Eoneren/E+ via Getty Images

Understanding IREN’s Business

Iris Energy (NASDAQ:IREN) is marketed as a pure-play sustainable Bitcoin (BTC-USD) mining company where 100% of its power used is renewable. To us, sustainable bitcoin mining is a big deal and it is one of the critical criteria for any Bitcoin mining company to be investable. It is one of the key reasons we got into Bitfarms (BITF) in the first place.

Kevin O’Leary explained this well. Institutions have yet to delve into Bitcoin in any major way due to ESG concerns. Non-sustainable Bitcoin mining companies can still meet ESG requirements by being carbon-neutral (e.g., buy carbon credit, or plant trees to offset generated carbons) but will not be able to do so once more concrete regulations are issued in the near future by relevant governing bodies. It is also difficult for auditors to endorse carbon credits due to large errors in estimation and are liable for inaccurate claims. Therefore, sustainability is key when looking at Bitcoin mining companies. In this respect, IREN has met our first criteria of being investable.

IREN is a relatively new and small player in the Bitcoin mining sector. Currently, the company only has 0.8 EH/s compared to other players such as Riot Blockchain (RIOT) (4.3 EH/s) and Marathon Digital Holdings (MARA) (3.9 EH/s).

So does IREN provide more upside for investors when compared to more established players such as RIOT and MARA? Let’s find out.

IREN: A Real Estate Company like McDonald’s?

Aside from being a sustainable Bitcoin mining company, another aspect we appreciate is ownership of land and grid-connected power facilities. This aspect assures investors that mining operations are in total control of the company. The risk of competition for power is eliminated and the ever-increasing cost of land leases is no longer an issue. Besides, Bitcoin’s price appreciation won’t be the only contributing factor to the size of IREN’s balance sheet.

However, the competitive advantage of owning the land and grid-connected power facilities we’re looking for is the flexibility of hosting a profitable data center. Sometimes Bitcoin mining is also referred to as “hosting data centers”, a term we normally associate with Google and Microsoft, and both are true. O’Leary explicitly stated that should Bitcoin mining become unprofitable, pivoting from Bitcoin mining to hosting data centers for Google and Microsoft is a viable backup plan. We’re not acquainted with ASIC for cloud computing yet, but it seems that ASIC could be used for data centers as well. Should IREN’s ASIC miners have such flexibility, IREN could be well hedged against a Bitcoin bear market.

Following this narrative, IREN’s business model looks very similar to McDonald’s (MCD) where McDonald’s owns lands and leases the lands to franchisees.

More than 84% (12.6 EH/s out of 15 EH/s) of land contributing to IREN’s Bitcoin mining is 100% owned by IREN. We estimate the value of the land and grid-connected power facilities to be worth $95.5mil in CY2022Q1 or 50% of IREN’s market cap. This figure is based on IREN’s recommended cost of acquisition of $66mil per 1 EH/s. Table 1 presents the details of estates owned by IREN. Bitcoin mining equipment was not considered in the computation because the equipment is expected to be worth 0 in 5 years. Just to be conservative.

If cash on hand and liabilities are considered, IREN’s physical assets would exceed its market cap at the time of writing. This made us wonder, at a $200mil market cap, are we buying IREN’s real estate and getting its Bitcoin mining business for free?

Table 1: IREN’s Estates

|

Location |

Land Ownership |

Mining Capacity [17.06.2022] |

MW |

Power Source |

Status |

|

|

Canal Flats |

British Columbia, Canada |

100% |

0.8 EH/s |

30 |

100% Renewable |

Operating |

|

Mackenzie |

British Columbia, Canada |

100% |

0.3 EH/s 1.5 EH/s (End2022) 2.4 EH/s (End 2023) |

80 |

100% Renewable |

Operating & Under Construction |

|

Prince George |

British Columbia, Canada |

50Y Lease |

1.4 EH/s (2022Q3) 2.4 EH/s (End 2023) |

85 |

100% Renewable |

Operating & Under Construction |

|

Childress County |

Texas, USA |

100% (>300 Acres) |

3 EH/s (2023Q1) 9.6 EH/s (2023Q3) 17.6 EH/s (No Date) |

600 |

Excess/Underutilized Renewable |

Operating & Under Construction |

Source: Author, IREN

Buy IREN = Buy Real Estate and Get Bitcoin Mining Business For Free?

We think yes and we might know why.

IREN is currently trading below its net asset value. As of CY2022Q1, IREN has $557mil in total assets or $253mil in hard assets (land, grid-connected power facilities, and cash only). IREN has $98mil in total liabilities. This implies IREN has hard assets (excluding all Bitcoin mining rigs and prepaid to suppliers) of $155mil in excess of liabilities. IREN’s market cap is $200mil. Hence, IREN’s hard asset-only NAV is close to 80% of its market cap. At this valuation, it does look like we’re buying IREN’s real estate and getting its Bitcoin mining business for free.

Why is that? We think that this is because the Bitcoin mining business is currently a loss-making business at the current Bitcoin price.

Firstly, as of CY2022Q1, IREN’s total expenses excluding impairment and gains on asset price fluctuation is $14mil, where IREN only managed to mine 357 Bitcoins compared to 364 Bitcoins in CY2021Q4. This is odd because IREN reported an increase in mining capacity from 0.685 EH/s in CY201Q4 to 0.8 EH/s in CY2022Q1.

We felt that the data presented could be more transparent. IREN reported QoQ growth in Bitcoin mined in its CY2021Q4 report but switched to YoY growth in Bitcoin mining in its CY2022Q1 report. Instead of reporting a QoQ 2% drop in CY2022Q1, IREN reported 449% growth YoY.

Secondly, at $20,000 per Bitcoin, IREN is losing $20,000 per Bitcoin mined. This mining cost is consistent in both CY2021Q4 and CY2022Q1. In CY2021Q4, IREN mined 364 Bitcoin and incurred $14.5mil in cost (excluding impairment and asset value fluctuations), which implies a cost of $40,000 per BTC. In CY2022Q1, IREN mined 357 Bitcoins and incurred $14mil in cost, which implies a cost of $40,000 per BTC as well.

IREN’s non-cash expenses such as management stock compensation are perceived to be high but align with the sector standard (Table 2). MARA remains the Bitcoin mining company with the highest stock compensation to management among the 3 companies. However, IREN could be paying more stock compensation to founders and executives as IREN is still a new player and more milestone rewards are yet to be unlocked.

Table 2: Average Management Stock Compensation Comparison Table Since 2021

| Miner |

% of Total Expenses (Excluding impairment and asset value fluctuations) |

| IREN | 30% |

| RIOT | 25% |

| MARA | 55% |

Source: Author

Even if non-cash expenses (such as depreciation and stock compensation) were to be excluded, IREN’s total mining cost per BTC ($22,550) remains higher than the Bitcoin price of $19,000 as of the time of writing.

Therefore, IREN’s Bitcoin mining is indeed a loss-making business and we associate this as the main contributor to IREN trading below its net asset value.

Valuation and Risks

We could not use our model to evaluate IREN’s Bitcoin mining business due to the Bitcoin price falling below IREN’s total mining cost per BTC. If Bitcoin sustainably falls below its total mining cash expenses per BTC ($22,550), its Bitcoin mining business would be worth 0 if IREN is sensible enough to stop mining at a cash loss.

Fortunately, IREN’s hard asset value is visible. As stated above, its hard asset value (land, grid-connected power facilities, and cash) in excess of liabilities is $155mil. Assuming IREN stops mining Bitcoin at a cash loss and minimizes non-cash expenses (such as stock compensation), a $155mil (or $2.90 per share) valuation is a good starting price to get into IREN. However, IREN is expected to see further downside on the overall sector sentiment.

What about IREN’s valuation based on expected capacity?

According to the IREN investor presentation, one of IREN’s investment value propositions is that IREN is trading at only 0.4x its expected hash rate. In other words, IREN is saying that it provides investors with better upside potential than other Bitcoin mining companies including MARA, RIOT, Hut 8 (HUT), Bitfarms, and Argo Blockchain (OTCPK:ARGKF).

Fig 1. Priced lower for good reason: Risks of not realizing target (IREN)

We find this proposition to be not as appealing because there is a big IF. IREN can only provide better upside ONLY IF it can follow through on its target mining capacity. Unfortunately, it is more likely that IREN will not achieve this target. Since IREN’s expected capacity is comparable to MARA and RIOT, let’s focus on MARA and RIOT.

History taught us that miners often miss targeted mining capacity. In CY2021Q1, MARA targeted 10.37 EH/s by early 2022. However, it only managed to achieve 3.9 EH/s, only 40% of the targeted capacity. With MARA and RIOT as references, the expected capacity grows about 0.4 EH/s quarterly. This aligns with IREN’s QoQ capacity growth as well. IREN’s CY2022Q1 QoQ growth is about 0.2 EH/s.

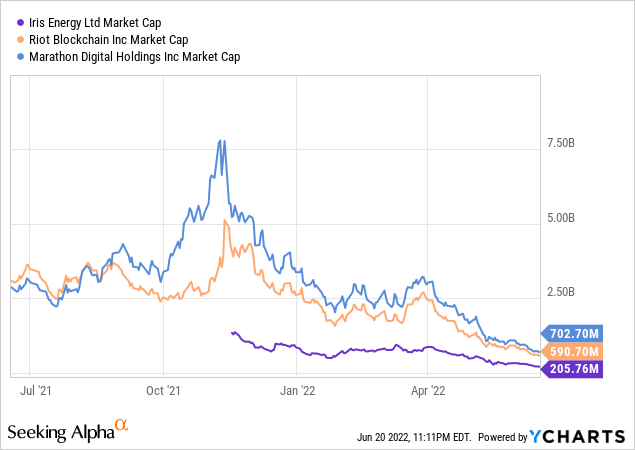

if we consider the risk of not following up on the targeted mining capacity, IREN is fairly priced. Given similar expected capacity, With the assumption that capacity growth is similar across mining companies, IREN should be priced 72% lower than MARA or 77% lower than RIOT.

As of 20.06.2022, IREN is priced 70% lower than MARA and 65% lower than RIOT. This means that IREN is fairly priced but RIOT should be priced 17% higher than IREN. This aligns with our previous findings that RIOT is 20% undervalued when compared to MARA.

Fig 2. Market Cap of IREN, MARA, RIOT (YCharts)

This finding shouldn’t be taken as a call to buy RIOT. In our recent coverage, we showed that Bitcoin has completed 4 out of our 5 predicted sequences of events and discussed why it is more probable for Bitcoin to break its $20,000 historic support level to reach $10,500 than to bottom out from here. This would complete all of our 5 predicted sequences of events. Should our thesis hold, we expect to see further downside for Bitcoin mining companies (including IREN, MARA, and RIOT) due to higher Beta and additional risks (e.g., insolvency).

Today, we continue to uphold our thesis that investors should consider staying away from Bitcoin miners until the end of 2022 when Bitcoin is expected to complete its 1-year bear market by then.

Conclusion

We find IREN attractive for the following reasons:

- IREN’s Bitcoin mining operations are powered by renewable energy, very different from being just carbon neutral.

- IREN owns at least 84% of the land and grid-connected power used to host its data centers. This provides IREN with the ability to recondition its equipment to host more types of data centers should Bitcoin mining become unprofitable.

- IREN’s market cap implies that investors are buying into its real estate and grid-connected power facilities, and are getting its Bitcoin mining business for free.

- Although IREN is currently fairly valued, IREN provides more upside if investors are willing to undertake more risks.

However, as stated above, we expect further downside for IREN which provides investors with a better entry price.

What we would like to see IREN improve is its mining cost. IREN’s mining cost is consistently about $40,000 for CY2021Q4 and CY2022Q1. This is 30% higher than both MARA and RIOT. Another aspect we’re concerned about is there might be more stock compensation for founders and executives waiting to be unlocked in the future. Imagine that the market cap keeps increasing but the share price remains relatively the same or does not grow as much due to dilution from stock compensations. Hence, these non-cash expenses are expected to prevent investors from realizing the full upside reward.