BeeBright

Thesis

Readers familiar with my writings know that I have been a perpetual bull for both Berkshire Hathaway (BRK.A) (NYSE:BRK.B) (“BRK”) and Apple (NASDAQ:AAPL). My overall view is that both stocks are excellent choices for long-term investors and really can be bought (or added) most of the time.

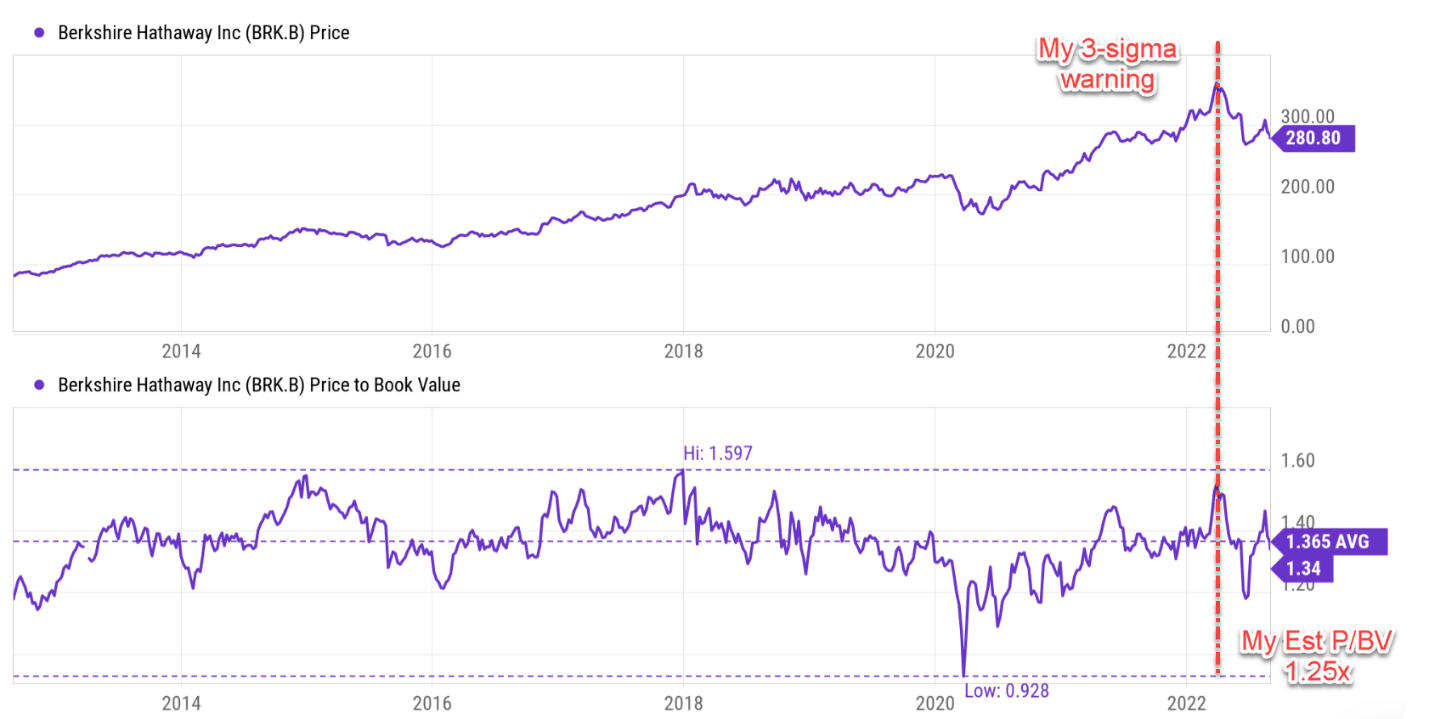

Although occasionally, extreme market movements make sometimes obviously worse and sometimes obviously better than most. For example, earlier this year in March, I wrote an article to show how expensive it was (what I called a 3-sigma event) and why a valuation contraction was highly likely. At that time, the stock was valued at 1.8x BV, almost above its historical mean by 3x sigmas. Many investors did not see it that way because they used the BV from the previous quarter, which was delayed (and higher). As a result, they saw a valuation lower than it actually was. Indeed, the stock prices have corrected substantially afterward as you already know.

Now, investors seem to be making the same error again, except in the opposite direction. Its valuation is reported at 1.34x as seen. But next, you will see why I think its current valuation is actually lower than 1.34x and my estimate is at 1.25x only. Furthermore, you will see the implications of such a valuation for investors (like myself) who want to own AAPL shares through BRK. I just set a $255 limit order to buy BRK.B shares with a real intention of owning AAPL shares. And you will why such a target price essentially allows me to own AAPL shares at a valuation ranging from about 9x of owners’ earnings to free.

Finally, before we dive in, note that all the subsequent analyses will be presented in terms of Berkshire Hathaway B shares. There are certainly differences between A and B shares (voting power et al). But in terms of economics, the use of financial data based on either A or B shares should be equivalent.

Seeking Alpha

BRK valuation is closer to the Buffett price than you think

As just mentioned, BRK’s current valuation is reported at 1.34xBV, close to its historical mean of 1.36x. Buffett mentioned multiple times that he would be an enthusiastic buyer of BRK shares at a price near 1.2x book value. So, the current price is above the “Buffett price” by more than 11% as reported. Not too attractive on the surface.

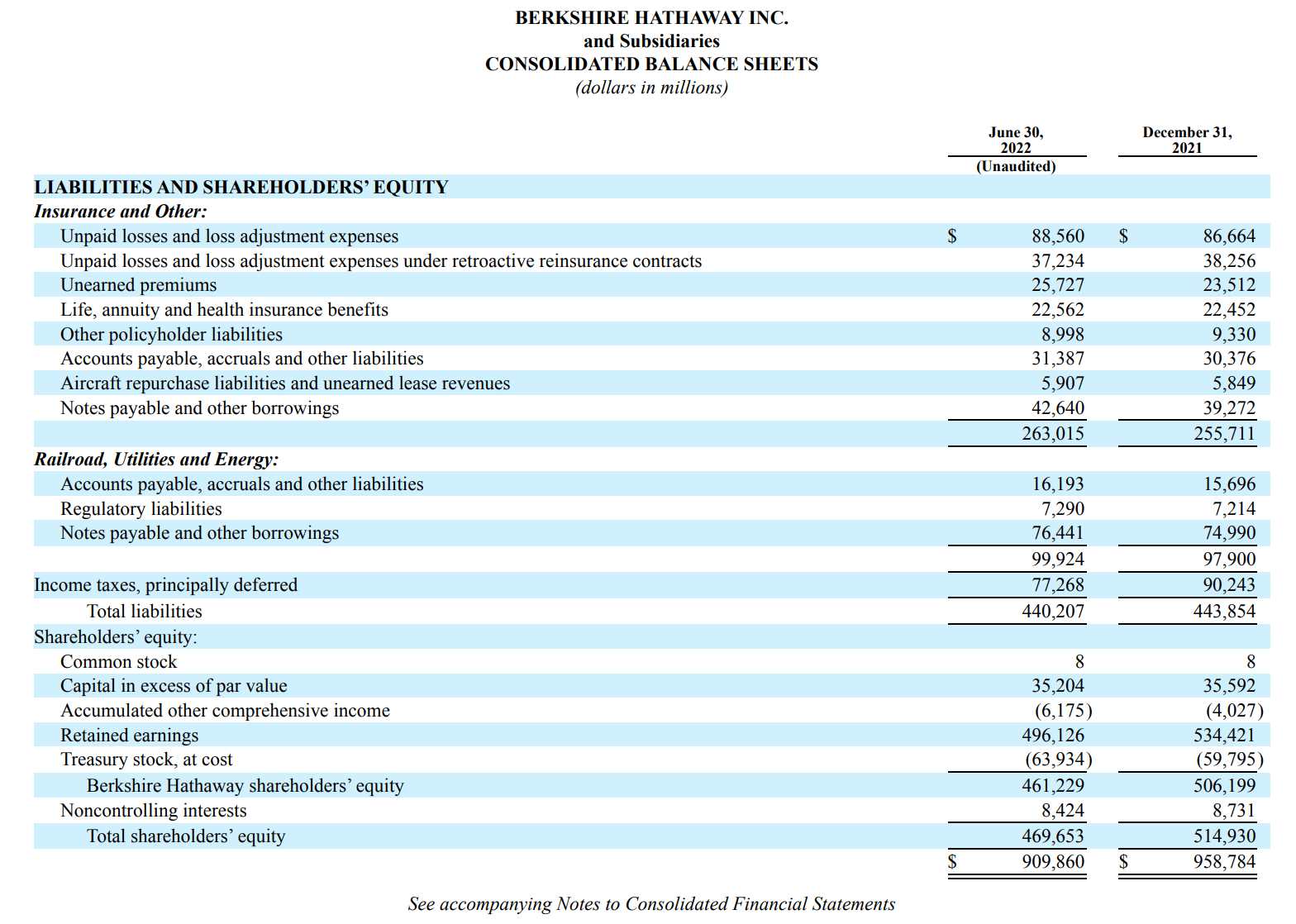

However, if you consider that A) the reported BV is based on its June 30, 2022, filing, and B) the market has moved up since then and thus its BV has expanded, you will get a different valuation. As an estimate, as of June 30, 2022, it reported a share count of 2.205 billion of equivalent B share outstanding and total equity of $469.6B, translating into a book value of $213 per share (and hence a P/BV multiple of ~1.34x at today’s price of $280 as of this writing).

But we need to consider that the market has rallied by about 5% since June 30 (the S&P 500 rallied from 3785 then to the current level of 3936). Now if we assume (I have to emphasize that this is an assumption) BRK BV rallied by the same amount too, then its current BV would be $223 per share. This would mean a P/BV ratio of 1.25x only at the current price, not only below the historical mean (by about 10%) but also quite close to the “Buffett price” of 1.2x book value.

BRK June-30, 2022, 10Q

The real meaning of the Buffett price

In case you ever wondered why/how Buffett picked a 1.2x target valuation out of thin air, it is because (at least in my opinion) owning BRK at 1.2x book is equivalent to owning its operating businesses at a dirt-cheap price – at only about 4x operating cash flow (“CFO”) as you can see from the table below.

As shown in the following table, Berkshire earns about $22 billion of operating earnings in recent years or about $10 per share. To wit, my estimate for its 2022 CFO is $10.75 per share. Most of us know that the reported PE ratios (see the second table below) are quite meaningless for a business like BRK because the GAAP numbers do not reflect its true economics at all. For example, in GAAP terms, according to its recent shareholder letter:

Berkshire earned $42.5 billion in 2020, which includes 4 main components a) the ~$22 billion operating earnings already mentioned, b) a $4.9 billion of realized capital gains, c) a $26.7 billion gain from an increase in the amount of net unrealized capital gains that exist in the stocks, and d) an $11 billion loss from a write-down.

Out of all these four components, operating earnings are what count most and are most relevant to the fundamentals of the business. However, it is not even the largest item based on the GAAP standard. Such discrepancies between accounting and economic earnings really illustrate the distortion in the commonly quoted PE ratios.

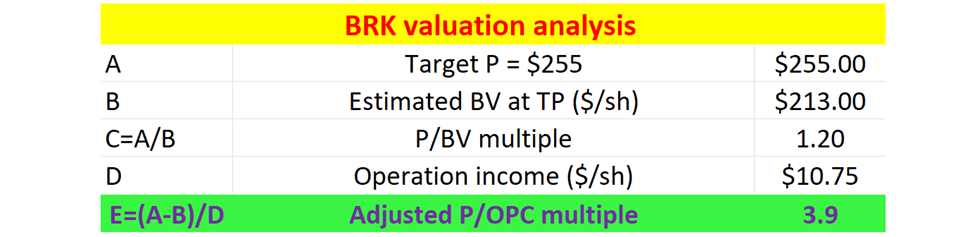

The first table below shows my method to correct such distortion. In this table, I am assuming that if my target price of $255 is reached, BRK’s book value will drop to its June 30 level, i.e., $213 per share. My observations show that market price always moves more than its book value. So, if my order is triggered, I get to buy BRK at a price of $255 per share. Then as a thought experiment, I could immediately liquidate the cash and all other equity investments (risks embedded in this assumption are discussed in the end), which would be worth $213. Therefore, I have essentially paid $42 to buy all the BRK operating business segments. Also just established earlier, these operating businesses are expected to generate an OFC of $10.75 per share. As a result, I would be paying about 3.9x OFC for all of BRK’s operating businesses.

And this table also illustrates why I set my limit order at $255 – this price corresponds to a P/BV multiple of 1.2x, i.e., exactly the Buffett price based on my projected BV of $213 if/when the target price is reached.

Author

Seeking Alpha

What does this mean for AAPL?

Next, we will see the implications of a $255 target price for investors who want to own AAPL shares via BRK.

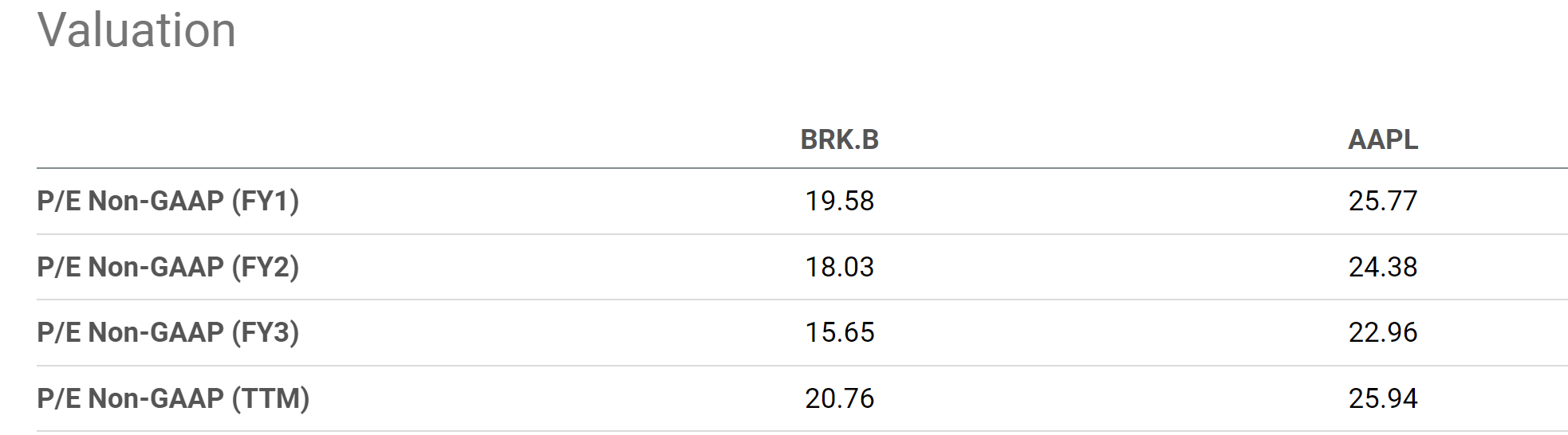

Firstly, the commonly quoted PE based on accounting financials also exaggerated AAPL’s valuation (by understating its true earning power). As you can see from the table above, AAPL’s current PE is quoted at 25.9x on a TTM basis and at 25.8x on a forward basis. Definitely not a “cheap” valuation by any stretch.

However, as argued in my earlier articles, AAPL is such a capital-light business that a good portion of its CAPEX expenditures are for growth and should not be considered a cost and should be added back to the owners’ earnings. Only the part that is for maintenance CAPEX should be considered a cost. Readers interested in more details could take a look at my earlier article and are highly recommended to take a look at Greenwald’s book entitled Value Investing.

All told, AAPL’s FWD EPS is about $6.10 on an accounting basis. But its true earnings power is higher by a good margin. Probably you can already see such a discrepancy by comparing its free cash flow versus its EPS. Its FWD free cash flow is estimated to be $6.35 per year, about 4% above its EPS. And even the free cash flow underestimates its true earning power because the free cash flow considers ALL the CAPEX expenditures as costs. When the growth part of the CAPEX is added back to the earnings, my estimate of its owners’ earnings is about $6.73 per share. As a result, its PE on the owner’s earnings basis is about 23.3x, not as high as it seems on the surface.

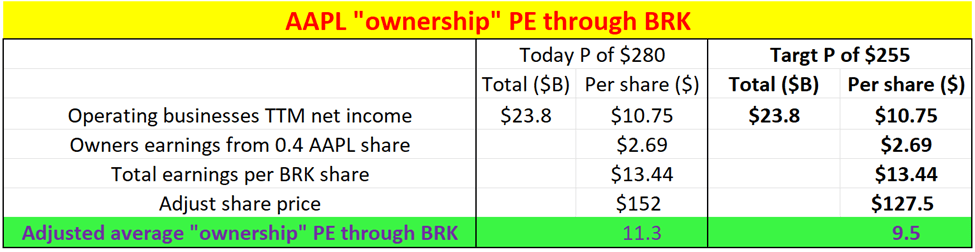

And the next table shows that its valuation is further discounted when owned through BRK. Quick math would show that under the current conditions,

- Each BRK share contains 0.40 AAPL shares.

- As of this writing, BRK’s equity portfolio is worth about $300 billion ($135 per BRK.B share) and $122 billion ($55 per BRK.B share) are invested in AAPL. That is, excluding AAPL, BRK’s equity portfolio is worth about $178B (or $80.5 per BRK.B share).

- And BRK’s cash position is about $105B ($47.5 per BRK.B share).

Based on the above quick facts, if we pay today’s market price of $280 to buy 1 BRK.B share and immediately liquidate the cash and all other equity investments except AAPL, we are essentially paying $152 ($280-$80.5-$47.5 = $152) for 0.40 AAPL shares and all the BRK operating business segments. Also as established before, 0.4 AAPL shares would provide an economic earning of $2.69 (=$6.73×0.4). So in the end, we are paying $152 to buy $2.69 of economic earnings from AAPL PLUS $10.75 of economic earnings from BRK’s operating businesses.

How you do the rest of the valuation is a matter of personal judgment now. If you take the aggregated average as I did in the following table, your average “ownership” PE of AAPL and BRK’s operation business is on average 11.3x. At my $255 limit order price, the average “ownership” PE of AAPL and BRK’s operation business would be in the single digit, about only 9.5x.

Furthermore, at a $255 target price, I would be getting the AAPL shares for free if I am willing to put a valuation of 11.8x OPC or above for BRK’s operating businesses (which is very reasonable in my view given the quality of the businesses). Because at an 11.8x OPC valuation or above, these operating businesses would be worth at least $127 per share by themselves alone (11.8 x $10.75=$127), already equal to or exceeding the adjusted price that I paid.

Author

Final thoughts and risks

As a perpetual bull for BRK and AAPL, my overall view is that there is really no bad time to buy or add their shares. Although occasionally, extreme market movements make sometimes obviously better than others. The thesis is that now is such a time. Due to a combination of market overaction, a delayed update of BRK’s book value, and discrepancies between true earnings vs accounting earnings, BRK is currently valued at only ~1.25x by my estimate, quite close to the Buffett price. At a target price of $255, my estimated valuation would be 1.2x. And such a valuation creates a backdoor to owning AAPL shares at heavily discounted valuations. And my estimated “ownership PE” for AAPL is in the range of 9.5x to free if the target price of $255 is triggered.

Finally, risks. The risks associated with both BRK and AAPL themselves have been thoroughly detailed by other SA authors already and won’t be repeated here. Here, I will focus more on the risks specific to the idea specific to this particular approach of analyses. A few key risks:

- Uncertainties in BRK’s equity portfolio. As aforementioned, the value of BRK’s sizable equity portfolio fluctuates together with the overall market. And the latest data available are those reported as of June 30. As a result, its current BV and future BV when/if the $255 target price is reached are my projections and estimations, which inevitably create some uncertainties in the analysis.

- This analysis assumes BRK’s cash position and equity investment are worth exactly the market price. This is a reasonable assumption given the liquidity of the holdings – they are mostly large mega-cap and large-cap businesses with large trading volumes. However, no one really knows what would actually happen when you try to liquidate $300+ billion worth of stocks. So there are definitely some uncertainties in the math above.

- BRK’s cash position and its insurance float. This analysis also assumed that all the cash positions are truly cash can. However, in reality, this is not entirely true because part of the cash is insurance float and cannot be entirely liquidated as assumed in my thought experiment above. But there are also good reasons to take the cash position out of the stock price (or some part of it). Cash is cash nonetheless – that is, if someone buys BRK completely, every $1 in the float counts as $1. And there is a very low chance – though probably no one, including Buffett himself knows how low the chance is – that all the float will be needed. Buffett mentioned that he will at least maintain a cash position of about $30B. So I am guessing we could use $30B as a minimum for estimating the float. Taking $30B out of the cash will make the valuations a bit higher than what’s presented above, but not by too much.