The late afternoon/evening financial media shows talked about the Monday session as if there had been some significant “risk-off” event. I had to chuckle just a bit at the never-ending effort to sensationalize whatever happens on a daily basis.

For the day, winners beat losers by roughly 9 to 7 at the NYSE, while losers beat winners by a 12/11 margin at the Nasdaq Market Site. Advancing volume took a 45.9% share of composite NYSE-listed trade and a 56.2% share of that metric for Nasdaq listings. Aggregate trading volume, on a day-over-day basis dropped 9.1% across NYSE listings, and dropped 10.9% across Nasdaq listings, while closing the session at a 22% deficit to the S&P 500’s 50-day trading volume SMA, and a 13% deficit to the Nasdaq Composite’s 50-day trading volume SMA.

Sounds like the pros simply yawned and found something else to do with their time on Monday.

That Said…

The ISM Manufacturing Index and S&P Global U.S. Manufacturing PMI for July both hit the tape on Monday after PMIs across the eurozone and China all printed in a state of contraction. While the U.S. results were not quite as poor as were the PMI results elsewhere, they were not exactly encouraging. The headline result for the ISM Manufacturing survey did print above 50 (52.8 to be exact), which is the border between expansion and contraction, but a number of key components are moving in the wrong direction.

New Orders are the lifeblood of any manufacturing survey. For July, from the ISM Manufacturing report, new orders hit the tape at 48.0, down from June’s 49.2, for a second straight month of (now accelerating) contraction. Manufacturing employment also printed in contraction, for a third consecutive month.

What I thought perhaps most interesting in this report, was in prices paid, which still printed well into expansionary territory at 60.0, but that was down from a scorching 78.5 print for June. This drop-off was the steepest single-month slowdown in pricing expansion for the U.S. manufacturing base since 2010. Yes, the economy is slowing. Yes, inflation is as well.

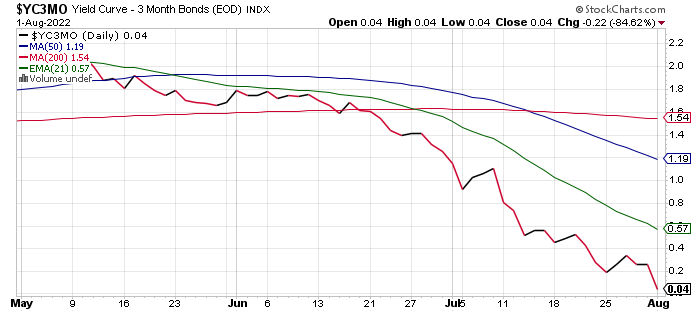

This further pressured the Treasury yield curve, which we brought up in the preceding section. If one still wants to pretend that economic contraction or outright recession is just wordplay, all you have to do is look at the slope of the mangled yield curve.

On Monday, the U.S. 2-Year/10-Year yield spread did this:

While the much more important U.S. 3-Month/10-Year yield spread did this:

Yup, four basis points for tying up one’s money for an extra nine years and nine months. Or is it the likely return of capital or for foreign accounts, the currency exchange rate carry-trade that folks are paying for? A healthy condition this is not.

Stagflation? That depends on inflation. We already know that economic growth has reversed.

Distraction

Markets also kept one eye on the Taiwan Strait as the PLA (People’s Liberation Army) conducted live-fire drills on the island of Pingtan. Of course, these military operations were intended to intimidate as U.S. Speaker of the House Nancy Pelosi tours Asia with stops in Singapore, Japan, South Korea and Malaysia all on the itinerary as well as an unannounced stop planned for Taiwan.

Global media sources are reporting that Pelosi will meet with Taiwanese President Tsia Ing-wen on Wednesday, despite Beijing’s foreign minister spokesperson Zhao Lijian’s statement that “The Chinese People’s Liberation Army will not sit back.”

Pelosi will be flown to Taiwan aboard U.S. Air Force aircraft with an escort of U.S. fighter jets. While I have no idea what Pelosi is or is not trying to accomplish in Asia, I certainly think that the second person in the line of succession to the U.S. presidency should be free to visit with Taiwanese leadership on the island without interference from mainland China if she deems the trip worthwhile.

Not making the trip once Beijing had taken up such aggressive-sounding posture became impossible without Pelosi having appeared to have capitulated to China. Nuff said.

‘I’ll Gladly Pay You Tuesday… For a Hamburger Today’

Do I love Apple borrowing $5.5B when they probably don’t need to, in order to fund share repurchases and dividend payments? Not really. The company ended the June quarter with a net cash position of $48.231B and total receivables of $42.242B. Apple already had $10.982B in short-term borrowings on the books and $94.7B in long-term debt. Over the prior three months, long-term debt had dropped by almost $9B, and had contracted for three consecutive quarters. Even tacking this $5.5B on to that number will not take Apple’s long-term debt-load back up to anything seen since the December 2020 quarter.

That said, at quarter’s end, Apple stood with a current ratio of just 0.86, and a quick ratio of just 0.82. Those are not stellar numbers. Not even close. Yes, I remain long the most widely held stock in our financial universe, and I am encouraged by recent strength in iPhone sales. That said, I would have preferred less borrowing, and less share repurchases.

Tonight’s the Night

Readers should keep in mind that AMD will be reporting performance across four business segments for the first time this evening. Those would be: the Data Center, where we expect to see significant strength, Embedded, Client, and Gaming, where we see potential for weakness.

Economics (All Times Eastern)

08:55 – Redbook (Weekly): Last 13.3% y/y.

10:00 – JOLTs Job Openings (June): Last 11.254M.

10:00 – JOLTs Job Quits (June): Last 4.27M.

16:30 – API Oil Inventories (Weekly): Last -4.037M.

The Fed (All Times Eastern)

10:00 – Speaker: Chicago Fed Pres. Charles Evans.

18:45 – Speaker: St. Louis Fed Pres. James Bullard.

Today’s Earnings Highlights (Consensus EPS Expectations)

Get an email alert each time I write an article for Real Money. Click the “+Follow” next to my byline to this article.