Even though the saga started after the fiscal quarter ended, Apple’s Q2 financial results are going to be profoundly different thanks to the Trump tariffs. Here’s what to expect from the results on May 1.

As regular as clockwork, Apple will be reporting its Q2 2025 earnings on May 1, with the results released ahead of the standard analyst and investor conference call at 5p.m. Eastern.

Apple’s CEO Tim Cook will be on the call, along with newly-installed CFO Kevan Parekh, to discuss the results and to take on questions from analysts.

Given the turbulent April Apple endured thanks to the introduction of tariffs against China and the rest of the world by President Donald Trump, Cook and Parekh will probably have a lot more questions about the supply chain than normal.

Last quarter: Q1 2025 details

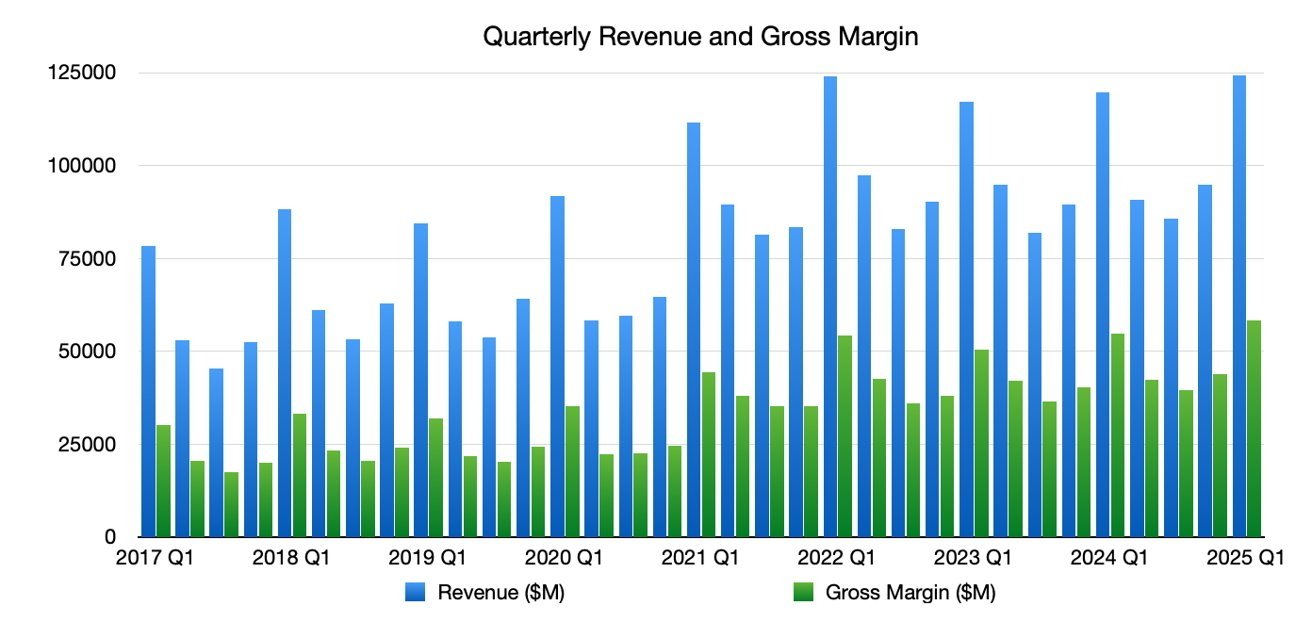

The Q1 results saw Apple report its highest figures for the year, including revenue growing year-on-year to $124.3 billion from $119.58 billion in the year-ago quarter.

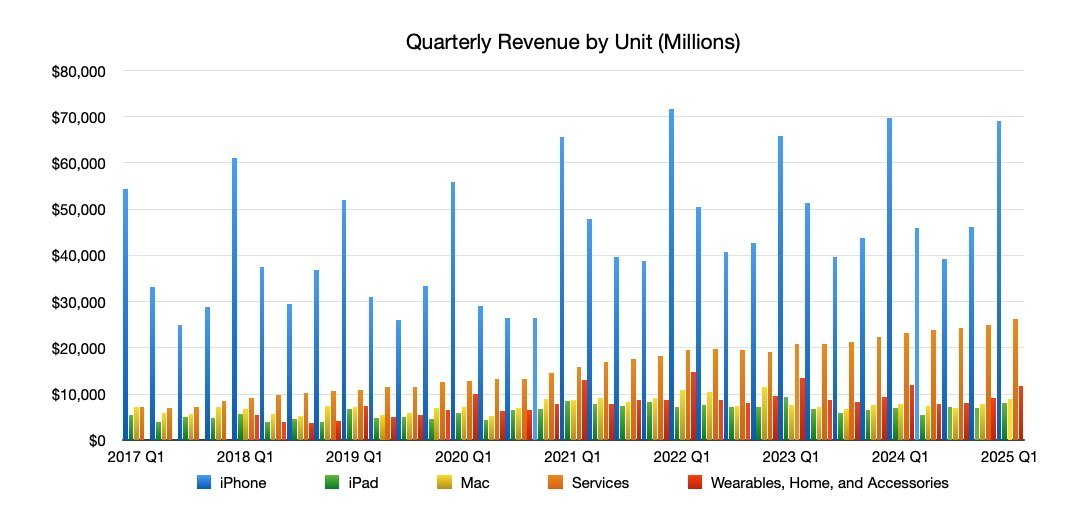

On a unit basis, iPhone was relatively flat year-on-year at $69.1 billion for the quarter, iPad rose from $7.02 billion to $8.088 billion, and Mac rose from $7.78 billion to $8.99 billion. Wearables, Home, and Accessories saw a small dip from $11.95 billion to $11.747 billion.

Apple quarterly revenue and gross margin as of Q1 2025

Services continued its growth streak, from $23.12 billion in Q1 2024 to $26.34 billion in Q1 2025.

That quarter had a lot of preceding launches, including the iPhone 16 range, USB-C on AirPods Max, the Apple Watch Series 10, and the Black Apple Watch Ultra.

Apple’s board of directors declared a cash dividend of $0.25 per share of common stock. The Earnings Per Share was listed at $2.41.

On a regional basis, which is quite pertinent this time around, Greater China revenue saw a YoY dip from $20.8 billion to $18.513 billion.

Year-ago quarter: Q2 2024

Typically the benchmark for comparison for the current quarter’s results, the Q2 2024 results were a bit of a dip for the company. Overall revenue of $90.75 billion was down from the previous Q2 2023’s figure of $94.8 billion.

Even so, there were quite a few positives. For a start, Apple beat Wall Street, with its consensus putting Apple’s revenue at somewhere between $82.32 billion and $86.15 billion.

Apple’s EPS of $1.53 was up year-on-year from $1.52, and also beat Wall Street’s forecast of $1.50.

Apple quarterly unit revenue, as of Q1 2025

That quarter had relatively few product launches, including the release of the Apple Vision Pro, as well as M3 Apple Silicon updates to the MacBook Air range.

Revenue from iPhone was $45.96 billion, down YoY from $51.3 billion. Mac was flat, from $7.45 billion one year prior to $7.2 billion.

There was a dip for iPad from $6.7 billion to $5.56 billion, while Wearables, Home, and Accessories shifted downward from $8.76 billion to $7.9 billion. Services kept up its growth trend, going from $20.9 billion in Q2 2023 to $23.9 billion in Q2 2024.

What happened in Q2 2025

As usual for the period, Apple had some product launches, including the iPhone 16e, the 11th-gen iPad, the M3 editions of iPad Air, the M4 MacBook Air, and an updated Mac Studio.

While it won’t have the same impact as in the massive Q1 results, there will still be the lingering effects of product launches from the end of 2024, including the iPhone 16 generation, a new iPad mini, and the November Mac launches.

These will have a material impact on revenue in the Q2 results.

Post-quarter Trump tariffs

A current hot-button issue that will be raised during the analyst conference call, and that Apple will probably advise on, is the state of tariffs. After the quarter ended, the Trump administration decided to issue “reciprocal tariffs” against each country in the world.

Given the volatile nature of the situation, it is almost certain that the tariffs, and what Apple can do to mitigate their effects on the supply chain as a whole, will dominate the analyst chatter.

The tariffs were heralded very early in Apple’s second quarter, but were not implemented until April, after the quarter ended. The tariffs won’t impact the results of the quarter itself, but will almost certainly play a factor in Q3 and future quarter discussions.

The tariff fight included a period of tit-for-tat rises, with Trump setting a high rate for China, then China fighting back with its own on imports from the U.S., followed by a response by Trump.

The affair severely impacted Apple’s stock price, with investors worried about the potential high price rises of Apple goods in the United States, caused by the tariffs.

Eventually, Apple and other tech companies were given some respite in the form of an exception. This is, however, temporary until new “semiconductor tariffs” arrive in the future.

China, meanwhile, was fed up of raising its tariff against U.S. goods, and went a different route. Instead, it ceased the exports of rare earth minerals and magnets, which can impact supply chains around the world.

While investors may be worried about future iPhone pricing, it probably won’t affect sales that much. Analyst research has determined that the intention to upgrade in the next 12 months is at an all-time high.

However, that survey occurred in March, before the tariffs hit the world. Consumer opinion may have changed a lot since then.

Wall Street Consensus

The Wall Street consensus refers to a survey of analysts. The results are averaged out to give a general opinion of where investors and analysts are leaning in their quarterly forecasts for Apple.

Yahoo Finance

In the estimates published by Yahoo Finance as of April 21, 27 analysts offered an average revenue estimate of $93.97 billion. The estimated range goes from a high of $95.9 billion to a low of $89.4 billion.

For the earnings per share, a group of 27 forecasts an average of $1.61, with a high of $1.66 and a low of $1.47.

TipRanks

On April 21, TipRanks offered its own consensus figures. The revenue forecast is at $93.94 billion, with a range from $89.4 billion to $95.9 billion.The earnings per share is expected to be $1.61, with a range from $1.47 to $1.67.

Analyst Expectations

As Apple’s results get closer to release, analysts offer what they believe will be included in the issued figures, and where Apple’s future could lead for the coming year.

Morgan Stanley

Morgan Stanley’s last major move on Apple was a cut of its price target from $275 to $252 on March 12, before the tariff trouble began. Analysts posited that the continued postponement of Siri improvements will temper iPhone upgrade rates.

At the time, analysts reduced the firm’s iPhone shipment forecast for the year to 230 million units, equating flat shipments year-on-year, but rising to 243 million in 2026. The slower-than-expected iPhone replacement cycle also cut down Morgan Stanley’s full-year revenue estimate to $436 billion.

On April 22, it reaffirmed its “Overweight” rating and a $200 price target.

Wedbush

On April 13th, Wedbush lowered its full-year earnings per share estimates for Apple, from $7.44 per share for the year to $7 flat. Wedbush’s consensus estimate puts Apple at $7.28 for the full-year earnings

Wedbush holds an “Outperform” rating for Apple, with a $250 price target.

Goldman Sachs

On March 6, Goldman Sachs reaffirmed its “Buy” rating for Apple, with a price target of $294.

The decision followed Apple’s March Mac updates, which Goldman Sachs analysts believed would help Apple reach a Q2 revenue growth target. That growth isn’t massive, with low to mid single-digit movement expected at around 6%, and an estimated revenue figure of $95.9 billion.

Evercore

On April 15, Evercore believed Apple was poised for upside in the quarter, but said the focus is on Q3, and how Apple deals with the tariffs. This included using aircraft and its logistical prowess to import products into the United States.

Overall, Evercore maintained its “Outperform” rating for the stock, with a price target of $250.

UBS

On April 14, a UBS note to investors offered that Apple had a strong financial health score. It had a robust position with $137.53 in EBITDA and a 46.5% gross profit margin that served as a buffer of sorts against regulatory issues like the tariffs.

It maintained a “Neutral” rating for Apple, with a price target of $236.