artiemedvedev/iStock via Getty Images

Looking back, Bitfarms (BITF) has a strong history of production and growing profitability mining the Bitcoin (BTC-USD) network. This success was based on acquiring reasonably priced hydroelectricity in Canada and securing bulk contracts for ASIC miners from suppliers like MicroBT. The chart below shows the proven-out production capacity during 2021. And though there are moderately different mining economics, balance sheets, and expansion plans, as a basic overview, the chart also compares Bitfarms to two of its close peers.

| Bitfarms | Marathon Digital (MARA) | Riot Blockchain (RIOT) | |

| Bitcoins Mined In 2021 | 3452 | 3197 | 3812 |

| March 2022 Market Cap | $650M | $2340M | $1740M |

But what about going forward, can Bitfarms defend and expand its share to maintain earnings power? The article below first gives a viewpoint on the competition and where the total network hash rate is headed this year. Also considered are Bitfarms’ plans for acquiring access to additional low-cost electricity, primarily through their Cordoba, Argentina expansion. Briefly toward the end, the delivery schedule and costs for the currently contracted mining equipment are covered. And as a conclusion, these two major costs are put into perspective alongside the balance sheet, earnings, and market capitalization.

The Competition In Aggregate

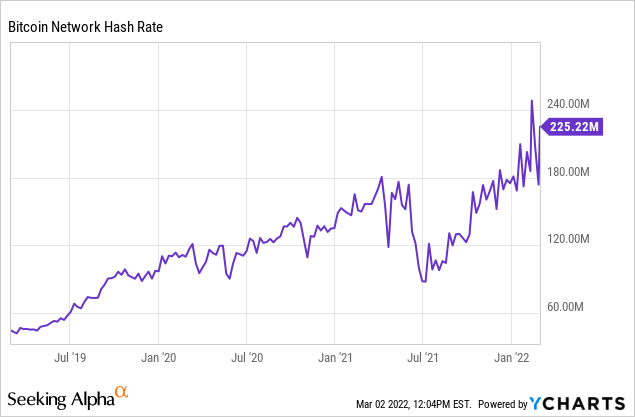

The key metric of competition in the Bitcoin network mining space is hash rate, a measure of computation power per second. Slightly simplified, a miner’s deployed and fully operating hash rate can be compared to the total network hash rate to find the company’s reward share. For a reference on the size of the “market”, on average, there are 144 blocks completed each day, and each block rewards 6.25 bitcoins.

Bitfarms’ current maximum hash rate is 2.3 EH/s (ExaHash), sometimes seen denominated as 2300 PH/s (PetaHash). The total network hash rate is approximately 225 million TH/s (TeraHash); note that this rate is derived from on-chain metrics and is inexact and volatile. There are a million TeraHash in an ExaHash, so Bitfarms has just over 1% share.

Mainly because of Bitcoin’s tripling in price at the end of 2020, Bitfarms’ gross margins went from negative to over 20%. The sustained high prices in 2021, above $30,000 per coin, kept Bitfarms’ gross margins over 60% during the first three quarters (Q4’21 to report this month).

The same high profitability environment held true across the industry. This led to a race to acquire more electrical power, as well as obtain new mining equipment. This general idea is demonstrated by the rapid expansion of the total network hash rate seen in the graph above. Note that the large downward spike in the rate during the summer of 2021 was caused by a crackdown on the Bitcoin network, and its mining, by Chinese regulators. And the quick rebound can be explained by Chinese miners migrating equipment abroad to other energy sources in countries like the US and Kazakhstan.

So what is the outlook for the total network hash rate in 2022? Industry participants are looking for the rate to double over twelve months.

One such observer is Rob Chang, CEO of bitcoin miner Gryphon Mining, who thinks it’s possible for the hashrate to reach 300 EH/s by the end of 2022. Meanwhile, Ben Gagnon, chief mining officer of Bitfarms, expects the hashrate to be between 300 and 350 EH/s by the end of next year. Bekbau of Xive also anticipates the hashrate doubling in 2022.

8 Trends That Will Shape Bitcoin Mining in 2022, coindesk.com, 12/15/2021

To counter this expected doubling in the total network hash rate, Bitfarms has reasonably priced, in progress, and somewhat proven plans to more than triple their hash rate over the next ten months. As discussed below, Bitfarms plans are slated to take their hash rate to 8 EH/s by year-end, which would represent a 2% share even if the total network reaches 400 million TH/s.

Argentina and Quebec Electrical Power Expansions

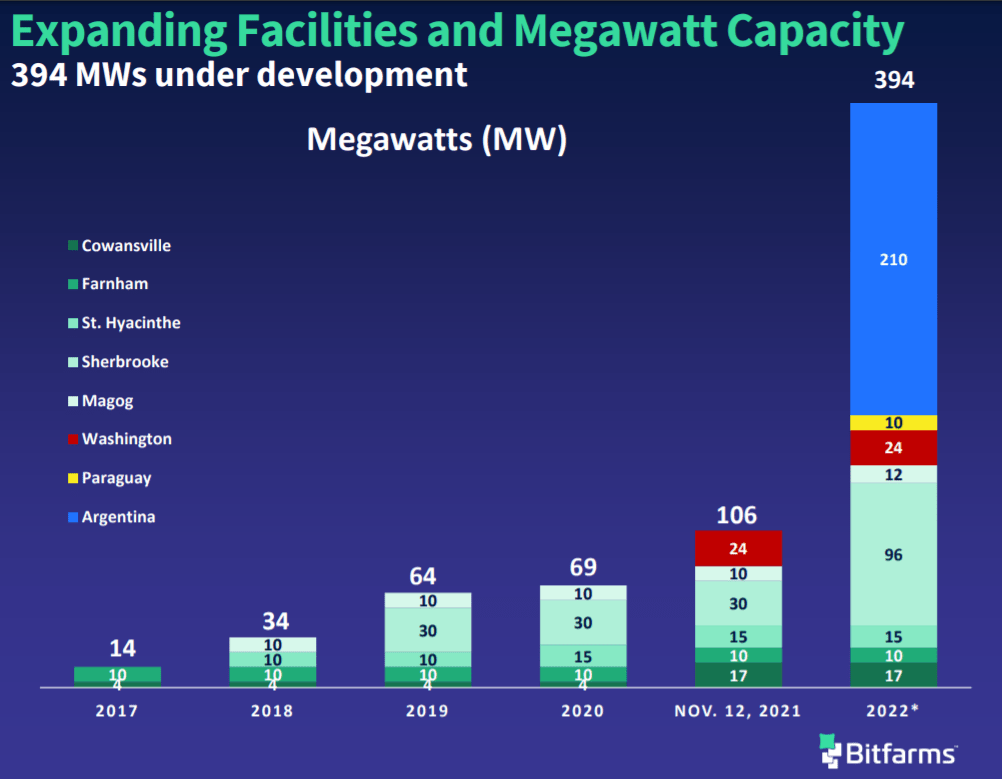

Last spring Bitfarms entered an agreement with a private power producer in Argentina for up to 210 MW. While there are various regulatory uncertainties in Argentina, there is an increasingly vital and growing crypto community. Energy prices are low and during the first four years of the eight-year power agreement, the cost per kilowatt-hour will be $.022. This compares well to Bitfarms’ current average price near $.04 per kilowatt-hour. Also, for about $100,000 per year, Bitfarms is leasing property on the grounds of the power producer to construct its mining facilities. Here it is useful to note that Bitfarms’ founder Emiliano Grodzki is from Argentina and began investing and mining there in 2016.

This past fall, Bitfarms contracted with two companies to design and build the facilities in Argentina. Construction has begun and is slated to be completed in stages by the end of this year. The costs are estimated to run about $50 million. When completed, the facilities are designed to house 55,000 miners with 5.5 EH/s of production. A large portion of the MicroBT equipment discussed in the next section is earmarked for these facilities.

Megawatts Projected 2022 (Bitfarms)

In addition to Argentina, Bitfarms is expanding its facilities in Sherbrooke, Canada from 30 MW to an eventual 96 MW at three new locations. Because of noise complaints from the community, current operations will move into new facilities and the existing building will likely be sold for approximately $2.4 million. Construction and buildout on the first 78 MW are split between two sites (Bunker and Leger) and are estimated to cost between $17-19 million. This month should see .7 EH/s of new hash rate come online at the two sites. Bitfarms will also identify and build a third site for the remaining 18 MW available by contract with Hydro Sherbrooke.

MicroBT Whatsminer Rig Deliveries

Bitfarms’ largest capital cost and current constraint on hash rate growth is equipment acquisition. The company is projecting that deliveries by year-end will bring their hash rate to 8.0 EH/s.

The primary equipment additions this year will be 48,000 Whatsminers from MicroBT. At the end of Q3’21, the company had already placed $75 million in deposits for mining equipment. The chart below shows the schedule of remaining payments on the Whatsminers, note the data is in 1000s of USD. Each month about 4000 units are expected for delivery. Bitfarms has a meaningful history and cooperative relationship with MicroBT and last year became their first official service partner in Canada.

in 1000s (Bitfarms)

The company also recently purchased 6100 late model Bitmain Antminers. Interestingly, these miners will be financed with a somewhat high rate, though shorter-term loan secured by the equipment itself. The deal with BlockFi is representative of Bitfarms’ diversified financing strategy, which is increasingly non-dilutive. Recall that in December the company secured a $100 million credit facility from Galaxy Digital that is collateralized by their holdings of bitcoins.

Putting The Numbers Into Perspective

At the time of writing, Bitfarms’ volatile market capitalization was $650 million. To think about if this is pricey or represents a value, consider the following balance sheet and EBITDA discussions. And note that there are obviously numerous moving parts and flows. Plus, the view is somewhat out of date, primarily using data from the end of Q3’21. It will be useful to revisit this process following the Q4 report in the coming weeks.

Balance Sheet Overview

Liquidity on Sept. 30, 2021 was $43 million in cash and $101 million in digital assets. But for perspective, note at the end of February, the company held 4886 bitcoins worth $200 million. In addition to the mining equipment deposits discussed in the prior section, by Q3’21, the company had already made a few million in deposits toward 2022 property and plant costs. Debts, the majority being due this year, were just over $12 million and there is another $12 million in lease obligations in the coming few years. So simplified net assets, excluding the mining equipment deposits, were about $115 million at the end of Q3’21.

Going forward, it is useful to contrast this net asset figure with the major expansion costs discussed above, which include $65 million for facilities and $155 million remaining on the MicroBT miners. This is especially relevant as a large portion of the expansion is going to be financed and meaningfully increase the long-term debt. However, it is useful to note that the debt ratio looks to remain reasonable (below 1) with digital assets growth offsetting new debt.

Adjusted EBITDA

Bitfarms’ valuation multiples are low and falling. Seeking Alpha’s Quant Ratings lists forward Non-GAAP P/E at 14 and forward EV to EBIT at 8. The graph below shows EV to EBITDA [TTM]; note the overall trajectory despite the fluctuations in the company’s market cap. Bitfarms’ earnings are growing and are now relatively large compared to its market cap.

EV/EBITDA TTM (Seeking Alpha)

The table below breaks out EBITDA information for Q3 of last year and for the combined first three quarters. Full-year adjusted EBITDA likely surpassed $100 million (Q4 reports in March). In a ratio to both the planned increase in debt and to the $650 million market cap, this earnings total compares favorably and “conservatively”.

Adjusted EBITDA (Bitfarms)

Though the underlying price per bitcoin is now down from the 2021 average, Bitfarms’ share capture explained above should drive total coins mined in 2022 over 5000. This increase would fully offset the less favorable price environment and maintain earnings potential. Because Bitfarms is trading at a low multiple to these earnings, has well-planned and meaningful growth plans, plus a solid balance sheet, it is my top pick among the miners and leveraged Bitcoin plays.

Author Note: When thinking about Bitcoin mining earnings, there are useful reasons to exclude items such as gains and losses caused by the changes in the valuation of digital assets held, costs associated with share-based compensation, or even the depreciation on quickly obsolete equipment. However, while preparing this article, I happened to listen to Warren Buffett’s recent message to the shareholders of Berkshire Hathaway. While talking about their railroad, BNSF, Buffett gave the following colorful warning on adjusted earnings that I thought worth sharing.

..old-fashioned sort of earnings that we favor: a figure calculated after interest, taxes, depreciation, amortization and all forms of compensation.

..Deceptive “adjustments” to earnings – to use a polite description – have become both more frequent and more fanciful as stocks have risen. Speaking less politely, I would say that bull markets breed bloviated bull ___.