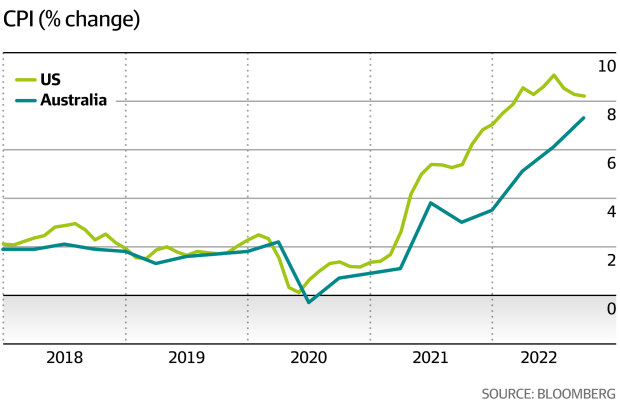

Alphabet missed analyst consensus estimates almost across the board. It reported weaker advertising revenue through Search and YouTube and higher operating expenses as spiralling inflation crimped growth in digital advertising and Apple’s privacy changes made it harder to target ads. This also showed up in Snapchat’s results last week.

Totus Capital’s Ben McGarry also pointed to Alphabet’s rate of headcount growth, which added nearly 13,000 staff in the third quarter and is expected to add less than half of that in the upcoming quarter, as other firms cut back on costs.

“People want to see action taken in an inflationary environment to manage costs and slowing the rate of growth… headcount reductions would have been better received,” he said.

Bleak times

Things weren’t much better at Microsoft as investors fretted about a slowdown in the software giant’s growth engine Azure, their cloud-computing arm which has now missed estimates for two straight quarters. The company posted its weakest quarterly sales growth in five years, throttled by the surging dollar and slumping PC demand. It also issued disappointing revenue forecasts.

As the week progressed, Meta forecast a bleak holiday quarter with significantly higher costs next year, sending its shares down 20 per cent in premarket trade and wiping about $US67 billion ($104 billion) off its market value.

Shareholders are starting to get restless. A scathing open letter from Brad Gerstner of Altimer Capital to CEO Mark Zuckerberg said Meta had “lost of confidence of investors”, drifting into the land of excess in a low rate world. He suggested layoffs, reducing capex and limiting the company’s metaverse investment.

“This lack of focus and fitness is obscured when growth is easy but deadly when growth slows and technology changes,” Gerstner wrote.

Amazon and Apple added to investor woes on Thursday. The former plunged 19 per cent after hours due to weaker-than-expected revenue and disappointing projections for the fourth quarter, while the latter reported weaker-than-expected iPhone and services sales.

“It’s been like watching speed trains derail from afar,” DNR Capital analyst Chris Tynan said.

“There was an expectation that these digitisation trends would continue at the pace brought forward during the pandemic. It looks like they’re not going to meet those expectations.”

The US earnings season is also happening at a difficult time for the equity market. Valuations of tech and communications services stocks have tumbled, leading declines on the S&P 500, as ultra-low interest rates which drove much of the sector’s growth through the pandemic are rolled back to combat soaring inflation.

Now, the market is glued to company earnings, watching for signs of sensitivity to the economy in a more hostile trading environment.

Outside of tech, US earnings are showing signs of resilience, presenting investors with a complex picture. Stronger-than-expected earnings from Bank of America fuelled optimism that US consumers are till spending in the face of soaring inflation and aggressive tightening by the Federal Reserve.

Netflix stemmed its subscriber losses in the third quarter, as popular programmes including the fourth season of Stranger Things helped it add 2.4 million members. The company has launched a lower-cost advertising-supported streaming service and a plan to limit widespread password sharing to shore up its business in the face of maturing subscription growth.

A low bar

Of the 170 companies in the S&P 500 reported so far, 75 per cent delivered consensus-beating results, according to Refinitiv data published by Reuters.

But they have a low bar to clear. Analysts now see aggregate S&P 500 earnings growth of 2.3 per cent, down from 4.5 per cent at the beginning of the month, Reuters reported.

Hugh Selby-Smith, co-chief investment officer at Talaria Capital, has been struck by the lack of earnings guidance issued by management. By his count on Tuesday, of the 101 S&P 500 companies that had reported, only 23 issued official guidance, down from 70 per cent this time last year.

Hugh Selby-Smith of Talaria Capital wants to see more forward guidance.

“It’s a function of uncertainty,” he said. “CEOs are among many things sales people. If they’re unsure about what it is the market wants to see, it’s easier not to say anything.”

With more companies due to report over the next two weeks, McGarry said weak tech earnings were a warning to investors who relied on the seemingly unstoppable tech sector over the past decade to boost returns.

“Valuations were starting to look reasonable so long as the earnings were holding on, but now we’re starting to see the earnings downgrades come through,” he said.

“That’s generally the second phase of a bear market. First, you get a valuation adjustment, second is the earnings adjustment.

Wake-up call

“It’s a bit of a wake-up call. If there’s a recession, or the economy is slowing, it’s probably not going to be one quarter, and then we bounce back sharply.

“The old rule of thumb is don’t buy the first downgrade. I wouldn’t be surprised if there are a few quarters of weak growth for big tech.”

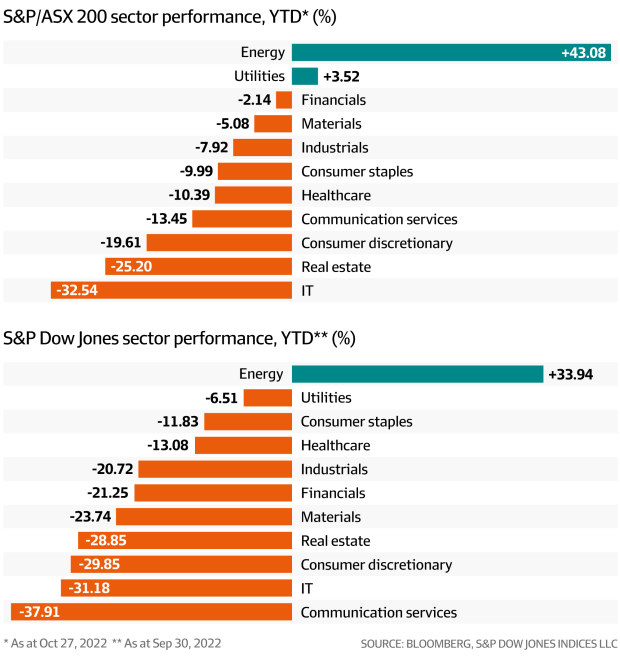

Analysts who spoke to The Australian Financial Review were reluctant to read weak US earnings through to the Australian market because of the S&P/ASX 200’s heavier weighting in resources and financials and the comparatively stronger economic outlook. However, they noted some specific names where investors should keep watch.

UBS telco, media and tech analyst Lucy Huang said media companies leveraged to advertising revenue could be impacted from an extended downturn, but she noted that a recessionary-type scenario was already priced in.

Tech companies with large energy-hungry data centres are another one to watch as electricity prices rise, which represent a large component of the cost base, she said. Microsoft results revealed an unexpected jump in data centre energy costs as Europe’s energy crisis eroded profitability.

Totus Capital’s McGarry said the lower growth rate for Azure was notable for data centre provider NextDC, a company that the firm is shorting.

UBS analyst Lucy Huang says companies reliant on ad revenue are doing it tough.

“It’s leveraged to that cloud infrastructure dynamic and if that’s slowing, that could impact them over time,” he said, also noting rising costs and more competition in the sector.

DNR’s Tynan also pointed to the impact on companies from a cloud computing slowdown.

“If you see the take-up and transition to the cloud as not as rapid as people were expecting during the pandemic, and you’ve got SMEs and enterprises delaying systems migrations,” he said.

“Microsoft pointed to business optimising workloads – trying to do more with less. These will impact the providers to some of these big tech names – NextDC, Appen, Megaport.”

Totus has been long US big tech for several years, but McGarry said they had reduced their exposure. But with small holdings in Microsoft and Alphabet, he said if companies focussed on cutting costs, there could be a multi-year opportunity.

“The likes of Apple have been able to keep costs flat and grow the top line and buyback stock,” he said.

“It’s been the best performing mega cap tech stock. So if the others get the memo…”

Perpetual’s Rice is still positive about Microsoft’s long-term outlook, but he harbours concerns for Alphabet and Meta.

“It seems like their core businesses are rapidly maturing, and it’s not clear what the next act is… what’s going to take off,” he said.

He sees greater opportunity in small to mid-cap high-growth tech which has been obliterated over the past year.

For many years it didn’t matter what you bought – you just needed to be part of the rally. That’s definitely changed

— Jonas Palmqvist, portfolio manager, Alphinity

Palmqvist said in this part of the cycle, it was all about being selective.

“The negative earnings cycle isn’t done yet,” he said.

“In fact, we think earnings downgrades globally are accelerating now. But it’s not everywhere. Even within tech, there are pockets that are seeing earnings upgrades.

“I think being really selective is key. For many years it didn’t matter what you bought – you just needed to be part of the rally. That’s definitely changed now.”