FTX, Bitcoin, Ethereum Latest:

- Bitcoin (BTC) threatens psychological support as sentiment continues to dwindle

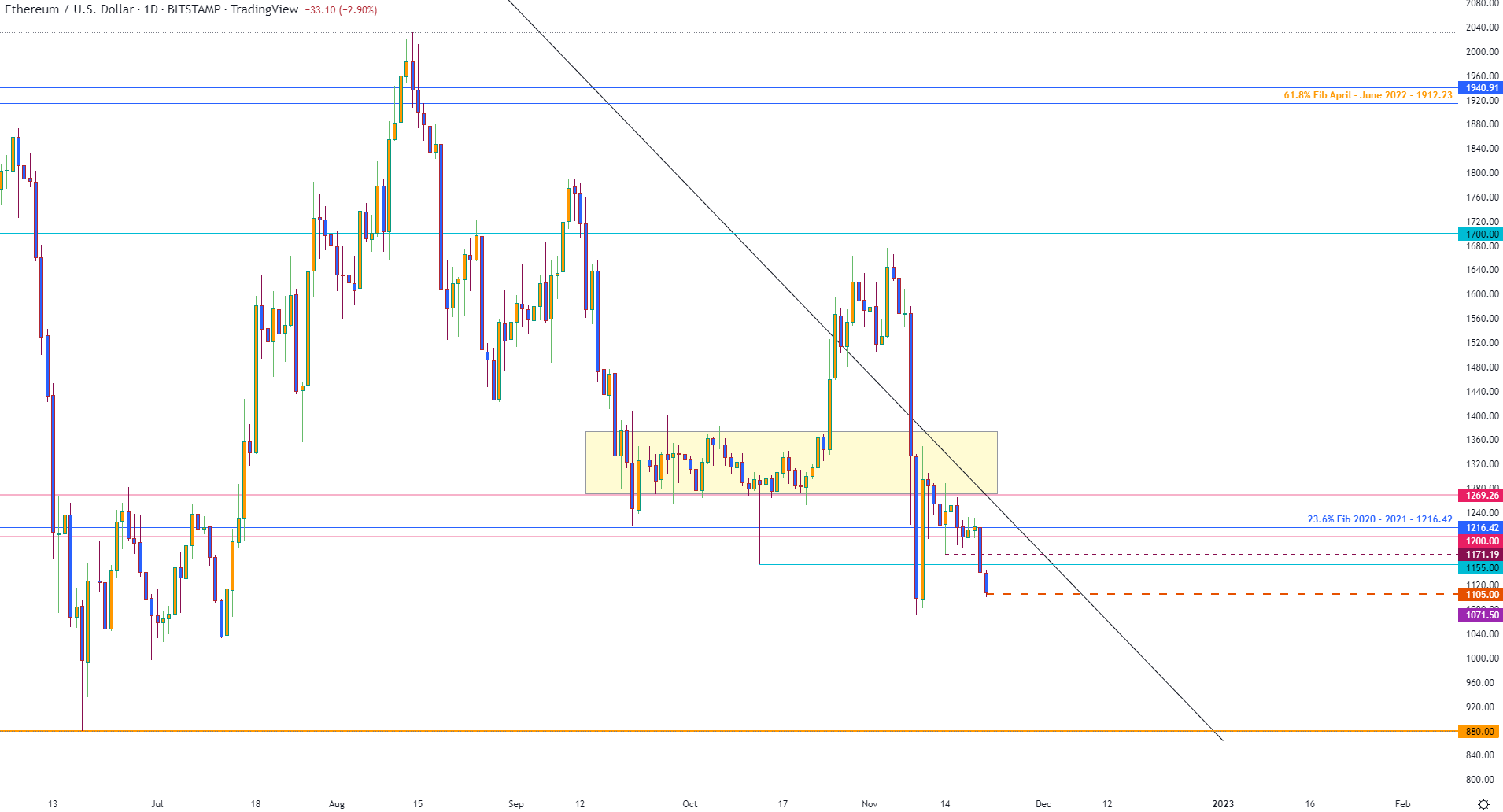

- Ethereum has fallen to another level of Fibonacci support after falling below $1,200

- FTX swindle intensifies as creditors mourn losses

- Grayscale’s Bitcoin Trust enters spotlight after refusing to share proof of reserves

Recommended by Tammy Da Costa

Get Your Free Introduction To Cryptocurrency Trading

During a period of rising interest rates and growing recession risks, cryptocurrency is depreciating at a rapid pace. With Grayscale’s Bitcoin trust now under scrutiny, the FTX contagion has already resulted in Billions of Dollars of losses.

A year after moving the FTX headquarters to the Bahamas and the exchange that was valued at $32Bn at the end of January is now worthless. As the investigation into Sam Bankman-Fried and the collapse of Alameda Research, FTX and its affiliates highlight the risks associated with speculative assets.

While altcoins remain the hardest hit by recent events, Bitcoin and Ethereum remain the leaders of digital assets.

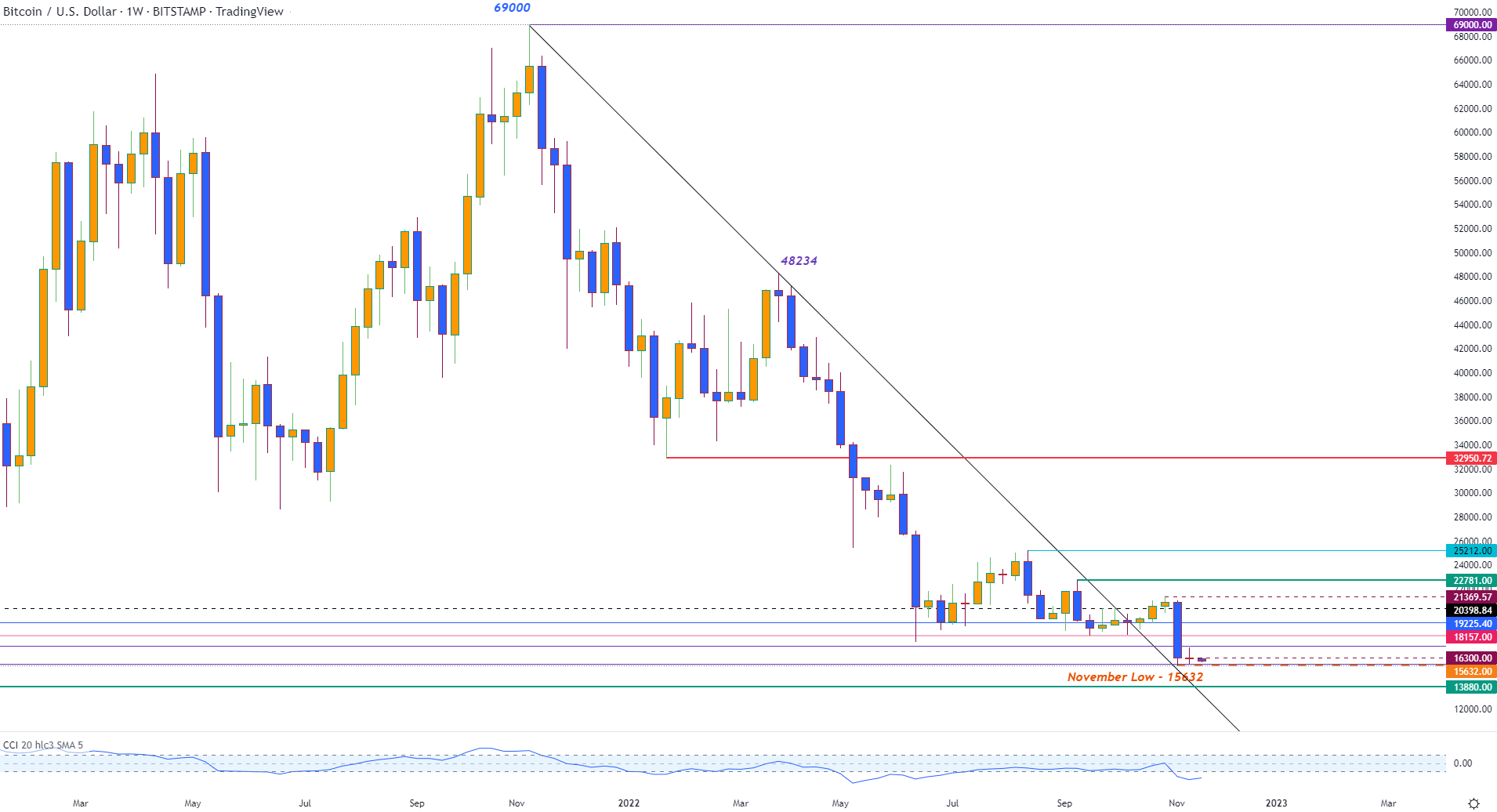

With a doji candle on the weekly chart highlighting an important zone of support, this week’s price action could assist in determining Bitcoin’s next move.

Bitcoin (BTC/USD) Weekly Chart

Chart prepared by Tammy Da Costa using TradingView

After dropping below the $16,000 psychological handle earlier today, a small-bodied candle below resistance at $16,300 has pushed prices into a technically significant range.

As a zone of confluency forms between $15,761 and $17,283, the key Fibonacci levels of the 2017 move continue to provide support and resistance for the imminent move.

Although the weekly CCI (commodity channel index) remains in oversold territory, the current fundamental backdrop could contribute to further declines.

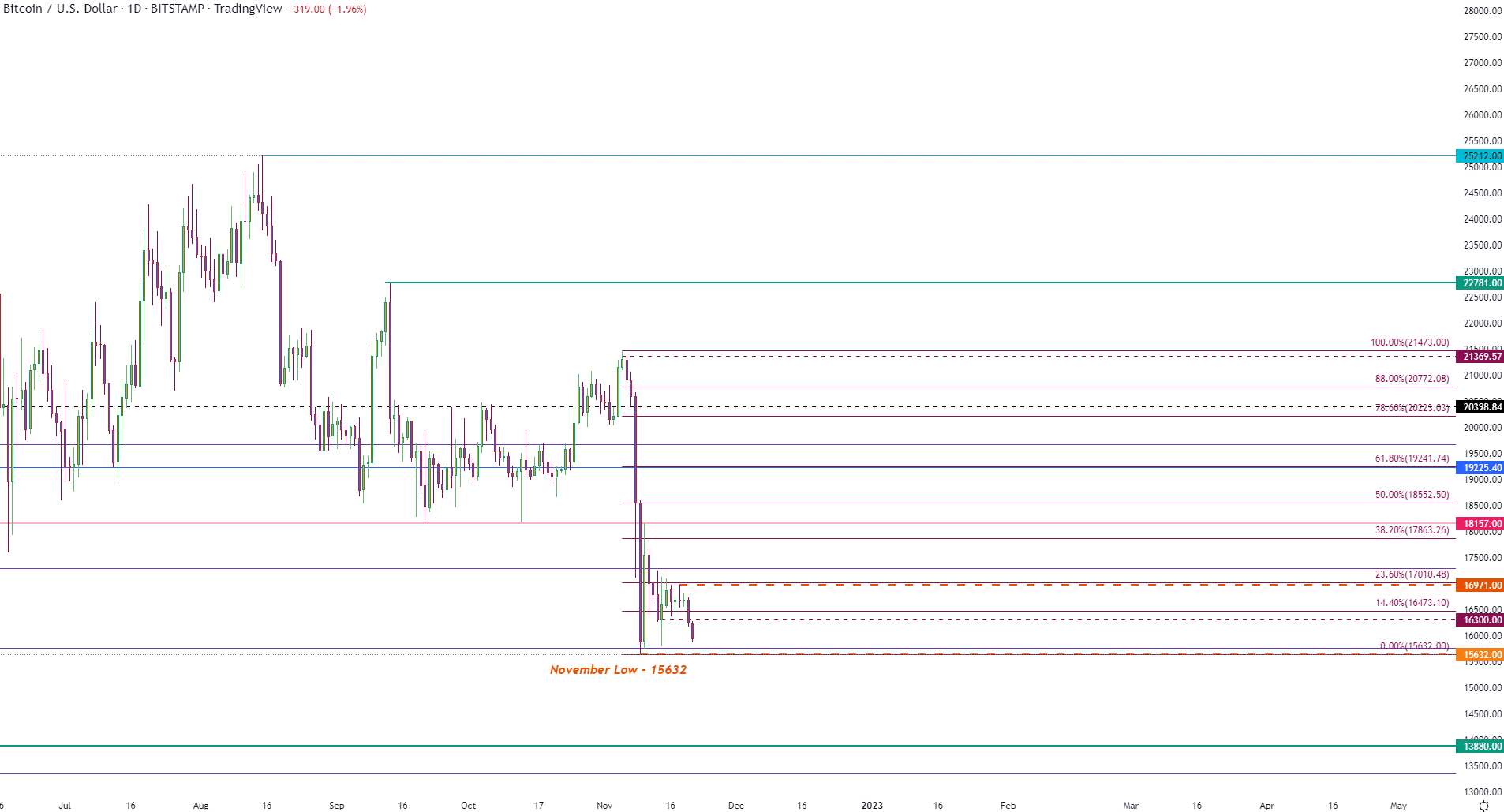

Bitcoin Daily Chart

Chart prepared by Tammy Da Costa using TradingView

Ethereum Daily Chart

— Written by Tammy Da Costa, Analyst for DailyFX.com

Contact and follow Tammy on Twitter: @Tams707