iPhone 15 Pro colorful lineup

Supply issues with the iPhone 15 Pro and iPhone 15 Pro Max will push sales into the next quarter, says Morgan Stanley, which has consequently cut its Apple price by $5.

Ahead of Apple’s next earnings call, typically held at the end of October, investment bank Morgan Stanley says these figures should be as predicted. But “iPhone supply shortages & stronger USD likely to result in a below-seasonal Dec Q[uarter] guide,” it says in a report seen by AppleInsider.

Morgan Stanley analysts have previously predicted a September quarter that is “materially higher” than the rest of the year. More than standing by this, the firm is fractionally increasing its expectations — but say the following quarter will be weaker.

“Solid margins & Services upside are highlights this quarter, but earnings unlikely to sway bulls or bears,” it says. “We are raising our Sept Q estimates slightly, but lowering Dec Q estimates by 5-9% (still 0-1% above Consensus) due to iPhone 15 pushout; PT to $210 (from $215).”

“We expect Apple to post a relatively in-line September quarter, with our $89.9B revenue forecast and $1.39 EPS forecast 0-1% above Consensus,” it continues. “However, we are now more guarded on the December quarter (F1Q24) than our prior forecast implied — not because of worsening demand data points – but because supply (both labor and component) remains a headwind that is resulting in a pushout of iPhone 15 Pro/Pro Max demand from the December ’23 quarter to the March ’24 quartear.”

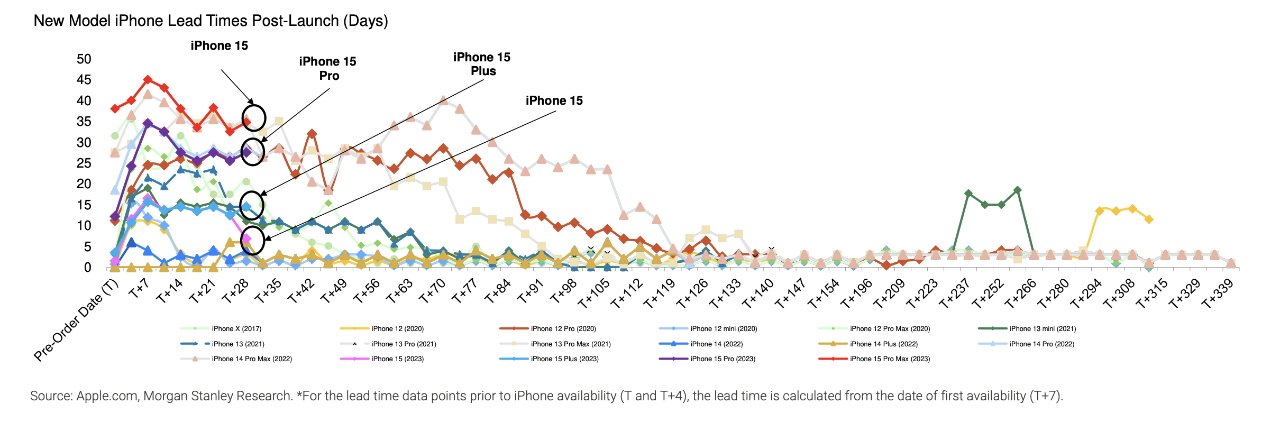

How current iPhone lead times compare to previous models (Source: Morgan Stanley)

Analysts from the firm also point to a stronger US dollar and unfavorable 14 week compare (primarily impacting Services)” as reasons to reduce its December quarter estimates.

Citing its supply chain sources, Morgan Stanley also says that two million of iPhone 15 Pro Max that had been “expected to be finalized by December are being pushed to the March ’24 quarter.”

There is also “slightly slower” that expected assembly of the iPhone 15 Pro “because of labor shortages in the Kunshan/Shanghai area.” Some one million of this model are being pushed out to the next quarter.

Morgan Stanley believes that sales of the Pro models are sufficiently outperforming the iPhone 15 and iPhone 15 Plus that it expects Apple will shift production capacity to the iPhone 15 Pro and iPhone 15 Pro Max in early 2024.

Mac and Wearables up, but iPads down

Overall, Morgan Stanley says there is “little change to our Mac, iPad and Wearables forecasts for the September or December quarters,” but there is movement within those categories.

So for instance, the company is “raising our September quarter Mac revenue forecast by 7% to account for better than expected shipments,” it’s also assuming that “iPad revenue continues to decline double digits” year over year.

The company predicts that the Mac and Wearables “will return to growth,” but says that’s not down to a “notable inflection in consumer demand.” Instead, it’s down to a “materially easier” year over year comparison, because of calendar differences between 2022 and 2023.

Services growth will slow down

Morgan Stanley is expecting a growth slowdown in Services, but not a contraction.

“Apple benefitted from a 14 week quarter in December ’22 (vs. a normal 13 week quarter), with the App Store one of the key beneficiaries of this dynamic,” says Morgan Stanley, “and thus Services faces a very challenging December ’23 compare.”

Once more, Morgan Stanley is raising its forecast fractionally for Apple’s Services earnings, only to say earnings will be lower in the next quarter compared to last year. Part of that, though, is down to that year over year calendar difference.

So the figures are likely to be down for the December quarter, yet overall Morgan Stanley remains positive for the future of Apple Services.

“We are encouraged by the acceleration of the Services business in the September quarter,” it says, “and believe that Services can continue to grow at a low-to-mid teens percentage Y/Y into FY24.”

In its last earnings report, the success of Services helped Apple slightly beat expectations to achieve total revenues of $81.8 billion, despite a weaker quarter for the iPhone.

")