Kelly Sullivan

Meta Platforms, Inc. (NASDAQ:META) just reported its first revenue loss ever in 2022 Q2 results. While its financial performance was weaker than expected, Many investors are long the stock given its distinct cash flow, large Daily Active Users (DAU), and amazing track record of acquisitions. The concerns are also well known regarding the competition with TikTok, risks of its Metaverse investment, Apple’s (AAPL) privacy push, etc. In this article, I will discuss some of my considerations around META’s business conflicts with Apple and why it is worth a close look after this second-quarter release.

Apple’s attempt to tame META

In recent years, Apple has made its ‘privacy’ efforts as one of its priorities. In 2018, Apple implemented privacy protection measures that required websites to stop tracking user behaviors and discard cookies if a site had not been visited in 30 days. In 2020, the App tracking transparency tool started to allow users to opt-in or out of tracking on different applications and obscure mobile identifiers (IDFA). All these measures make META’s Ad targeting and measurement inaccurate. In fact, all advertisers and publishers will suffer from this. Apple’s decision may hurt small businesses in reaching audiences and limit growth; so there are some risks to going too far with this. But we don’t know what Apple will do next, which is a huge headwind for META.

META Ad effectiveness compromised

Of course, META will be impacted, but the question is, how serious is this? I think one consequence for sure is the weakening of its competitive position. Previously, META’s IDFA-based device tracking was the best. Its capabilities to do multi-touch attribution models are the best. After Apple’s policy changes, META may lose all these advantages to some extent. And META may have to compete with others on a contextual advertising basis instead of at the user level.

The last line of defense is still intact, for now

Fortunately, without IDFAs, Mobile measurement platforms (MMPs) like Appsflyer, Adjust, Tune and Kochava could still use fingerprinting which is basically a less reliable way to identify devices through IP addresses and operating systems. This is very hard for Apple to track because this information could be shared through the server-to-server connections, which is a blind spot beyond Apple’s purview.

Fingerprints are around 90% accurate but are still tracked without user consent. Apple may completely ban this to prevent developers from transferring data to their servers. However, there is a couple of counterarguments. First, 90% doesn’t mean a unique identifier to the individual because there is still a 10% chance of being random. Second, developers needed fingerprinting information to update their apps. If Apple bans fingerprinting, they have to block SDK updating until ad tech partners (e.g., AppLovin, Adjust) stop fingerprinting. This will lead to unnecessary costs for developers who Apple claims they will always protect.

Another solution for Apple is to respond by introducing a private relay that will hide IP addresses. But It is still in beta, and also slows users’ internet down. So not ready yet. But who knows what will happen next? I think we all need to keep a close eye on this if we are investing in META.

Sales may slow down but it is not the end of the world

All being said, even if advertisers understand that META’s Ad ROIs are not as effective as before, where will their money go to? They really don’t have many options. As of right now, other than META and Google (GOOG) (GOOGL), those alternative ad networks have limited reach and their self-serve systems are less powerful.

The current environment is a good test for META as inflation, supply chain problems, recession, war, and the end of government stimulus all mixed together. People are traveling more, which leads to less spending on other categories. A slowdown is inevitable because less consumer spending will directly decrease the advertiser’s budget.

As the table below, META’s $28.15B revenue is still a lot higher than 2020 Q2 and 2019 Q2. META’s average revenue per user is still around $10. In the short term, META’s ad business is not going to disappear or be cut in half.

META vs GOOG Ad revenue (Author)

GOOG’s ads are growing faster but it didn’t suffer from Apple’s privacy policies. I think META still holds its Ad positions. However, future uncertainties still exist.

Video adoptions are good, but App Tracking Transparency (ATT) issue is still out of META’s control

According to the 2022 Q2 call,

Reels engagement is also growing quickly. I shared last quarter that Reels already made up 20% of the time that people spend on Instagram. This quarter we saw a more than 30% increase1 in the time that people spent engaging with Reels across Facebook and Instagram.

Personally, this is not bad at all. It clearly shows META’s execution on videos. META’s technology stacks will catch up very quickly given its strong capabilities in AI and software development. I don’t think TikTok is eating META’s lunch. The management has also expressed their confidence in delivering great long-term results in this area. Moreover, the recent news about META’s decision to share Ad revenue with creators should work very well for its video platforms.

META can plan and adjust its investment in AI systems, Video platforms, and the reality lab. But Apple’s ATT impact is still totally out of META’s hands. As the conference call stated in last quarter:

On the $10 billion impact, we shared our estimated $10 billion impact on ATT last quarter to give a sense of the order of magnitude, and we believe it’s still to be that order of magnitude on the expected impact.

According to this the 2022 Q2 call, these headwinds continued:

we’re also continuing to face targeting and measurement headwinds such as Apple’s iOS changes, which we believe are contributing to the growth challenges across the digital advertising industry.

And Zuckerberg has recently told employees this:

So yeah, Apple is going to be a competitor. I think that that’s pretty clear, but it’s actually a very deep competitor. It’s not just [that] they have a device that has some more features than us. It’s a very deep, philosophical competition about what direction the internet should go in.

Bottom line

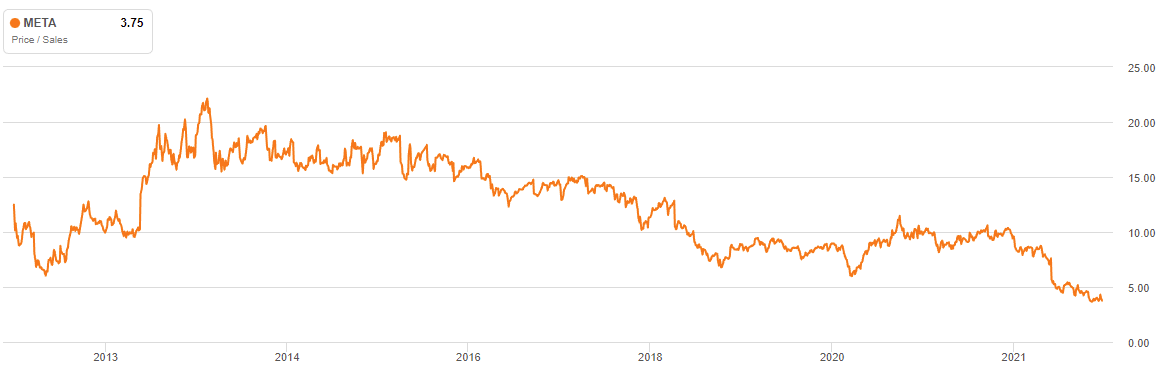

Overall, META is a cheap stock that has zero debt, strong cash flows, and buybacks with growth prospects and long-term investment for the future. No matter what metrics I use, the stock looks undervalued. The PS ratio has dropped to an all-time low of 3.75 (the chart below).

Historical PS ratio (Seeking Alpha)

I think the market is discounting lots of challenges META faces. The threats of Apple should definitely be one that investors keep a close watch on.