Feline Lim/Getty Images News

Investment Thesis

Despite the recent correction, Apple Inc. (NASDAQ:AAPL) stock continues forward on its long-term uptrend. While the Invesco QQQ ETF (QQQ) recently went into a bear market, AAPL stock is down by less than 15% from its all-time high. The strength and confidence of investors in Apple CEO Tim Cook & Team has continued to buttress AAPL stock’s onward march.

Nevertheless, AAPL is not immune to the tech bear market as a tech stock. However, we believe such opportunities have presented investors with a long-term perspective another fantastic opportunity to add AAPL stock at fair value.

Apple has continued to demonstrate the mastery of its supply chain through several product launches. The Cupertino-based company has been unfazed by the supply chain snarls, even though it was also impacted. However, Apple’s well-established partnership with its suppliers and its massive scale have reinforced the strength of its supply chain. Furthermore, the company has continued to demonstrate its willingness to focus on users first. Apple’s “unilateral” move to deprecate its IDFA has sent advertisers and publishers into a tailspin. Despite that, surveys have shown that Apple’s move has been well received by its users. Therefore, Cook was also praised by Berkshire Hathaway (BRK.A) (BRK.B) CEO Warren Buffett recently, as he emphasized (edited): “Tim Cook, Apple’s brilliant CEO, quite properly regards users of Apple products as his first love, but all of his other constituencies benefit from Tim’s managerial touch as well.”

We discuss what investors should consider when investing in AAPL stock. We also share why AAPL stock is a Buy.

Pros Of Buying Apple Stock

Over the past year, the supply chain snafu has demonstrated the prowess of Apple’s supply chain leadership. We have also discussed it extensively in our previous articles (here and here). We shared that Apple’s mastery over its suppliers has assured tremendous supply visibility for the company. The company has become Taiwan Semiconductor’s (TSM) largest customer. Their relationship has continued to deepen as Apple leveraged TSMC’s advanced packaging technologies to develop its UltraFusion packaging architecture.

Therefore, it has made possible the development of its latest M1 Ultra SoC, which Apple introduced in its latest Mac Studio product. TSMC and Apple engineers work closely together, as both companies are heavily dependent on each other for their success. Therefore, we believe that Apple has been able to depend on TSMC reliably for the production and future development of its advanced chips, well ahead of its peers.

Therefore, investors should never discount Apple’s supply visibility with TSMC. Qualcomm (QCOM), which uses both Apple and Samsung (OTC:SSNLF) as part of its multi-sourcing strategy, was disappointed with the yield in its 4nm chips produced by Samsung. Therefore, the company has reportedly asked for TSMC’s 3nm capacity to produce its next-gen 3nm chips. The foundry race will continue to intensify as Samsung is still a distant #2, while Intel (INTC) is likely not competitive until 2025. Therefore, Apple investors can rest assured that the strength of its relationship with TSMC is highly beneficial.

In addition, Apple’s ability to vertically integrate hardware and software “seamlessly” has continued to wow us. Apple’s Silicon Engineering Group is a leading chip designer that demonstrated Apple’s prescience to move away from Intel for its chips. It has allowed Apple tremendous leverage to customize its chips and expand its scope of products with multiple permutations. And Apple’s customized silicon has continued to dazzle its users. Couple its vertical integration with its iOS gatekeeper role, we believe that Apple’s moat is unique. We think no other company has created such a powerful moat encompassing software prowess, silicon edge, and consumer ecosystem dominance.

Cons Of Buying Apple Stock

AAPL stock consensus price targets Vs. stock performance (TIKR)

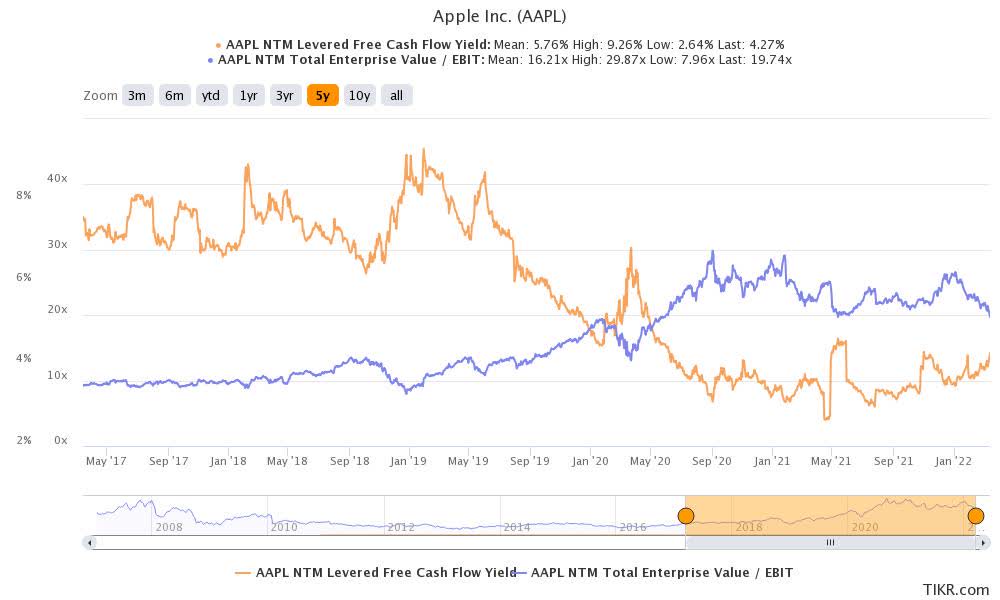

AAPL stock EV/NTM EBIT & NTM FCF yield % (TIKR)

AAPL stock has outperformed the NASDAQ as it has not entered a bear market. Therefore, we are not surprised that AAPL stock is not undervalued. We can also observe from the first chart above that AAPL stock is still a distance from its most conservative price targets (PTs). In contrast, many tech stocks that we monitor have already breached their most conservative PTs during the recent market rout.

Furthermore, its NTM EBIT multiple and FCF yield are not markedly higher than its 5Y mean. Therefore, one can argue that AAPL stock doesn’t seem attractive enough. We concur to a certain extent. AAPL stock returned 346% (CAGR: 34.7%) over the past five years. Therefore, investors should not expect such fantastic gains over the next five years. Hence, if you are hunting for an undervalued stock to add due to the tech rout, AAPL stock is certainly not one of them.

Furthermore, the company’s exposure to TSMC as its sole foundry also lends itself to political risks concerning China. Some investors have also been concerned about whether China would consider a potential invasion of Taiwan in the future. Therefore, if Russia was successful in its war against Ukraine, these investors think that China could be emboldened to attempt an invasion against Taiwan.

In addition, Apple also depends on Foxconn (OTCPK:HNHAF) to produce its hardware products. The recent COVID-19 lockdown in Shenzhen has affected Foxconn’s production, forcing it to divert to other plants. Nevertheless, Foxconn has a well-diversified supply chain, and Shenzhen accounted for about 20% of its production. But, if the highly transmissible Omicron variant were to spread to Zhengzhou, the impact could be significant. Analysts estimated that Zhengzhou accounted for 50% of Foxconn’s China production. Therefore, if an extended lockdown were to occur, it would most likely impact AAPL stock.

Bottom Line: AAPL Stock Is A Buy

We are long-term AAPL stock investors. Apple’s management has consistently demonstrated its execution prowess over the years, and Cook rarely has disappointed. Therefore, we believe that AAPL will find a way to manage an adverse impact on its production if any. We see any potential “thrashing” of AAPL stock price as an opportunity to add long-term exposure if that happens.

Therefore, we reiterate our Buy rating on AAPL stock.