Following its January 28-29 meeting, the Federal Reserve kept interest rates unchanged, stating that it would wait for more substantial progress on inflation before considering any further cuts. However, what caught markets by surprise was Fed Chair Jerome Powell’s unexpectedly positive comments on crypto—his most accommodating stance on digital assets to date.

Editor’s note: this article was written prior to the U.S. government reaching a tentative deal with Mexico’s government to at the very least suspend implementation of the tariff for one month. You can read about this development here.

Although Powell didn’t endorse crypto outright, his acknowledgement of its role in the financial system represented a major shift from previous skepticism.

As we at Outset PR observed, Powell’s shift reflects a broader trend—not just regulatory acceptance but also a fundamental change in how traditional financial institutions perceive digital assets.

This meeting was also the first since President Donald Trump returned to office, having clearly stated his desire for lower interest rates. While the Fed has historically operated independently of the White House, Trump has openly challenged its authority:

“I think I know interest rates much better than they do, and I think I know it certainly much better than the one who’s primarily in charge of making the decision.”

Despite this potential for conflict, Powell has been deliberate in maintaining the Fed’s independence, refusing to engage in Trump’s rhetoric on interest rates. When asked in November whether he would resign if Trump requested it, Powell responded with a firm “no”, adding that demoting Fed officials from their governorships is not permitted under the law.

Fed opens doors to crypto banking

Powell’s crypto-related remarks were particularly noteworthy, as he directly stated that U.S. banks are allowed to serve crypto clients, provided they manage the associated risks properly:

“Our role with Bitcoin really is to look at, with crypto, it really is to look at the banks. We think banks are perfectly able to serve crypto customers as long as they understand and can manage the risks, and it’s safe and sound. A good number of the banks that we regulate and supervise do that.”

He also clarified that while the regulatory threshold for banks engaging in crypto remains high, the Fed is not opposed to innovation:

“If you’re making a choice to conduct that activity inside a bank which is inside the Federal safety net, with deposit insurance, then you want to be pretty sure that it’s a safe and sound activity. So, we’re not against innovation, and we certainly don’t want to take actions that would cause banks to terminate customers who are perfectly legal just because excess risk aversion may be related to regulation and supervision.”

This triggered a BTC price spike to $105,000 before leveling out, driven by fresh confidence in Bitcoin as a financial superpower. It also contrasts sharply with Powell’s previous wariness toward crypto. As recently as March 2023, Powell described the crypto space as one riddled with “a lot of turmoil,” fraud, and “lots of things like that.”

However, Bitcoin (BTC) experienced a notable drop following President Trump’s announcement of 25% tariffs on Canada and Mexico—highlighting its similarity to traditional assets, as it reacts to macroeconomic shocks in much the same way. As an emerging macro asset, it naturally experiences volatility during periods of economic uncertainty.

What is also apparent is that Bitcoin’s perceived risk level has greatly diminished in the eyes of regulators, as they increasingly see it as an asset that can integrate peacefully into the existing financial framework.

Institutional boom positions Bitcoin as a macro hedge

While past cycles were dominated by retail speculation, the current cycle is seeing record institutional inflows—$16.6 billion in Bitcoin ETFs alone in Q4 2024, bringing total assets under management (AUM) past $105 billion, according to the latest Coinbase x Glassnode analysis. This level of institutional adoption is staggering, considering that gold ETFs took nearly five years to reach a similar AUM milestone.

Furthermore, open interest in Bitcoin derivatives increased by 60% in Q4 to nearly $100 billion. Spot and derivatives trading volume surpassed $3 trillion per month in the last two months of 2024—the first time this threshold was crossed.

A significant portion of Bitcoin demand stems from investors hedging against excessive government debt and fiat currency risks. According to the latest Congressional Budget Office (CBO) projections:

- The federal budget deficit is set to reach $1.9 trillion in 2025, growing to $2.7 trillion by 2035.

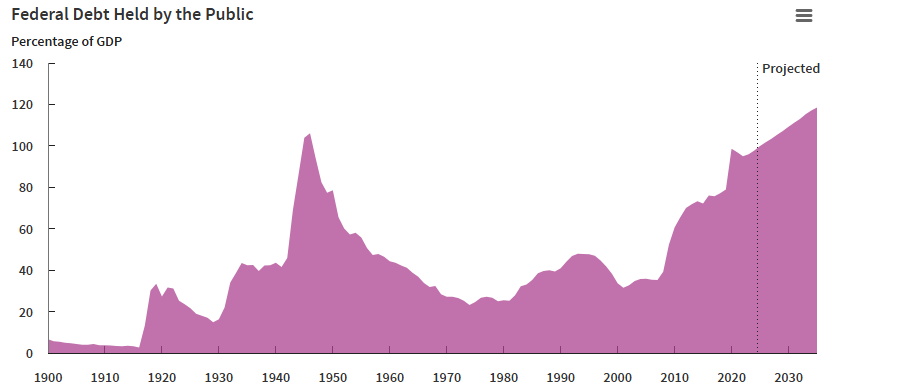

- Federal debt held by the public will surge from 100% of GDP in 2025 to 118% by 2035, surpassing its post-WWII peak of 106% in 1946.

Additionally, CBO projections suggest gradual reductions in the federal funds rate through 2026, along with a decline in the rate on 10-year Treasury notes through the end of 2026. Historically, Bitcoin thrives during periods of monetary easing—as seen in 2020–2021, when unprecedented Fed stimulus fueled a 500% surge in Bitcoin’s price.

With long-term Treasury yields expected to decline and the Fed signaling a measured approach to rate cuts, Bitcoin’s scarcity-driven value proposition is becoming even stronger as investors seek alternatives to dollar-based assets.

Final takeaway

With the federal budget deficit projected to hit $1.9 trillion this year and public debt expected to soar past 118% of GDP by 2035, concerns over the long-term stability of fiat currencies continue to grow. At the same time, the Federal Reserve is signaling its acceptance of crypto and preparing to cut interest rates through 2026—a combination set to spark a surge in liquidity and investment pouring into alternative assets.

Against this backdrop, Bitcoin is shedding its speculative-only past, transitioning into a legitimate macroeconomic hedge.