New Eroad CEO Mark Heine on what went wrong, and his comeback plans Video / NZ Herald

One of our larger tech firms has joined the multinationals in laying off staff – and there could be more cuts to come.

But its CEO says a cull of 10 per cent of its

workforce, and office closures, are tied to repositioning after a recent merger of operations with a rival – and that the looming recession could in fact benefit his company.

In the short term, however, there could be more trimming, with a “thorough strategic review” announced today that is designed to save more costs.

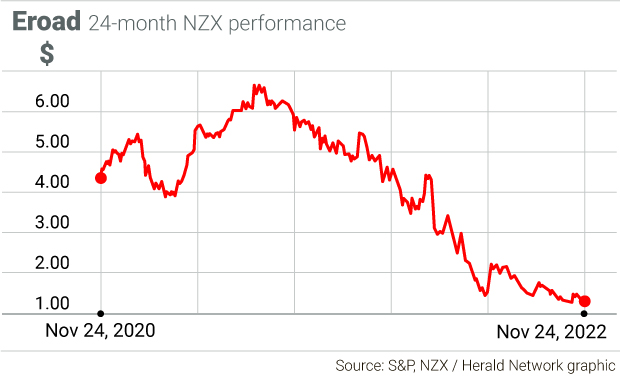

Eroad shares were flat in midday trading after the Auckland-based firm reported breakeven first-half numbers, offered a broad strokes outline of its review, and confirmed its full-year guidance.

The morning’s trading – which saw Eroad’s shares jump by as much as 8.3 per cent – was muddied by transposed numbers, which were corrected at 11am.

The NZX-listed fleet tracking firm made a $552,000 net profit (and a net loss of $5.8 million on continuing operations) for the six months to September 30 as first-half revenue rose 78 per cent to $85m on the back of its December 2021 takeover of rival Coretex.

A $1m ebit profit was reported for the first half, vs a $6.8m ebit loss in the first half of FY2022, but chief executive Mark Heine told the Herald he was focusing on the normalised figure that included costs associated with the $158m Coretex deal. On that basis, Eroad had an ebit loss of $3.4m for the period.

It reaffirmed full-year guidance given earlier this month, when it tightened its full-year revenue forecast to $154m-$164m (from the previous $150m-$170m) and ebit between breakeven and a $5m loss.

“This is a messy result with a number of abnormal costs and other non-cash items relating to the integration of Coretex and foreign exchange swings,” Jarden analyst Guy Hooper told the Herald.

Overall, the first-half numbers appeared to be in line with expectations, when adjusted for the Coretex merger, bar a small ebit miss, Hooper said.

Alongside the result, Eroad announced an external strategic review into the appropriate cost base and rationalisation of its product suite, with a particular focus on the North American market, the Jarden analyst noted.

“The review is a positive step forward, in our opinion, with the company’s strategic direction and product market fit appearing to lack in that market. We estimate the current share price implies a negative value for Eroad North America,” Hooper said.

The results of the review and an updated strategy are expected to be released in the first quarter of next year.

Meantime, Hooper has maintained his neutral rating, and his 12-month price target, which he sliced from $2.75 to $1.65 with Eroad’s market update earlier this month.

Workforce cuts

Eroad has cut around 10 per cent of its staff over the past few months and closed two offices, Heine said.

The layoffs took its total headcount down to 480, though Heine says a number of roles will be added in R&D. Things should washout with a net reduction of around 40 people, Heine said.

Eroad has also reduced its four Auckland offices to three, and closed its standalone office in the US state of Oregon, where staff will now use an office share. An office in San Diego will remain.

Missteps in North America

Heine, who became CEO in June following the abrupt departure of longtime chief executive Steven Newman, earlier said Eroad made strategic missteps in the key North American market.

“We were focusing less on hardware and more on services. We slowed down our hardware journey. We probably didn’t invest as much there from 2017 to 2019 as we should have. We got off the pace a bit and that slowed down our sales,” Heine told the Herald in June.

The CEO pitched the Coretex deal as the solution.

“They are where we were going to be in two years’ time,” he said.

“They already had the product suite that we were looking to do. Their CoreHub product, which is a 4G-enabled, Internet-of-Things device with Bluetooth sensors, cameras and other sensors, we see that as a fantastic piece of technology. It’s going to be a key enabler of growth.”

Accordingly, the shuttered Oregon office was an Eroad outpost pre-merger. The San Diego office – which will become the combined company’s sole office on the US west coast – was a Coretex stronghold.

‘Meaningful’ deal

Today, Heine said Eroad’s five-year, 9000-truck deal with US foodservice logistics giant Sysco, was evidence the strategy was already starting to pay off.

Jarden’s Hooper estimated the contract would be worth around $6m, and described it as meaningful.

Craigs Investment Partners’ analyst Josh Dale called Eroad’s American deals “much-needed good news” after an “annus horribilis’ that saw shares fall from a high of $6.70 in July last year to $1.38 with Newman’s exit in July, largely on weaker-than-expected North American business.

Both see the deals as just the first stages of a turnaround, however, and retained their respective neutral ratings following Eroad’s market update on November 7 (which included the full-year numbers re-affirmed today).

Overall, Eroad said the number of its telematic units in trucks increased by 4 per cent or 8822 to 217,519 in the first half.

New Zealand continued to be its largest market, with 112,280 (from a year-ago 106,916), followed by North America 90,596 (from 87,682) and Australia with 14,643 (from 14,099).

Most of the units are tied to monthly subscriptions for software and services. Annualised monthly recurring revenue – which gives a 12-month forward view, based on the current run rate – hit $158.3m in the first half from the year-ago $134.6m.

Recession opportunity

Recent layoffs by tech multinationals have been driven, in part, by economic slowdown fears.

But Heine argues the gloomy outlook creates opportunities for his company.

“Historically, we’ve found recessions have not been a bad thing for Eroad. Our customers want to take cost out of their business, and that’s exactly what our product does – whether its fuel consumption or whether its asset utilisation or getting productivity out of their drivers.” (Eroad’s hardware and software tracks trucks, calculates the most fuel-efficient routes, tallies road-user charges, and monitors both engines and drivers, among other features.)

Heine does concede that there’s one negative impact, however: companies are taking longer to make buying decisions. He says Eroad has a strong pipeline – “We’ve got 22 pilots for 32,000 units in North America alone” – but trying to gauge when that business will actually land is tricky in the current environment.

Jarden’s Hooper also cautioned that “a number of larger enterprise customers in Australia and North America up for renewal.”

Impact of 2G and 3G mobile network shutdowns

Hooper played down market chatter, in some quarters, that 2G and 3G mobile network shutdowns in NZ, Australia and North America would leave users of older Eroad products high and dry.

“Eroad’s products built in 2019 or later are on 4G or 5G,” the Jarden analyst told the Herald.

“There are some legacy EHUBO 2.0 or 2.1 products out there that don’t work on 4G but I don’t believe it is material.

“As at March 2022, 94 per cent of Eroad and 88 per cent of Coretex legacy North American customers were on 4G.”

Heine said the customers who were still on 2G or 3G represented an upsell opportunity.

Vodafone NZ said it would turn off its 3G network at the end of August 2024.

Spark has yet to give a kill date for its 3G network but said it would give at least 12 months’ notice.

Vodafone has committed to maintaining its 2G mobile network until 2025. Its thinking is that 3G devices could trip down to 2G. (Spark scrapped its 2G network in 2012.)

While consumer phones use faster, more capable 4G or 5G (fourth and fifth generation) mobile networks, older 2G and 3G technologies are often used with internet-connected devices.

Hooper said Vodafone NZ’s pledge to maintain its 2G network until at least 2025 gave Eroad breathing space in its largest market.