It started in Asia. Equities opened stronger on Monday. The optimism in Asia that then spread to Europe and also included US equity index futures stood in stark contrast to the mood on Wall Street this past Friday after the Bureau of Labor Statistics published that agency’s twin employment surveys for the month of May.

What gives? First, the Shanghai Composite popped 1.2% as Hong Kong’s Hang Seng popped 2.7%. The Caixin Services PMI for China printed at what would have not too long ago been considered an anemic 41.1 (above 50 signals expansion), but this 41.1 came in the wake of April’s 36.2. Though this was China’s third consecutive print deeply inside of contractionary territory for the services sector, Asian investors are seeing this as an improving situation, as a signal that there is still demand across the Chinese economy that is starting to return now that Covid-related lockdowns in Shanghai and other locales appear to be lifting to varying degrees.

It would also appear that Saudi Arabia is betting on a rebirth of Chinese demand not just for services but for crude oil, as Aramco raised prices for its Arab Light crude for Asian customers by $2.10 per barrel from June to $6.50 above its benchmark price. Markets had expected and had priced in an increase of roughly $1.50. Aramco also increased prices for all grades for the European and Mediterranean regions, while leaving prices for US customers unchanged for a second consecutive month. This has global oil prices edging higher through the wee hours.

Finally… Probably as key as any news event to the bid seen under global equities was news that Chinese regulators has decided to conclude their roughly year long probe into DiDi Global (DIDI) and other US listed Chinese tech firms, as the regulators are apparently ready to allow these firms to remove a ban on allowing those apps to add new users. After having shot their own economy in the foot repeatedly over the past year, it would seem that Chinese regulators may be preparing to let that ecosystem run with less central interference as the nation attempts to recover economically from Covid.

Here at Home…

Equity markets “snapped” their one week winning streak last week here in the US. While that may mislead just a bit it is technically true, as Friday’s equity market selloff gave up enough ground to turn the holiday shortened four day workweek negative after all of your favorite indexes had sapped seven or eight week losing streaks the week prior.

For a short week, US markets went through quite a bit, as the Federal Reserve rolled into its first month of quantitative tightening, and a number of Fed officials including Vice Chair Lael Brainard kept up the hawkish rhetoric. Investors also dealt with an earnings warning and guide-down from tech giant Microsoft (MSFT) based solely on changing currency exchange rates, and almost dire sounding warnings on the state or direction of the US economy from the likes of JP Morgan (JPM) CEO Jamie Dimon and Tesla (TSLA) CEO Elon Musk, the latter of those two being among a number of corporate leaders announcing either “slowdowns” in hiring or worse.

Then there was May “Jobs Day” on Friday. According to the Bureau of Labor Statistics’ Establishment Survey, the US created an estimated 390K non-farm positions in May, which was about 65K above consensus view. While the Unemployment Rate remained unchanged at 3.6% and the Underemployment Rate edged just slightly higher from 7.0% to 7.1%, wage growth did slow… from year over year growth of 5.5% to 5.2%, as the average workweek stayed at 34.6 hours. While the picture painted is one of maybe slightly past peak employment, it also paints a picture of a labor market still strong enough to further propel already hot consumer level inflation. This would be what happened to US stocks on Friday.

Marketplace

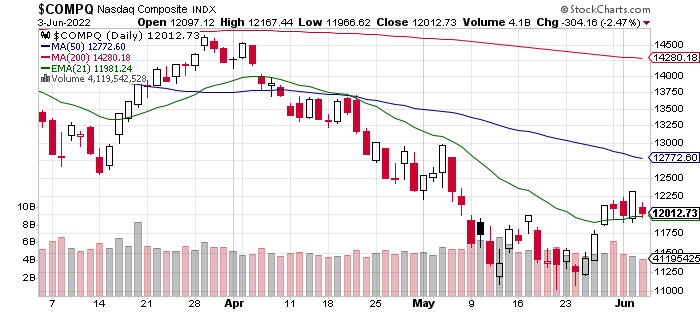

The S&P 500 gave up 1.63% on Friday to close 1.2% lower for the week. The Nasdaq Composite surrendered 2.47% on Friday to close down 0.98% for the week. The Russell 2000 traded off 0.77% on Friday to finish the week down 0.26%. You get the idea. Equities were higher for the week going into Friday. For the week, two of the 11 S&P sector-select SPDR ETFs gained ground, while nine shaded red. Energy (XLE) was way out in front at +1.11%, while Health Care (XLV) led to the downside, losing 3.13%. Interestingly, the more defensive sectors took four of the five bottom rungs on the weekly sector performance tables, which could indicate some optimism despite the overall weakness.

Note this…

… It appears that despite Friday’s negativity that the S&P 500, Nasdaq Composite and Russell 2000, here we use the iShares Russell 2000 ETF (IWM) as a proxy, all held onto recently established support at their respective 21 day EMAs. In addition to the sector performance standings, this would indicate that nearly no technical damage was done to US equity markets on Friday.

Need one more potentially optimistic take-away from Friday’s selloff? I have a good one for you. Equity market breadth was lousy on Friday. What did you expect? Losers beat winners at the NYSE by a rough 5 to 2 and at the Nasdaq by roughly 7 to 4. Advancing volume took just a 22.9% share of composite NYSE-listed trade and just a 30.6% share of that metric for Nasdaq-listed names.

This is where it gets fun. Aggregate trading volume fell like a pea rolling off of a table on Friday from Thursday. Trading volume in the aggregate fell 6.7% on Friday for Nasdaq names and a stunning 16.5% for NYSE names. In fact, Friday was the lightest trading day experienced across subordinate names to the Nasdaq Composite since February 4th and across the S&P 500 since December. The activity across these two indexes fell 18% and 24% short of their respective 50 day trading volume SMAs.

What I am telling you is that there was almost zero conviction behind Friday’s selloff. The pros mostly sat on their hands. I don’t know what they did for most of the day, but it certainly was not for the most part, acting to reduce their long-side equity market exposure.

Semiconductor Beatdown?

On Friday, Micron Technology (MU) dropped 7.2% in response to the downgrade made by Piper Sandler’s five star rated (at TipRanks) Harsh Kumar. Kumar took Micron down to “underweight” from “neutral” while setting a $70 target price on the stock. Kumar sees slowing sales across markets for smartphones and PCs, which is where Micron and the firm’s memory business is highly exposed. Kumar went out of his way to express confidence in Micron’s data center business.

The Philadelphia Semiconductor Index gave up 3.02% on Friday, sinking all boats including Sarge names such as Nvidia (NVDA) , Advanced Micro Devices (AMD) and Marvell Technology (MRVL) . These three names were down 4.45%, 2.11% and 4.02%, respectively. Know what? None of these names do a large smartphone or memory business. AMD has exposure to PCs, but let’s be honest… Kumar’s warning largely does not apply to the entire industry as this industry is so specialized. Can one part or several parts of the semiconductor universe succeed while others do not? Or succeed less?

Why not? Does anyone really want to bet against the further adoption of the digital cloud by corporate America, or the corporate globe as much of the white collar world remains mobile? Are any global players in any industry going to choose to remain on-premise? No. my opinion is that almost all will ultimately choose to adopt a hybrid cloud model at a minimum. I am exactly where I want to be right now in regards to cloud adoption and corporate focus upon the data center. That’s to remain long Nvidia, Advanced Micro Devices and Marvell Technology.

The Week Ahead

The focus this week, will of course be on this Friday’s May print for CPI. Right now, expectations are for a headline print that does not cool at all from April’s year over year growth of 8.2%. This may be taken as severely disappointing by folks that do not follow the data and do not follow key economists. I am not sure how the high-speed, keyword reading algorithms that currently control equity market price discovery will react to that kind of print, even if core inflation does drop to 5.9% from 6.2% as expected. Bear in mind that the Fed has gone into their media blackout period ahead of their June 15th policy decision, so you will not hear anything from the plate spinners nor the jugglers.

Of course there’s plenty going on between here and there. Today (Monday), Apple (AAPL) is set to kick off WWDC22, the annual developers’ conference. Oddly, in recent years, on average, Apple stock has underperformed the S&P 500 the week of this conference though one might expect that any conference where a number of updates are announced might act as an upside catalyst.

This year, rumors are rampant that Apple will announce an update to the iPadOS that will make iPads behave more like computers, that there will be updates announced to iOS 16, that there could be changes made, especially in regards to healthcare services to Apple Watch, and lastly, that Apple may have nailed down some – or maybe more than some – NFL programming for the Apple TV+ streaming service. The NFL Sunday Ticket Package would be a game-changer.

This Wednesday afternoon, expect to see potential headlines emerge from the Bloomberg Technology Summit as Amazon (AMZN) CEO Andy Jassy participates. Jassy is expected to announce some of the initiatives currently being pursued by Amazon, also with a potential focus upon healthcare. Don’t forget Amazon stock split 20 for 1 over the weekend past.

Lastly, but certainly not leastly, Advanced Micro Devices will hold the firm’s investor day this Thursday. Investors are hoping that CEO Lisa Su will offer up a new three year sales growth forecast as well as an update on the integration of Xilinx into the firm. As a shareholder, I am expecting to hear something exciting.

That Said…

… Rock on, my noble friends.

Economics (All Times Eastern)

No significant domestic macroeconomic data-points scheduled for release.

The Fed (All Times Eastern)

Fed Blackout Period.

Today’s Earnings Highlights (Consensus EPS Expectations)

After the Close: (COUP) (.05)

(MSFT, XLE, NVDA, AMD, AAPL and AMZN are holdings in the Action Alerts PLUS member club. Want to be alerted before AAP buys or sells these stocks? Learn more now.)

Get an email alert each time I write an article for Real Money. Click the “+Follow” next to my byline to this article.

")