Mario Tama/Getty Images News

Shares of Apple (AAPL) soared after reporting earnings which comfortably beat consensus estimates. There are a lot of reasons to like the stock – growing dividends, share repurchases, and lots of profits. Yet with the stock trading at 28x earnings, I question whether bullish arguments are driven by sentiment or rational thinking. Investors should question why AAPL has invested so much into share repurchases even as the valuation continues to soar. With the net cash position down to $80 billion versus the current market cap of nearly $3 trillion, the stock faces new challenges as I expect earnings to be volatile exiting this period of peak iPhone sales. This is an incredible time to sell and reallocate in the tech sector.

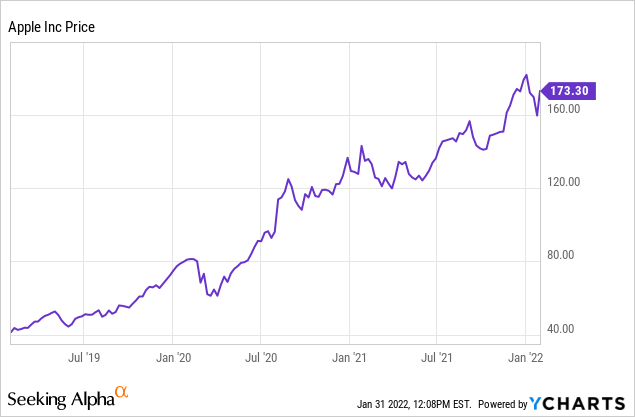

AAPL Stock Price

Amidst a crash in tech stocks across the board, profitable tech stocks like AAPL have been more or less spared from the carnage.

YCharts

AAPL’s 3-year price performance remains stellar as the stock has delivered multiples in returns in just a few years time. Unfortunately, the strong performance appears to have blinded investors to the likelihood of poor future returns.

How Were Apple Stock Earnings

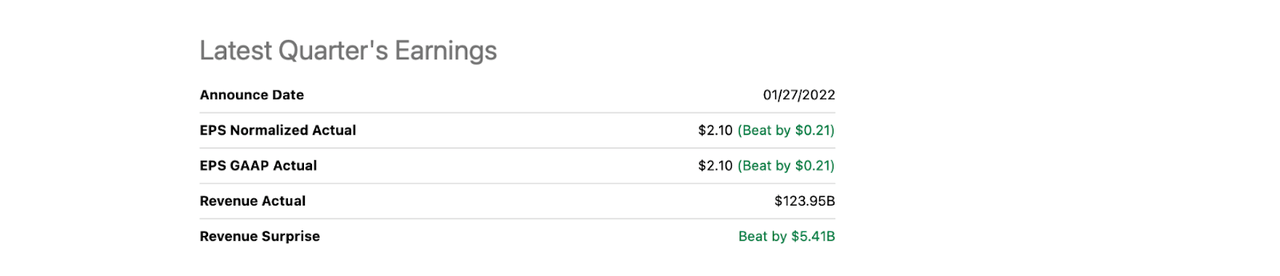

AAPL’s earnings were admittedly quite strong, as the company comfortably beat consensus estimates on both the top and bottom lines.

Seeking Alpha

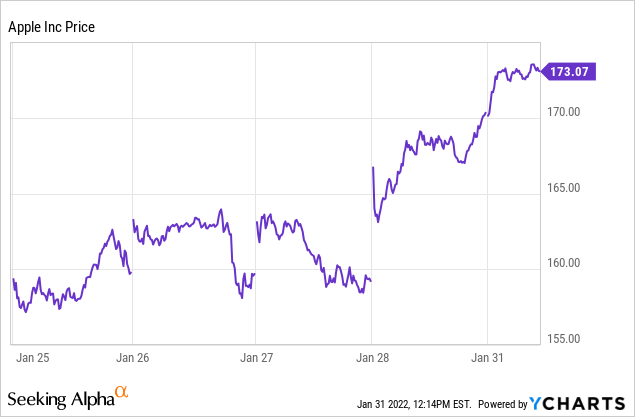

Wall Street liked the results so much that the stock jumped nearly double-digits the very next day, which is even more impressive when considering the bleak sentiment present for the tech sector overall.

YCharts

When I take a deeper look at the results, I am growing concerned by what seems to be an overly enthusiastic reaction to arguably normal results.

AAPL Stock Key Metrics

While net sales increased by only 11.2%, net income grew by a faster 20.1% (due to operating leverage) and EPS grew even faster at 25% (due to share repurchases). We can see a breakdown of net sales by category below (the latest quarter’s results are on the left):

FY 22 First Quarter Results

AAPL ended the quarter with $203 billion of cash versus $123 billion in debt for a net cash position of $80 billion. The company paid out $3.7 billion in dividends and bought back $14.4 billion or 93 million shares. At least a surface level analysis shows strong results.

What Is Apple Stock’s Forecast?

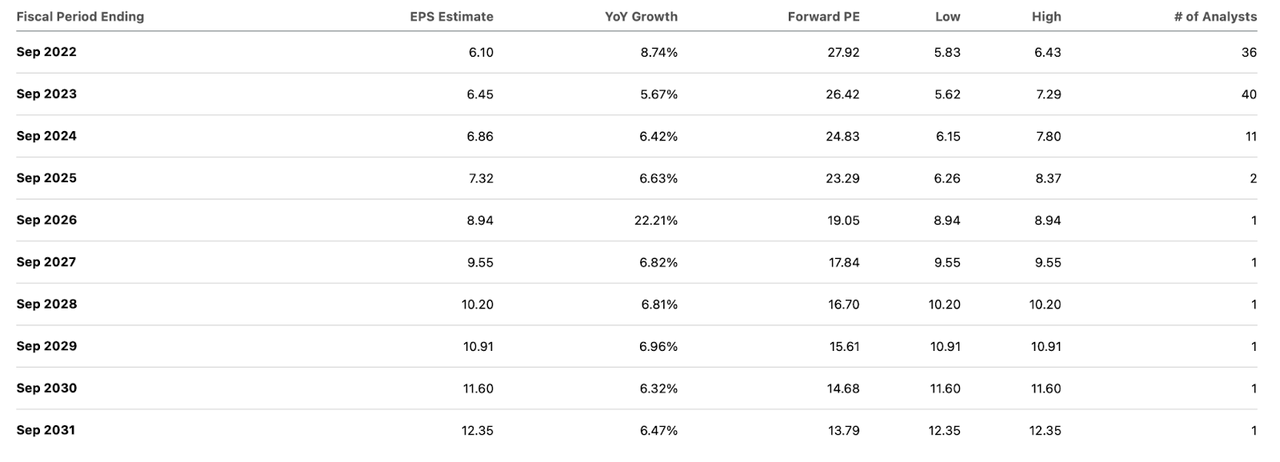

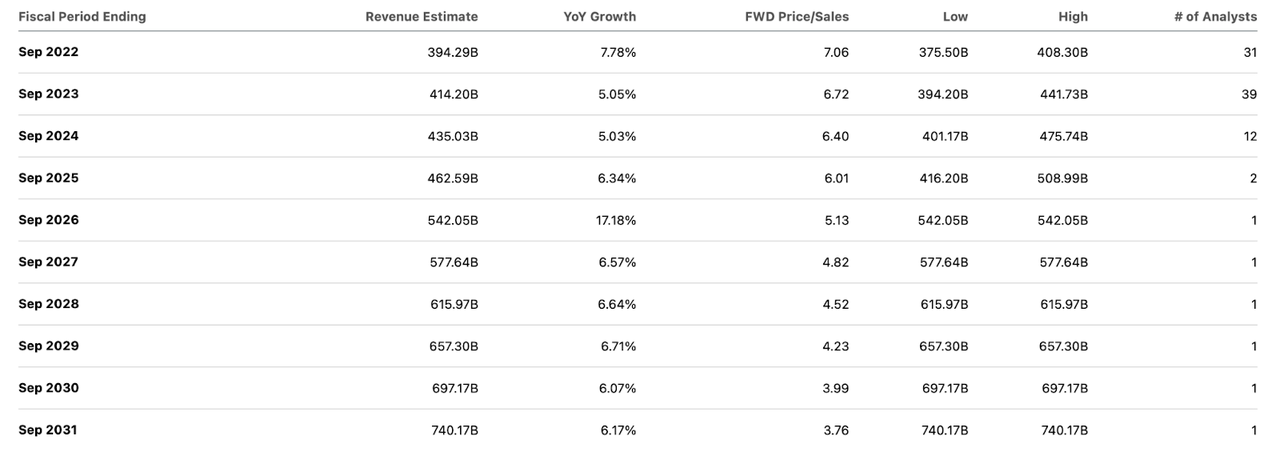

If you gauge sentiment across my fellow contributors and investors, as is evident by the 28x forward PE multiple, there seems to be a belief that AAPL will grow very rapidly over the coming years. Yet consensus estimates call for earnings to grow at a slower rate over the coming decade.

Seeking Alpha

One could argue that these estimates may be conservative relative to consensus revenue estimates, considering that they seem to factor in minimal operating leverage.

Seeking Alpha

I am sure AAPL bulls will make the argument that these estimates are far too conservative, but is this the case?

I must point out that AAPL hardware sales tend to be more cyclical than of the secular growth nature. In particular iPhone sales grew by 39% in 2021 after declining slightly in 2020. It appears that AAPL is benefitting from the benefit of a 5G supercycle as well as pent-up demand. Investors should not expect the strong growth to continue – investors actually should expect hardware sales to eventually decline from current levels. Moving forward, it is reasonable to expect Android to continue taking market share, if only due to the fact that Android phones tend to be significantly cheaper than iPhones. The numbers support this prediction: Android market share has increased from 25% in 2012 to 72% as of 2021. This price detail is very important because AAPL’s latest iPhone13 already costs $900 for the 256 gigabyte product, with pricing being a key driver of growth for the company. Will AAPL be able to continue increasing prices so aggressively as it approaches and breaks the $1,000 price point? I am not so confident.

This forecast is important because hardware sales make up around 81% of net revenues and 69% of gross profits. Yes, AAPL bulls will counter that the services segment is growing very rapidly – it grew at a 23.4% clip in the latest quarter. However, because it remains such a small component of the overall business, this explains why the business overall is not expected to produce strong growth moving forward.

Is AAPL Stock A Buy, Sell, or Hold?

I suspect that there are four main reasons why investors remain so bullish on the stock. First, AAPL has strong support of Wall Street analysts, being rated 4.39 out of 5:

Seeking Alpha

Next, AAPL has been a strong performer in recent years – investors tend to view the fundamentals more optimistically when the stock is rising.

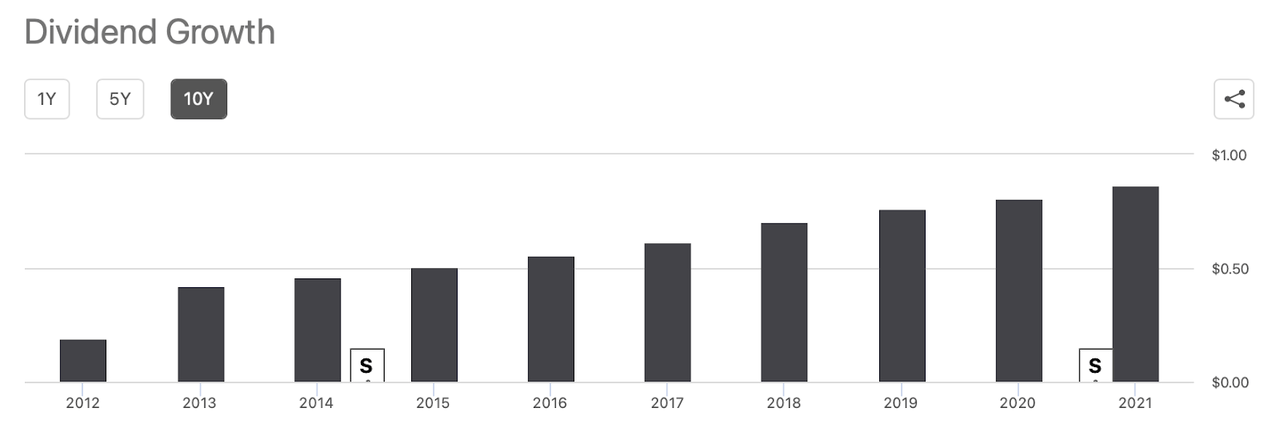

AAPL has consistently grown its dividend for many years at a rapid pace.

Seeking Alpha

I wouldn’t be surprised if many dividend investors have made AAPL part of their portfolio as their “only tech stock.”

Finally, AAPL has been a serial repurchaser of shares, buying back the equivalent of many companies every single year.

Yet all of these reasons are backwards looking and speak nothing to what will occur in the future. I find it highly concerning that investors seem to be very enthusiastic about the fact that AAPL is reporting “record numbers,” but it is instead the forward growth rate that will drive future returns. The fact that AAPL earned over $123 billion in revenues in the latest quarter is very impressive, but should not be a reason to be buying the stock at 28x forward earnings.

Should investors really be cheering the incessant share repurchases even as the multiple has expanded above the 25x range? AAPL bulls might argue that the share repurchases are not stopping innovation, but that isn’t such an easy argument. Research & development (R&D) stood at $6.3 billion – only 11.6% of gross profits. In comparison, mega-cap tech peers Meta Platforms (FB) and Alphabet (GOOGL) spent 27.2% and 20.5%, respectively. Both FB and GOOGL are out-spending AAPL in R&D in spite of producing lesser profits. While one could make the argument that AAPL is producing very high quality smart phones, I just don’t see the argument that one should buy the stock due to some impressive innovation that will be coming over the next few years. If one wants that kind of upside, FB or GOOGL make a lot more sense. I note that FB and GOOGL trade at much cheaper valuations relative to their growth rates.

Which brings us to the question: if AAPL will not grow so rapidly over the coming years, then is the stock really that attractive at 28x earnings? Further, considering that AAPL has around $90 billion of free cash flow every year, should it really be repurchasing shares? That money could be put towards differentiating its business model and potentially boosting its growth rates. Just because a company could buy back shares does not mean it should. I expect the multiple to contract rapidly when it becomes clear that product sales have reached a peak. I find it highly concerning that the company has been so focused on buying back stock instead of boosting its R&D budget or making external acquisitions. It looks like a lot of the praise for AAPL’s management team is driven by the rising stock price. If AAPL stock were to struggle, then I suspect that investors will suddenly become more critical of the capital allocation decisions of recent years.

I have made the case that AAPL will likely not grow very rapidly over the coming years, not nearly enough to justify buying at these prices. But perhaps the best argument to sell AAPL is due to the more attractive opportunities elsewhere. I have already mentioned FB and GOOGL, both of which trade at lower earnings multiples in spite of materially faster growth rates. But beyond mega-cap tech, the broader tech sector has experienced a crash that has created numerous buying opportunities. Now isn’t the time to be buying AAPL and hoping for a best case scenario of 7% annual returns – it is instead time to be sifting through the tech rubble and stocks that can deliver multibagger returns over the next few years. Many tech stocks in my coverage are flashing buy signals and appear priced for phenomenal returns. AAPL may be a “feel good” stock due to the growing dividends and share repurchases, but those characteristics had more meaning when the stock was trading at 10x earnings than now when the stock trades at 28x earnings. Investors counting on the same reasons driving the rising stock price in the past to work moving forward are likely to be disappointed. I rate shares a hold but heavily emphasize that better opportunities are elsewhere.