luza studios

Bitfarms Ltd. (NASDAQ:BITF) is one of the world’s largest Bitcoin mining companies with its operating hash rate representing approximately 2% of the global Bitcoin network. While the stock had a heyday back in 2021 reaching a peak market value above $1.5 billion, the setup here has been a disaster with shares losing more than 90% in 2022 amid the crash in Bitcoin (BTC-USD) prices. In hindsight, it’s clear expectations for the company and the broader sector got ahead of themselves.

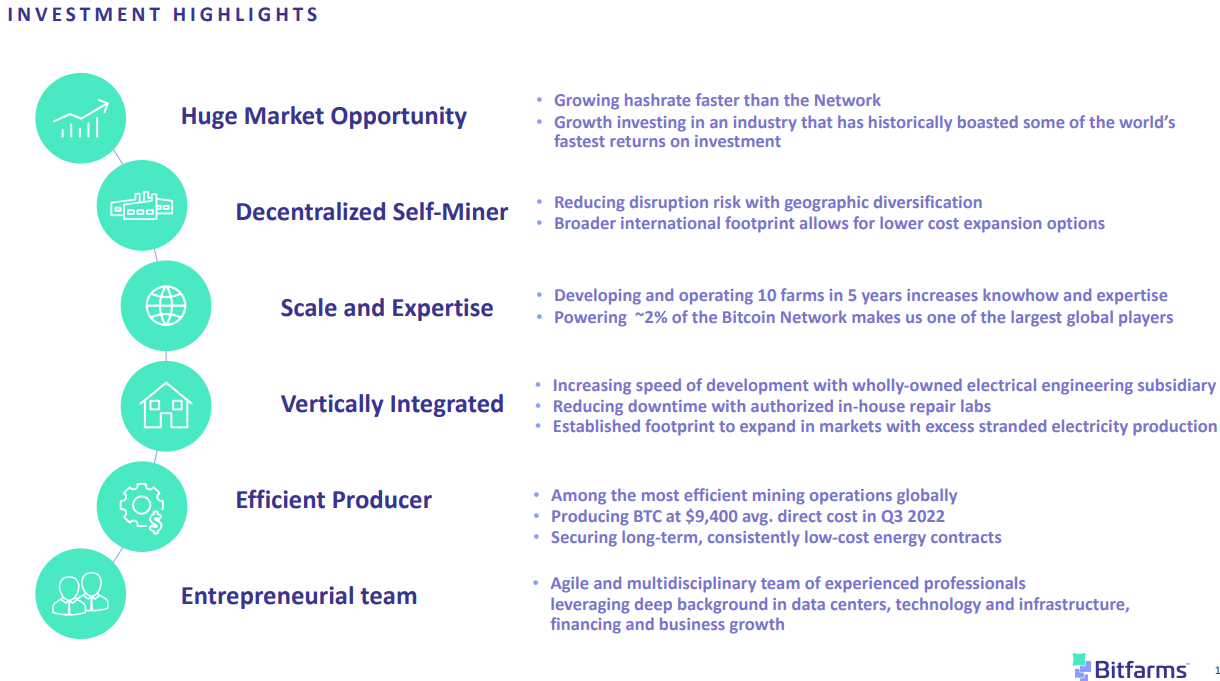

That being said, Bitfarms holds its place as a survivor with the operation moving along, and in our opinion, one of the better names in this highly speculative segment. Its business model as a “self-miner” by not relying on outsourced hosting or even offering mining services to other parties has proven to be an advantage considering those steps led to some high-profile bankruptcies among other industry players.

There’s no easy turnaround for Bitfarms which is now dependent on a sustained rally in the price of Bitcoin for its long-term success. Still, we can point to what are some encouraging fundamentals including continued mining growth and positive operating cash flows even in the current pricing environment. A relatively large balance sheet position of cash and BTC holdings brushes aside any solvency fears meaning BITF will remain relevant for the foreseeable future.

BITF Key Metrics

We mentioned Bitfarms being a self-miner meaning the company builds out the data centers where its Bitcoin mining machines are located. This strategy is in contrast to others in the industry that took an alternative path by either contracting with third-party hosting suppliers like what Marathon Digital Holdings, Inc. (MARA) has done or even the more ambitious model of playing both sides by mining and offering mining-as-a-service which was the death sentence of Core-Scientific (CORZ).

In the case of MARA, the company’s hosting provider “Compute North” went bankrupt amid the surge in energy prices as a cost coupled with the drop in Bitcoin led to a collapse in demand for its services. MARA had partnered with Compute North on the development of new projects with the disruptions representing a setback to its expansion plans. Core-Scientific, once seen as a sector “blue-chip” given its scale, also got crushed by extreme energy prices at its Texas facilities, although it was the large debt that ultimately led to the company filing Chapter 11 just this month.

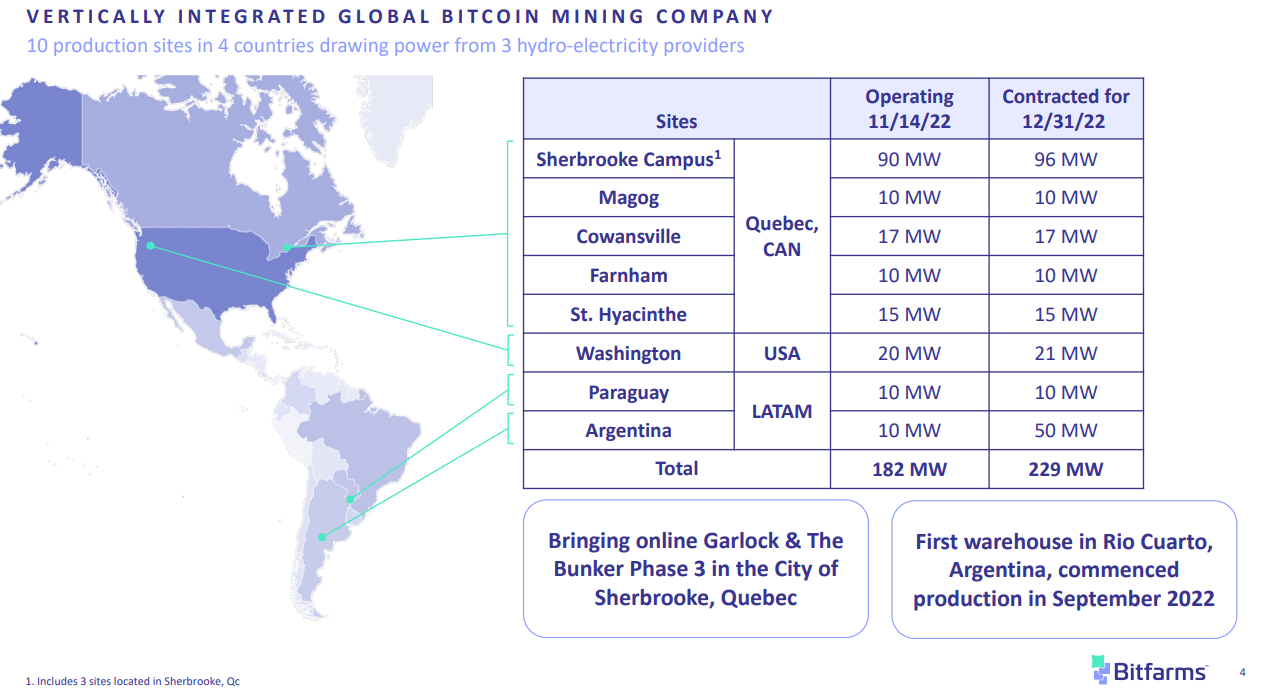

In this regard, Bitfarms benefits from its vertical integration by focusing on setting up and managing its production facilities while avoiding hosting arrangements. Currently, the company has 10 sites across Canada, the U.S., and Latin America sourcing renewable energy, mostly through hydroelectric power purchase agreements.

Company IR

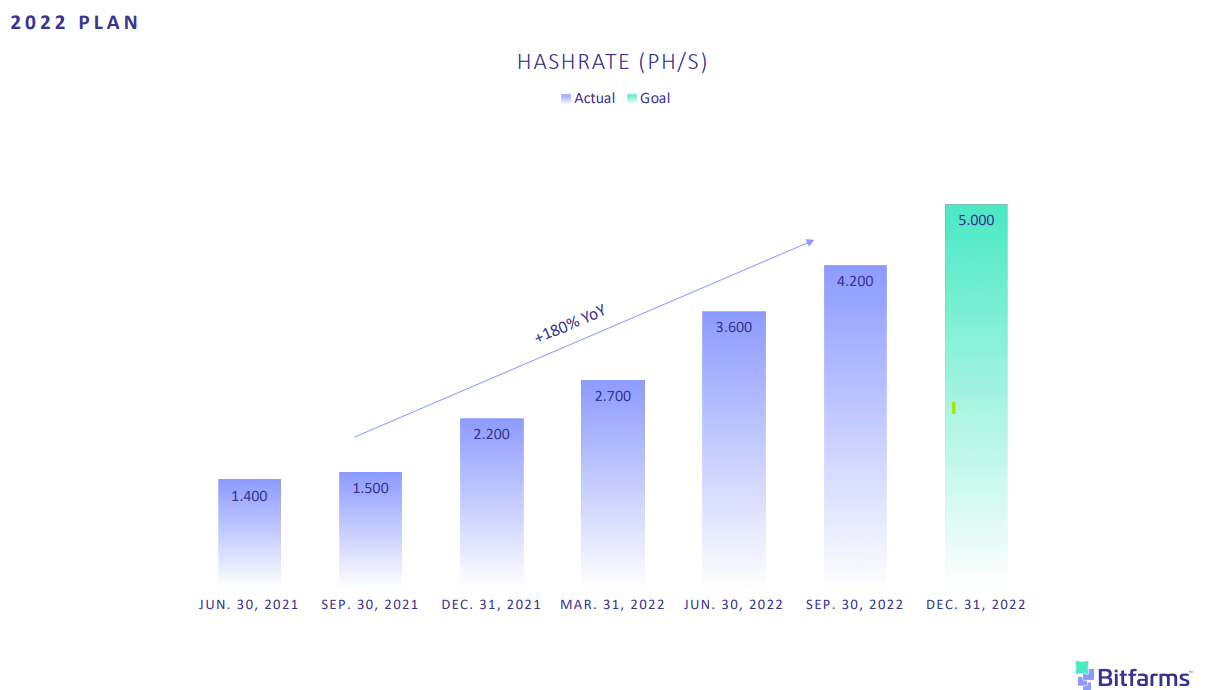

The latest update was that the company was on track to operate 188 MW of power through the year-end of 2022 implying a Bitcoin mining hash rate capacity of 5.0 exahash compared to 4.4 EH/s in November. The result is nearly double the operation Bitfarms presented at the end of 2021. In Q3, the company installed its latest delivery of 7,000 ” MicroBT Whatsminers” mining rigs which added approximately 0.8EH/s.

Company IR

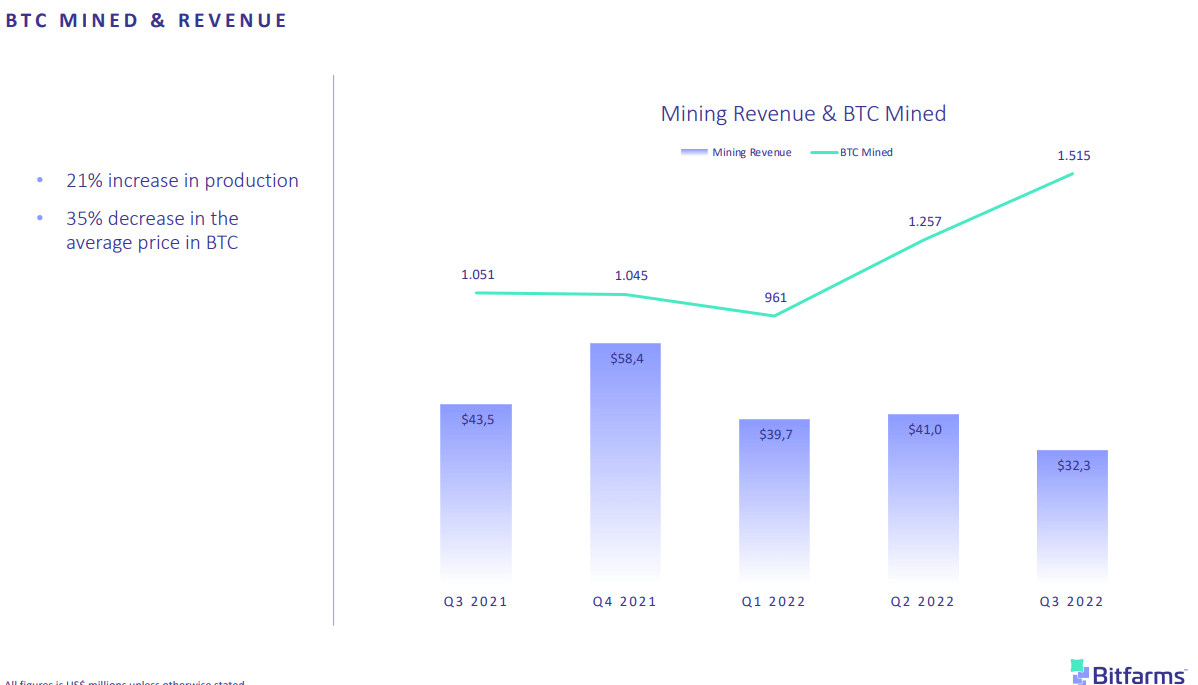

On the other hand, even as Bitfarms produced 1,515 BTC in Q3, up 21% from Q2 and 45% y/y, the momentum hasn’t been able to escape the sharply lower BTC pricing. Q3 revenue at $32.3 million was down from a peak of $58.4 million in Q4 2021 which was at the height of the Bitcoin cycle.

Company IR

An important point here is that Bitfarms reported a Q3 Bitcoin production cost of $9,400 BTC, which has climbed 18% from the end of last year. Part of this reflects the climbing network difficulty along with modest energy and FX volatility. The figure ticked lower by 5% from Q2 based on some operational efficiency with the mix of production into lower-cost sites. Management notes that it remains among the lowest-cost producers among publicly reporting miners.

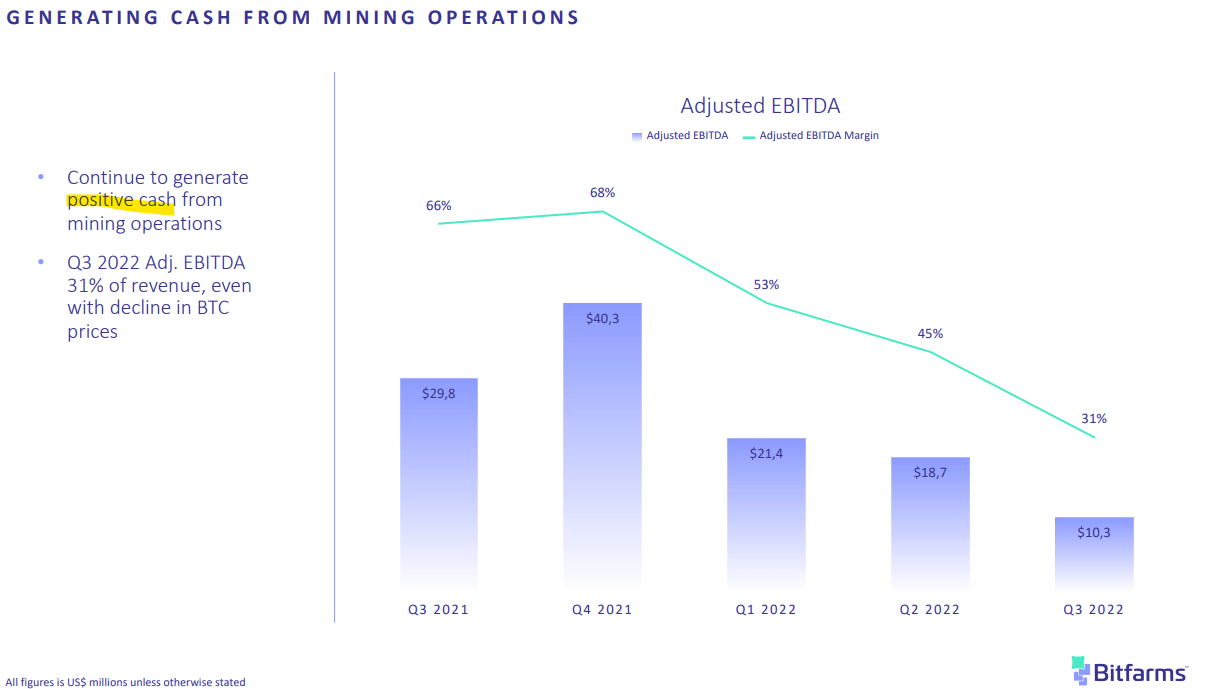

The bigger takeaway is that the underlying mining business remains profitable while acknowledging the margin above breakeven has gotten tighter. Q3 adjusted EBITDA at $10.2 million and 31% margin is down from the Q4 2021 peak of $40.3 million and 68% margin. This trend largely explains the poor stock price performance, with BTC prices above $50k in 2021 a completely different reality in terms of potential profitability.

Company IR

The company ended Q3 with $36 million in cash and 2,064 BTC on the balance sheet forming its total liquidity at $76 million at the end of the period against $86 million in total long-term debt. One of the strategies being employed to deal with the ongoing expansion efforts has been to regularly sell its Bitcoin production and a portion of its holdings as a method to generate cash as part of its financing strategy.

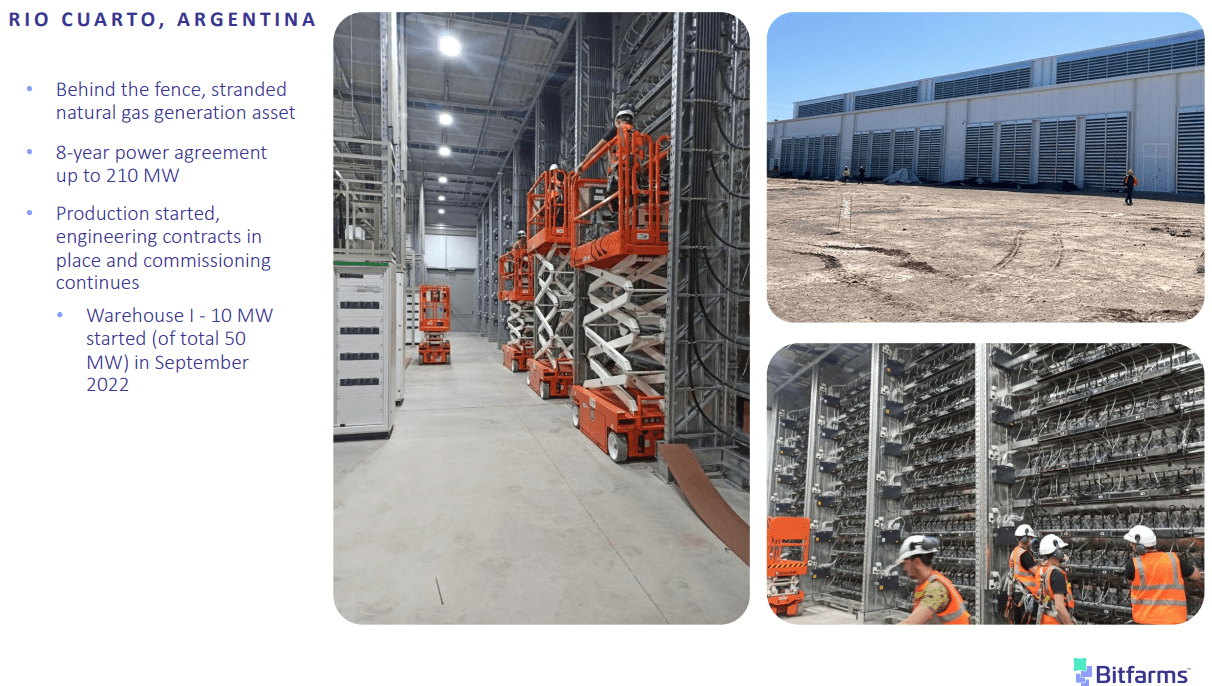

Back in Q2, Bitfarms was able to negotiate an agreement with vendors to postpone delivery of some equipment into 2023, and payment terms recognizing the changing market conditions. Still, the plan is to move forward with a buildout of facilities in Quebec Canada, Argentina, and Paraguay. On this point, some logistical challenges with importing equipment into Argentina delay some deployments in 2022 but management is particularly enthusiastic about growth opportunities in the country along with neighboring Paraguay as low-cost mining jurisdictions.

Company IR

The latest update from the November operational report is that Bitfarms sold 400 BTC during the month from holdings along with converting 453 it mined during the period, generating proceeds of $14.6 million while paying down $10 million in debt related to loans and equipment purchases. The 1,664 BTC reported as of November 30th represents an approximate value of $27.5 million at the current market value. Keep in mind that all this is in the context of a company with a current market value of around $100 million.

What’s Next For Bitfarms

There’s no reason to beat around the bush, Bitfarms and the entire Bitcoin mining industry will need BTC prices to recover, and ideally reclaim the all-time high at some point in the future. Whether that’s in 2023 or in several years from now, the other side would be a scenario where BTC crashes lower or even goes to zero among the more pessimistic or crypto skeptic predictions.

The attraction of BITF is simply that we believe it could outperform the Bitcoin market price to the upside as a leveraged direct-play in digital assets. Assuming a rally in Bitcoin prices, we would also expect BITF to capture the momentum as sentiment improves adding to some level of valuation multiples expansion.

At the current BTC monthly mining production level for Bitfarms averaging about 475 BTC per month, the annualized rate approaching 5,700 implies a revenue potential of nearly $100 million, at the current market price. By this measure, shares are trading at approximately 1x forward sales.

Simply put, a positive $1,000 change to the BTC market price can add an incremental $5.7 million to annual revenue. A scenario where BTC climbs back toward $25k would drive a 50% increase to the top line, with the operating leverage supporting significantly higher adjusted EBITDA.

Inversely, mining revenue would be proportionally reduced on lower BTC prices with operating losses ballooning particularly if BTC approaches the company’s cost of production. The other dynamic to consider is that over time the network difficulty climbs meaning the value of Bitfarms hashrate mining capacity will gradually become diluted. This means that the company will need to either continue growing capacity faster than the network, or count on the price of BTC to rally materially, sooner rather than later.

Again, there are many moving parts and BITF will need the combination of luck and continued execution for the long-term strategy to work. Going forward, operating margins have room to improve as it facilities under development go online while infrastructure Capex requirements trend lower.

Company IR

We’ve been Bitcoin bulls and last wrote about how the sector casualties ls this year including the collapse of “crypto-alts” like Terra coins (LUNC-USD), and bankruptcies among exchanges including “Celsius Network”, Voyager Digital (OTCPK:VYGVQ), and the latest “FTX” scandal could mark a cycle capitulation. The upside for Bitcoin is that it emerges stronger by consolidating its position as the “gold standard” of crypto, largely immune to the fraud or manipulation seen in smaller tokens.

In hindsight, it’s clear there was too much exuberance and speculative money in the sector, although there is a case to be made that the long-term vision for Bitcoin as an alternative asset and store of digital wealth is alive and well.

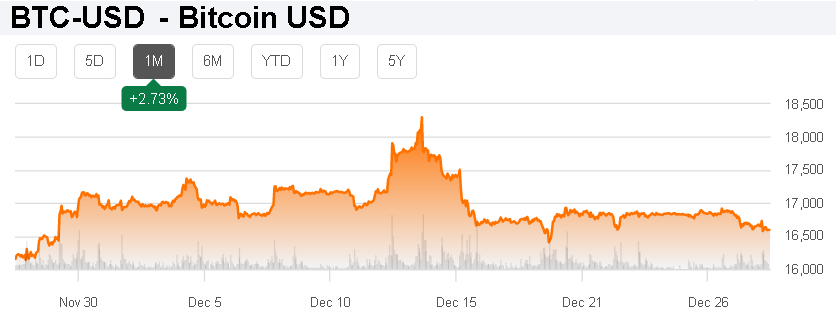

It’s telling that BTC has traded in a relatively tight range over the last few months. One interpretation of this apparent stabilizing bottom is that it progresses into the first step toward a rebound. A broader market turnaround in 2023 including a view that “tech” and high-growth segments gain momentum could open the door for Bitcoin to outperform the upside.

On the downside, Bitcoin would like also be exposed to a further deterioration of the macro outlook driving a new round of volatility in financial markets. A break under $15,000 in the near term as an important level of technical support would likely kick start an accelerated selloff lower.

Seeking Alpha

Final Thoughts

As bad as the trading action in BITF has been, we sense that the fundamental value has been discounted beyond the underlying trends. In our view, with a bullish outlook on Bitcoin, BITF is well-positioned to rebound as higher Bitcoin prices further strengthen its financials.

Bitcoin and the crypto sector remain high-risk with a very real possibility that there is another leg lower for any number of reasons. Within that group, Bitcoin miners have earned the distinction as the absolute gutter of the market following a disastrous 2022 forcing a reassessment of the industry’s long-term viability.

Still, we see the potential upside in Bitfarms as representing an attractive risk-adjusted return opportunity. The stock can work as a small position with a larger diversified portfolio. In terms of monitoring points, the monthly production levels are the key to watch along with the next balance sheet update.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.