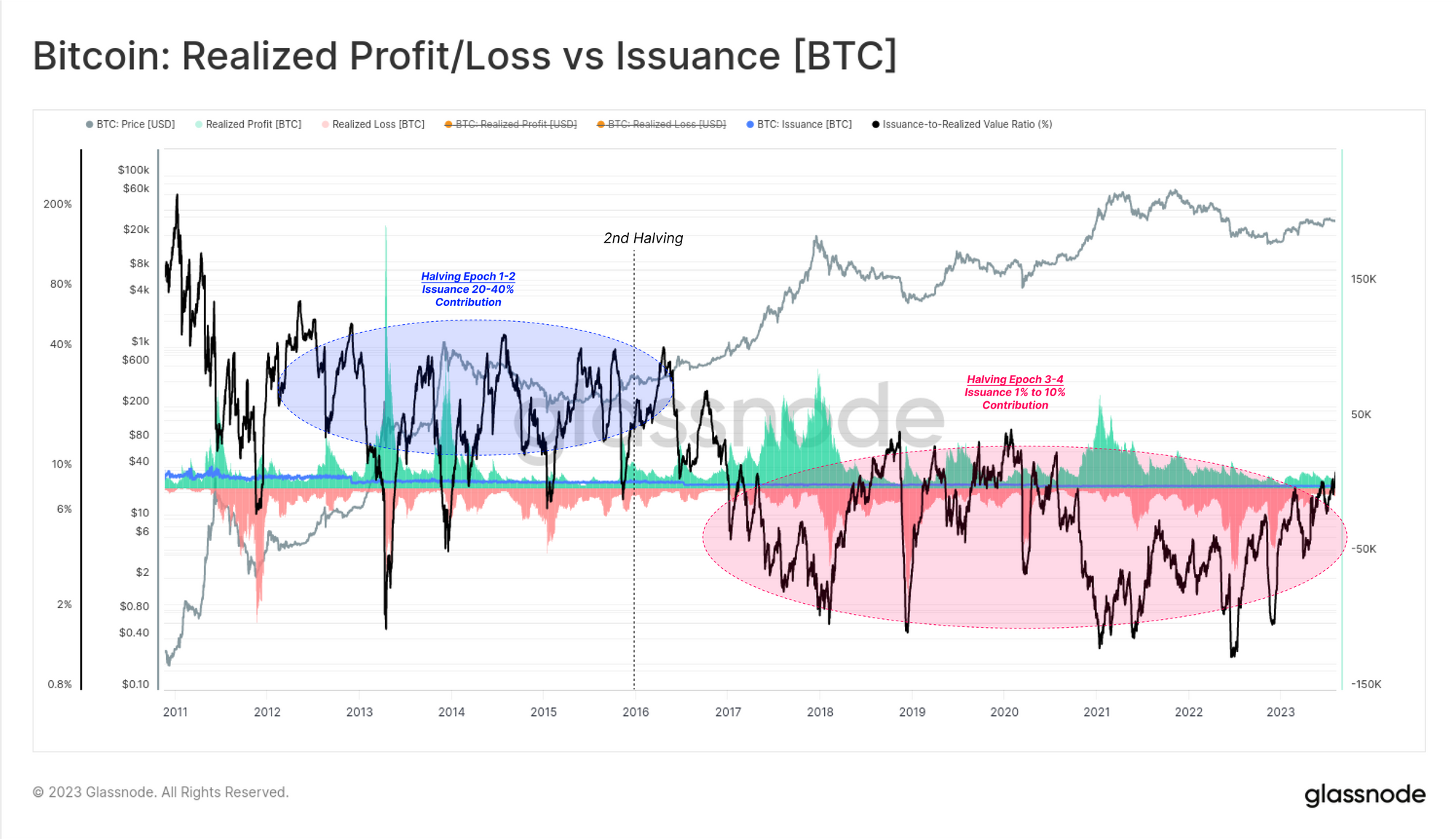

“In modern times, the Thermocap accounts for just 8.7% of the total value stored within the Realized Cap,” explains Glassnode. To better see how the role of the miners has changed, the analytics firm has shared another chart; this time for the issuance’s daily contribution.

Looks like the issuance doesn't make up too much of the metric | Source: Glassnode

Up until Bitcoin’s second halving in 2016, the Bitcoin miners were responsible for 20% to 40% of the net value entering or exiting BTC every day. As the market has matured further and the miners’ block rewards have been cut down in the halvings, the indicator’s contribution has observed a notable decline.

In recent years, the issuance’s contribution towards the daily realized value has often been as low as 1-2% and has only reached a high of 10% during specific periods.

“The influence of miners and new issuance can therefore be argued to be most meaningful during periods of exceptionally light liquidity and minimal trade volume,” notes Glassnode. “This is often pro-cyclical, with miner distribution pressures reaching a relative maxima during late stage bear markets when investor attention/demand is at its weakest.”

BTC Price

Bitcoin has steadily been climbing during the past few days as the asset has now recovered back towards the $26,400 level.

BTC has been slowly, but surely, rising recently | Source: BTCUSD on TradingView

Featured image from Brian Wangenheim on Unsplash.com, charts from TradingView.com, Glassnode.com