Apple CEO Tim Cook

Apple’s fourth fiscal quarter results will be issued on November 2. Here’s what happened in the quarter and what to expect Apple will reveal in its figures.

Apple confirmed on October 5 that it will announce its fourth-quarter earnings on November 2. As is customary for the results, a conference call will follow, hosted by CEO Tim Cook and CFO Luca Maestri, with the results due at around 4:30 p.m. ET followed by the call itself from 5:00 p.m. ET.

Last Quarter: Q3 details

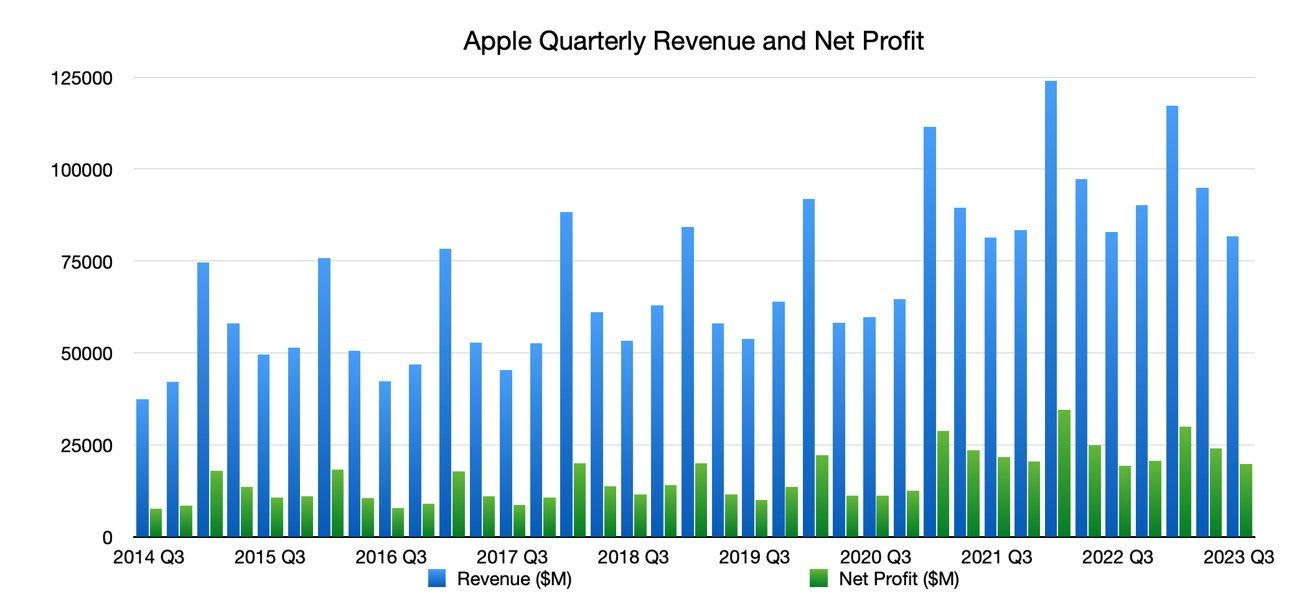

Apple’s results release for the last quarter, Q3, was relatively level for the company, with it posting revenue of $81.8 billion for the period, down just 1% year-on-year. The quarterly earnings per diluted share was up 5% year-on-year, however, at $1.26.

Traditionally the quietest quarter, iPhone revenue was down 2% year-on-year to $39.67 billion, with iPad down 20% to $5.79 billion, and Mac down 7% to $6.84 billion. Wearables, Home, and Accessories saw a 2% rise to $8.28 billion, and Services saw an 8% YoY growth to $21.21 billion.

For the quarter, Cook mentioned the “all-time revenue record” for Services driven by over 1 billion paid subscriptions. Maestri said the quarterly YoY performance improved from the March quarter and that Apple had a “very strong operating cash flow of $26 billion.”

During the Q3 quarter, Apple made several product introductions, including the M2 Max and M2 Ultra versions of the Mac Studio, the Mac Pro with Apple Silicon, and the 15-inch MacBook Air. While the launches had a small effect on the Q3 results, their availability throughout the whole of Q4 should be more meaningful for investors.

This was also the quarter that Apple WWDC revealed the Apple Vision Pro, a product that won’t have any meaningful impact on the balance sheet until its launch, sometime in early 2024.

As usual for Apple’s financials, the company declined to offer a forecast for the Q4 results.

Year-Ago Quarter: Q4 2022

With year-on-year figures being important to investors, the data points compared to the year-ago quarter of Q4 2022 will be important.

At that time, Apple earned $90.15 billion in revenue, with an earnings per share of $1.29.

Revenue from iPhone was up 9.7% to $42.6 billion, iPad went down 13.1% to $7.17 billion, and Mac sales skyrocketed 25.4% to $11.5 billion. Services reached $19.18 billion, and Wearables, Home, and Accessories rose to $9.65 billion.

What happened in Q4 2023

The quarter, which runs from the start of July until the end of September, is usually a great time for Apple to introduce the products that it will be releasing to take advantage of holiday season sales. Due to the timing, this will always include the annual September Special Event, which sees the launch of iPhones.

There were slightly fewer products launched in the quarter than in Q4 2022, partly because of the timing of launches in both periods. For example, Apple launched an updated MacBook Air at the start of Q4 2022, but it launched the Mac Studio, Mac Pro, and MacBook Air at the end of Q3 2023 instead.

Since these were all introduced on September 22, there will be minimal impact to Apple’s revenue since any possible preorders or purchases were only made in a little more than a week in the quarter itself.

Investors probably won’t see much benefit from the launches for the quarter, with the holiday season sales during the next quarter, Q1, will always be the big one to watch for.

What Wall Street Thinks

Using figures sourced from Yahoo Finance on October 23, a consensus of 24 analysts reckon that Apple will report a revenue of $89.25 billion on average. The estimates ranged from $87.8 billion at the low end to $92.1 billion on the high side.

The group’s earnings per share estimate is $1.39, based on the opinions of 28 analysts. The range is from $1.35 to $1.45.

Analysts monitored by CNN Money on October 23 believe the fourth quarter revenue will be $90.3 billion on average. The range goes from $82.8 billion at the lowest point to $97.2 billion at the highest.

The earnings per share estimates have a consensus of $1.36, ranging from $1.17 to $1.51.

On Marketwatch on October 23, the analyst estimate consensus for the earnings per share is $1.39, with a range of $1.35 to $1.45.

Individual analysts on Apple

Quarterly revenue for Apple.

JP Morgan

In an October 30 note from JP Morgan seen by AppleInsider, analysts believe that revenue of $88.9 billion will be reported for the fourth quarter, implying a -1 YoY decline. Slow momentum in consumer spending on smartphones, PCs, and tablets is blamed for this trend.

There is an expected growth of 7% in iPhone revenue to $45.8 billion, thanks to a period of inventory build and an extra week of shipping compared to the iPhone 14 series. Lower demand in China and underwhelming consumer spending momentum have been “driving an elongation of the replacement cycle,” JPM reckons, impacting sales of recently launched products.

Services is expected to reach double-digit growth again, offsetting hardware revenue contractions. Price increases for Services products will help accelerate growth, but JPM thinks it will also drive consumers towards bundled plans.

Apple will “modestly beat consensus for earnings with tight cost control and robust gross margins,” the analysts write, in what is described as results that “fare better than feared.” Earnings per share is forecast at $1.40.

JPM has a 12-month price target of $2.30 and rates Apple as “Overweight.”

Morgan Stanley

The October 30 note from Morgan Stanley has Apple posting a “better than expected Sept Q but guide to a below seasonal/Consensus Dec Q,” which creates “a tactically cautious setup.”

Overall revenue is expected to hit $89.9 billion with a $1.39 EPS. Revenue from iPhones is thought to be around $45 billion, with Canalys and IDC figures indicating shipments of 50M to 53M in the quarter as being higher than Morgan Stanley’s 48M forecast.

“We know iPhone channel inventory was at the low end of the normal range coming into the quarter, and thus it’s reasonable to assume shipments could have outpaced builds in the quarter given the need to fill the channel,” the firm writes.

An acceleration of Services growth is expected again, and record gross margins are expected to be called out during the results.

AAPL is rated as “Overweight” by Morgan Stanley, with a 12-month price target of $210.

Oppenheimer

In an October 30 interview, Oppenheimer cut its price target for Apple from $220 to $200, citing China demand concerns and “macro-related factors.” A lack of return for consumer sentiment and worsening exchange rate headwinds make the quarter tough for the iPhone maker.

For the period, it is reckoned that iPhone, Mac, and iPad shipments will be “weaker than what we expect.” However, demand in North America and Europe is still considered “pretty healthy,” thanks to “robust” net additions from carriers.

Piper Sandler

Piper Sandler used its pre-financials note to discuss Q1 2024 earnings estimates rather than Q4 2023. The discussions were largely about weak demand in China potentially harming Q1 earnings and the iPhone 15 product mix leaning towards Pro models that could boost the ASP and the upgrade cycle being timed more towards iPhone 12 users.

There were relatively bits of Q4 2023 data in the note seen by AppleInsider but not much dialog on the quarter itself.

For the most pertinent figures for Q4, Piper Sandler reckons Apple will reach revenue of $87.8 billion, with an EPS of $1.36. It holds a 12-month price target of $220 and rates AAPL shares as “Overweight.”

")